Hopefully by this time we all know about index funds. The idea is that by investing in a large, diversified portfolio, one can enjoy the average return across many assets and avoid their individual risk. Because assets are imperfectly correlated, they don’t always go up and down at the same time or in the same magnitude. The result is that one can avoid idiosyncratic risk – the risk that is specific to individual assets. It’s almost like a free lunch. A major caveat is that there is no way to diversify away the systemic risk – the risk that is common across all assets in the portfolio.

We can avoid the idiosyncratic risk among assets. But, we can also avoid idiosyncratic risk among times. Each moment has its own specific risks that are peculiar to it. Many people think of investing as a matter of timing the market. However, people who try to time the market are actively adopting the specific risks that are associated with the instant of their transaction. This idea seems obvious now that I’m writing it down. But I had a real-world investing experience that– though embarrassing in hindsight – taught me a heuristic for avoiding overconfidence and also drilled into my head the idea of diversifying across time.

I invested a lot into my preferred index fund this past year. I’d get a chunk of money, then I’d turn around and plow it into the fund. What with the Covid rebound, it was an exciting time. I started paying more attention to the fund’s performance, identifying patterns in variance and the magnitude of the irregularly timed and larger changes. In short, by paying attention and looking for patterns, I was fooling myself into believing that I understood the behavior of the fund price.

And it’s *so* embarrassing in hindsight. I’d see the value rise by $10 and then subsequently fall to a net increase of $5. I noticed it happening several times. I acted on it. I transferred funds to my broker, then waited for the seemingly regular decline. Cha-ching! Man, those premium returns felt good. Success!

Silly me. I thought that I understood something. I got another chunk of change that was destined for investing. I saw the $10 rise of my favorite fund and I placed a limit order, ensuring that I’d be ready when the $5 fall arrived. And I waited. A couple weeks passed. “NBD, cycles are irregular”, I told myself. A month passed. And like a guy waiting at the wrong bus stop, my bus never arrived. All the while, the fund price was ultimately going up. I was wrong about the behavior of the fund. Not only did I fail to enjoy the premium of the extra $5 per share. I also missed what turned out to be a $10 per share gain that I would have had if I had simply thrown in my money in the first place, inattentive to the fund’s performance.

Reevaluation

I hate making bad decisions. I can live with myself when I make the right decision and it doesn’t pan out. But if I set myself up for failure through my own discretion, then it hurts me at a deep level. What was my error? Overconfidence is the answer. But why did it hurt me?

Overconfidence was clearly an internal defect. But the market doesn’t care about your internal circumstance. So, while I was overconfident, that wasn’t the means by which I missed out on easy returns. Attempting to purchase at just the right time caused me to adopt time-specific risk. If I had made my purchase willy-nilly, as it were, then I’d have been both confident and better off.

That’s when it occurred to me. By purchasing across many assets, we avoid idiosyncratic risk by asset. But, if we purchase across many times, then we can reduce our idiosyncratic risk by time. Hopefully an example can illustrate.

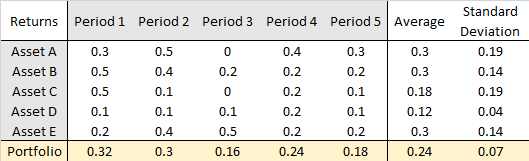

Consider a portfolio of 5 assets across 5 periods. Below is a table that illustrates the conventional way that people consider diversification. The portfolio of assets has the average return, but much less than the average standard deviation. *But*, it assumes that you are, in fact, holding during the 5 periods. Although it’s true that it represents some interval of time, it ignores that, IRL, we have a decision to make about which time interval whose return and standard deviation we will adopt. This is a risky decision! How do we not teach this in corporate or personal finance classes???

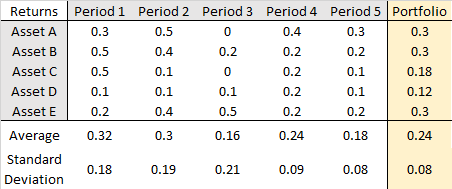

If we switch the axes, then we can see that our portfolio can be considered as including multiple risky time periods rather than multiple risky assets. Each of those time periods has its own average and standard deviation of returns. By holding for multiple periods, we diversify away some of the risk that is associated with individual time periods. The implication is that making small contributions to your portfolio diversifies the times at which you buy. Mathematically, the same average return exists by investing a large chunk of change assigned to a random time period.

As humans we have foibles. Foible #1 is that we think that we understand underlying causation when we see patterns. It can be useful. But our understanding can also be illusory. Foible #2 is that we are bad at identifying random processes. Recognizing patterns is part of how we survive. So, when faced with a stochastic process, we inevitably overlay the pattern that our brain has interpreted.

Always Be Buying

The heuristic that helps us to avoid these two foibles and also helps to diversify away the intertemporal idiosyncratic risk is to always be buying. If you are saving and investing, always be buying so that you can enjoy a little of the good times and avoid a lot of the bad times.

PS. The obvious parallel occurs during retirement. If it weren’t for the fact that our lives are finite, I’d say that we should always be selling. But, c’est la vie.

PPS. Sometimes, like after a crisis, you may really want to adopt that idiosyncratic risk. May the odds be in your favor!

One thought on “Avoiding Intertemporal Idiosyncratic Risk”