There has been a lot of shade thrown at the United Kingdom recently from economists and political scientists. Economic growth has gone down the tubes and there have been six prime ministers over the past decade. As an American, I didn’t really know if that was a lot. The social media says that we’ve had a lot of turnover recently. Is six prime ministers in ten years a lot in the UK’s parliamentary system? I grew up watching Tony Blair on TV for a ten-year stretch. But I had no context for the historical norm or whether there is any precedent. Here I look at the data.

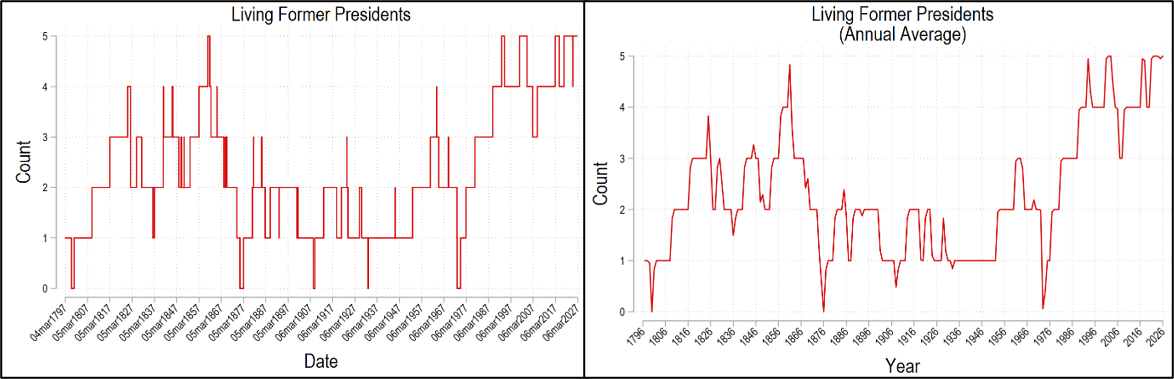

Right now, there are a record number of former prime ministers still living (PM). Prior to the recent spike, the maximum number of living people who had left office was five. Right now in 2026, there that number is nine! And if the current PM, Andy Burnham, follows the recent trend of short stints in office, then they’ll hit ten. As an American, it’s hard for me to imagine having 10 living former presidents. According to the below charts, the British are probably a bit jarred too!

Why So Many?

In last week’s post I noted that we’re tied for the most living former presidents. But truly, the UK’s numbers are what inspired me to look at this topic in the first place. To recap, the number of living ex-executives can be caused by 1) Longer lifespans, 2) Leaving office at a younger age, and 3) More unique executives. In the US, being currently tied for the record is overwhelmingly driven by longer lifespans. What about the UK?

What could be better than creating data so valuable that an institution is happy to host and update it forever, like the Sean Lahman baseball database?

Creating data that sells for $375 million, like the Center for Research in Security Prices. University of Chicago professors assembled this series of finance datasets over decades, starting in 1960 with an effort to track every transaction of every publicly traded security. U Chicago sold CRSP to Morningstar last year for $375 million.

Why could they sell it for so much? It helps to be working in finance, where the willingness to pay is the highest. It also represents 65 years of work from what became a large team that included Nobelists like Eugene Fama. The data was valuable enough to become widely used by key institutions even though CRSP charged for it:

Today, $3 trillion in fund assets are linked to CRSP Market Indexes, including U.S. equity ETFs run by Vanguard, and more than 600 subscribers across 35 countries use CRSP Research Data Products.

Did U Chicago sell CRSP at the right time? On the one hand, I wonder if this was a fire sale driven by federal grant cuts putting pressure on the U Chicago budget. On the other hand, assembling datasets like this is only going to get easier in the age of AI, so perhaps Chicago sold at the top.

For now though there is still an edge in having restricted datasets that AIs haven’t trained on and can’t access. When I ask myself what advantage my human research assistants have over AIs in 2026, the most obvious answer is that they can legally access restricted databases like CRSP or, in my current case, HeinOnline.

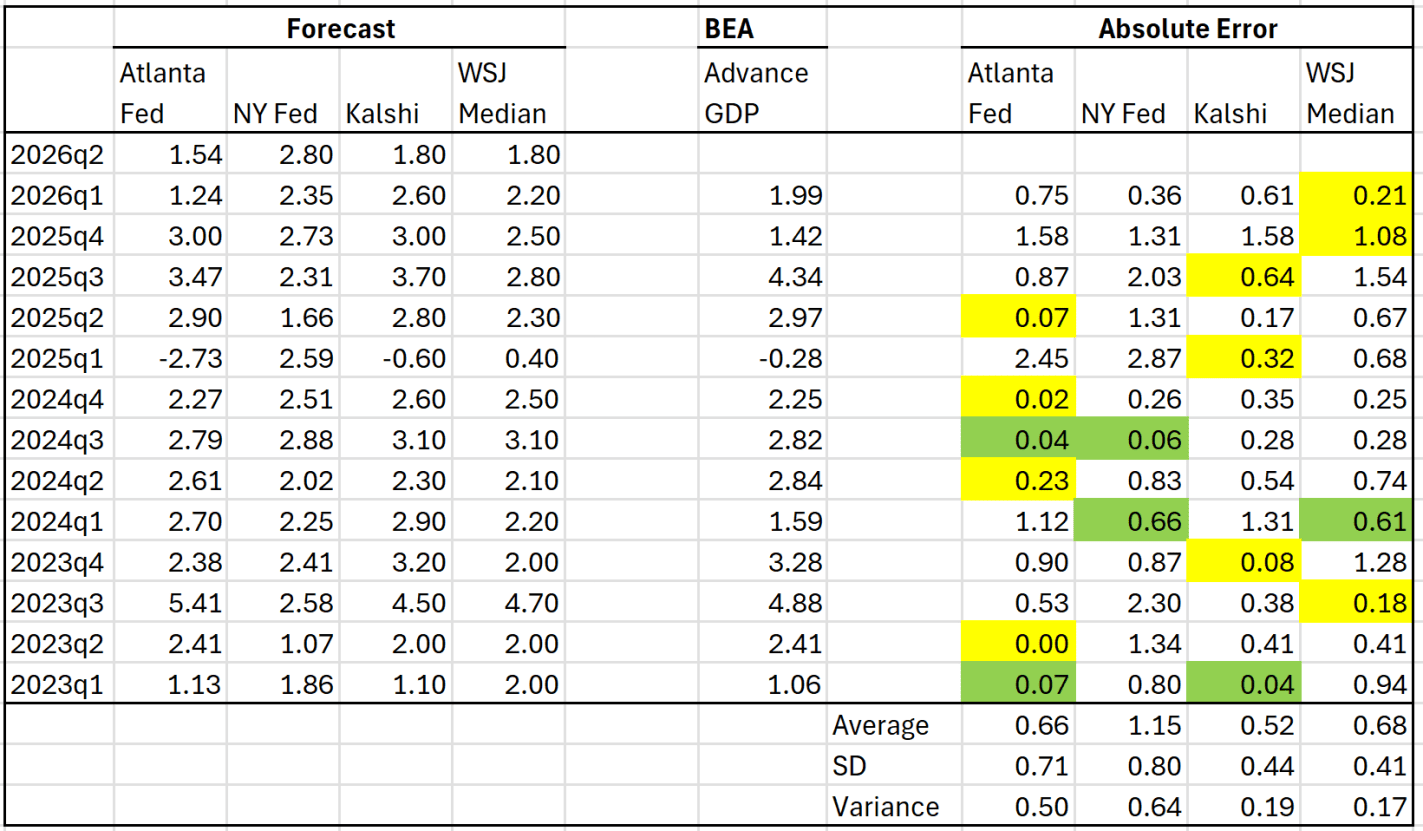

GDP growth data for the second quarter of 2026 comes out tomorrow. As I have been doing for the past several quarters, here is an update on two model forecasts (Atlanta and NY Feds), betting market implied estimates (Kalshi), and an average from a survey of economists (WSJ). Yellow shading indicates which forecast was closest to correct in each quarter (green is if two forecasts were about the same).

In the past two quarters, the WSJ survey has been the best predictor. The Atlanta Fed GDPNow model used to be my favorite, but it has performed pretty poorly in the past 3 quarters. As I have discussed before, an average of the Atlanta Fed and Kalshi was better than any single predictor. I continue to include the NY Fed estimate, even though it seems to be a very terrible predictor, because some people like to talk about it.

The Atlanta Fed, Kalshi, and the WSJ survey are all showing very similar estimates for Q2. If I was a betting man, I would bet on 1.8% for the BEA advance estimate.

If you count president Trump, the number of living former presidents is at a historic high of five (Clinton, G.W. Bush, Obama, Trump, Biden). The number of living ex-presidents can increase for three reasons. 1) More people becoming president, 2) ex-presidents having longer lifespans, and 3) presidents leaving office earlier in life. Why do we have so many right now?

The historical maximum number of people who both 1) leave office and 2) live simultaneously with others is five. It first happened in 1861 when Abraham Lincoln (16th) was president for just under a year before John Tyler (10th) died in 1862. Since then, the number of living ex-presidents has been mostly below four if not below 3. The figures below graph the number of people living who have been US president. The left graph uses daily data and the right uses the annual average (weighted by day).

In fact, besides Washington, we’ve had four other periods when there were ZERO ex-presidents living. The first was under Grant (18th). This changes my perspective of that period. Living ex-presidents provide a sense of continuity – that something from the past continues today. They give us hope that our country will continue into the future. Grant presided over part of the reconstruction era. For part of this presidency, there was no one else who knew how he felt and no living person who had been in his position. What a tenuous time!*

The other presidents who, at some point, had no living predecessors were Theodore Roosevelt (26th), Herbert Hoover (31st), and Richard Nixon (37th). But since 1981, we’ve had three or more living presidents. So, most of us feel like that’s “normal”. Imagine if there was just Trump, and that’s it. That’d feel jarring.

1) Are More People Becoming President?

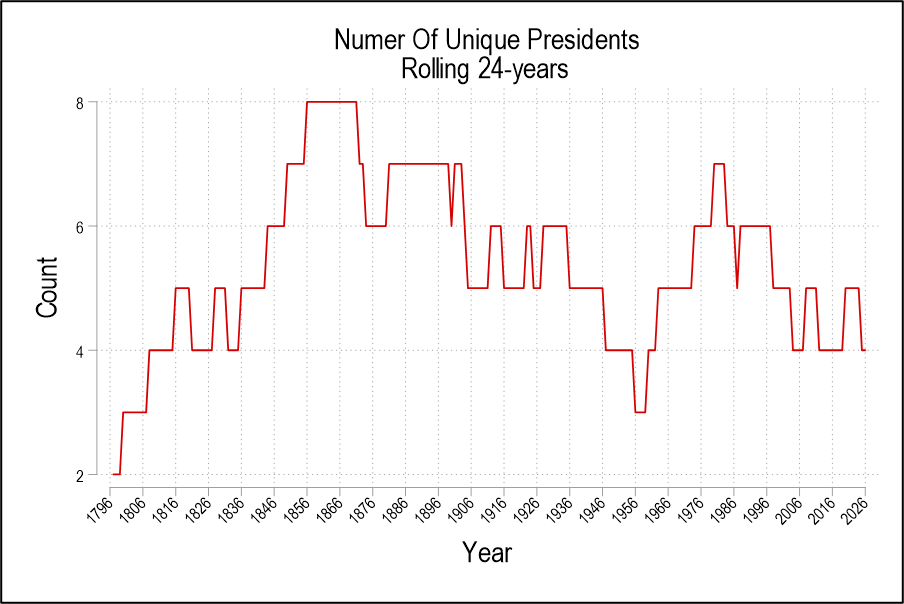

A presidential term is four years and only one president was in office for more than two terms, Franklin Roosevelt (32nd). Let’s take a 24-year trailing average. With 8-year tenures, the least number of presidents is 3. With 4-year tenures, the greatest number of presidents is 6. Assassinations and other deaths of sitting presidents can push the number higher. The graph below is the number of unique people to act as head of state over the prior 24 years (I say ‘unique’ because Cleveland (22nd & 24th) and Trump (45th & 47th) both served two non-consecutive terms).

We can conclude that the number of unique presidents is not exceptionally high at this time. The historical average is about 5.2 unique presidents. We’ve been below that since 1998 owing to a higher proportion of two-term presidents since then. Before Biden (46th), Bush (41st) was the last time that we had a one-term president. So, in terms of executive regimes, the 21st century has been unusually stable. But this stability also places downward pressure on the number of surviving ex-presidents. So, we’ve had many living ex-presidents despite our few regime changes. Reason 1) doesn’t explain why we have so many living ex-presidents now.

The Lahman Baseball Database offers player- and team-level stats all the way back to 1871 as freely downloadable files. It includes over 20,000 players and has been cited by 192 academic papers. That sounds like something that takes an enormous amount of effort to put together, but it seems to have been compiled by just one guy, journalist Sean Lahman.

This looks like yet another example of a lone individual outperforming the huge, well-funded institutions you might expect to compile such datasets- this time not the government but MLB, ESPN, et c.

Sean Lahman has graciously agreed to donate the Lahman Baseball Database, an open source collection of historical baseball statistics, to SABR.

The Lahman Baseball Database — which Lahman created in 1996 and has made freely available online every year since then — contains complete batting and pitching statistics back to 1871, plus fielding statistics, standings, team stats, managerial records, postseason data, and more. While Lahman and others had previously released smaller datasets online, his database allowed researchers to perform complex queries across the entire history of the game for the first time. The Lahman Baseball Database has served as the foundation for many popular baseball research projects and simulation games, including Out of the Park Baseball and Baseball Mogul.

SABR plans to continue to update the database and make it available for free online every year at SABR.org/lahman-database.

I can only hope more of us will compile datasets worth handing off to an institution that will keep updating them.

Claude Fable is Anthropic’s most capable publicly available “Mythos-class” model. It is optimized for long-running autonomous tasks and deep knowledge work. The roll out of this product has been dramatic. Little people like me have access to it for only two weeks, and I doubt I will be able to afford it thereafter. With my window of access, I posed it the following prompt:

“This article indicates that a much smarter model might not be possible because the universe is opaque. Since Tyler Cowen made this statement, AI has helped people make breakthroughs in math and biology. Write this again in 2026 using the latest state of technology. Is the smartest LLM today much smarter than GPT-4? And is the universe legible?” and I copied in my blog post Is the Universe Legible to Intelligence?

One line from Fable’s response: “Notice where the wins clustered: mathematics with checkable proofs, protein structures with experimental ground truth, contest problems with known answers. These are the maximally legible domains — places with a fixed target and a way to verify that you hit it.”

The writing is coherent and contains no obvious hallucinations. Is the answer true, and does it tell the whole truth?

Whenever you read something think about who wrote it, and keep in mind that every author/model has a bias and limitations. In my paper with Will Hickman, we found that just reminding people that a paragraph has an author (whether the author is human or AI) increased the demand for fact checking from readers. LLMs will become more persuasive and closer to (but never completely) correct. Keep reading all things with some skepticism whether they are written by scientists, politicians, or AI.

Regardless, there is definitely such a thing as making the known world more legible to AI today. Thus, people are talking about increasing funding for data availability and the possible demise of the “research paper.”

One of my strongest AI/research takes is that it dramatically increases the value of building new descriptive datasets, digitizing archives etc.

Analysis might be free now, but Fable can’t deduce historical city sewer budgets from first principles. https://t.co/PiJngivhqK

Research papers are more like stories than facts. The demand for stories is not going away, but I definitely cannot predict the future of the write-for-pay scientist.

AI, potentially, could go and get its own new data, instead of waiting for humans to archive it. Thus, the self-improving AI might take us beyond the current models… unless they run up against something that is not legible to intelligence…

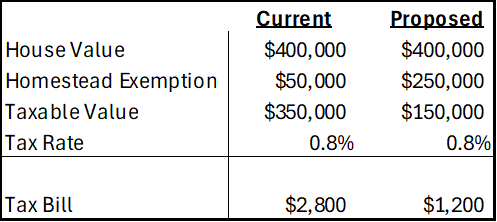

Voters this November will face a proposed amendment to the Florida state constitution on property tax reform. Currently, Florida has what’s called a ‘homestead’ exemption of $50,000. If a residential property is your primary residence, then your home’s assessed value is $50k less before taxes are calculated. There is no exemption for rental property or 2nd homes or vacation homes. The proposed amendment increases the exemption to $250k by 2028 and then indexes it to inflation.

First, let’s get an idea of the magnitudes. The median home in Florida is priced at about $400k and the average property tax rate is around 0.8%. Below compares the current consolidated tax bill against that of the proposed amendment. Given current home prices and local tax rates, the new exemption would have a huge impact on municipal governments who get the bulk of their revenue from property tax. In fact, there is no Florida state property tax, so the proposed amendment would adopt a new rule for municipalities and not the state government.

What Motivates the Amendment?

The current homestead exemption of $50k was established in 2008. A subsequent amendment in 2024 allowed half of that to be indexed to CPI-U. The average home price in Florida has risen 114% since 2008 and 84% since 2020. That’s a lot faster than inflation, but the tax burden is partially offset by a maximum of 3% annual increase in assessed value. Regardless, many individuals face a larger tax bill over time even independent of whether their income or use of public services has changed. Plenty people are feeling the squeeze.

What’s the Purpose of the Homestead Exemption?

The exemption is available for primary residences only. That means that rentals and vacation homes do not qualify. It’s important to keep in mind that, given some total revenue, every tax break for one group or activity implies a higher tax rate for others. So, clearly, the effect is to tax residents less and tax seasonal residents and visitors more. Florida doesn’t have an income tax, but it does have a sales tax, gasoline tax, and others that are disproportionately borne by non-residents. Given that higher income individuals tend to have higher home values, the homestead exemption is a way to lower the tax burden of lower income households. Obviously, the lowest income individuals are renters, but so are non-residents who Florida prefers to tax.

The Economics

Homeowners

The exemption is enjoyed by all primary residences, but helps low income owners the most. And, given a stable amount of municipal tax revenue, a higher homestead exemption requires that municipalities replace that revenue. This might take the form of higher local fees and taxes, making life harder for lower income people to, say, own a car or make purchase if taxes on those activities rise. Revenue stability might also be helped by higher property tax rates. The higher the property value is above $250k, the greater the average tax burden that is borne. So, someone with a very high property value may find themselves with an even higher property tax bill after municipalities adjust to the proposed statewide rule. In this sense, the new amendment would be a step in the direction of tax progressivity (a higher proportion taxed from those with higher income/wealth).

Indexing

Normally, I am in favor of indexing nominal values to CPI. In this case, we need to think about what the goal is. Let’s assume that the goals is to provide relief to lower income homeowners specifically and all primary residence homeowners generally. Does indexing to the CPI help? It depends!

My post and chart from last week showed the phenomenal growth of average income in the US since the Founding. Using GDP per capita historical estimates and adjusting for inflation, this figure is about 46 times greater today than right around the time we declared independence.

It will probably not surprise you that some folks were skeptical. Could this really be true? Two major objections were raised to using GDP per capita. First, wouldn’t it be better to use a median income value rather than a mean (simple average)? Second, wouldn’t a measure of wages be better than GDP per capita?

I really would like to show you an annual series of median income data back to 1776, but unfortunately it just doesn’t exist. Good median income data are hard to find much before the 1950s, much less the 1770s. However, while median values are often better for showing levels, the growth rates of median wages and mean wages aren’t that different for periods when we have comparable data. Consider the following chart, which compares median wages (as calculated by EPI using CPS data) and mean wages (from BLS’s series for non-supervisory workers) since 1973. I have stated these in nominal terms, so don’t take this as real growth rates, but rather it is a raw comparison of two series (we could apply the same inflation adjustment to both, but that won’t change the picture, only the numbers).

Median wages increased by 667% and mean wages increased by 657%, almost identical. Again, these aren’t inflation adjusted, but that’s not the point of this exercise. The point is that whether you use mean or median wages, at least since 1973, the growth rates are the same. Was this true if we went back another 200 years? We can’t say for sure. But many people have this same skepticism about mean wages in recent decades. I think it is better to use median values when you have them, but we shouldn’t throw up our hands and claim we know nothing if all we have is mean wages.

Next, consider the following chart. It begins in 1790, but instead of using GDP per capita, as I did last week, it uses a measure of average wages from economic historian Lawrence Officer. This measure is for “production workers in manufacturing,” and it is a total compensation measure, meaning that it will include the value of fringe benefits as well — though these aren’t noticeable in the data until the 1930s. This is still an average value, but because it is for manufacturing laborers, it won’t be distorted by the wages of managers and owners in that industry, and it won’t be affected by the growth of new industries that might require more years of education (indeed, manufacturing wages are lowering than overall average wages today, so this is taking the hard case). I have also included a second line, which only includes manufacturing wages (not benefits) that I have blended with Officer’s compensation series starting in the 1930s, in case you think including benefits is somehow “cheating.” (Note the log scale again, as in last week’s chart.)

The trends here are very much in the ballpark from the GDP per capita chart I created last week. Using total compensation, wages are 65 times higher than in 1790. Using only wages, they are 49 times higher. Notice that these are both better than the 46 times multiplier using GDP per capita. How is that possible, since I am using the same price deflator in both cases? First, average hours of work have fallen significantly since the 18th century, so incomes haven’t risen quite as much as wages. Second, there was a bit of a decline in GDP per capita during the Revolutionary War, and if we use 1790 as the baseline for GDP per capita, the multiplier is 63. But again, these numbers are all in the ballpark: whether the true figure for a typical American is 46x, 49x, 63x, or 65x, this is a tremendous amount of economic growth.

If you want to look at that chart pessimistically, you will see that there is some reduction in growth rates in the past few decades. That’s true whether we use wages or compensation. This is a well known issue, and has been discussed endlessly in academic papers and on social media. I don’t want to glaze over it here, but I mostly will: the long-run trend of growth in the US is amazing. That’s true whether you use GDP per capita, or wages or compensation for production workers.

So once again, Happy 250th Birthday to the USA and all of you living in the wake of that amazing 250 years of economic growth!

We celebrate 250 years since the Declaration of Independence was signed on July 4th, 1776. That’s the day that we celebrate our country’s birth. So, it’s very American of us to celebrate the day that we merely declared independence (not the day that the revolutionary war ended). We simply said we were independent from the crown. Regardless, we celebrate 250 years as a people. BUT, our government is only 237 years old. The current constitution replaced the articles of confederation in 1789. So there are some caveats to the whole semiquincentennial thing.

An important distinction that is baked into the American pie is that we are not our government. Our government is younger than we are. Our government has a piggy bank called ‘US Treasury’. It can spend and borrow for the US national government. It can also impose tax liabilities on the population in order to service those outlays. Now that it’s the government’s 237th birthday, what’s its basic financial track record?

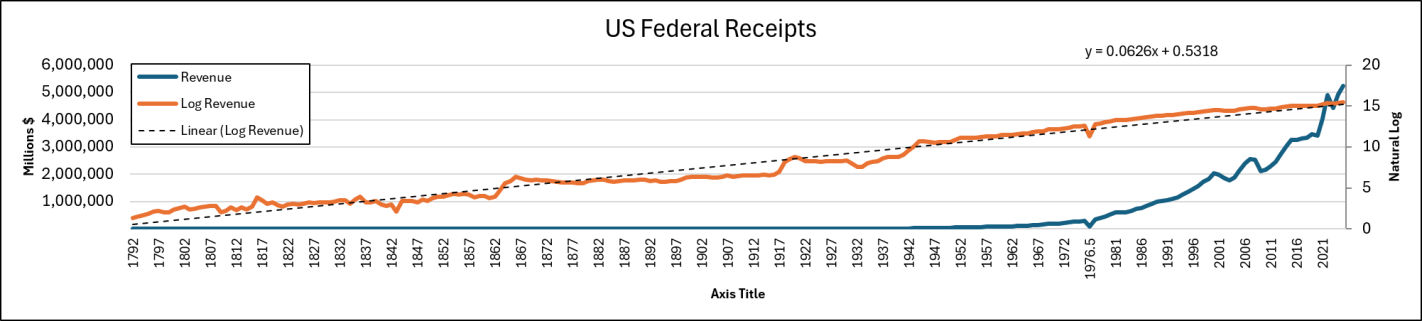

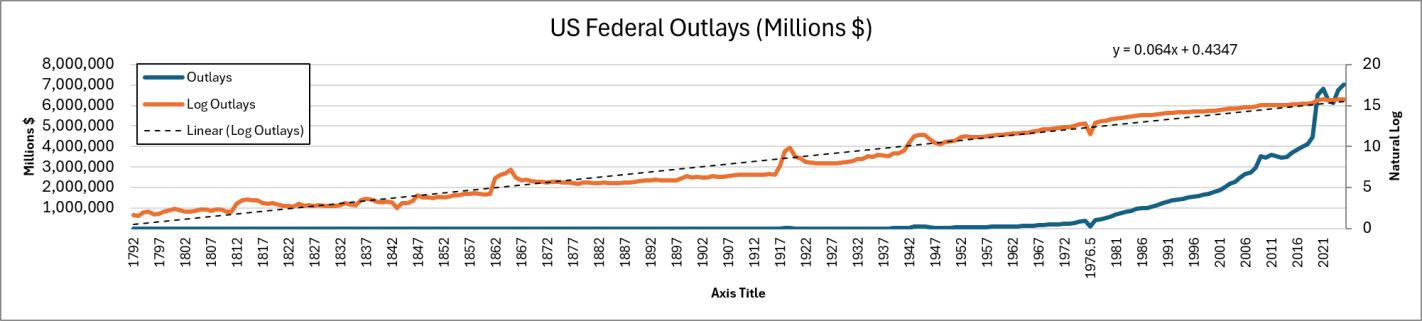

I like to think in the long run, for better or for worse, and I don’t like to get hysterical. So, let’s look at the full span of the 237 years – well – 235 years. The oldest annual data that we have is from Bicentennial Historical Statistics, which goes back to 1792. Below are the series for Federal Receipts and Outlays (revenue and spending).

The blue line is in nominal dollars and the orange line is the natural log so that we can see the changes in growth rates more easily. These aren’t inflation adjusted numbers, so we should expect to see some inflationary patterns. Long-run inflation was pretty stable prior to the 1913 Federal Reserve act and wee can see that reflected in both series. There was some drift upward in terms of revenue and expenditures. But the primary pattern was one of punctuated rises followed by plateaus. That’s a pretty standard ratcheting leviathan pattern. There’s a bump up for the big events in the first half of our history: the War of 1812, Civil War in 1861, and World War I in 1917.

Then, after the great depression and leaving the gold standard (mostly), in about 1933 a new and positive trend in cash flows began. In fact, it’s amazing how consistent the raw nominal series is. We can see where World War II is in the series, but after that we appear to have traded punctuated increases for steady increases. Even the higher inflation rates of the 1970s look pretty muted and on trend (Btw, the blip in 1976 is a record-keeping artifact. There was a 3 month gap-period when the US government changed its fiscal year start/end). Even the new growth in total cashflows seems to be slightly bending downward and growing a little more slowly.

But rest assured, spending has exceeded revenues. Below is the long run deficit. I don’t take the log for this one since there are negative numbers. It’s hard to tell from the line graph, but the first big and persist swing in the deficit arrived after the Fed was established and the onset of WWI. The deficit hit $9 billion in 1918, which was 10x the prior peak of $0.9 billion at the end of the civil war in 1865. Notice that the above government revenues stayed flat or fell after 1920, but the outlays began trending upward before the revenues. The deficit doesn’t really start its long, steady march until 1932. Of course, for the past quarter century, the national government has been in a deficit mess (even if you measure the proportion of GDP).