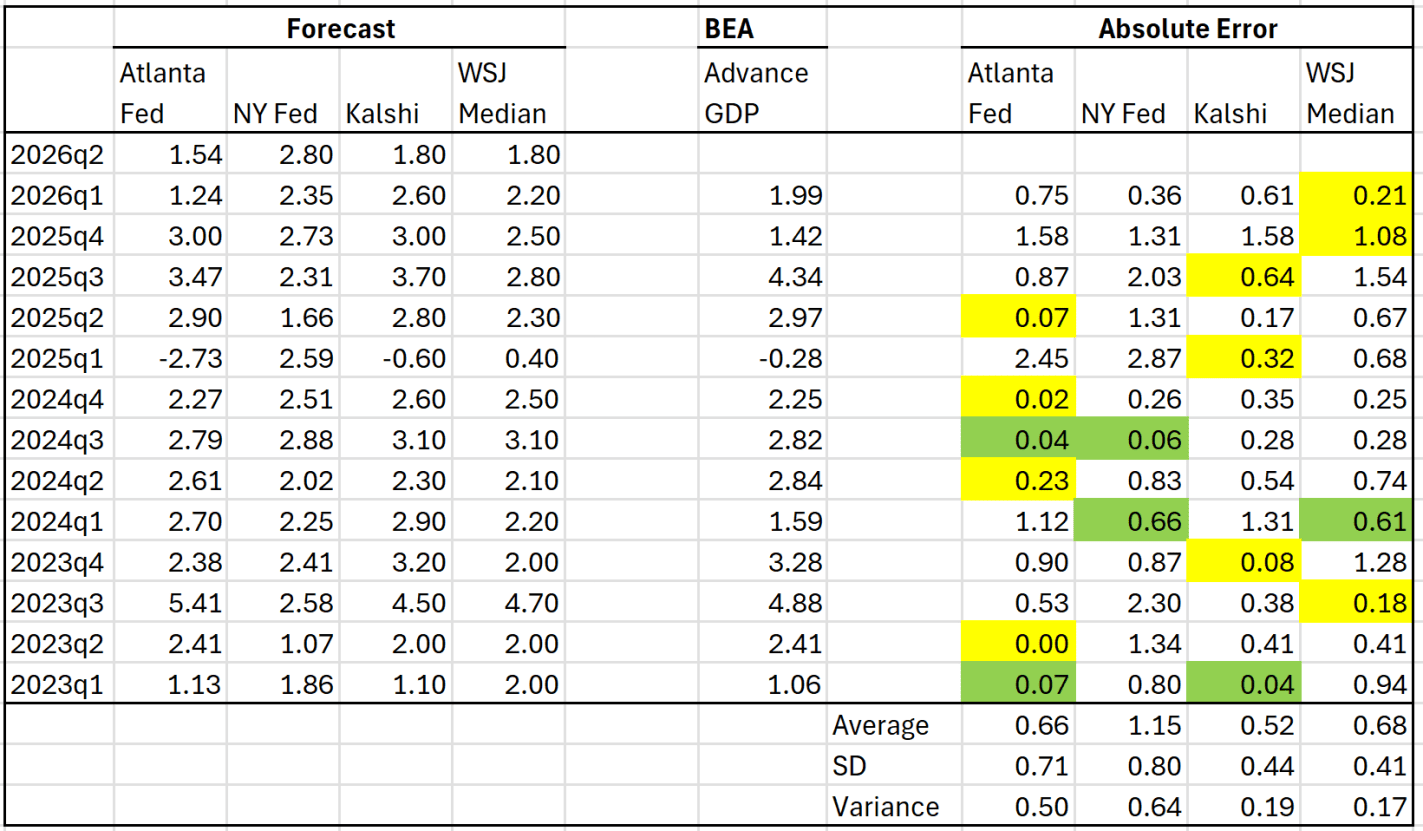

GDP growth data for the second quarter of 2026 comes out tomorrow. As I have been doing for the past several quarters, here is an update on two model forecasts (Atlanta and NY Feds), betting market implied estimates (Kalshi), and an average from a survey of economists (WSJ). Yellow shading indicates which forecast was closest to correct in each quarter (green is if two forecasts were about the same).

In the past two quarters, the WSJ survey has been the best predictor. The Atlanta Fed GDPNow model used to be my favorite, but it has performed pretty poorly in the past 3 quarters. As I have discussed before, an average of the Atlanta Fed and Kalshi was better than any single predictor. I continue to include the NY Fed estimate, even though it seems to be a very terrible predictor, because some people like to talk about it.

The Atlanta Fed, Kalshi, and the WSJ survey are all showing very similar estimates for Q2. If I was a betting man, I would bet on 1.8% for the BEA advance estimate.

I have a new essay up at Human Progress today. Here’s a slice of it:

The productivity slowdown is not an immutable law of nature. It is, at least in part, the consequence of policy choices. Human ingenuity remains as powerful as ever. We have more scientists, more capital, and better tools than any previous generation. The challenge is not generating ideas; it is allowing those ideas to spread.

…

An additional one or two percentage points of annual productivity growth may sound insignificant. Yet when compounded over decades, the effects are transformative. Higher productivity means higher incomes, better health outcomes, more abundant energy, and greater opportunities for future generations. The ideas already exist. The question is whether we will allow them to flourish.

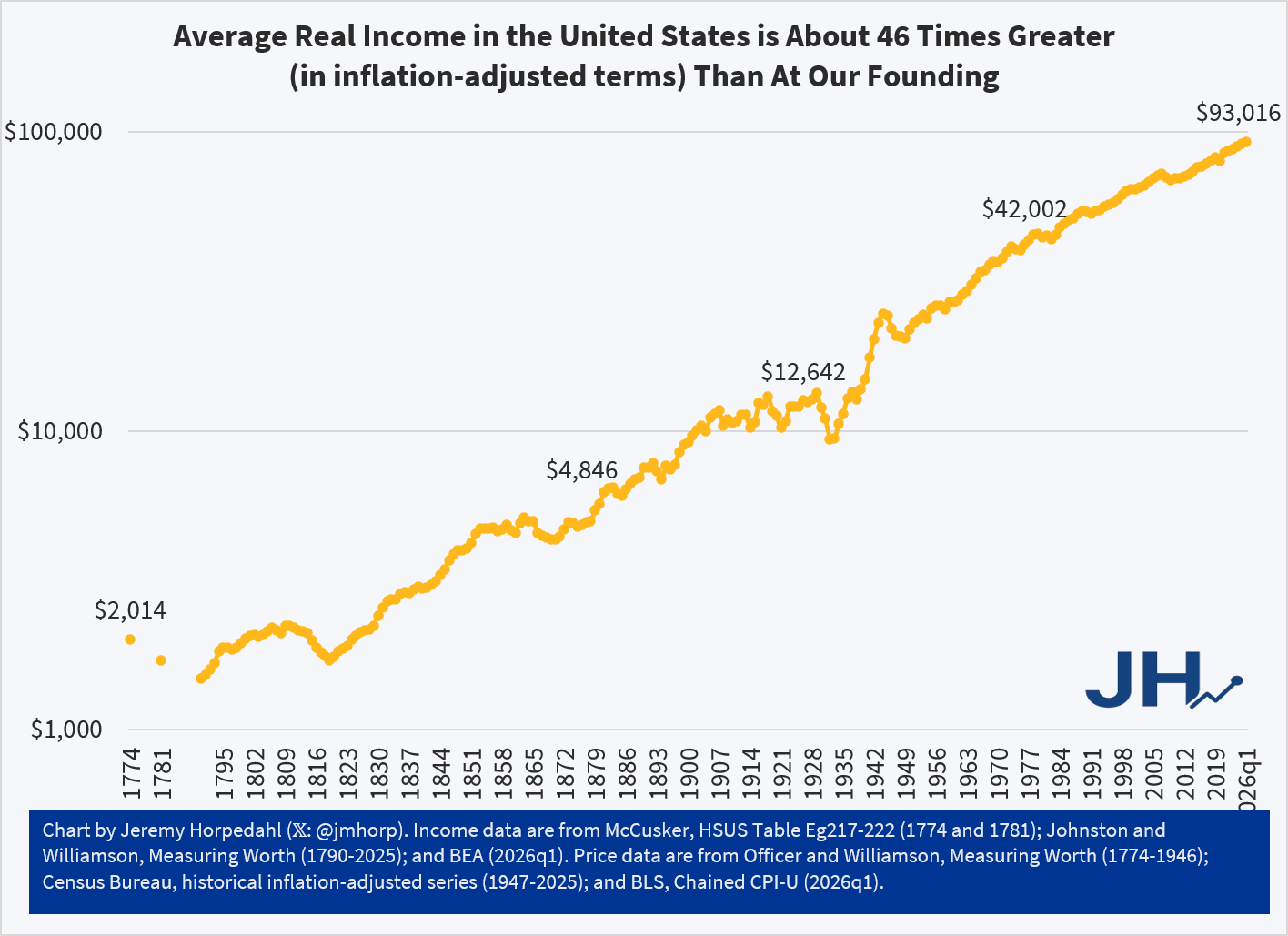

My post and chart from last week showed the phenomenal growth of average income in the US since the Founding. Using GDP per capita historical estimates and adjusting for inflation, this figure is about 46 times greater today than right around the time we declared independence.

It will probably not surprise you that some folks were skeptical. Could this really be true? Two major objections were raised to using GDP per capita. First, wouldn’t it be better to use a median income value rather than a mean (simple average)? Second, wouldn’t a measure of wages be better than GDP per capita?

I really would like to show you an annual series of median income data back to 1776, but unfortunately it just doesn’t exist. Good median income data are hard to find much before the 1950s, much less the 1770s. However, while median values are often better for showing levels, the growth rates of median wages and mean wages aren’t that different for periods when we have comparable data. Consider the following chart, which compares median wages (as calculated by EPI using CPS data) and mean wages (from BLS’s series for non-supervisory workers) since 1973. I have stated these in nominal terms, so don’t take this as real growth rates, but rather it is a raw comparison of two series (we could apply the same inflation adjustment to both, but that won’t change the picture, only the numbers).

Median wages increased by 667% and mean wages increased by 657%, almost identical. Again, these aren’t inflation adjusted, but that’s not the point of this exercise. The point is that whether you use mean or median wages, at least since 1973, the growth rates are the same. Was this true if we went back another 200 years? We can’t say for sure. But many people have this same skepticism about mean wages in recent decades. I think it is better to use median values when you have them, but we shouldn’t throw up our hands and claim we know nothing if all we have is mean wages.

Next, consider the following chart. It begins in 1790, but instead of using GDP per capita, as I did last week, it uses a measure of average wages from economic historian Lawrence Officer. This measure is for “production workers in manufacturing,” and it is a total compensation measure, meaning that it will include the value of fringe benefits as well — though these aren’t noticeable in the data until the 1930s. This is still an average value, but because it is for manufacturing laborers, it won’t be distorted by the wages of managers and owners in that industry, and it won’t be affected by the growth of new industries that might require more years of education (indeed, manufacturing wages are lowering than overall average wages today, so this is taking the hard case). I have also included a second line, which only includes manufacturing wages (not benefits) that I have blended with Officer’s compensation series starting in the 1930s, in case you think including benefits is somehow “cheating.” (Note the log scale again, as in last week’s chart.)

The trends here are very much in the ballpark from the GDP per capita chart I created last week. Using total compensation, wages are 65 times higher than in 1790. Using only wages, they are 49 times higher. Notice that these are both better than the 46 times multiplier using GDP per capita. How is that possible, since I am using the same price deflator in both cases? First, average hours of work have fallen significantly since the 18th century, so incomes haven’t risen quite as much as wages. Second, there was a bit of a decline in GDP per capita during the Revolutionary War, and if we use 1790 as the baseline for GDP per capita, the multiplier is 63. But again, these numbers are all in the ballpark: whether the true figure for a typical American is 46x, 49x, 63x, or 65x, this is a tremendous amount of economic growth.

If you want to look at that chart pessimistically, you will see that there is some reduction in growth rates in the past few decades. That’s true whether we use wages or compensation. This is a well known issue, and has been discussed endlessly in academic papers and on social media. I don’t want to glaze over it here, but I mostly will: the long-run trend of growth in the US is amazing. That’s true whether you use GDP per capita, or wages or compensation for production workers.

So once again, Happy 250th Birthday to the USA and all of you living in the wake of that amazing 250 years of economic growth!

For America’s 250th birthday, my present to all of you is this chart showing our economic history. Average income in the US has increased dramatically since the country was founded. This chart attempts to provide one, continuous series, using the best available income data and inflation adjustments (well, mostly continuous — before 1790 there are just a few estimates). Sources are listed at the bottom of the chart. The y-axis is a log scale.

The Atlantic has a great article about the history of the Boeing 747 aircraft, which is slowly being retired by airlines. Lots of fun details in the article about the plane itself and about that era. The author is also conscious of the fact that flying was expensive back then, and that a lot more people fly today (though in part, the 747 was a cause of mass flying). Still, the tone of the article is nostalgic for the era, in addition to just being a nice obituary for a marvel of engineering and luxury.

But just how much more expensive was flying when the 747 was introduced? The article doesn’t exactly tell us, though they do give some inflation-adjusted figures on the cost of building the planes. They do give us some hint of how luxurious flying was, even in coach: “on a 1970 Pan Am flight from JFK to Heathrow, a coach-class passenger would have enjoyed filet mignon.”

Sounds nice! But expensive. In 1970, a roundtrip flight on Pan Am from New York to London was $420. First class was $750. To put those numbers in context, the average wage in 1970 was $3.40, meaning it would have taken 124 hours of work to buy the coach ticket, and 221 hours to buy the first class ticket. The average wage today is $32.31, meaning that the coach ticket is the equivalent of almost $4,000 today, and the first class ticket is over $7,000. Filet mignon is nice, but not $4,000 nice.

Today, you can buy a coach ticket from New York to London for around $800. Of course, there is no one single price today, as there was in 1970 (something that frustrates buyers, to be sure), but I’ve searched multiple websites in different months, and you can generally get a direct flight for around $800 in economy class (often cheaper if you don’t have a direct flight). Today most airlines have multiple upper classes for international flights, not a single first class, but on American Airlines you can generally get a business class ticket to London for around $4,000 and a first class ticket for a bit over $5,000 (both direct flights from NYC).

In other words, for the same amount of work as buying one coach ticket in 1970, you could buy five tickets in 2026. Or, if you desire that luxury, you could also buy one business class ticket today, for roughly the same amount of hours worked as the coach ticket in 1970. Business class seats today take about half the hours of work as a first class seat in 1970, and an international first-class ticket today takes about 75% of the hours worked in 1970 as a first class ticket (American Airlines Flagship First class is a truly luxury experience, probably better than 1970, even though there is no piano bar on the plane).

The decline is much smaller than the decline for coach seats, but it is still a decline. But that is an important point: the biggest gains from deregulation and competition in air travel and the non-rich, who mostly weren’t flying anyway. Is the experience as good as 1970? Of course not, and The Atlantic article stresses this point repeatedly. You won’t get filet mignon, you’ll probably be in a cramped seat, with a frustrated flight attendant. But you can afford it, which for most middle-class families is probably the most important fact.

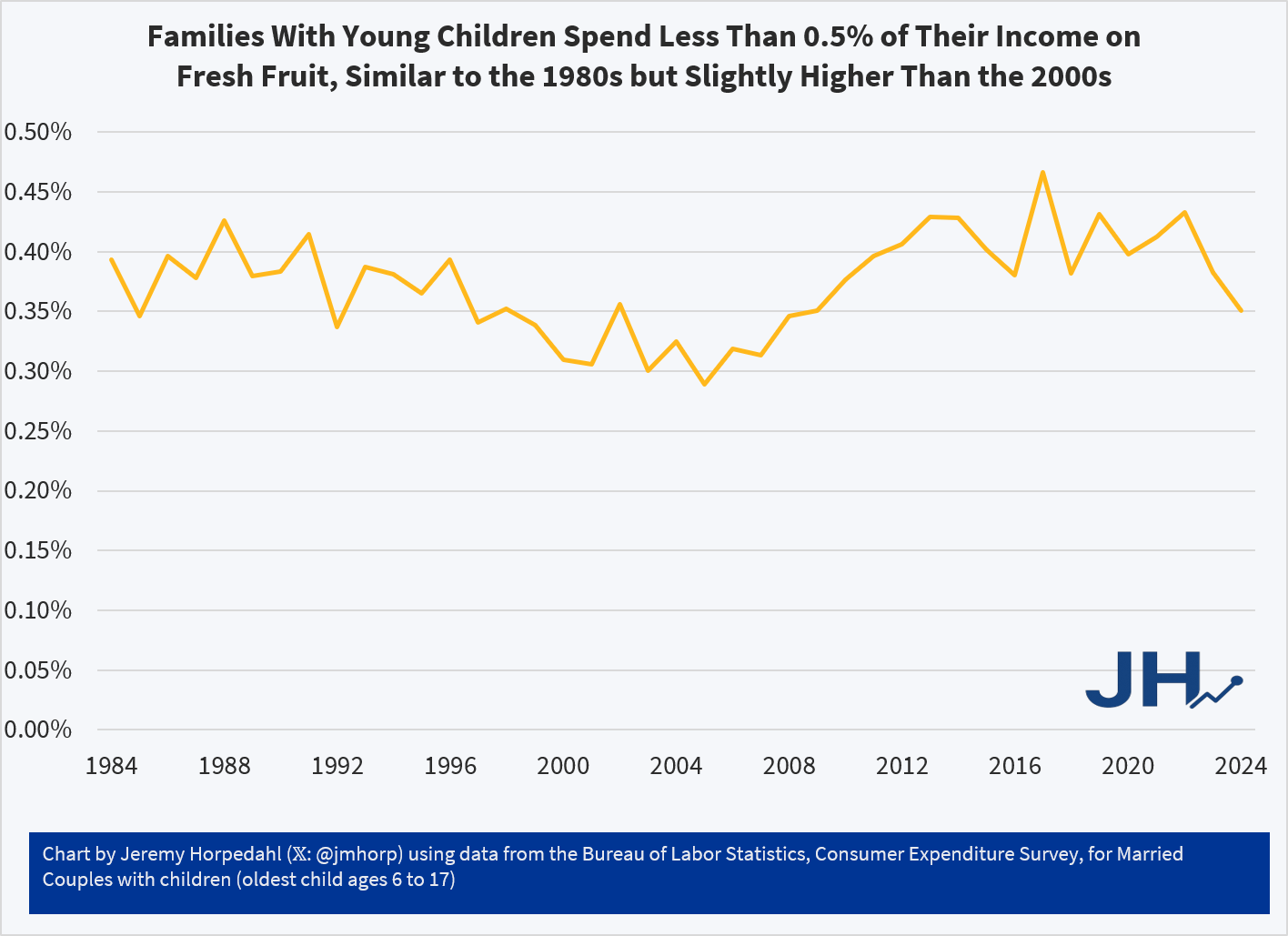

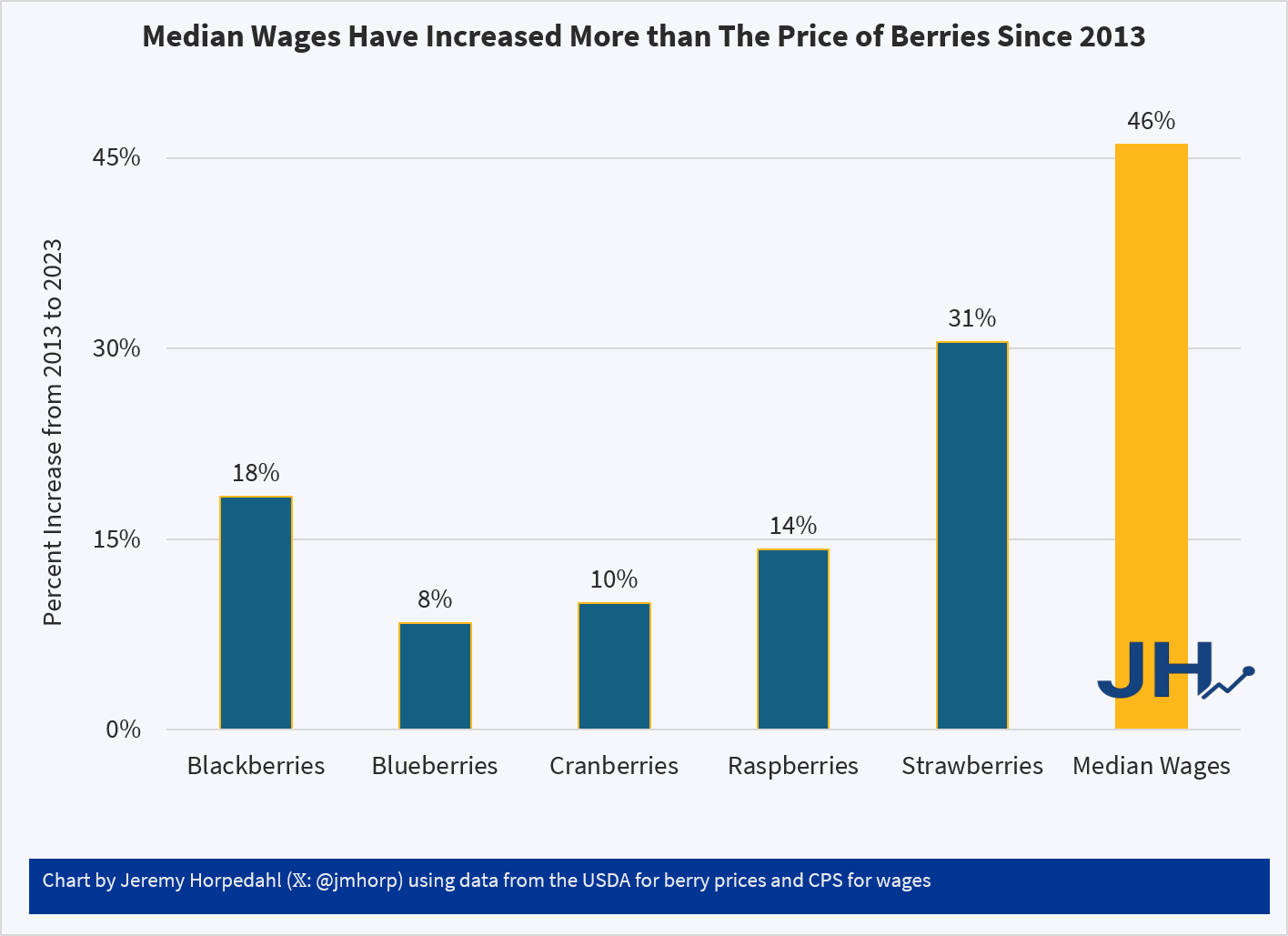

The Washington Post recently ran a fun, data-filled article on berry consumption and parenting. Lots of good tidbits in the article, including that Americans eat a lot more berries than in the recent past, and that a lot of the availability is thanks to foreign trade and imports. But despite being somewhat light-hearted, the article does seem very negative, especially in the title and introduction, about how parents are spending a lot of money on berries.

First things first, are berries breaking the budget for parents? Probably not. While the Consumer Expenditure Survey doesn’t give us data on specific types of berry spending, the broader category of Fresh Fruits is a very small share of consumer spending. It has pretty consistently consumed between 0.30% and 0.45% of income for families with children over the past 4 decades. That’s less than $1 out of every $200 of income. True, there has been a slight rise since over the past 20 years or so, but this is still a small share of the budget.

On average, families with children are spending around $600 per year on Fresh Fruit. And that’s all fruit, not just berries! Just a little over $10 per week. But even for an item that families spend a small share of their income on, such as eggs, perhaps the fact that prices have increased so much recently makes families stand up and notice. Berry spending might seem out of control, even if it’s a small share of income.

What does the price data on berries show? My usual source on this the BLS average price data that forms the basis for the CPI, but they only publicly publishes a series for strawberries, not the other famous berries (blueberries, raspberries, etc.). There is one chart on prices in the WaPo article, but it only compares strawberries to bananas over time (they got both of these from BLS). Because banana prices have been very stable in nominal prices over time, it looks like strawberry prices are exploding! But it’s really more notable that banana prices haven’t rise.

USDA does have some fruit and vegetable specific retail price data, but it only goes from 2013 to 2023. That’s shorter than I would normally like, but it can give us a clue about whether there has been some recent explosion in berry prices. And ending in 2023 isn’t ideal either, but overall inflation has been moderate since 2023, so it’s probably an OK source to use. Here’s what the data shows (prices are for fresh berries, except cranberries which are for dried):

Relative to median wages, berries of all kinds are now more affordable than a decade ago. Parents may still feel squeezed by all the berries their kids are eating, but in terms of affordability and share of the family budget, there is probably no need for a Berry Panic.

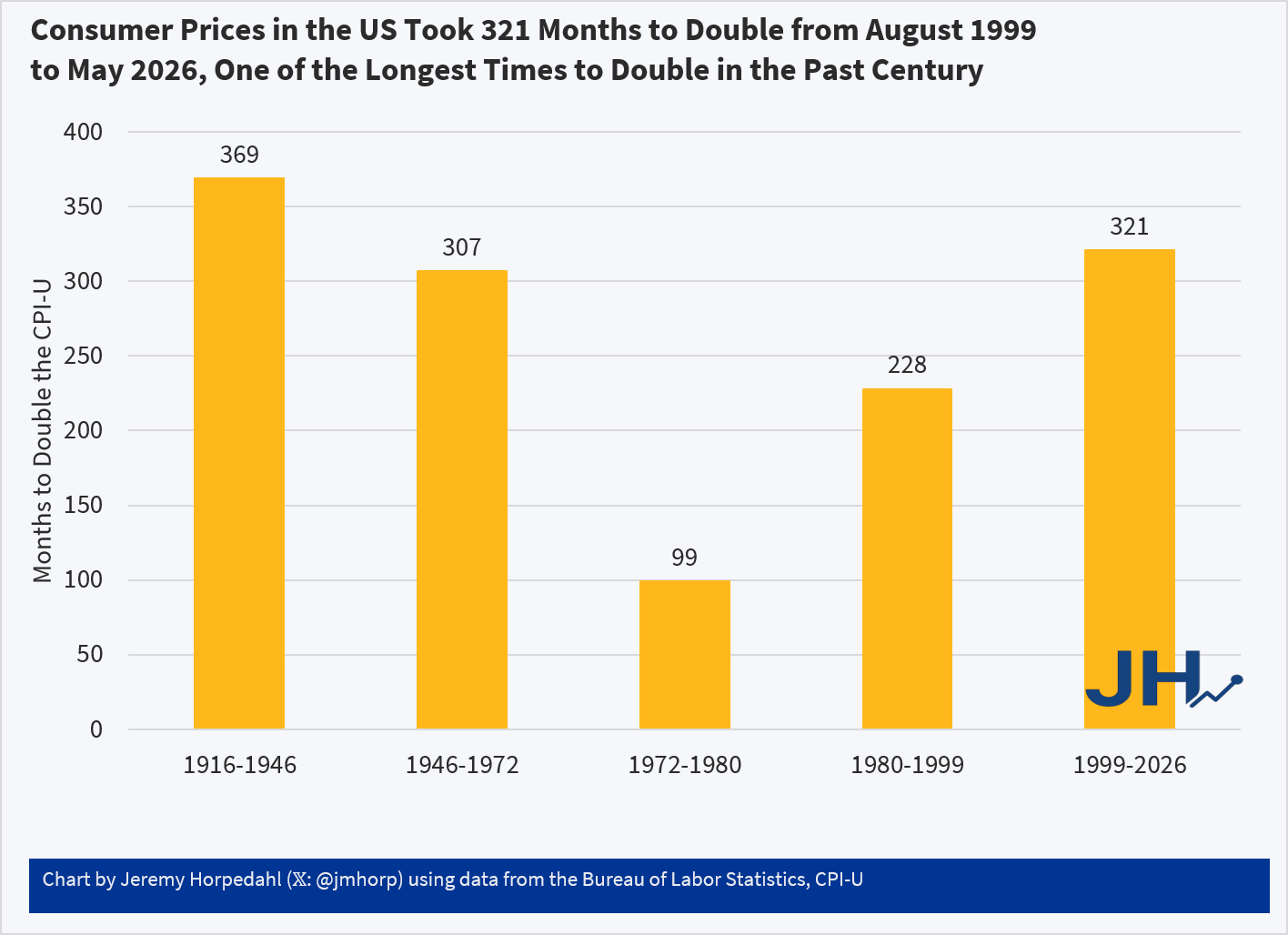

Two years ago I wrote about post about how long it took consumer prices to double in the US. The most recent time period looked pretty good compared to most of the 20th century. But lately I’ve seen a lot of social media posts talking about prices doubling (e.g., “you need twice as much income as the 1990s to match the standard of living back then”), so it’s worth looking at again.

The results aren’t that different:

Using the CPI-U, consumer prices in the US doubled in the most recent 321 months. Not only is that a longer period of time to double than most of the 20th century, in the prior 321 months (November 1972 to August 1999) consumer prices doubled twice: nominal prices were almost 4 times higher in August 1999 than in November 1972!

While the CPI-U does slightly overstate inflation, we don’t get much different results if we used chained indexes. For example, using the PCEPI, it took 390 months for prices to double between October 1993 and April 2026. Either way, prices roughly doubling from some time in the 1990s to today is accurate. But wages have more than doubled since then: you only have to go back to July 2005 for average wages to double (they are up 139% since August 1999 and 190% since October 1993). Or if we use a median wage series (such as EPI’s using CPI data), nominal wages doubled from 2002 to 2025 (I have readjusted that series back to nominal wages). In real terms, median wages are 22 percent since 1999 and 29 percent since 1993.

Of course, it would be better if prices weren’t doubling over any time frame! But the most recent doubling of prices that we lived through is the longest period to double in the lifetime of almost everyone alive in the US today.

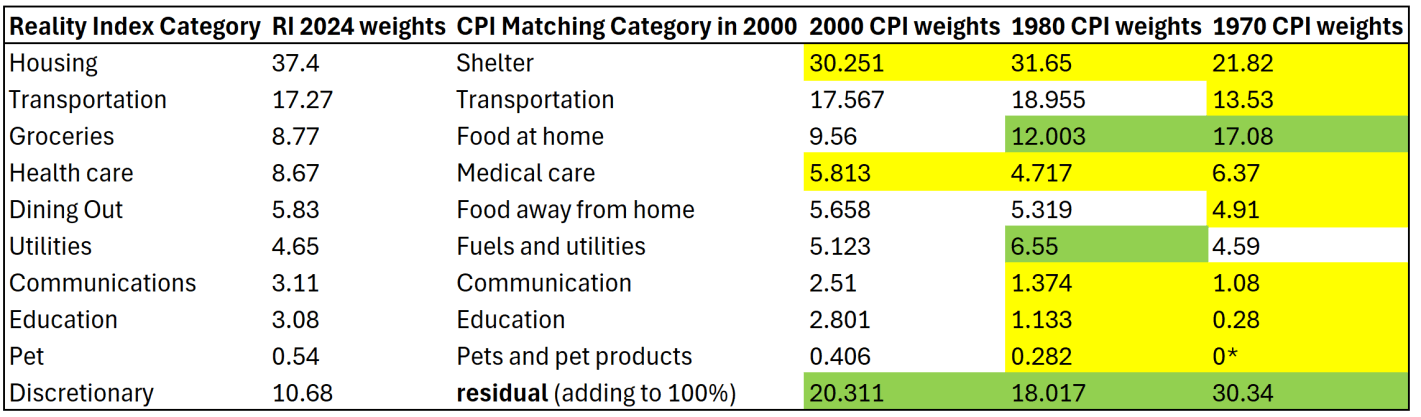

Over the years, many people have tried to create alternatives to the CPI for measuring inflation. Probably the most famous is “Shadow Stats,” which Tim Lee has convincingly shown isn’t actually measuring price inflation (it’s just adding a fixed factor to the CPI).

But the CPI critics keep coming. One that was recently released is called the “Reality Index.” This index tries to improve on the CPI-U in two ways. First, it uses fixed weights for the items in the basket, and importantly it uses the 2024 weights and applies them to past years (this is called a Paasche index). Second, it takes out some BLS prices to avoid using hedonically adjusted prices, and other price calculations that the Reality Index author thinks are weird.

Both of these changes are problematic. I will explain why.

1. Fixed Basket of Goods/Services Doesn’t Make Sense

Many critics of the CPI complain about the shifting weights in the CPI. “We just want to measure the cost of a fixed basket over time.” But measuring a fixed basket over time isn’t actually that useful. I will explain why in a moment. But that’s not even what the Reality Index does! Instead, it takes the 2024 CPI weights (which come from the Consumer Expenditure Survey), and then consistently applies those weights to past years. The Index isn’t measuring the cost of a fixed basket of goods from some past year — it is using the 2024 basket, and assuming that’s what people consumed in the past.

The author of the Reality Index, Tom Elliott, is either confused about this or is being deliberately misleading, for example in a recent WSJ essay promoting the Index, he says “That same basket, the one the government says rose 1.87 times since 2000, has actually risen about 2.4 times.” But that’s false. To do that calculation, you would need to use the 2000 CPI weights and follow them forward to 2024 (this is called a Laspeyres index). Instead, he uses the 2024 weights and follows them backwards. He could do the calculation that he references in the WSJ essay, but he does not.

To see why this is a bad approach, let’s compare the weights in the Reality Index with a few past years. I have done my best to translate the weights for the 10 categories listed on this page to actual BLS categories, though I will admit that none of their category weights matched exactly to what I found at BLS. But I’m pretty confident it is correct.

I am also pretty confident that the “discretionary” category is just a residual for everything that wasn’t in the other 9 categories, though I can’t find them explicitly saying this. Yellow highlighting indicates the category in past years was smaller than the 2024 weights. Green highlighting indicates past years were larger weights.

The first thing you might notice is that the CPI weights have changed significantly over time. Relative to 1970, housing/shelter gets almost twice as much weight today. Conversely, groceries/food at home gets about half the weight today as it had in 1970. The “discretionary” category (the residual to make it add to 100%) used to be 30 percent of a household budget, using this approach! That should really give you pause: do we really think a typical household in 1970 considered 30% of their budget to be “discretionary”? I highly doubt it. That discretionary category includes clothing, which was over 10% of household spending in 1970 (it’s around 2% today).

Related to that, you may also notice that categories which have had above average inflation over this time frame — such as housing, healthcare, and education — all have bigger weights today than in the past. Meanwhile, food and clothing have seen less price inflation, but they are weighted much less. This process will tend to overstate inflation of the past, as the CPI in 1970 placed less weight on, say, housing, so when you put more weight on it, of course the inflation rate will go up. And indeed, as the Reality Index’s historical analysis shows, the biggest gaps in inflation between the RI and CPI were in the 1970s (4.9% gap in 1979 and 4.7% gap in 1978). But this is ahistorical: people were not spending 37% of their budget on shelter in the 1970s! In fact, they were spending almost as much on groceries in 1970 as they did on shelter.

The Reality Index is essentially projecting backwards to a fake reality of the past, because it uses the 2024 weights in all past years. But this isn’t capturing anything real about the world, and it is at best an interesting thought experiment. Of course, part of the reason people now spend more of their budget on housing and healthcare is because they have gotten more expensive and to some extent crowded out other spending. But they are also categories we might expect demand to increase as incomes increase (normal goods). And notice this is the opposite of the standard critique of the CPI: as things get more expensive, critics claim the CPI assumes people spend less on those items. Instead, the CPI-U weights are updated each year based on the latest Consumer Expenditure Survey data, and goods/services with higher rates of inflation now consumer more of the weight of the CPI than in the past.

(*Note: the “pet” category is listed as 0% in 1970 because BLS didn’t itemize it separately due to it being so small. That’s of little consequence, since it is such a small share in every year — I’m surprised they didn’t just stuff pets in the discretionary category.)

2. Swapping Quality-Adjusted Measures for Nominal Prices is Often a Bad Idea

Using the 2024 weights for past years is reason enough to not find the Reality Index useful. But let me just say a few words about the substitute prices that the Reality Index uses. The changes are either trying to use something that isn’t hedonically adjusted for quality, or to overcome some of the strange calculations, especially for housing and health care.

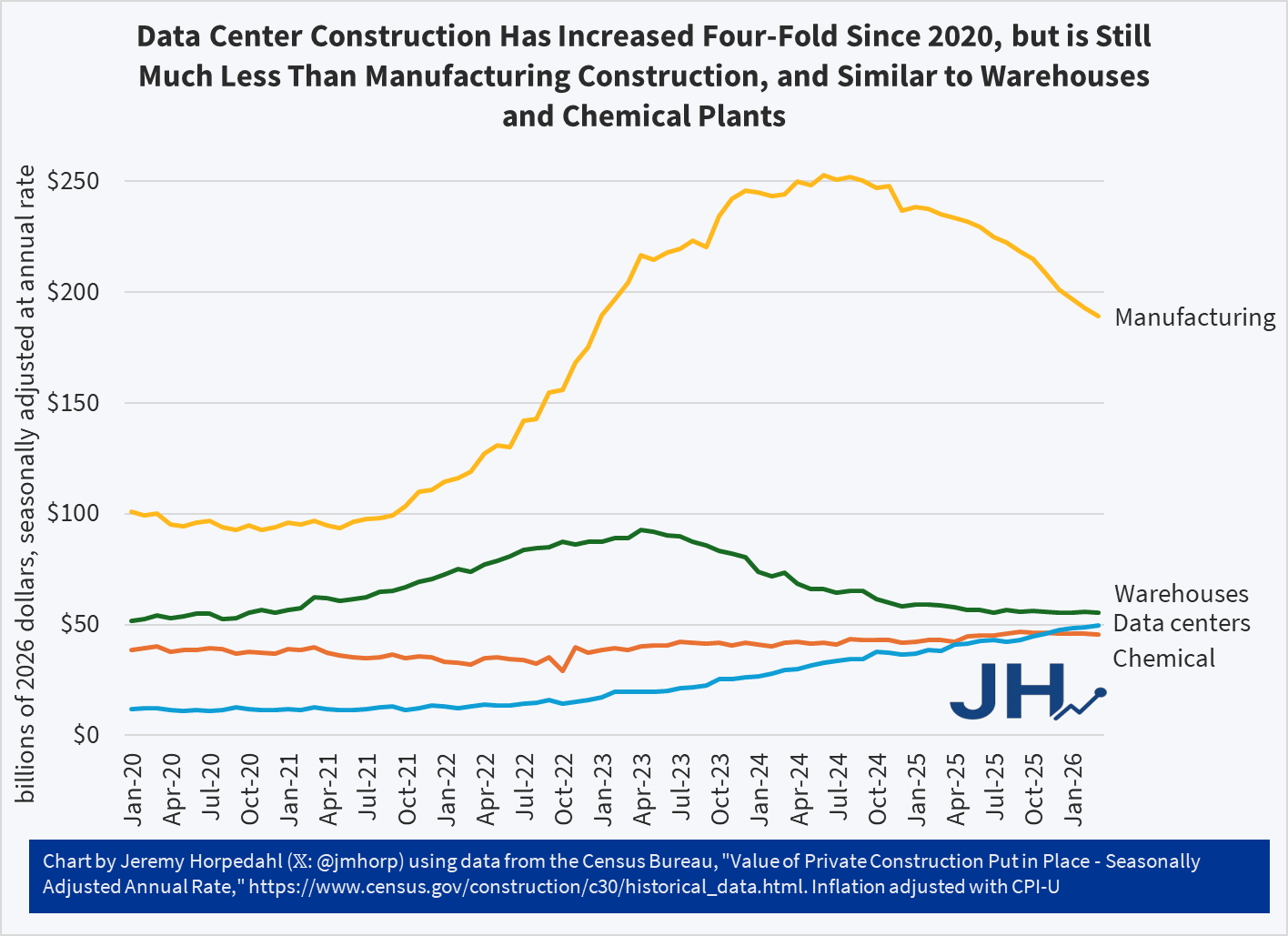

Data centers seem to be popping up everywhere. And based on the value of current construction, the US is indeed building a lot more data centers than we were in 2020 or 2021, about four times as much data center construction (inflation adjusted).

But… did you know that we build a lot more good-old manufacturing than data centers? Almost four times as much in recent months. And that’s even after a decline in manufacturing construction over the past year and a half.

The US also builds about the same amount of warehouses and chemical plants as we do data centers. Data centers may exceed those two categories in a few years, but for now they are pretty similar.

Keep in mind that manufacturing and chemical facilities also use a lot of electricity and water, and have plenty of local negative externalities! Warehouses probably have a lot less resource consumption and external effects, but it’s not zero either.

Are data centers popping up everywhere? Well, people are certainly noticing them. But so are lots of other types of buildings, which rarely register more than a peep from concerned citizens and local media, unless there is some clear and obvious external effect.