We celebrate 250 years since the Declaration of Independence was signed on July 4th, 1776. That’s the day that we celebrate our country’s birth. So, it’s very American of us to celebrate the day that we merely declared independence (not the day that the revolutionary war ended). We simply said we were independent from the crown. Regardless, we celebrate 250 years as a people. BUT, our government is only 237 years old. The current constitution replaced the articles of confederation in 1789. So there are some caveats to the whole semiquincentennial thing.

An important distinction that is baked into the American pie is that we are not our government. Our government is younger than we are. Our government has a piggy bank called ‘US Treasury’. It can spend and borrow for the US national government. It can also impose tax liabilities on the population in order to service those outlays. Now that it’s the government’s 237th birthday, what’s its basic financial track record?

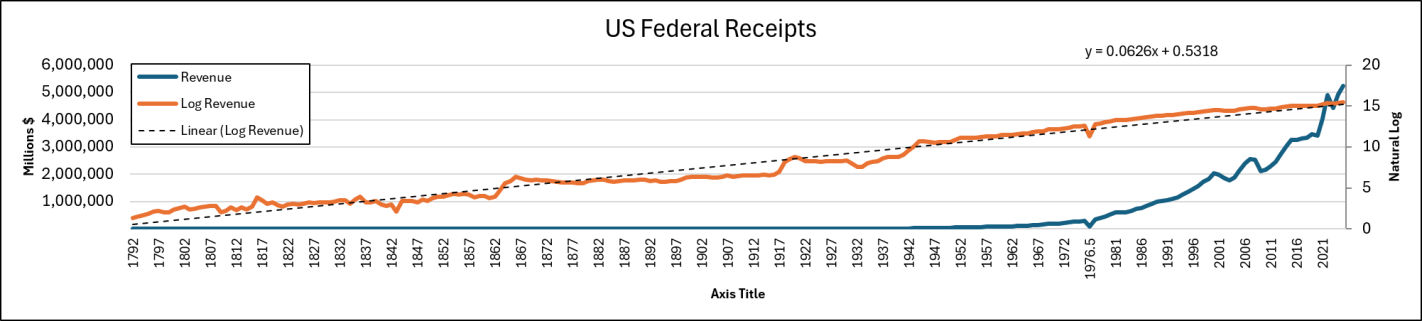

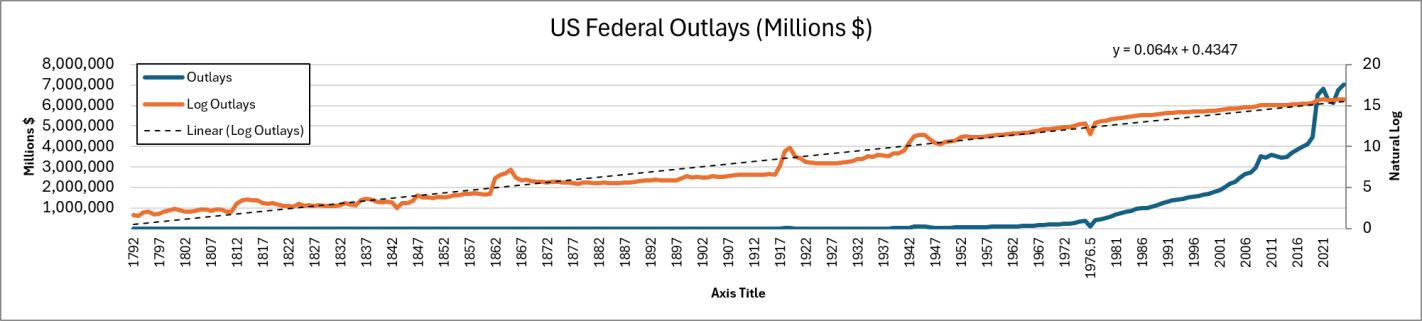

I like to think in the long run, for better or for worse, and I don’t like to get hysterical. So, let’s look at the full span of the 237 years – well – 235 years. The oldest annual data that we have is from Bicentennial Historical Statistics, which goes back to 1792. Below are the series for Federal Receipts and Outlays (revenue and spending).

The blue line is in nominal dollars and the orange line is the natural log so that we can see the changes in growth rates more easily. These aren’t inflation adjusted numbers, so we should expect to see some inflationary patterns. Long-run inflation was pretty stable prior to the 1913 Federal Reserve act and wee can see that reflected in both series. There was some drift upward in terms of revenue and expenditures. But the primary pattern was one of punctuated rises followed by plateaus. That’s a pretty standard ratcheting leviathan pattern. There’s a bump up for the big events in the first half of our history: the War of 1812, Civil War in 1861, and World War I in 1917.

Then, after the great depression and leaving the gold standard (mostly), in about 1933 a new and positive trend in cash flows began. In fact, it’s amazing how consistent the raw nominal series is. We can see where World War II is in the series, but after that we appear to have traded punctuated increases for steady increases. Even the higher inflation rates of the 1970s look pretty muted and on trend (Btw, the blip in 1976 is a record-keeping artifact. There was a 3 month gap-period when the US government changed its fiscal year start/end). Even the new growth in total cashflows seems to be slightly bending downward and growing a little more slowly.

But rest assured, spending has exceeded revenues. Below is the long run deficit. I don’t take the log for this one since there are negative numbers. It’s hard to tell from the line graph, but the first big and persist swing in the deficit arrived after the Fed was established and the onset of WWI. The deficit hit $9 billion in 1918, which was 10x the prior peak of $0.9 billion at the end of the civil war in 1865. Notice that the above government revenues stayed flat or fell after 1920, but the outlays began trending upward before the revenues. The deficit doesn’t really start its long, steady march until 1932. Of course, for the past quarter century, the national government has been in a deficit mess (even if you measure the proportion of GDP).

Continue reading