I’ve recently gone back and started listening to the archived episodes of the ‘Macro Musings’ podcast hosted by David Beckworth. The show started in 2016. At that time, there was still a sense of malaise after the 2007-2008 Great Financial Crisis (GFC) and the slow recovery that followed it. We were also in a prolonged low-interest rate environment.

A recurring theme is whether the Fed should have engaged in expansionary policy earlier than they did in response to the GFC. There are multiple ways to answer. It’s not helpful to say ‘knowing what we know now’. The Fed didn’t have that opportunity. It’s a little bit more helpful to say ‘if the Fed had a different target or different tools’. The target and tools are higher-order policy decisions and changing them can be helpful in the future. But they typically can’t be changed with the flip of a switch. After all, the 2% inflation target itself rolled out over the course of decades.

The most awkward/damning question is “Given the target, tools, and data that the fed actually had, did they make the right decision?”. If the answer is ‘no’, then that warrants a serious investigation of individuals, groups, processes, etc. I don’t mean a legal investigation. I mean the decentralized kind in which public and expert trust can be affected.

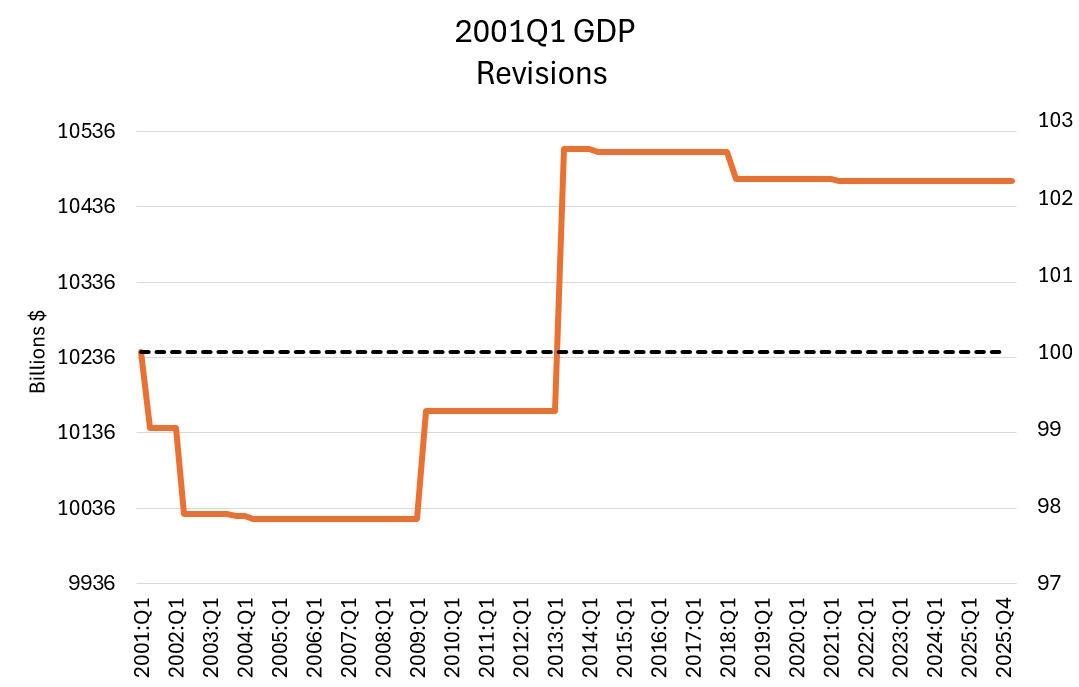

A concept that Beckworth often mentions concerning Fed culpability/performance during the GFC is the problem of data revisions. Currently, we know what the revised data says about NGDP, inflation, employment, etc. But the Fed only had the contemporary numbers and immediate revisions. In a world where economic growth is lousy or stellar in a range of 1-3%, small revisions can matter a lot. For example, below are the 2001q1 NGDP revision values over time.

Revisions occurred twice by 2002q2, revising NGDP down by more than 2%. Subsequent revisions raised the value on record to nearly +3% of the initial estimate, before settling at a less elevated value. Sheesh! In a world where a 1% swing is a big deal, how can we possibly expect the Fed to succeed at managing aggregate demand?

Things are not so scary as they might seem. The Fed doesn’t much care about revisions to an individual quarter. Rather, they care about the direction of change over time. Whether future revisions increase GDP by 2% is unimportant. What’s important is whether one period’s value is lower relative to the earlier value. That’s the relevant difference that tells us how the economy is changing.

Now, in 2026, our current understanding of NGDP during the GFC follows the below pattern starting in 2005q1 (lest I omit important pre-trends). NGDP growth had weakened in 2007q4, turning negative in 2008q1. Weak growth resumed in 2008q2. Then we had near-zero or negative growth for the next five quarters. Of course, we’re now approaching twenty years later, so we have the huge benefit of hindsight and revisions. Keep in mind that the contemporary numbers aren’t available until the subsequent quarter. By the yard stick of NGPD, the Fed should have been loosening by Q3 or certainly Q4 of 2008 if they cared about supporting total spending. Maybe as early as Q2 is they were especially sensitive.

Continue reading