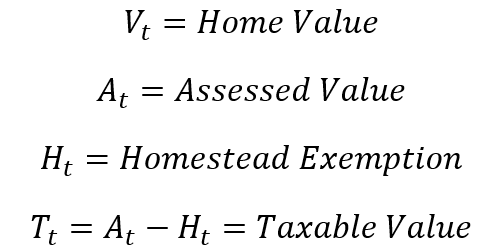

Voters this November will face a proposed amendment to the Florida state constitution on property tax reform. Currently, Florida has what’s called a ‘homestead’ exemption of $50,000. If a residential property is your primary residence, then your home’s assessed value is $50k less before taxes are calculated. There is no exemption for rental property or 2nd homes or vacation homes. The proposed amendment increases the exemption to $250k by 2028 and then indexes it to inflation.

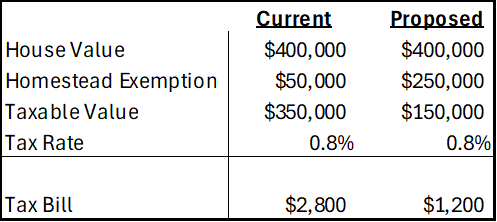

First, let’s get an idea of the magnitudes. The median home in Florida is priced at about $400k and the average property tax rate is around 0.8%. Below compares the current consolidated tax bill against that of the proposed amendment. Given current home prices and local tax rates, the new exemption would have a huge impact on municipal governments who get the bulk of their revenue from property tax. In fact, there is no Florida state property tax, so the proposed amendment would adopt a new rule for municipalities and not the state government.

What Motivates the Amendment?

The current homestead exemption of $50k was established in 2008. A subsequent amendment in 2024 allowed half of that to be indexed to CPI-U. The average home price in Florida has risen 114% since 2008 and 84% since 2020. That’s a lot faster than inflation, but the tax burden is partially offset by a maximum of 3% annual increase in assessed value. Regardless, many individuals face a larger tax bill over time even independent of whether their income or use of public services has changed. Plenty people are feeling the squeeze.

What’s the Purpose of the Homestead Exemption?

The exemption is available for primary residences only. That means that rentals and vacation homes do not qualify. It’s important to keep in mind that, given some total revenue, every tax break for one group or activity implies a higher tax rate for others. So, clearly, the effect is to tax residents less and tax seasonal residents and visitors more. Florida doesn’t have an income tax, but it does have a sales tax, gasoline tax, and others that are disproportionately borne by non-residents. Given that higher income individuals tend to have higher home values, the homestead exemption is a way to lower the tax burden of lower income households. Obviously, the lowest income individuals are renters, but so are non-residents who Florida prefers to tax.

The Economics

Homeowners

The exemption is enjoyed by all primary residences, but helps low income owners the most. And, given a stable amount of municipal tax revenue, a higher homestead exemption requires that municipalities replace that revenue. This might take the form of higher local fees and taxes, making life harder for lower income people to, say, own a car or make purchase if taxes on those activities rise. Revenue stability might also be helped by higher property tax rates. The higher the property value is above $250k, the greater the average tax burden that is borne. So, someone with a very high property value may find themselves with an even higher property tax bill after municipalities adjust to the proposed statewide rule. In this sense, the new amendment would be a step in the direction of tax progressivity (a higher proportion taxed from those with higher income/wealth).

Indexing

Normally, I am in favor of indexing nominal values to CPI. In this case, we need to think about what the goal is. Let’s assume that the goals is to provide relief to lower income homeowners specifically and all primary residence homeowners generally. Does indexing to the CPI help? It depends!

There is no single inflation rate. The prices for different goods change differently. Home values may change at a rate that is different from consumer goods. For most of the past several decades, home prices have grown faster than consumer prices. What’s the implication of this divergence? We can examine it from the perspectives of the homeowner and of the local government.

If CPI grows slower than home values, then the homestead deduction wouldn’t keep up and the taxable portion of homes would rise. Homeowners pay more and municipalities get a windfall of revenue if tax rates remain unchanged.

If CPI grows faster than home values, then homeowners feel a lower tax burden as inflation chips away at the taxable value of their home. But this also means that municipalities get squeezed. They may face shortfalls, layoffs, budget cuts, or new taxes. I find that a bit awkward. If inflation is high and workers require higher wages, then municipalities will receive less revenue at exactly the same time as it becomes more difficult to hire and retain workers.

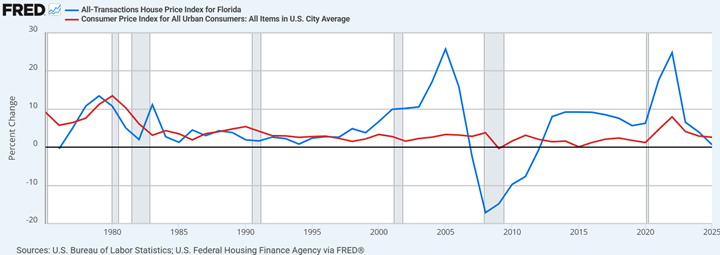

Below is the annual percent change in Florida home prices and the CPI since 1975 (the earliest data). The two are correlated, but not the same. Anytime that the blue line exceeds the red line, homeowners would pay more in property taxes even with the homestead exemption that’s indexed to inflation. When the red line exceeds the blue line, municipalities get pinched instead.

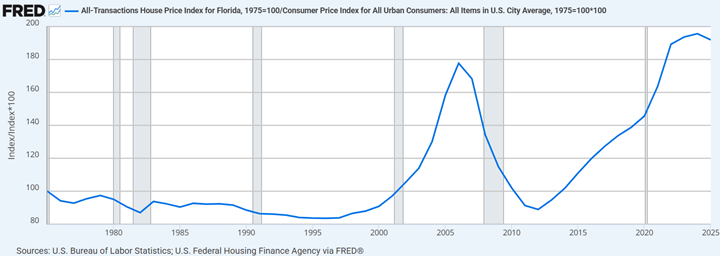

Making the unreasonable assumption of a stable taxable proportion, we can approximate the net effect using the below equation and graph that’s indexed to 100 in 1975:

We can see that there would have been large swings in taxable value. From 1975 to 1996 taxable value would have fallen by 16%. Without an offsetting increase in households or tax rates, this translates to falling municipal revenues. From 2012 to 2024, the taxable portion would have risen by 120%.

An Asymmetric Grace/Curse

(This section has been updated. Details are in post script.)

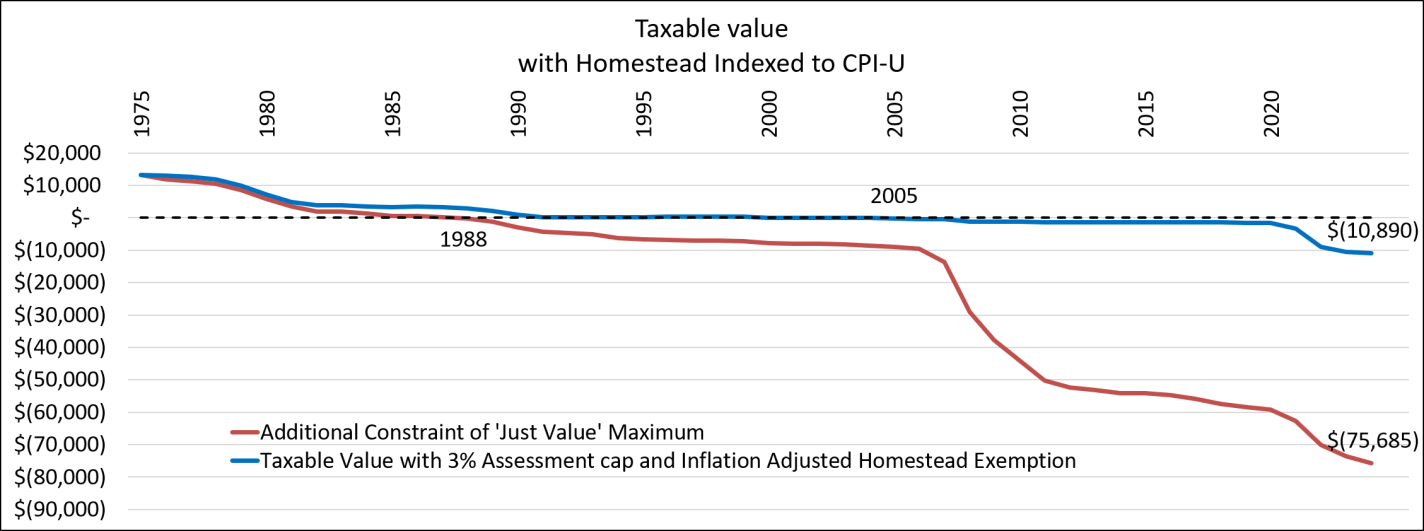

The above figure is quite misleading because the current law already has a built-in maximum year-over-year assessment value increase. Municipalities can’t increase a home’s value assessment by more than the lesser of A) 3% or B) CPI-U inflation or zero if there is deflation. Therefore, assessed values will very likely be consistently underestimated.

There is no such restriction on the homestead exemption, however. So, if both a home’s value and CPI rise by 6%, then the assessed value only rises by 3% while the homestead exemption rises by the full 6%. That means that the taxable portion of the home falls by in *nominal* terms! The blue line in the figure below uses the data since 1975 again, but includes the binding 3% assessment growth cap. If the proposed amendment had been in place, similarly exempting 62.5% of the home value, then *all* of the taxable value would have been eroded by 2005.

But there is yet a 3rd constraint on the growth of assessments! Home value assessments can’t exceed the ‘just’ value. That could mean a bunch of things. One way that I interpret it here is that the assessment increase also can’t C) surpass the actual growth rate in the price of the house. The definition here is a bit fuzzier since prices and assessed values update at different frequencies. But, if we accept that the assessed values grows at the minimum of A), B), and C), then that yields the red line above where *all* of the taxable value of primary residences would have eroded away by 1988 – just 13 years after indexing the homestead exemption to inflation. According to current law and adding the proposed amendment, the assessed value can fall, but the homestead exemption always ratchets up.

Yay or Nay?

No legislation is perfect. But do the benefits outweigh the negatives? Florida resident-homeowners would be taxed less. The effects would be lopsided and very progressive. I think that the higher homestead exemption would be initially welcomed by everyone given the rapid increase in home prices over the last decade. However, the inflation adjustment is terribly specified since consumer prices and home prices tend to grow at very different rates. Especially in the presence of the 3% appraisal growth cap, the proposed legislation eventually whittles away the tax base down to nothing. The negative impacts on municipalities – the providers of most government amenities and services – would be devastating.

Let’s also remember that property taxes, while not perfect, are among the most efficient taxes in the US. They are easy to understand, well targeted, and pretty close to a lump-sum tax in the short-run.

I don’t think that the state government needs to get involved and limit the autonomy of local government. A much better solution would be for local municipalities to lower their property tax rates. Even better would be if they adopted two-part taxes that included both a fixed portion that taxes land area and a variable portion that taxes property value. But municipalities just changing local tax rates in response to home value increases and old exemption amounts would be better than updating the state constitution. I say that responsible members of civil society vote no on the proposed amendment.

Additional Facts:

- None of the above analysis is applicable to school district taxes, which is usually about 40% of municipal tax revenues.

- Total property tax collections in Florida is are about $43 billion.

- 36% of property tax revenue is from primary residences, the remainder is rentals and commercial real estate and 2nd homes.

- Under the proposed tax rules, home prices would not change in the same way as they did historically. With a lower tax burden, home prices would rise faster because it would be less expensive to own a home.

- Given a homestead exemption of $250k and a home value of $400k, all it takes is 25 years of identical 5% inflation and property value growth to eliminate the taxable value entirely.

- There is no similar zero lower bound to the ‘just’ value rule. Assessed values felll after the 2008 financial crisis.

- The cap on Non-homestead assessment increases also falls from 10% to 5% in the proposed amendment. So, snowbirds will not entirely be picking up the tab, though they will get increasingly worse relative tax treatment.

- New residents must live in Florida for 5 years before they qualify for the full proposed exemption.

- The proposed amendment also redefines the rollback rate. The rollback rate says that revenues can keep pace with Florida median income without extra voting requirements. The new limit says that rollback rates must remain revenue neutral on pre-existing homes in nominal terms.

- There are State-imposed voting requirements on the amount by which municipalities can raise property taxes.

Edit: I adjusted the last graph and related numbers to more accurately reflect that the taxable amount is a residual of the home value assessment and the homestead exemption. Below is the math. Given that the average home price in 2025 was $400k, we can use the index to find that the average value in 1975 was about $35k. The proposed homestead of $250k is 62.5% of the 2025 value. So, a comparably proportional 1975 homestead exemption would be $21.9k. I assume that the assessed home value was identical to the actual home value in 1975.

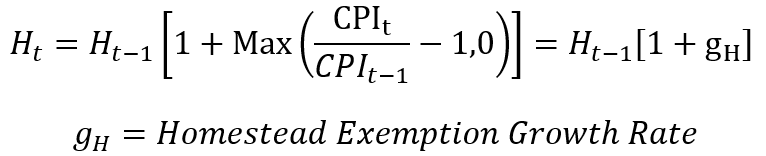

The homestead exemption grows at the rate of inflation that’s measured by the CPI-U, or zero if there is deflation.

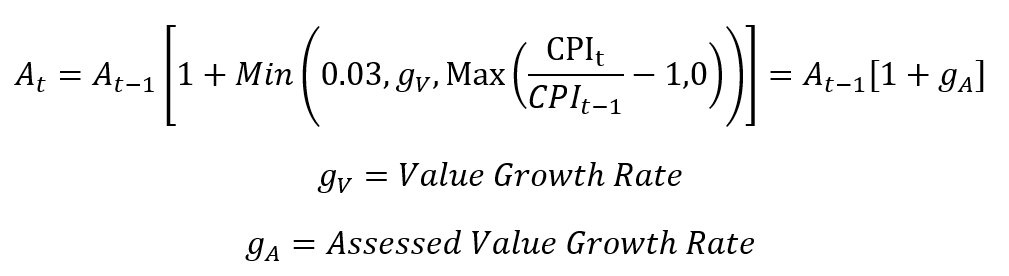

The assessed value grows at the lesser of A) 3%, B) the percent change in ‘just’ value, C) the rate of inflation that’s measured by the CPI-U, or zero if there is deflation. Here, for tractability, I assume that the percent change in just value is the same as the percent change in the home value.

The growth rate of the homestead exemption is always greater than or equal to the growth rate of the assessed value. Therefore, the homestead exemption eventually exceeds the assessed value and taxable value becomes negative.

When I bought my home in 2015 the property was reassessed at current (2015) value. The people who lived there before me had been in the home for about 24 years so benefitted with property tax progressively lower after inflation year over year as you state. How do these numbers change given properties once sold are then reassessed to a higher current value?

LikeLike

That’s a great question. As you say, sale updates the assessed value, which puts upward pressure on the tax bill. BUT:

So, you are right that the assessed value can increase at sale. But, either of the above effects can drive the taxable value to zero.

LikeLiked by 1 person