Next week the Fed will almost certainly hold interest rates steady. Stephen Miran will probably dissent saying the Fed should be cutting rates. Kevin Warsh, Trump’s nominee for Fed Chair, would also like to see cuts. But other prominent voices think that rising oil and gas prices mean we should be raising rates.

I still think that rate hikes make more sense than cuts- but not because of oil. The high oil and gas prices we’re seeing are obviously driven by supply shocks from the Iran war- not increasing demand. Raising rates to fight an oil shock would mean repeating a classic mistake.

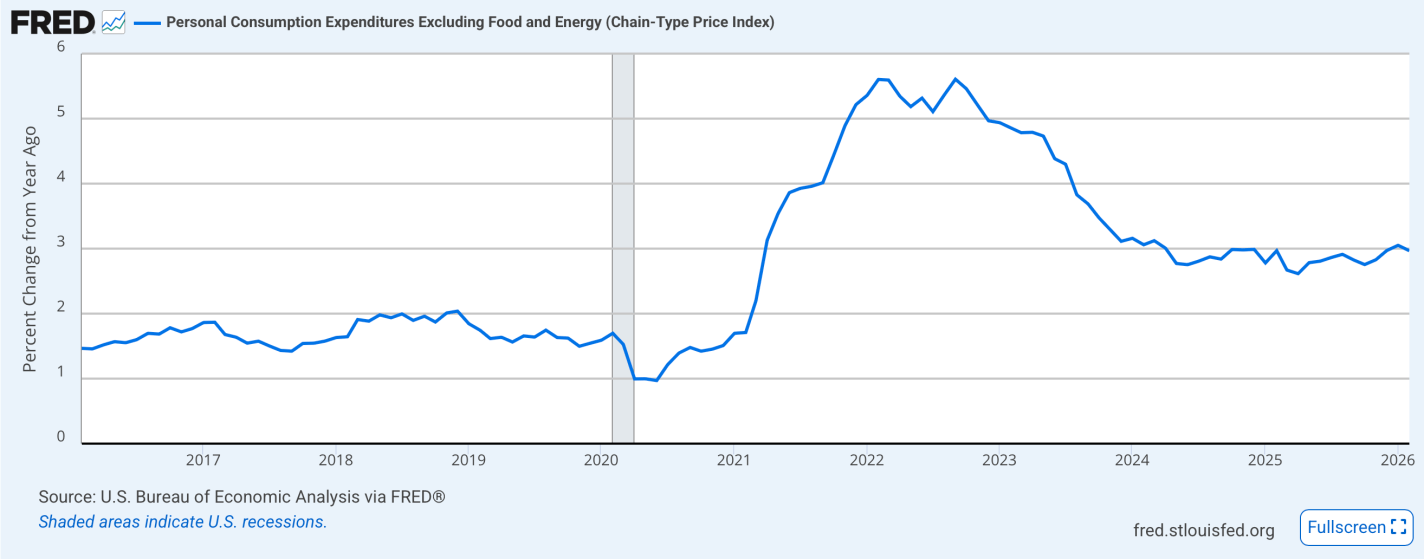

But raising rates to fight core inflation that is at 3% makes perfect sense. Especially when inflation (overall or core) hasn’t been at or below the Fed’s supposed 2.0% target in over 5 years, and market forecasts predict it will stay well above 2.0% for the next 5 years.

Especially when real GDP is growing, and NGDP is still above trend, and the unemployment rate is 4.3%. Financial conditions are so loose that stock markets are hitting all time highs in the middle of a war.

Various Taylor Rules suggest that the Fed Funds rate should be between 4.25% and 6.25%, but the Fed currently has us at 3.75%.

I see so many good arguments to raise rates- there is no reason to bring up a bad one like oil prices. If we must latch on to a headline to find the argument to raise rates, let’s focus on a shoe company’s stock going up 600% because they announced they were pivoting AI.