In the past several years there has been increasing salience and support of pronatalist policies. Several people have turned to the IRS income tax code, which already includes some incentives regarding children. The Child Tax Credit (CTC), which lowers a person’s tax liability on a dollar-per-dollar basis, is the most obvious item that addresses children. The other tax credit is for child care expenses, but I won’t be focusing on that here.

Below are the 2021 marginal tax rate brackets and the standard deductions. The standard deduction reduces the taxable income, and then the tax rates are applied.

After the tax liability is calculated, it’s reduced by any tax credits, such as the CTC. In 2021, households earned a credit of $3,600 for every child under 6 years old and $3,000 for every child under 18 years old. Median household income in 2020 was $67,521. That means that the tax liability was reduced by 5.3% – or 3/55ths – of median gross income. But, I have a problem with that.

The standard deduction for a married couple is simply the standard deduction of single person multiplied by two. Do you know why? Because married people are twice the number of single people, of course! Somehow, when it comes to counting adults, we acknowledge that they are whole persons. But when it comes to counting children, we start slicing and dicing with tax code complication. Why do we not just multiply the standard deduction by the number of people in a household (as if a person is a person, no matter what). For many earners, that would be a substantial benefit – though not all tax payers would come out ahead.

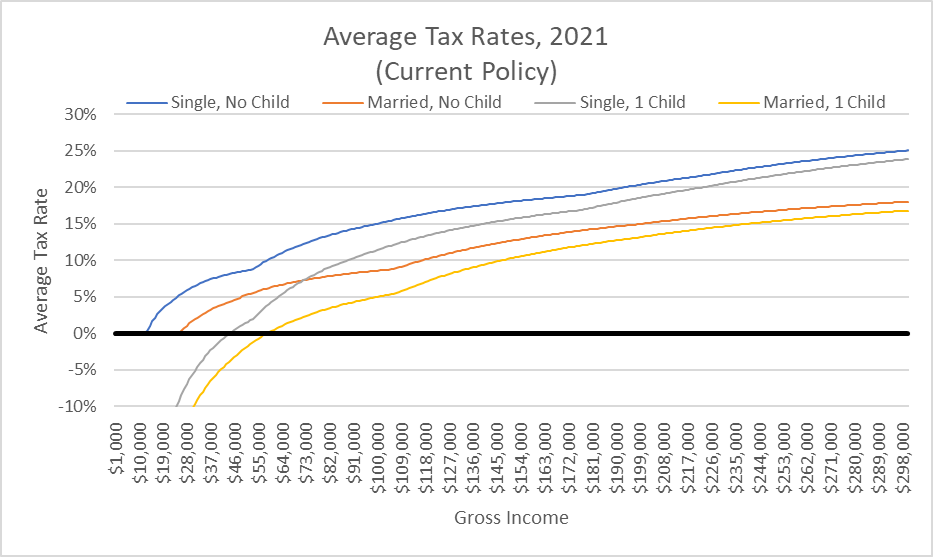

Before we go any further: the federal income tax code is a big ol’ messy mess. There are bunches of complications and details that I will not address. Below is the current average tax rate (ATR) in four cases: Single with no children, Married with no Children, Single with 1 child, & Married with 1 child. For simplicity, I assume that they take the standard deduction, the CTC with a child under six years of age, and that there are no phase-outs.

What do we see in the above? First, being married is nice. There are some economies of scale that you enjoy in the household. For example, you only use 1 bedroom, 1 dining room, etc. Not only that, having 1 of 2 people working has tax advantages if they are married. The standard deduction isn’t refundable, so a non-working single individual doesn’t gain anything. But when that non-working person is married, their spouse enjoys the lower tax rate that results from the larger standard deduction.

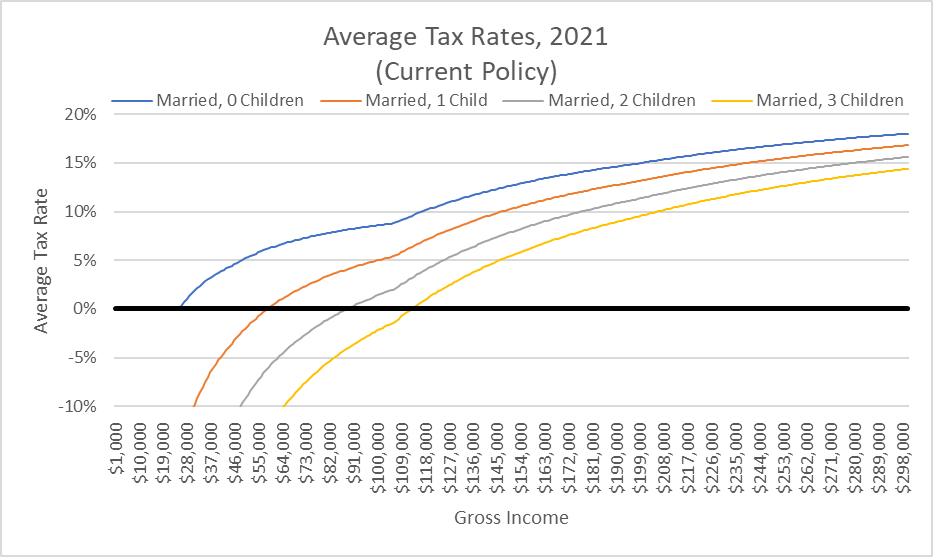

Second, having a child is nice. They reduce the tax liability and the average tax rate – even below zero for people with lower gross incomes. We also see that the difference in ATR due to having a child falls as incomes rise. That is, having a child doesn’t change the ATR so much as a person’s gross income increases. What about the effect of having multiple children under the current system? Below are the ATRs of married people by the number of kids that they have. Again, we can see that having more children provides a substantially lower average tax rate, and that the difference shrinks as income rises.

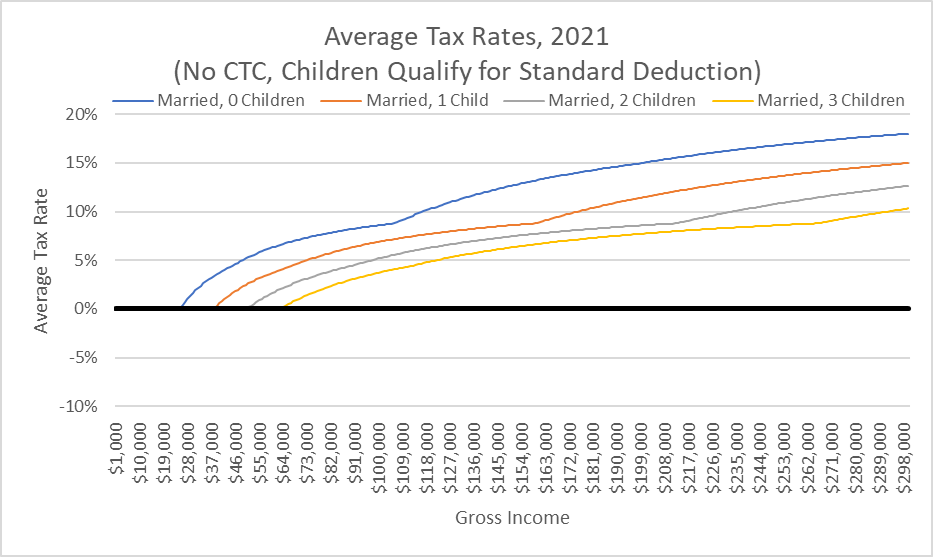

But, echoing my point above, the current system counts children as ‘special’. What if we counted children just like adults? Below is a graph that reflects the average tax liability by income and number of children if we removed the CTC, allowed the individual standard deduction to apply to children, and adjusted the tax brackets similarly. First, note that that no one has a negative tax rate. Second, the amount by which the ATR falls with an additional child depends on they the income of the household. Those kinks in the curve are due to tax bracket changes. The ATR benefit of having children still decreases with income, but the margins are less applicable. Compared to the previous graph, note that high earning households would receive hefty ATR discounts by having more children (people are touchy about whether we should want richer people to have more kids. I’ll leave that discussion for another time). Finally, notice what happens to the lower income ATRs. Under the current system, a family with three children grossing about $113k has a tax liability of zero. Treating children like they are whole persons would result in lower income families paying a *higher* tax rate than they do under the current rules.

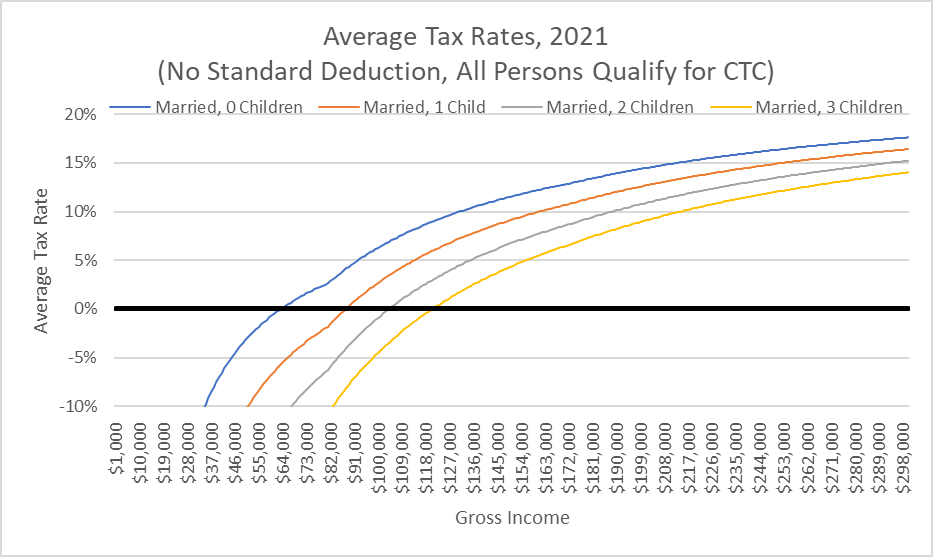

This brings us to the reasoning behind why we treat children kind of like they are 3/55ths of a person. If the IRS tax treatment of children switches from credits to deductions, then poorer people lose out and richer people enjoy some nice tax breaks. Maybe that makes this a political nonstarter. Alternatively, we could switch the standard deduction to a credit. By making the credit refundable, we can still help poorer families, while lowering the ATR advantage of children to higher income earners. That would look something like the below in which I assume that there is no standard deduction and that the CTC also applies to adults.

This graph looks a lot like the current policy except, with credits instead of deductions, adults aren’t penalized with a higher tax rate just because they are adults. Anyone can enjoy a negative ATR, provided their income is low enough or they have enough children. Each additional child still provides less of a tax advantage. That is, if you want to have a zero tax liability, children have diminishing marginal benefits. This system looks good to me, but I suspect that the public has feelings about a childless married couple making $50k per year facing a negative average tax rate.

Finally, I personally find that all of these deductions and credits add needless complexity to our tax code. I prefer a different tack. Here me out, because it sounds more confusing than it is. What if we could build tax code that favored more children without dollar-denominated CTCs or standard deductions? To boot, the following policy would also encourage density, reduce sprawl, increase the number of people per home, and reduce housing scarcity generally? Are you ready?

Here’s what I favor. We levy the marginal tax on a per-person basis (PPB). That is, we calculate the average income per person in a household, calculate the tax that each individual would pay, then multiply it by the number of people in the household. Badda bing badda boom! Now people have an incentive to have kids, the tax treatment of children becomes identical to the tax treatment of adults, and we’ve made the pro-natalists and the environmentalists happy. Using the current individual tax rates, the below is what the ATR would be.

First of all, note that the vertical axis changed. Taxing on a per person basis ‘penalizes’ persons who are 1-person households. Achieving pronatal goals and reducing our environmental impact can’t just be due to handing out goodies. There’s no such thing as a free lunch. That is, we can’t just offer people lower tax rates if they densify/adopt/give birth. We would also need to impose costs on those who do not densify/adopt/give birth. That’s just the way of the world. The tax revenues and the real resources that they represent must come from somewhere. I prefer this PPB system greatly. We can talk about how the tax rates or brackets ought to change – maybe people shouldn’t be paying 10% of their incomes to the government when their incomes are extremely low. OR, and hear me out, the tax code is not the place to provide poverty relief. Maybe we should simplify the tax code with simple rules that don’t change based on whether your married or have children. After all, one could opt to live in a commune and still enjoy the benefits of the PPB tax code.

Deductions and credit are the stuff of opacity. Let’s simplify.

“Fortunately” married people vote more than singles so maybe this has a chance of turning into policy.

On the other hand I’ve found that pronatalist arguments tend to have a whiff of xenophobia or racism. It would be easy to demonize such a policy as encouraging “the wrong kind of people” to have children….

LikeLike