Other than being the smallest state, of course. In other places I’ve lived, it was more obvious what made them stand out. Boston has the most high-quality universities, including the oldest one (though it is expensive and traffic-ridden). New Orleans has the best food, live music, and festivals (though terrible crime and roads). I’ve lived in Rhode Island since 2020 and I’ve enjoyed how it seems to have no big negatives the way many other places do- it’s been pretty nice all around. But it has been harder to see anything where Rhode Island really stands out.

What should a tourist see or do here that they couldn’t do elsewhere? The Italian food is great, but that’s true of several other cities. You can find Portuguese food here in a way you can’t in most of the US. Probably the Cliff Walk in Newport is our best entry: a 3-mile trail along cliffs where you can see the Atlantic on one side, and Gilded-age mansions on the other.

For those living here, what stands out is the compactness. This makes sense for the smallest state, but it is even more true than you would expect, because even within Rhode Island most people are clustered within the small portion of the state that is within 5 miles of Providence.

Because of this, I almost never feel the need to drive more than 10 miles or 20 minutes; this wasn’t so true any of the other ~dozen places I’ve lived. I can easily walk to the Bay, the Zoo, and my kids’ school; then its a 20 minute drive or less to work, several good hospitals and universities, sailing, several beaches, forest hikes, the state capital, the excellent airport, Amtrak, every good grocery store, leaving the state, et c. Most other places either lack some of those things entirely or involve longer drives to get to them, though probably there’s somewhere else like this I don’t know about.

Or perhaps the best thing about Rhode Island is our people:

What do you think I missed about Rhode Island? Or if you haven’t been here, what do you think is most special about where you live?

Ray Fair at Yale runs one of the oldest models to use economic data to predict US election results. It predicts vote shares for President and the US House as a function of real GDP growth during the election year, inflation over the incumbent president’s term, and the number of quarters with rapid real GDP growth (over 3.2%) during the president’s term.

Currently his model predicts a 49.28 Democratic share of the two-party vote for President, and a 47.26 Democratic share for the House. This will change once Q3 GDP results are released on October 30th, probably with a slight bump for the dems since Q3 GDP growth is predicted to be 2.5%, but these should be close to the final prediction. Will it be correct?

Probably not; it has been directionally wrong several times, most recently over-estimating Trump’s vote share by 3.4% in 2020. But is there a better economic model? Perhaps we should consider other economic variables (Nate Silver had a good piece on this back in 2011), or weight these variables differently. Its hard to say given the small sample of US national elections we have to work with and the potential for over-fitting models.

But one obvious improvement to me is to change what we are trying to estimate. Presidential elections in the US aren’t determined by the national vote share, but by the electoral college. Why not model the vote share in swing states instead?

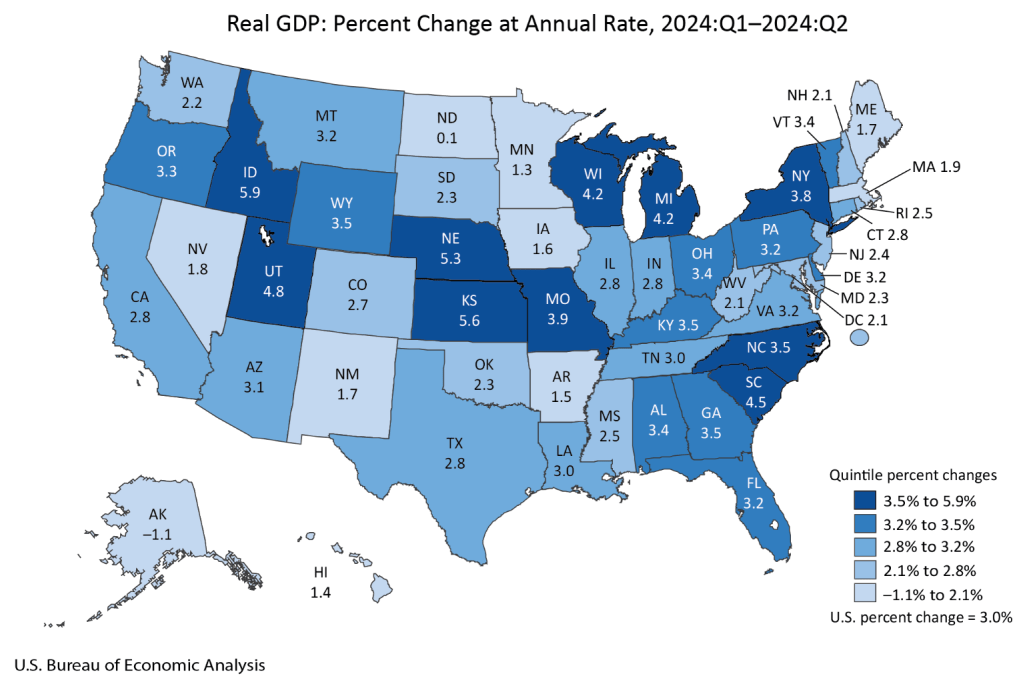

Doing this well would make for a good political science or economics paper. I’m not going to do a full workup just for a blog post, but I will note that the Bureau of Economic Analysis just released the last state GDP numbers that they will prior to the election:

Mostly this strikes me as a good map for Harris, with every swing state except Nevada seeing GDP growth above the national average of 3.0%. Of course, this is just the most recent quarter; older data matters too. Here’s real GDP growth over the past year (not per capita, since that is harder to get, though it likely matters more):

Region

Real GDP Growth Q2 2023 – Q2 2024

US

3.0%

Arizona

2.6%

Georgia

3.5%

Michigan

2.0%

Nevada

3.4%

North Carolina

4.4%

Pennsylvania

2.5%

Wisconsin

3.3%

Still a better map for Harris, though closer this time, with 4 of 7 swing states showing growth above the national average. I say this assuming as Fair does that the candidate from the incumbent President’s party is the one that will get the credit/blame for economic conditions. But for states I think it is an open question to what extent people assign credit/blame to the incumbent Governor’s party as opposed to the President. Georgia and Nevada currently have Republican governors.

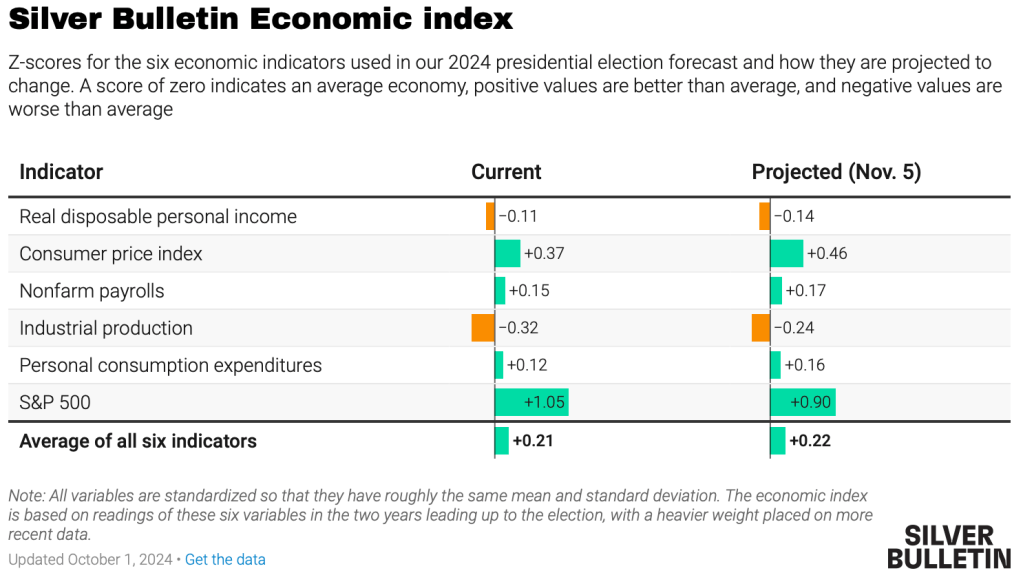

Overall I see this as one more set of indicators that showing an election that is very close, but slightly favoring Harris. Just like prediction markets (Harris currently at a 50% chance on Polymarket, 55% on PredictIt) and forecasts based mainly on polls (Nate Silver at 55%, Split Ticket at 56%, The Economist / Andrew Gelman at 60%). Some of these forecasts also include national economic data:

Gelman suggests that the economy won’t matter much this time:

We found that these economic metrics only seemed to affect voter behaviour when incumbents were running for re-election, suggesting that term-limited presidents do not bequeath their economic legacies to their parties’ heirs apparent. Moreover, the magnitude of this effect has shrunk in recent years because the electorate has become more polarised, meaning that there are fewer “swing voters” whose decisions are influenced by economic conditions.

But while the economy is only one factor, I do think it still matters, and that forecasters have been underrating state economic data, especially given that in two of the last 6 Presidential elections the electoral college winner lost the national popular vote. I look forward to seeing more serious research on this topic.

I missed Alan Kreuger’s 2019 book on the economics of popular music when it first came out, but picked it up recently when preparing for a talk on Taylor Swift. It turns out to be a well-written mix of economic theory, data, and interviews with well-known musicians, by an author who clearly loves music. Some highlights:

[Music] is a surprisingly small industry, one that would go nearly unnoticed if music were not special in other respects…. less than $1 of every $1,000 in the U.S. economy is spent on music…. musicians represented only 0.13 percent of all employees [in 2016]; musicians’ share of the workforce has hovered around that same level since 1970.

there has been essentially no change in the two-to-one ratio of male to female musicians since the 1970s

The gig economy started with music…. musicians are almost five times more likely to report that they are self-employed than non-musicians

30 percent of musicians currently work for a religious organization as their main gig. There are a lot of church choirs and organists. A great many singers got their start performing in church, including Aretha Franklin, Whitney Houston, John Legend, Katy Perry, Faith Hill, Justin Timberlake, Janelle Monae, Usher, and many others

The Federal Reserve cut interest rates yesterday for the first time since 2019. They raised rates dramatically in 2022 to fight off high inflation, and kept them high since. This cut signals that they are now less worried about inflation, which is now nearing (but not at) their 2% target, and more worried about the slowing (?) labor market. To me their action was reasonable, but doing a smaller cut or waiting longer would also have been reasonable, because the labor market is giving such mixed signals at the moment.

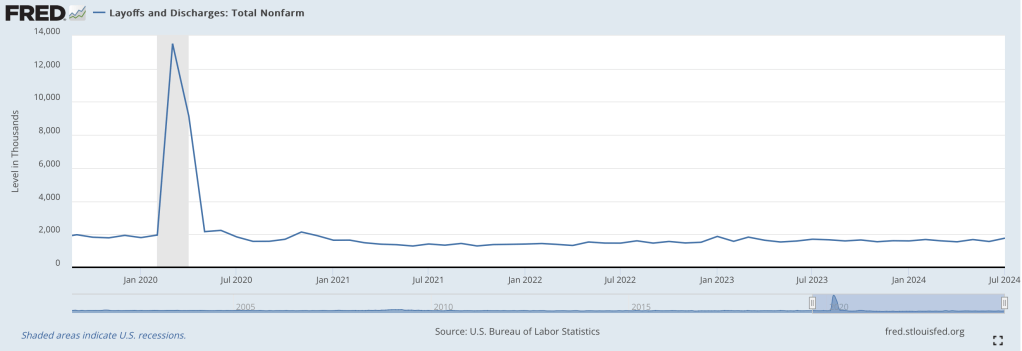

Most concerning is that unemployment increased from 3.5% last July to 4.3% this July. On previous occasions that unemployment in the US increased that rapidly, we then saw recessions and much more growth in unemployment. But unemployment ticked down to 4.2% last month, and layoffs have been flat:

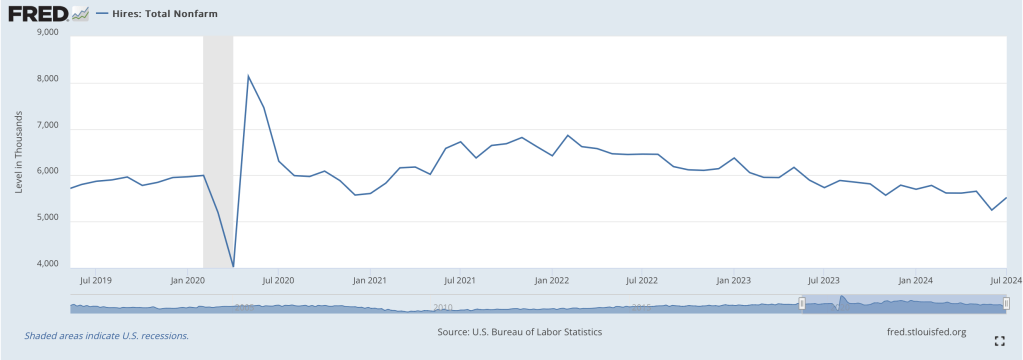

How do you get a big increase in unemployment without a big increase in layoffs? There are two main ways, one good and one bad, and we have both. The bad news, especially for new graduates, is that hiring has slowed:

But the better news is that there are simply more people wanting to work. This is generally a good sign for the economy; in bad economic times many people don’t count as “unemployed” because they are so discouraged that they don’t bother actively looking for work. In July though, prime-age labor force participation hit 84%, the highest level since 2001:

The prime-age employment-to-population ratio just hit 80.9%, also the highest level since 2001:

Labor force participation and employment-to-population among all adults are not so high, though it could be a positive that many people under 25 are in school and many people over 54 are able to retire. Finally, total payrolls got a big downward revision, but one that still implies positive growth every month.

Looking beyond the labor market though, GDP grew at a strong 3.0% in Q2, and is projected to be similar in Q3. Inflation breakevens are exactly on target. Overall it looks like some recession indicators that worked historically, like the Sahm Rule and Yield Curve Inversion, are about to break down- especially now that the Fed cutting is rates.

Cowen’s 2nd Law states that there is a literature on everything. I would certainly expect there to be a literature on the best-selling musician in the world. And of course there is; Google Scholar returns 23,500 results for “Taylor Swift”, and we’ve done 5 posts here at EWED. But surprisingly, searching EconLit returns nothing, suggesting there are currently no published economics papers on Taylor Swift, though searching “Taylor” and “Swift” separately reveals hundreds of articles about the Taylor Rule and the SWIFT payment system. Google Scholar does report some economics working papers about her, but the opportunity to be the first to publish on Taylor Swift in an economics journal (and likely get many media interview requests as a result) is still out there.

Swift presents a variety of angles that could be worthy of a paper; re-recording her masters forcopyright reasons, her efforts to channel concert tickets to loyal fans over re-sellers, or her sheer macroeconomic impact. I’ve added a note about this to my ideas page (where I share many other paper ideas).

In the mean time, I’ll be giving a short talk on the Economics of Taylor Swift at 7pm Eastern on Monday, September 16th, as part of a larger online panel. The event is aimed at Providence College alumni, but I believe anyone can register here.

Update 10/25/24: A recording of the event is here, and a recording of a followup interview I did with local TV is here.

The answer sure seems to be “nothing”. I just went for an eye exam for the first time since Covid and realized that I’ve been wasting my money by paying for vision insurance.

The problem isn’t the eye exam- that went fine, and was covered fine with a $35 copay. But it was covered by my health insurance, not my vision insurance. So what is the vision insurance good for, if it doesn’t cover eye exams?

The answer is supposed to be “glasses”. It is supposed to cover frames up to $150 with a $0 copay, and basic lenses with a $25 copay, from in-network providers. That sounds ok- but there are two problems.

One is that almost none of the in-network providers (like Glasses dot com or Target optical) appear to actually offer lenses where the $25 copay applies; instead the minimum lens price is at least $85.

The second problem is that the premiums are high enough that even if I use them to get $25 glasses (which I eventually found I could through LensCrafters), it wouldn’t be worth it. They don’t sound high at first, which is how I got suckered into signing up for this scam in the first place. It’s just $5/month for single coverage; that sounds like nothing, especially for an employer benefit. It is a rounding error compared to health insurance premiums, and it comes out of pre-tax money. A small waste, but still a waste. Why?

Glasses are just so cheap if you can avoid the monopoly retailers and get them somewhere like Zenni. Zenni will sell you perfectly functional (and IMHO good-looking) prescription eyeglasses for $16. Their frames start at $6.95, lenses at $3.95, and shipping at $4.95. Catch a sale, or order enough to get free shipping, and you could actually get glasses for well under $16.

Or you can do what I did- order glasses from Zenni with premium options that pushed them up to $50- and find it is still cheaper than using the insurance I already paid for to get the cheapest pair available at most of their in-network retailers. The cheapest possible deal with insurance would be to pay $60/year in premiums, get glasses as often as the insurance allows so as not to waste the benefit (every 12 months- much more often than I find necessary), find frames listed under $150 to get for $0 copay, and find an in-network provider that actually offers lenses for the $25 copay. In this best-case scenario you are still paying $85 per pair of glasses. Given that the $60 in premiums came from pre-tax money, perhaps you can argue that it was really more like $40 in real money; but you can also buy glasses from a competitive retailer like Zenni using pre-tax money from an HSA or FSA.

So as far as I can tell, vision insurance really is useless. I certainly decided not to use it for my latest pair of glasses even though I had already paid years of premiums; Zenni was still much cheaper for a comparable product. I’m dropping vision insurance now that open enrollment is here. My take-home pay will be going up, and EyeMed will stop getting my money for nothing.

Is there anyone vision insurance makes sense for? I think it could makes sense for someone who really wants brand name glasses, or for someone who really wants to get their glasses in-person at the optometrist, and wants new glasses every year. For everyone else, run the numbers for your own plan, but I suspect you would also be better off just buying glasses directly.

Disclaimer: This post is not sponsored & doesn’t use affiliate links; Zenni is the best option I currently know of, but I’d be happy to hear of other competitive retailers you think are better, or an argument for when vision insurance is actually useful.

That is the title of a 2020 book by Dierdre McCloskey and Art Carden. It attempts to sum up McCloskey’s trilogy of huge books on the “Bourgeois Virtues” in one short, relatively easy to read book. I haven’t read the full trilogy, so I can’t say how good the new book is as a distillation, but I found that it was easy to read and at least makes me think I understand McCloskey’s basic thesis for why the world got rich. I share some highlights here.

Part 1 of the book aims to establish that the world did in fact get richer over recent centuries, plus give a basic explanation of liberal political thought. If you already know this you could skip this part and cut down an easy 189 page read to a very easy 106 page read (part 1 is for some reason written in a way that assumes you disagree with the authors, which grates when you don’t, or perhaps also if you do).

Part 2 gets to what I at least came for- digging into the history to solve the puzzle of why the Industrial Revolution / Great Enrichment took off when and where it did. Which means first, explaining why many things people think made 18th century England special were actually common elsewhere, like markets:

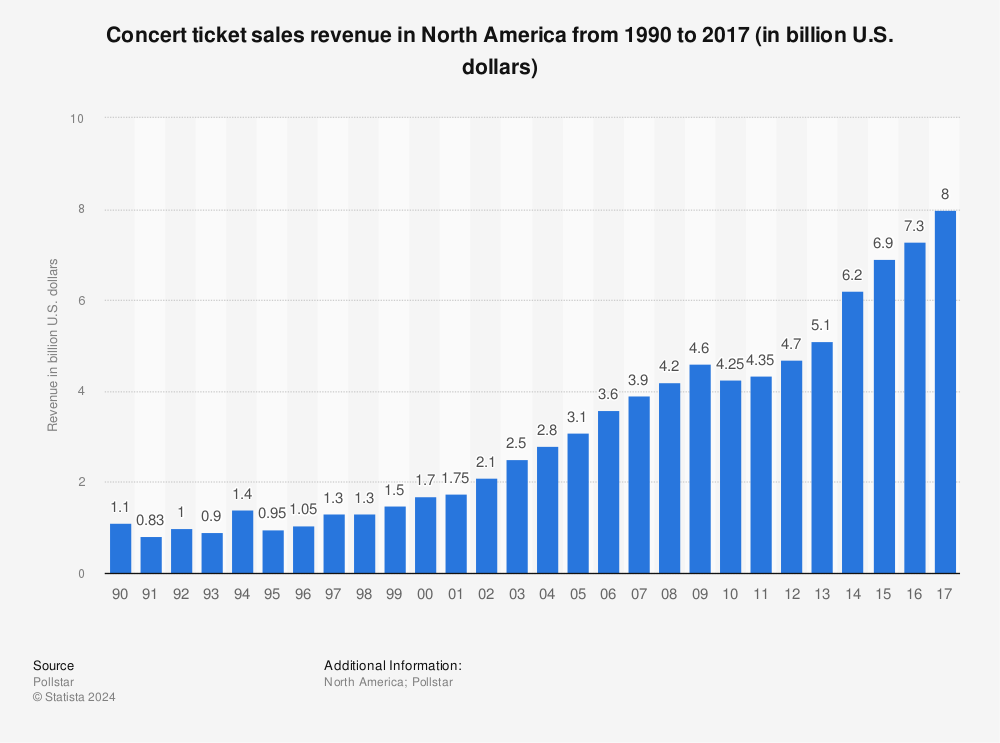

Recorded music sales peaked in 1999- then came Napster and other ways to listen to the exact music you want for free. Recorded music sales still haven’t fully recovered, but with the rapid growth of paid streaming since 2014, they have been increasing again:

Meanwhile, live music sales have exploded since the ’90s:

The latest report from Pollstar on the top live tours is positively glowing:

2023 was a colossus, the likes of which the live industry has never before seen. If 2022 was a historic record-setting year, which it was, then this year completely blew it out of the water— by double digits. Total grosses for the 2023 Worldwide Top 100 Tours were up 46% to $9.17 billion

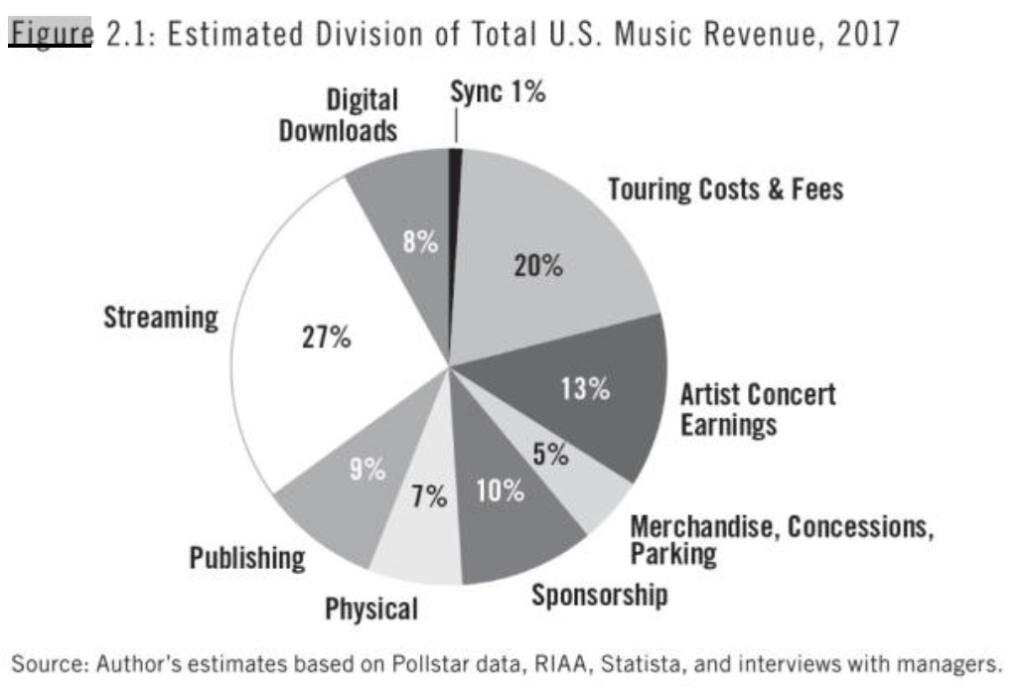

When you combine live and recorded sales, total spending on music has now passed the 1999 peak; this is the biggest the market for music has ever been. Of course, this doesn’t mean its an easy time to be a musician; touring is hard work and, as always, record labels and others are taking a big share of the money before it gets to artists. And opinions differ about whether today’s environment is good for creating good new music.

There are dozens of songs about how the road is hard, and the more time you spend on the road, the less they sound like cliches than like a simple and sometimes stark description of your life. Sooner or later everybody spots the exit that has their name on it –John Darnielle

The BLS data is noisy but suggests that the number of musicians in the US has been fairly flat and is projected to stay that way. A lot will depend on whether live music continues to grow, how much of that is captured by a few superstars, and whether the current streaming paradigm continues, or goes in a more or less artist-friendly direction. But now that consumers are willing to pay for music again, artists at least have a fighting chance.

I just got the new Robinhood Gold credit card after 4 months on their waitlist. It offers 3% cash back on everything- except travel, which is an even better 5%. This seems to be a much better deal than the typical credit card (which offers ~0-1% back in cash or equivalents), and even better than the previous best alternative I know of (the Citi Double Cash, which pays 2% back). So, is there a catch?

As far as I can tell, there are two, but one is minor and the other is avoidable.

The minor catch is that while they advertise the Gold Card as having no annual fee, you need to be a Robinhood Gold member to get it. Robinhood Gold has a $50/year fee, though it comes with other benefits, and getting the extra 1%+ back on the credit card will itself pay for the fee assuming you spend at least $5k/yr on the card.

The potentially major catch, and the reason I assume Robinhood is offering such a good deal, is that they want to entice you to open a brokerage account and to make bad decisions with that account that make them money. Much like a casino that offers you free drinks and cheap hotel rooms in the hope that you will choose to gamble and end up losing way more than the cost of the “complimentary” things they gave you. This is a major risk, but if you know what to avoid you can still come out ahead. The last time my friends dragged me to a casino I got handed plenty of free drinks despite the fact that I never gambled. Similarly, Robinhood might nudge its users to lose money in ways large (options) and small (overtrading with market orders).

But while Robinhood’s interface might suggest these bad choices, it absolutely does not require them. You can simply choose not to enable options trading, not to over-trade (and to turn off price alerts that nudge you to do so), and to use limit orders instead of the default market orders when buying stocks. In fact, you could avoid using Robinhood to buy stocks altogether, and simply use their brokerage account as a way to earn 5% interest while using it to pay off your credit card (though on the other hand, Robinhood could benefit people if it nudges them to do stock investing at all instead of keeping everything in a checking account).

The fact that Robinhood Gold brokerage accounts pay 5% interest on uninvested cash is its other big advantage. You can find savings accounts elsewhere paying 5% or a bit more, but many won’t maintain that rate, and they have transaction limits. Robinhood also pays a 1% bonus on cash transferred in if you keep it there.

Someone moving to the Robinhood ecosystem from a bad setup (paying with cash, or debit cards, or credit cards with no rewards that are paid off from a checking account that earns 0%) could in theory increase their real spending power by 8%+. Even someone in a more common situation (has a 1% rewards card but most of their spending is on things like mortgages that aren’t credit-card-eligible, pays the credit card from a 0% interest checking account but sweeps excess cash to a high-yield savings account paying 4%) could still increase their total spending power 1-3%. Not huge, but a big deal for something that can be set up for less than a days work.

This is now the best single-account setup I know of- assuming you can stay out of their casino. Churning through different accounts can get you a better return, but it is also a lot more work and has its own risks. If you want to up your returns some without the fees or risk of the Robinhood ecosystem, then something like the Citi Double Cash paid from a high-yield (4%+) savings account is probably the way to go.

Disclaimer: I might be wrong about this but if so I am honestly wrong; this post is not sponsored and I’m not even using referral links when I easily could. Still, do your own research and let me know if I’ve missed anything

Update: Robinhood CEO Vlad Tenev did an interview on Invest Like the Best this week where, reading between the lines, he confirms both the positive and negative things I say here. They make most of their money overall on options and active traders; 3% cash back exceeds the interchange fees they get from merchants, but they expect the card to be profitable because some users will carry a balance (and pay interest) and because it will push people to sign up for Gold (so pay fees and perhaps trade more). He notes that there is another card that offers 3% cash back, but it is only available to those with at least $2 million managed by Fidelity.

Despite its many flaws*, I always like to checkinon what the Taylor Rule suggests for the Fed. Its virtues are that it gives a definite precise answer, and that it has been agreed upon ahead of time by a variety of economists as giving a decent answer for what the Fed should do. Without something like the Taylor Rule, everyone tends to grasp for reasons that This Time Is Different. Academics seek novelty, so would rather come up with some new complex new theory of what to do instead of something undergrads have been taught for years. Finance types tend to push whatever would benefit them in the short term, which is typically rate cuts. Political types push whatever benefits their party; typically rate cuts if they are in power and hikes if not, though often those in power simply want to emphasize good economic news while those out of power emphasize the bad news.

The Taylor Rule can cut through all this by considering the same factors every time, regardless of whether it makes you look clever, helps your party, or helps your returns this quarter. So what is it saying now? It recommends a 6.05% Fed funds rate:

Fed Funds Rate Suggested by the Bernanke Version of the Taylor Rule Source: My calculation using FRED data, continually updated here

I continue to use the Bernanke version of the Taylor Rule, which says that the Fed Funds rate should be equal to:

Core PCE + Output Gap + 0.5*(Core PCE – 2) +2

*What are the flaws of the Taylor Rule? It sees interest rates as the main instrument of monetary policy; it relies on the Output Gap, which can only really be guessed at; and it incorporates no measures of expectations. If I were coming up with my own rule I would probably replace the Output Gap with a labor market measure like unemployment, and add measures of money supply shifts and inflation expectations. Perhaps someday I will, but like everyone else I would naturally be tempted to overfit it to the concerns of the moment; I like that the Taylor Rule was developed at a time when Taylor had no idea what it might mean for, say, the 2024 election or the Q3 2024 returns of any particular hedge fund.

That said, people have now created enough different versions of the Taylor Rule that they can produce quite a range of answers, undermining one of its main virtues. The Atlanta Fed maintains a site that calculates 3 alternative versions of the rule, and makes it easy for you to create even more alternatives:

Two of their rules suggest that Fed Funds should currently be about 4%, implying a major cut at a time that the Bernanke version of the rule suggests a rate hike. On the other other hand, perhaps this variety is a virtue in that it accurately indicates that the current best path is not obvious; and the true signal comes in times like late 2021 when essentially every version of the rule is screaming that the Fed is way off target.