The 2025 first quarter GDP data came in slightly bad: negative 0.3%. I think the number is a bit hard to interpret right now, but it’s hard to spin away a negative number. A big factor pulling down the accounting identify that we call GDP was a massive increase in imports, specifically imports of goods. It’s likely this is businesses trying to front-run the potential tariffs (and keep in mind this was pre-“Liberation Day,” so probably even more front running in April), so the long-run effect is harder to judge.

But aside from the interpretation of the GDP estimate, we can ask a related question: did anyone predict it correctly? I have written previously about two GDP forecasts from two different regional Federal Reserve banks. They were showing very different estimates for GDP!

Both the Fed estimates ending up being pretty wrong: -1.5% and +2.6%. But there are two other kinds of forecasts we can look at.

The first is from a survey of economists done by the Wall Street Journal. The median forecast in that survey was positive 0.4%. This survey got the direction wrong, but it was much closer than the Fed models.

Finally, we can look at prediction markets. There are many such markets, but I’ll use Kalshi, because it’s now legal to use in the US, and it’s pretty easy to access their historical data. The average Kalshi forecast for Q1 (a weighted average of sorts across several different predictions) was -0.6%. Pretty close! They got the direction right, and the absolute error was smaller than WSJ survey. And obviously, much better this quarter than the Fed models.

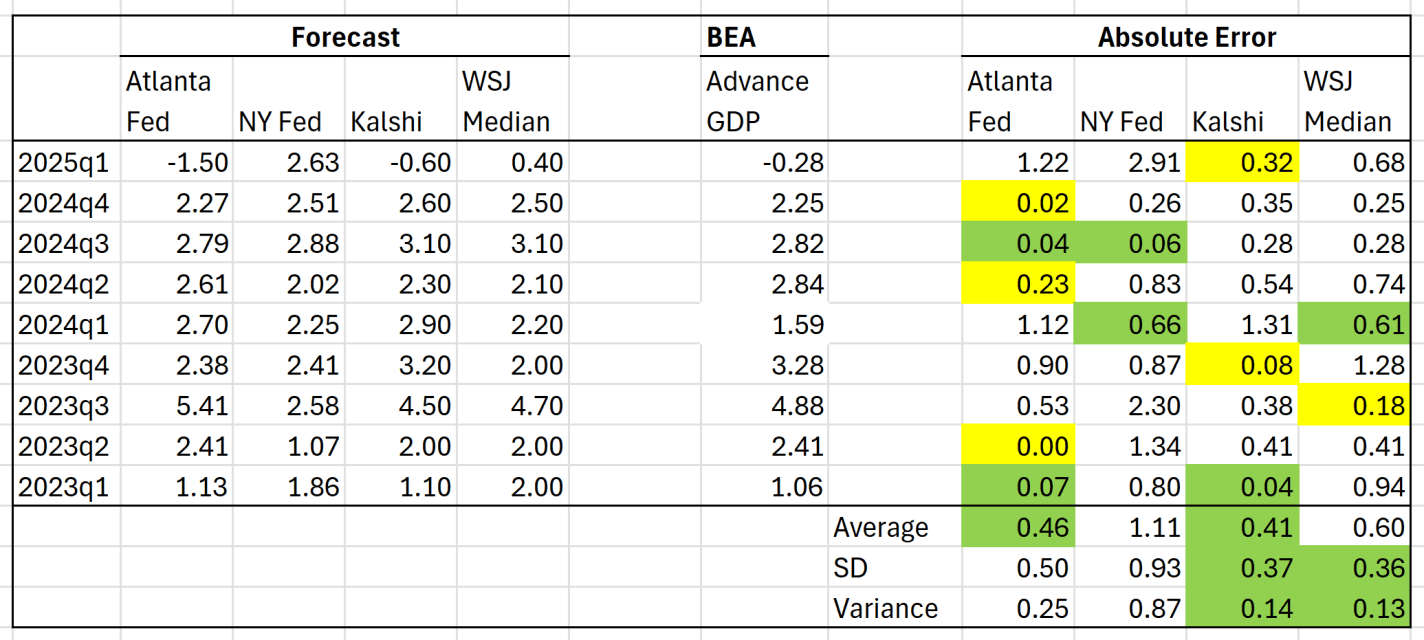

But this was just one quarter, and perhaps a particularly weird quarter to predict (Atlanta Fed even had to update their model mid-quarter, because large gold inflows were throwing of the model). You may say that weird quarters are exactly when we want these models to perform well! But it’s also useful to look at past predictions. The table below summarizes predictions for the past 9 quarters (as far back as the current NY Fed model goes):

Yellow highlighted cells indicate it was the best prediction that quarter among these four options (best defined as lowest absolute error, not direction). Green highlighted cells are when two of the four essentially tied (no hard rule here, just my judgement). For the Atlanta Fed in the most recent quarter, I use their “gold adjusted,” which going forward is their preferred model.

The Atlanta Fed model seems to be the best. It’s either the best or tied for the best in 5 of the 9 quarters, and in four of those quarters it is almost right on (less than 0.1 error). The NY Fed model is tied for the best in 2 quarters, but never alone as the best forecast. Kalshi is the best twice (and tied once), and the WSJ survey are the best alone just once and tied once. For the average absolute error, the Atlanta Fed and Kalshi are about the same (though if you don’t use the gold-adjusted model for the Atlanta Fed in 2025q1, their average error goes up to 0.59).

The standard deviation of the errors is lowest for Kalshi and the WSJ survey (0.37 and 0.36), so perhaps that’s another argument in favor of Kalshi over the Atlanta Fed: similar average error, lower standard deviation.

Perhaps we can average across these forecasts to beat any single one of them? Not obviously so. Average the Atlanta Fed model and Kalshi forecast, it can only beat the Atlanta Fed alone in 3 of the 9 quarters (and basically tying in one), and the average error isn’t much better than either one alone (about 0.39). Averaging across the Atlanta Fed, Kalshi, and WSJ forecasts is a little better, but still only clearly beats the Atlanta Fed model in 4 of 9 quarters. The first average (Atlanta Fed and Kalshi) has the lowest standard deviation (0.31) of all of these possible combinations.

Putting the NY Fed forecast into any of these averages makes the forecast worse. A weighted average of two forecasts, such as 40% Atlanta Fed and 60% Kalshi, doesn’t improve much on a simple average either.

While considering all methods is useful, if you are going to follow just one model, the Atlanta Fed GDPNow model is a fine one to follow, even if it was off a bit in 2025q1 (despite tweaking the model mid-quarter!). But there is an argument for Kalshi as well: even though it rarely gets it exactly right, the errors are low and the variance of the errors is low.

A simple weighted average of Atlanta/Kalshi/WSJ is the best if you want to minimize the variance: the mean error is 0.4, while the standard deviation is 0.31 and the variance is 0.098.

Your analysis is wrong for 2023Q4: Kalshi should be yellow there with just 0.08 error.

LikeLike

Thank you! I have fixed it.

LikeLiked by 1 person