Jerome Powell’s term as Fed Chair ends in late May 2026. President Trump has said that he will nominate a new chair and the US senate will confirm them. It may take multiple nominations, but that’s the process. The new chair doesn’t govern monetary and interest rate policy all by their lonesome, however. They have to get most of the FOMC on board in order to make interest rate decisions. We all know that the president wants lower interest rates and there is uncertainty about the political independence of the next chair. What will actually happen once Jerome is out and his replacement is in?

The treasury markets can give us a hint. The yields on government debt tend to follow the federal funds rate closely (see below). So, we can use some simple logic to forecast the currently expected rates during the new Fed Chair’s first several months.

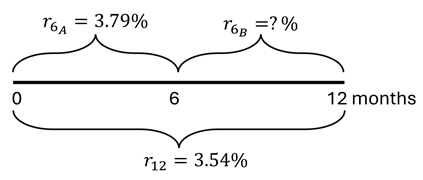

Here’s the logic. As of October 16, the yield on the 6-month treasury was 3.79% and the yield on the 1-year treasury was 3.54%. If the market expectations are accurate, then holding the 1-year treasury to maturity should yield the same as the 6-month treasury purchased today and then another one purchased six months from now. The below diagram and equation provide the intuition and math.

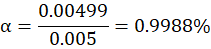

Since the federal funds rate and US treasury yields closely track one another, we can deduce that the interest rates are expected to fall after 6 months. Specifically, rates will fall by the difference in the 6-month rates, or about 49.9 basis points (0.499%). This cut is an expected value of course. Given that the cut is between a half and a zero percent, we can back out the market expectation of for a 0.5% vs 0.0% cut where α is the probability of the half-point cut.* Formally:

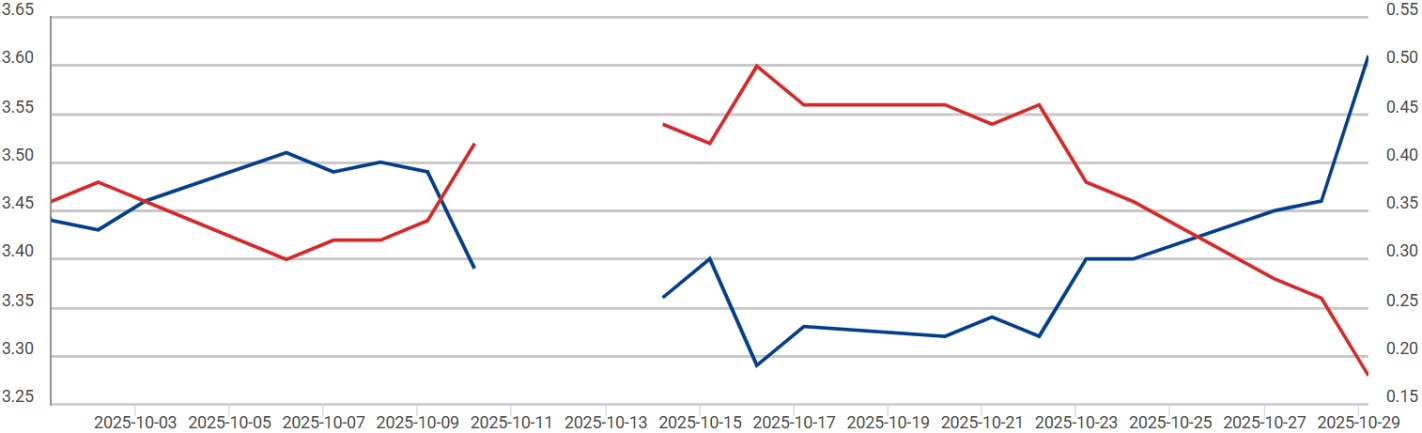

As of October 16, markets were 99.88% confident that interest rates would be cut by half a percent around Jerome Powell’s departure. Conveniently, however, we can track these expectations in real-time by watching how these numbers change each day. Let’s see how these expectations have changed throughout October. Below is the forward 6-month treasury rate implied by the October six and 12-month yields (left axis, Blue). Just as above, this forward rate implies a rate change relative to the average rate over the next six months – a rate cut (right axis, Red). With the most recent federal funds cut on the 29th, the market predicts less difference between rates over the next six months versus the following six months. The expected difference as of the 29th was only 18 basis points (0.0018%).

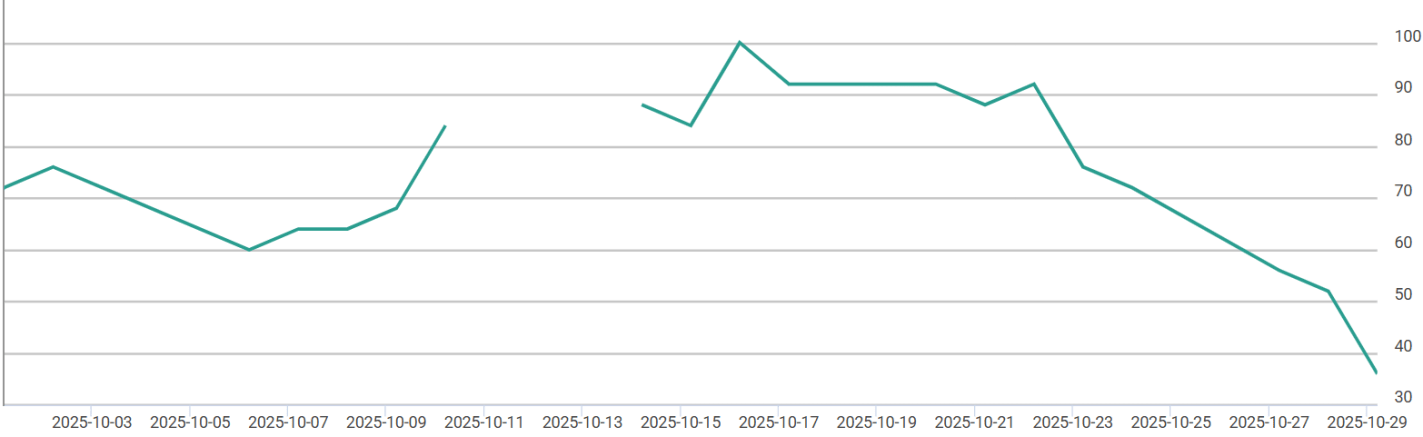

With the recent cut, the forecasted additional cuts to occur 6 months from now are less than 25bp. For the sake of consistency, we can identify the probability of a 0.5% cut vs a 0% cut. That’s exactly what the below chart depicts: The probability of a half-point cut near the end of Powell’s term. As of mid-October it was a foregone conclusion. But with the recent cut, the probability of a 0.5% cut is only 36%. Another, probably more valid interpretation is that the probability of a 0.25% cut is placed at 72% versus zero. The point is, the expected magnitude or probability of future cuts has substantially subsided.

What Does It Mean?

Markets may or may not provide good forecasts. While it’s true that they have a profit incentive to get it right, they can’t know the future. If they are mostly right, then we should not expect big policy changes when Jerome Powell leaves his position. Interest rate policy is approaching the forecasted rates, reducing the expectation for bigger cuts occurring 6-12 months from now. This means that Powell is loosening faster than anticipated. It also means that markets are relatively placid about the impact that president Trump’s nominee and future chair will have on policy.

*There are many possible interest rates, so this is a simplification down to two possibilities.