I’ve taught GT a total of 5 time. Below are my average student course evaluations for “I would recommend this class to others” and “I would consider this instructor excellent”. Although the general trend has been improvement, improving ratings and the course along the way, some more context would be helpful. In 2019, my expectations for math were too high. Shame on me. It was also my first time teaching GT, so I had a shaky start. In 2020, I smoothed out a lot of the wrinkles, but I hadn’t yet made it a great class.

In 2021, I had a stellar crop of students. There was not a single student who failed to learn. The class dynamic was perfect and I administered the course even more smoothly. They were comfortable with one another, and we applied the ideas openly. In 2022, things went south. There were too many students enrolled in the section, too many students who weren’t prepared for the course, and too many students who skated by without learning the content. Finally, in 2023, the year of my changes, I had a small class with a nice symmetrical set of student abilities.

Historically, I would often advertise this class, but after the disappointing 2022 performance, and given that I knew that I would be making changes, I didn’t advertise for the 2023 section. That part worked out perfectly. Clearly, there is a lot of random stuff that happens that I can’t control. But, my job is to get students to learn, help the capable students to excel, and to not make students *too* miserable in the process – no matter who is sitting in front of me.

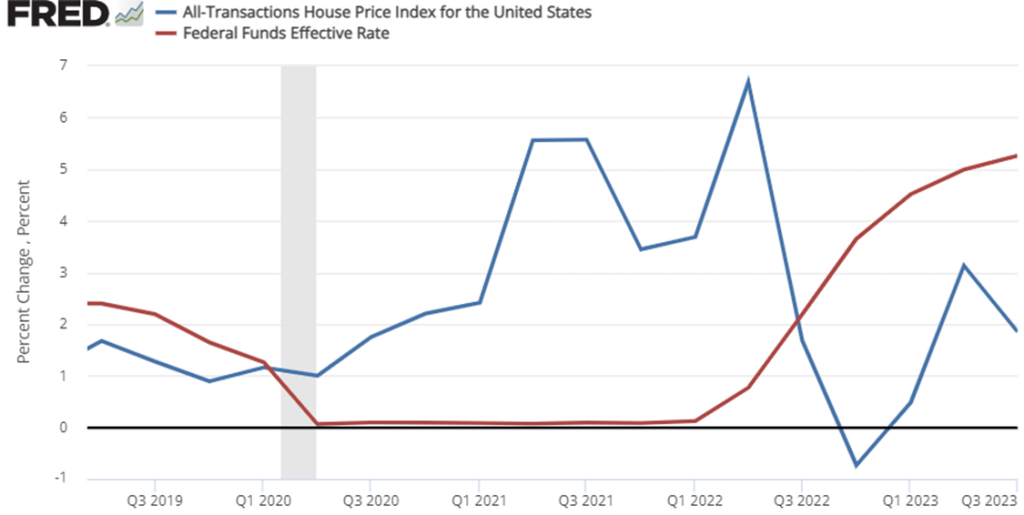

The third quarter ‘All Transaction’ housing price data was just released this week. These numbers are interesting for a few of reasons. One reason is that home prices are a big component of our cost of living. Higher home prices are relevant to housing affordability. This week’s release is especially interesting because it’s starting to look like the Fed might be pausing its year 18-month streak of interest rates hikes. In case you don’t know, higher interest rates increase the cost of borrowing and decrease the price that buyers are willing to pay for a home. Nationally, we only had one quarter of falling home prices in late 2022, but the recent national growth rate in home prices is much slower than it was in 2021 through mid-2022.

Do you remember when there were a bunch of stories about remote workers and early retirees fleeing urban centers in the wake of Covid? We stopped hearing that story so much once interest rates started rising. The inflection point in the data was in Q2 of 2022. After that, price growth started slowing with the national average home price up 6.5%. But the national average masks some geographic diversity.

I’ve written about government spending before. But not all spending is the same. Building a bridge, buying a stapler, and taking from Peter to pay Paul are all different types of spending. I want to illustrate that last category. Anytime that the government gives money to someone without purchasing a good or service or making an interest payment, it’s called a ‘transfer’. People get excited about transfers. Social security is a transfer and so is unemployment insurance benefits. Those nice covid checks? Also transfers.

Here I’ll focus on Federal transfers, though the data on all transfers is very similar if you include states in the analysis. Let’s start with the raw numbers. Below is data on GDP, Federal spending, and federal transfers. Suffice it to say that they are bigger than they used to be. They’ve all been growing geometrically and they all exhibit bumps near recessions.

Austrian economists rightfully have some gripes about mainstream macroeconomics – specifically about aggregation. The conventional wisdom says that a fall in output can be prevented or remedied in the short-run by an expansion of total spending (via increasing the money supply). Total output is stabilized and the crisis is averted. Even if rising spending preceded the output decline, the standard prescription is the same.

The Austrian Business Cycle theory says that, actually, the prior expansion in spending resulted in yet-to-be-realized poor investments due to easy credit. The decline in output is self-inflicted by unsustainable endeavors, and the money supply expansion response prevents the correction. The consequence is more malinvestment. The Austrians say that the focus on gross investment is a misleading aggregation and commits the fallacy of composition that all investment is the same or the same on relevant margins.

Both schools of thought are on firm ground. I don’t see them as conflicting. They both make valid points and are correct about the world. The conventional wisdom is able to paper-over short-run hiccups, and the Austrians recognize that resources are suboptimally allocated. The two sides are talking past each other to some extent.

The market process of seeking profits and satisfying consumer demands is a messy process. Prices and profits (and losses) incentivize firms with information that they use to adjust their behavior. They innovate and reallocate resources from bad projects and toward money-making projects. When firms earn negative profits (a loss) they learn that their understanding of the world was wrong and that they malinvested their scarce resources. Therefore, malinvestment is a standard and *necessary* part of the market process of identifying and serving the changing and unknown demands of individuals. Without malinvestment we lack the necessary information to distinguish success from failure.

Mal-investment is harmful insofar as it represents resources that were invested such that future output did not rise as it could have otherwise. So, while malinvestment is necessary to the market process, a preponderance of it makes us poorer in the future. Luckily, firms have incentives and finite resources such that mal-investment remains somewhat tamed. Indeed, malinvestment is the cost that we bear for innovation and identifying what works.

The issue is that the above discussion is oriented to the long-run. The conventional wisdom is oriented toward resolving the short-run threats. The two meet one another when malinvestment realizations occur in a correlated manner. It’s not that policy causes malinvestment. Rather, depressed interest rates and easy credit prevent firms from identifying which of their projects turned out to be more or less productive. Firms persist in bad investments because they can’t discriminate between the failed and successful projects ex ante.

So, when interest rates suddenly rise, low or negative productivity projects are identified and resources are reallocated. The discovery and reallocation process takes time. And if many projects are found to be failures at once, then the result is a drop in economic activity that is detectable at the aggregate level. The problem is not that malinvestment exists. The problem is that malinvestment was permitted to persist and grow such that the eventual realization of losses is correlated and has macroeconomic effects. We observe spending, output, and employment declines. That’s the ‘business cycle’ part of the Austrian Business Cycle. Interest rates rising helps to identify the bad projects. That’s good. But policy that increases the popularity of bad projects is bad. It makes us poorer in the long-run and more vulnerable to declines in the short-run.

I keep reading and hearing people who are waiting for the shoe to drop on the next recession. They see high interest rates and… well, that’s what they see. Employment is ok and NGDP is chugging along.

One indicator of economic trouble is the delinquency rate on debt. That’s exactly what we would expect if people lose their job or discover that they are financially overextended. They’d fail to meet their debt obligations. But the broad measure of commercial bank loans is quiet. Not only is it quiet, it’s near historic lows in the data at only 1.25% in 2023Q2. Banks can lend with a confidence like never before.

But maybe that overall delinquency rate is obscuring some compositional items. After all, we know that many recessions begin with real-estate slowdowns. Below are the rates for commercial non-farmland loans, farmland loans, and residential mortgages. All are near historical lows, though there are hints that they’re might be on the rise. But one quarter doesn’t a recession make. I won’t show the graph for the sake of space, but all business loan delinquency rates have also been practically flat for the past five years.

Do you know someone who likes practical gifts? Then these timely recommendations are for you given that Christmas is on the horizon. If none of the below recommendation strike your fancy, then there’s also the list that I made last year. The nice thing about practical gifts is that they tend to remain good gifts from year after year. This year’s list mostly concerns home-goods.

I didn’t build my house. And whoever installed the light fixtures had the poor foresight of choosing ones with candelabra bulbs (smaller bulbs with smaller plugs). They are much less bright. I like a nice bright room because it makes everything feel cleaner, neater, and there’s always enough light. I can always provide accent lighting with lamps, but the overhead light needs to – well – enlighten the room. I found these 800 lumen candelabra bulbs and they are pricey, but they are better than the daily resentment of a disappointing overhead light.

If you liked last year’s custom length Velcro recommendation, then you’ll also like this year’s worm-gear clamps. Have you ever needed a heavy-duty fix that’s also fast and easy? It’s the same clamp that’s used in to affix dryer exhaust ducts. It’s great for any project that needs a quick and secure solution. It’s super easy if you have a drill, and relatively easy if you just have a screwdriver. I used mine for some mechanical elements of my golf card.

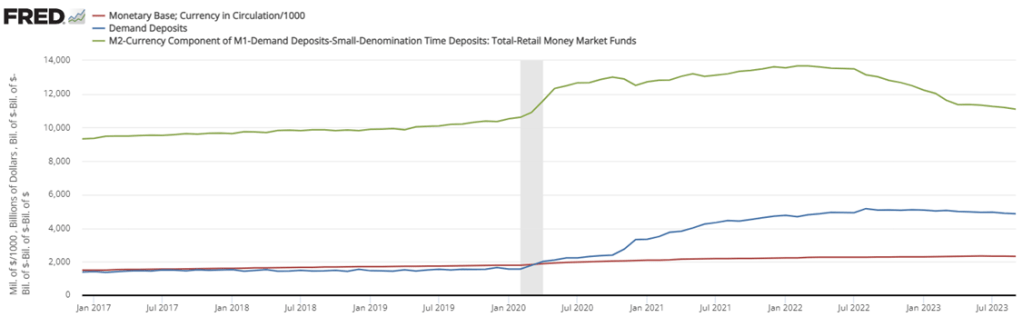

Money and interest rates have been in the news because the Fed wants to slow the rate of inflation, maintain financial stability, and avoid a recession. Let’s break it down. First, some broad context. The M1 and M2 were all chugging along prior to 2020. M2 was growing along with NGDP and, after raising interest rates, the Fed had begun lowering them again. Then Covid, the stimuli, and the redefinition of M1 happened. Now, we’re trying to get back to something that looks like normal. See the graphs below.

But these aggregates gloss over some relevant compositional changes. Let’s go one-by-one.

The monetary base includes both bank reserves and currency in circulation. We could break it down further, but I’ll save that for another time. What we see is that while currency in circulation did grow faster post-covid, it was nothing compared to the growing reserve balances. From January to May of 2020, currency grew by 7.5% while reserves almost doubled. That means a few things. 1) People weren’t running on banks. Covid was not a financial crises in the sense that people were withdrawing huge sums of cash. 2) Banks were well capitalized, safe, and stable. Further, uncertainty aside, banks were ready to lend. And they did. Not long after the recession, everyone and their brother was re-financing or taking on new debt. More recently, we can see that currency has stabilized and, again, most of the action has been in reserve balances. As of September 2023, reserve balances are down 23% from the high in September 2021.

The thing about the monetary base, however, is that reserves don’t translate into more spending unless the reserves are loaned out. The money supply that people can most easily spend, M1, is composed of currency held outside of banks, deposit balances, and “other liquid deposits” (green line below).* See the graph below. Again, most of the action wasn’t in the physical printing of hard, physical cash. People’s checking account balances ballooned thanks to less spending on in-person services and thanks to the stimulus checks and other relief programs. Deposit balances more than doubled from January to December of 2020. Ultimately, deposit balances were 3.3 *times* higher by August of 2022. Since then, the balances have been on a slow, steady decline of about 5.8% over the course of the year. But even then, it’s those “other” deposits, previously categorized as M2, where most of the action is. The value of those balances have fallen by a whopping 2.5 *trillion* and 19% dollars in the past 18 months. People are drawing down their savings.

Finally, we get to M2, the less liquid measure of the money supply. Besides the M1 components, it also includes small time deposits, such as CD’s, and money market funds (not including those held in IRA and Keogh accounts). Money market funds and small time deposits have *increased* in value since the post stimulus tightening as people chase the allure of higher interest rates on offer. Measured by volume, the declines in the broad money supply have darn near all come from declines in M1 (again, the jump is redefinition). And of that, it’s almost entirely coming out of “other” liquid deposits, as illustrated above. That’s savings balances. It’s true that there is some other-other balances, but it’s mostly savings accounts.

Zooming in on just those “other” balances (below left), people still have higher balances than they did prior to the pandemic. But by now, they’re below the pre-pandemic trend. Savings accounts are depleted. However, since many people don’t use savings account anymore due to the decade plus of low interest rates, it’s appropriate to consider both “other” accounts and demand deposits (below right). By that measure, we still have plenty of post-Covid liquidity at our disposal.

*Other liquid deposits consist of negotiable order of withdrawal (NOW) and automatic transfer service (ATS) balances at depository institutions, share draft accounts at credit unions, demand deposits at thrift institutions, and savings deposits, including money market deposit accounts.

PS. So where is all this above-trend NGDP coming from, if not the money supply? Hmmmm.

Alfred Hitchcock’s ‘Psycho’ famously omits graphic violence. You never see the bad guy stab anyone – though it’s heavily implied. Some say that this accounts for the impact of the film. The most thrilling parts are left to the viewer’s imagination. And a person’s imagination can be pretty terrifying. The delight of the unseen was especially appropriate at a time of 13 inch televisions and black-and-white movies. If the graphics on the screen couldn’t carry the movie, then the graphics in a person’s mind would do the trick.

Fast forward to ‘Burn Notice’. I don’t watch this show, but my in-laws do. They have a huge TV with a super high resolution. The TV has a diagonal span that almost surpasses my height. I’m short, but not that short. This is a big TV. I’ve only seen Burn Notice at their house. It strikes me as poorly acted, poorly written, and self-serious to the point of absurdity. I keep expecting that self-referential nod to the open secret that the show is ridiculous, but it never comes. It’s a bad show. From all that I can see in high definition, there’s nothing worth seeing.

What is so good that I watch? Although I’m seven years late, I’ve recently been watching Marvel’s Luke Cage. Being a superhero show, some of the standards are lowered. The script is weak at times, the acting is OK, and the plot has some credibility holes. But the point of the show is to explore a world in which superheroes exist, and one of them happens to live in Harlem. Luke Cage is part of the earlier Marvel cadre of post-acquisition-by-Disney shows that also includes Iron Fist, Daredevil, & Jessica Jones. These shows are less tongue-in-cheek and comedic than the later shows like Loki, Wandavision, or Moon Knight. I enjoy watching Luke Cage on a small 40 inch television, and occasionally on my phone.

Then I stayed at an Airbnb last weekend that had a HUGE TV. This thing easily had a diagonal measure that surpassed my height. After getting the kids down and answering emails, I sat down to enjoy my current go-to show before hitting the hay. And dang it if I wasn’t distracted the entire time. On this massive screen I could see every pore on everyone’s face and every blank stare parading as acting. I could see each and every glare of poor lighting and every character’s ill-timed reply and change of expression. Most of the show is one big charade.

Much to my dismay, I had discovered that I was watching ‘bad tv’. Let me be clear. I’m not supposed to watch bad tv. That’s the realm of those other people. But me? I have enlightened preferences and a refined pallet. I’m not a person who watches bad tv. But that grandiose self-conception has been dashed by this serendipitous visit to a nice Airbnb.

I’ve had some time to dwell on my new revelation and this is what I’ve settled on. First, I’m going to keep watching Luke Cage on my small TV and I’m going to enjoy it. There is little that I can do now about the nagging knowledge that, given a higher resolution, it’s not a good show. You can’t unknow things. Second, maybe Burn Notice isn’t a bad show. Maybe it’s just a bad show when I can see too much detail, such as on my in-law’s TV. Maybe I would enjoy it on a TV with lower resolution. Regardless, I’m not going to watch it.

Third, now I have a new margin of preference over shows and movies. Now I consider whether a show or movie would be helped or hurt by more visual detail. Quick-paced, big-budget action shows like Jack Ryan are probably better in greater detail. Game of Thrones is probably better as a 4k experience. But shows in which the comedy or the drama unfolds by virtue of the circumstances, rather than the visual spectacle, are probably best watched at a lower resolution. When the audience experience hinges on implications and connections that occur in the viewer’s mind, that’s probably a better show at a lower resolution. Luke Cage is a ‘good’ show in low-res. In high-res, I’m afraid that see too much.

When Hitchcock omitted visual detail, he leaned on the mind’s eye to fill in the gaps. He was guiding the brain toward conjuring the unnerving scenes that he could not as easily mimic on screen. Advances in home entertainment have moved the goalpost. A more detailed viewing experience changes the type of shows that we are willing to watch because we have a new criteria for fitness. The supply side response on the part of studios is that shows lacking visual stimulation will need to lean more on the mind’s eye and our interpretations of social interactions in order to for audiences to experience the best version of the show. Because the best version won’t be in front of us. We know too much.

I don’t like when celebrities are ‘caught’ saying deplorable things in a heated moment. Sometimes they say really awful things, specifically about observables such as race, weight, sex, nationality, odor, etc. Plenty of people have done it. I won’t mention the names or link to any particulars here.

My problem isn’t that I wish celebrities had better behavior – although I do. My problem is with the entire fallout of how we’re all supposed to take the celebrity seriously when they were enraged. When people get angry they say things that are designed to hurt others. People will say things that they don’t mean or wouldn’t normally say. And it’s not like they are betraying some unspoken belief that they’ve hidden. Angry people often say wicked things for the sole purpose of hurting someone else’s feelings. In the moment, the offender tries hard to communicate disrespect – not due to a lack of respect – but due to how it will make the other person feel.

I find the entire circumstance weird. If someone is boiling over and saying patently ridiculous things to me and calling me names, then I have a very hard time taking them seriously. All the same, context matters and words can hurt. It’s weird that we know that people can say untrue things in order to hurt us, and then it actually hurts us. Strange.