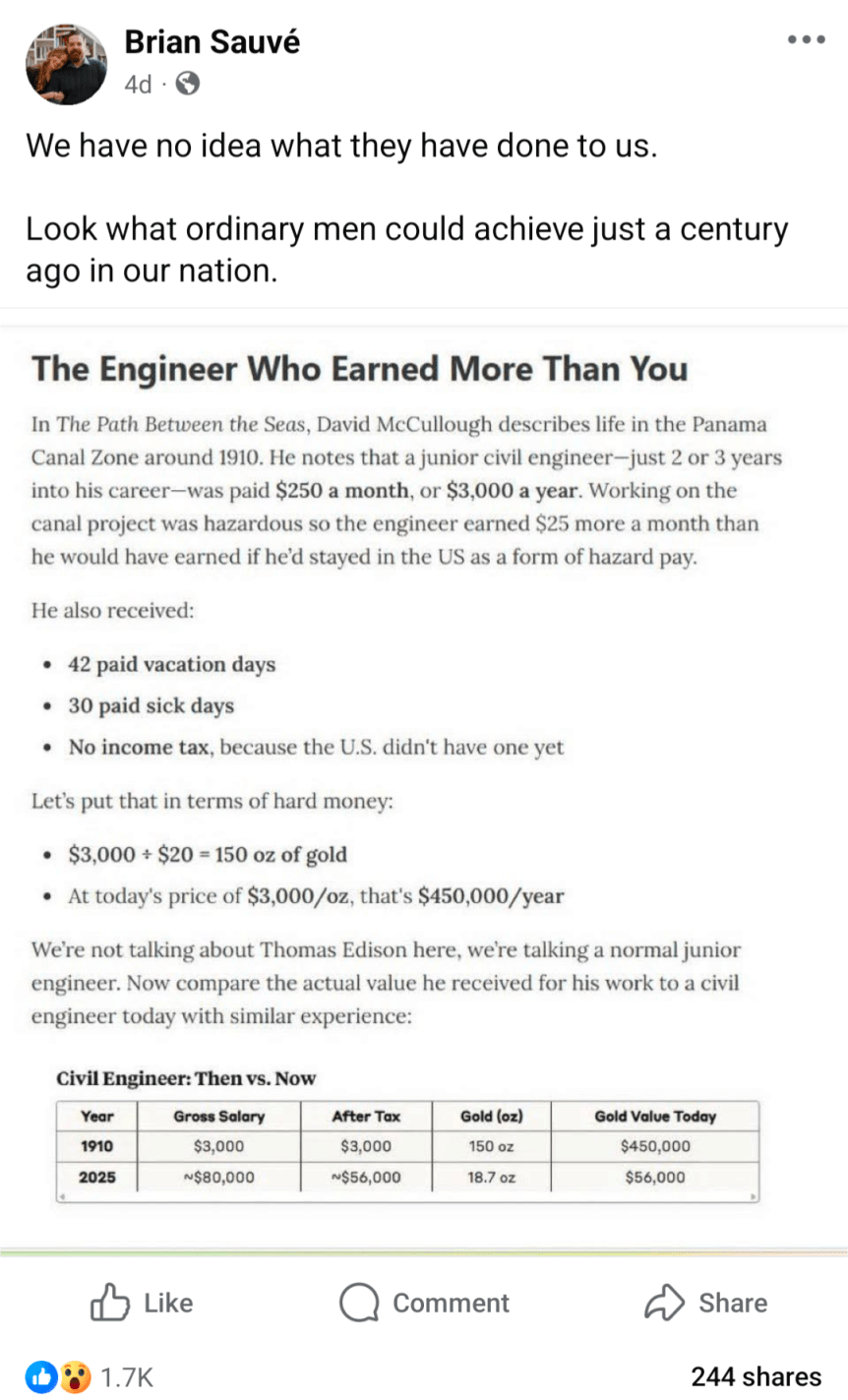

Inflation adjusting income and prices from the past is a common theme in my blog posts, including fact checking of other attempts to do these adjustments. But here is a really novel one, in a viral post from Facebook (which comes from this essay), which claims that a civil engineer earned the equivalent of $450,000 in today’s terms:

Can this be correct? If so, it would represent massive stagnation in incomes over time. Thankfully, there are two major errors, or at least misleading aspects to the calculation.

The listed salary was not one of an “ordinary man” — far from it.

Using gold prices to inflation adjust the incomes is very misleading.

First, the salary: $3,000 per year was definitely not what ordinary men earned. The average wage, for example, for a production worker in manufacturing was 18 cents per hour. You would need to work almost 17,000 hours to earn $3,000 at that wage, which of course is not possible. In reality, the average worker put in 57 hours per week — which means they earned about $500 if they were able to work 50 weeks per year (most probably didn’t). So already we see that the civil engineer working on the Panama Canal is making about 6 times as much as an “ordinary man.” Agricultural workers, the other main industry of 1910, earned about $28 per month ($22 if they also received board) — even less than manufacturing, and only about 1/10 of the engineer

Second, the gold price adjustment is misleading. Yes, in 1910, gold was how we defined currency in the US. But you can’t eat gold, and most people only keep a little gold on hand that can be described as providing services for them (such as jewelry). What people really wanted were real goods and services, and mostly goods. Around 1910, the average American household spent about 40% of their income on food, 23% on housing, and 15% on clothing. Comparing standards of living over time requires us to look at what people spend their money on, not what the currency is denominated in. And that’s what a good consumer price index does: it compares the prices of all consumer spending at different points in time, not just one thing like gold, allowing us to make rough comparisons of income over time.

Using the Measuring Worth historical CPI (which extends the BLS CPI back before 1913), we see that the index was 9.21 in 1910, and it stands at 323.364 in August 2025. So the 18-cent manufacturing wage from 1910 is roughly equivalent to $6.32 in current dollars. The average manufacturing wage today? Around $29. And of course, workers today have a whole range of fringe benefits, worth roughly another $13.58 for private sector workers. This means that an “ordinary man” today working in manufacturing can buy 5-7 times as many real goods and services as his 1910 counterpart for each hour he works. And the work is, of course, much safer today: BLS reports 23,000 industrial deaths in 1913 (61 deaths per 100,000 workers), but only 391 manufacturing deaths in 2023 (0.003 deaths per 100,000 workers).

But what about that extraordinary man in 1910, the civil engineer? How was he doing compared with today? Using the same historical CPI, we can see that $3,000 in 1910 is roughly equivalent to $105,000 today. Not bad! That’s almost exactly the median pay for civil engineers today. But keep in mind the civil engineer working in Panama was an unusually highly paid position. A 1913 report from the American Society of Civil Engineers suggests that most early career civil engineers were making closer to $1,500 per year — half of the Panama engineer. Engineers were also a highly skilled, very rare profession in 1910. And don’t forget that about 10% of the American workers on the Canal died in the construction, mostly from disease so the engineers were probably just as susceptible to death as the laborers.

Finally, we might ask a different question: what if you had held onto gold since 1910? Let’s say your great-great grandfather was a civil engineer, and managed over the course of a few years to save one year’s salary in gold. He even managed to hide it during the 1930s-1970s, when private holding of gold was generally illegal in the US.

How much would that 150 ounces of gold be worth today? That answer is simple: about $615,000 today (gold has gone up a bit just since that calculation was done in May!). But was that a good investment? Not really. A $3,000 investment in the stock market from 1910 to 2024 would be worth about… $120 million (it’s actually a bit more than that, since the market continued to rise after January 2024). Of course, that would have required a bit of active management, since index funds don’t come along until much later. But your great-great grandfather would have been much wiser to set up a trust for you and have it actively managed to approximate the entire US stock market, rather than to bury 150 ounces of gold in his backyard.

Even assuming you lost half the value to management fees, the stock portfolio today would be worth at least 100 times as much as the gold.

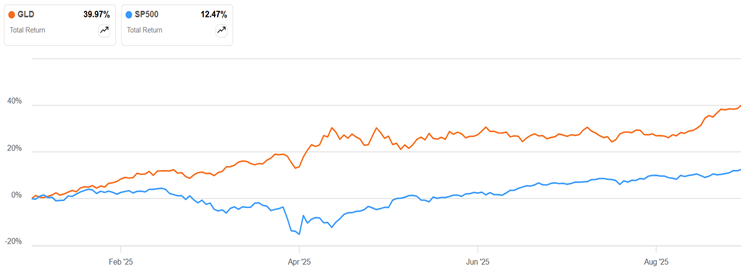

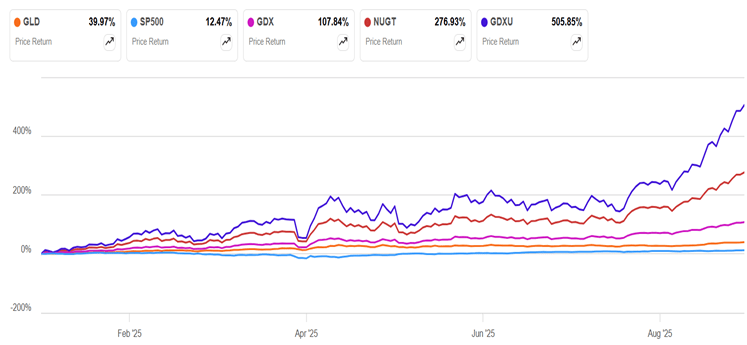

Stocks (e.g., S&P 500) are up 12.5 % year to date. That is pretty good for 9.5 months. But gold has been way better, up 40%:

Fans of gold cite various reasons for why its price should and must keep going up (out of control federal debt and associated money-printing, de-dollarization by non-Western nations, buying by central banks, etc.). I have no idea if that is true. But if it is, that raises the question in my mind: for the limited amount of funds I have to invest in gold, can I get more bang for my investing bucks, assuming gold continues to rise?

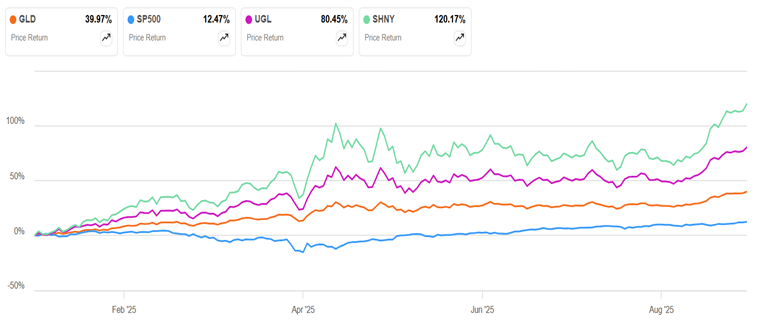

It turns out the answer is yes. A straightforward way is to buy into a fund which is 2X or 3X leveraged to the price of gold. If gold goes up 10%, then such a fund will go up 20% or 30%. Let’s see how two such funds have done this year, UGL (a large 2X gold fund) and a newer, smaller 3X fund, SHNY:

Holy derivatives, Batman, that leverage really works! With GLD (1X gold) up 40%, UGL was up 80% year to date, and 3X SHNY is up 120%. So, your $10,000 would have turned into $24,000. The mighty S&P500 (blue line) looks rather pitiful in comparison.

But wait, there’s more. Let’s consider gold “streamers”, like WPM (Wheaton Precious Metals) or FNV. They give money to mines in return for a share of the production at fixed, discounted prices, so their cash flow soars when gold prices rise. Year to date, FNV is up 73%, while WPM is up 91%.

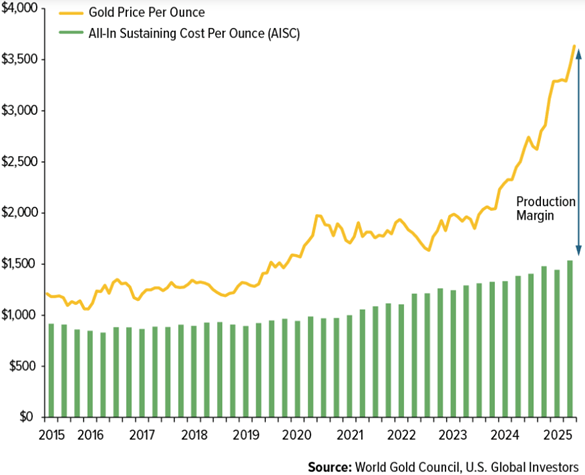

And then there are the gold miners themselves. They tend to have fairly fixed breakeven costs of production, currently around $1200-1400/oz. Again, their profit margin rockets upward when gold prices get far above their breakeven:

GDX is a large fund of representative mining stocks. For icing on the cake, there are funds that are 2X (NUGT) or 3X (GDXU) leveraged to the price changes in mining stocks. The final chart here displays their year-to-date performance in all their glory:

The blue S&P 500 line is lost in the noise, and even the orange 40% GLD line is left in the dust. The 1X miner fund was up 108%, the 2X fund NUGT was up 276%, and the 3X GDXU was up 506%. Your $10,000 would have turned into $51,000.

Of course, what goes up fast will also come down fast, since leverage works both ways. For instance, from Oct 21 to Dec 30, 2024, gold was down a mere 4%, but WPM was down 15%, the 1X gold miner GDX was down 20%, and 3X GDXU down an eye-watering 54%. That means that your $10,000 turned into $4,600 in two months. Imagine watching that unfold, and not panic-selling at the bottom. Gold fell by more than half between 2011 and 2015. If it fell by even 20% (i.e., gave up half of this year’s gains), I could see a 3X miner fund losing over 90% of its value (just a guess).

One more twist to mention here is the “stacked” fund GDMN, which uses derivatives to be long 1X gold PLUS 1X gold miners. It is up 151% this year, which is nearly four times as much as gold. This fund seems to have a nice combination of decent leverage with moderate volatility. It has on average kept pace with the 2X miner fund NUGT, with shallower dips. NUGT has surged way ahead in the past two months as miner stock prices have gone nuts, but that is somewhat exceptional.

Disclaimer: As usual, nothing here should be considered advice to buy or sell any security.

Arrrr, me hearties! What think ye of a venture to raise a gigantic hoard of sunken treasure?

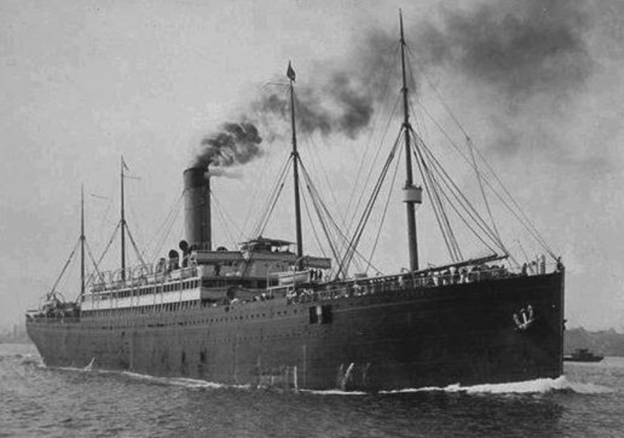

The story begins with the last voyage of RMS Republic. This was a luxurious passenger steamship of the White Star Line, which sailed between Europe and America.

Republic was a large vessel (15,000 tons displacement) for her day, and was known as the “Millionaires’ Ship” for the number of wealthy Americans who sailed back and forth on her. A number of such magnates were aboard on her last voyage. In January, 1909 Republic left New York City with passengers and crew, bound for Gibraltar and Mediterranean ports. In thick fog off the island of Nantucket, Republic was rammed amidships by the Italian liner Florida. Florida’s bow was crumpled back, but she stayed afloat. The damage to Republic was fatal. The engine rooms flooded, the ship began to list, and it was clear that the passengers needed to be evacuated.

Using the new-fangled Marconi “wireless” apparatus, a CQD distress signal was broadcast by radio operator Jack Binns. This was the first wireless transmission that resulted in a major life-saving marine rescue. (Binns had to scramble and improvise to get this done, since his apparatus had been damaged and the ship’s power was lost as a result of the collision, so he was a technology nerd turned hero, duly lauded by a ticker-tape parade). It was hard for other ships to locate Republic in the fog, but eventually nearly all the passengers and crew from Republic and from the damaged Florida were safely transferred to other ships.

As was the custom of the time, she did not carry enough lifeboats to hold all the passengers, but only enough to ferry them to some other ship; it was assumed that on the busy Atlantic route there would always be other large ships around. (That scheme played out well with the Republic, but when sister White Star liner Titanic sank four years later, the dearth of lifeboats helped doom some 1,500 people to a watery grave.) Despite efforts to save her, Republic went down stern-first on January 24. She was the largest ship ever to sink at the time. There were reports at the time that she was carrying some $3 million (1909 dollars) of gold, which went down with the ship. That would translate to hundreds of millions of dollars today for that gold.

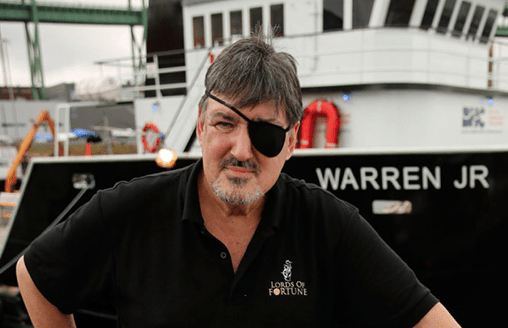

But wait, there’s more, maybe much more. Enter a modern-day pirate, Martin Bayerle:

Bayerle looks like a pirate, sporting a genuine eyepatch covering an eye lost in an explosives accident. He killed a man who was fooling around with his wife, which seems like a piratical thing to do, and he is after a ship’s gold. His salvage enterprise is even formally described in legal court papers as “modern day pirates”.

His company, Martha’s Vineyard Scuba Headquarters, Inc. (“MVSHQ”), acquired salvage rights to the wreck of the Republic. In 2013 he published a book, The Tsar’s Treasure, detailing his thesis that Republic carried far more gold than was publicly acknowledged. He notes that there was no formal inquiry regarding the sinking of Republic, which was highly unusual and is suggestive of a cover-up. Cover-up of what?

Well, Europe at the time was a tinder box of potential conflict, which did in fact erupt five years later in World War I. Czarist Russia was a key part of the European military equation. Britain was counting on Russia to help contain the emerging militaristic Germany. Russia had incurred huge debts in its disastrous war with Japan in 1905. Russia was about to issue a new round of bonds in 1909, to roll over its debt from 1905. It was critical that that bond issuance would go forward.

Bayerle believes that a large amount of gold was stashed in the hold of the Republic, destined for European banks, to support the Russian bonds of 1909. The revelation that that gold was lost would have jeopardized this crucial financial transaction, perhaps leading to Russia’s collapse, which is something Britain could not afford. Hence, the cover-up. Bayerle estimates that the value of this trove is up to $10 billion in today’s money. Shiver me timbers!

This geopolitical speculation, together with stories of failed previous salvage attempts on Republic, all make for a rollicking yarn. Is it for real? Nobody knows, but Bayerle is offering investors a chance at a slice of the booty. If you are inclined to “Dare to dream the impossible” (per the website), you have the opportunity to invest in his Lords of Treasure enterprise as they make a dive on the site this summer.

I don’t happen to have that much risk appetite, but it should be an interesting story to follow.

UPDATE

According to the June 2025 Lords of Fortune Newletter, salvage operations originally slated for 2025 are being put off till 2026, as funding is still being developed. We note the technical challenge of picking through hundreds of tons of steel plate and girders, deep underwater, in search of a smallish volume of gold. On the other hand, Capt. Bayerle’s recent researches suggest the gold trove may be even larger than earlier estimated, up to some $30 billion. So high risk meets high reward here. It seems ironic that VC’s will throw say $300 million into dubious tech unicorns or the latest crap-coin, but eschew a pretty sure bet of at least breaking even here (if only the lowest estimates of the Republic gold pan out) with a good shot at 10X-ing their investment. We will stay tuned.

To say Warren Buffett is not a fan of gold would be an understatement. His basic beef is that gold does not produce much of practical value. His instincts have always been to buy businesses that generate steady and growing cash by producing goods or services that people need or want – – businesses like railroads, beverage makers, and insurance companies.

Here are some quotes on the subject from the Oracle of Omaha, where I have bolded some phrases:

“Gold … has two significant shortcomings, being neither of much use nor procreative. True, gold has some industrial and decorative utility, but the demand for these purposes is both limited and incapable of soaking up new production. Meanwhile, if you own one ounce of gold for an eternity, you will still own one ounce at its end” — Buffett, letter to shareholders, 2011

“With an asset like gold, for example, you know, basically gold is a way of going long on fear, and it’s been a pretty good way of going long on fear from time to time. But you really have to hope people become more afraid in the year or two years than they are now. And if they become more afraid you make money, if they become less afraid you lose money. But the gold itself doesn’t produce anything” — Buffett, CNBC’s Squawk Box, 2011

This from when the world’s 67-cubic foot total gold hoard was worth about $7 trillion, which by his reckoning was the value of all U.S. farmland plus seven times the value of petroleum giant ExxonMobil plus an extra $1 trillion:

“And if you offered me the choice of looking at some 67-foot cube of gold … and the alternative to that was to have all the farmland of the country, everything, cotton, corn, soybeans, seven ExxonMobils. Just think of that. Add $1 trillion of walking around money. I, you know, maybe call me crazy but I’ll take the farmland and the ExxonMobils” – – Cited in https://www.nasdaq.com/articles/3-things-warren-buffett-has-said-about-gold

And my favorite:

“Gold gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head“. – – From speech at Harvard, see https://quoteinvestigator.com/2013/05/25/bury-gold/

One thing Buffett did NOT say is that gold is “barbarous relic”. That line is owned by John Maynard Keynes from a hundred years ago, referring to the notion of tying national money issuance to the number of bars of gold held in the national vaults:

“In truth, the gold standard is already a barbarous relic. All of us, from the Governor of the Bank of England downwards, are now primarily interested in preserving the stability of business, prices, and employment, and are not likely, when the choice is forced on us, deliberately to sacrifice these to outworn dogma, which had its value once” – Monetary Reform (1924)

Has Buffett’s Berkshire Hathaway Beaten Gold as an Investment?

Given all that trash talk from the legendary investor, let’s see how an investment in his flagship Berkshire Hathaway company (stock symbol BRK.B) compares to gold over various time periods. I will use the ETF GLD as a proxy for gold, and will include the S&P 500 index as a proxy for the general U.S. large cap stock market.

As always, these comparisons depend on your starting and ending points. In the 1990s and 2000s, BRK.B hugely outperformed the S&P 500, cementing Buffett’s reputation as one of the greatest investors of all time. (GLD data doesn’t go back that far). In the past twelve months, gold (up 41%) has soundly beaten SPY (up 14 %) and completely trounced BRK.A (up 9%), as of last week. A couple of one-off factors have gone into these results: Gold had an enormous surge in January-April as the world markets digested the implications of never-ending gigantic U.S. budget deficits, and the markets soured on BRK.A due to the announced upcoming retirement of Buffett himself.

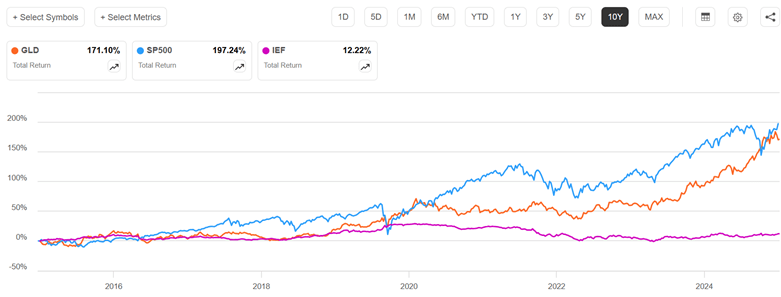

Stepping back to look over the past ten years shows the old master still coming out on top. In this plot, gold is orange, S&P 500 is blue, and BRK.A is royal purple:

Over most of this time period (through 7/21/2025), BRK.A and SP500 were pretty close, and gold lagged significantly. Gold was notably left behind during the key stock surge of 2021. Even with the rise in gold and dip in BRK.A this year, Buffett’s company (up 232%) still beats gold (198%) over the past ten years. BRK.A pulled well ahead of SP500 during the 2022 correction, and never gave back that lead. In the April stock market panic this year, BRK.A actually went up as everything else dropped, as it was seen as a tariff-proof safe haven. SP500 was ahead of gold for nearly all this period, until the crash in stocks and the surge in gold in the first half of 2025 brought them to essentially a tie for the past decade.

Anyone who reads financial headlines knows that gold prices have soared in the past year. Why?

Gold has historically been a relatively stable store of value, and that role seems to be returning after decades of relative neglect. Official numbers show sharply increased buying by the world’s central banks, led by China, Poland, and Azerbaijan in early 2025. Russia, India and Turkey have also been major buyers. There is widespread conviction that actual gold purchases are appreciably higher than the officially-reported numbers, to side-step President Trump’s threatened extra tariffs on nations seen as de-dollarizing.

I think the most proximate cause for the sharp run-up in gold prices in the past twelve months has been the profligate U.S. federal budget deficit, under both administrations. This is convincing key world actors that the dollar will become increasingly devalued over time, no matter which party is in power. Thus, it is prudent to get out of dollars and dollar-denominated assets like U.S. T-bonds.

Trump’s erratic and offensive policies and statements in 2025 have added to the desire to diversify away from U.S. assets. This is in addition to the alarm in non-Western countries over the impoundment of Russian dollar-related assets in connection with the ongoing Russian invasion of Ukraine. Also, there is something of a self-fulfilling momentum aspect to any asset: the more it goes up, the more it is expected to go up.

This informative chart of central bank gold net purchasing is courtesy of Weekend Investing:

Interestingly, central banks were net sellers in the 1990s and early 2000s; it was an era of robust economic growth, gold prices were stagnant or declining, and it seemed pointless to hold shiny metal bars when one could invest in financial assets with higher rates of return. The Global Financial Crisis of 2008-2009 apparently sobered up the world as to the fragility of financial assets, making solid metal bars look pretty good. Then, as noted, the Western reaction to the Russian attack on Ukraine spurred central bank buying gold, as this blog predicted back in March, 2022.

Private investors are also buying gold, for similar reasons as the central banks. Gold offers portfolio diversification as a clear alternative from all paper assets. In theory it should offer something of an inflation hedge, but its price does not always track with inflation or interest rates.

Here is how gold (using GLD fund as a proxy) has fared versus stocks (S&P 500 index) and intermediate term U. S. T-bonds (IEF fund) in the past year:

Gold is up by 40%, compared to 12.6% for stocks. That is huge outperformance. This was driven largely by the fact that gold rose strongly in the Feb-April timeframe, while stocks were collapsing.

Below we zoom out to look at the past ten years, and include the intermediate-term T-bond fund IEF:

Gold prices more than doubled from 2008 to 2011, then suffered a long, painful decline over the next two years. Prices were then fairly stagnant for the mid-2010s, rose significantly 2019-2020, then stagnated again until taking off in 2023. Stocks have been much more erratic. Most of the time stock returns were above gold, but the 2020 and 2024 plunges brought stocks down to rough parity with gold. Since about 2019, T-bonds have been pathetic; pity the poor investor who has been (according to traditional advice) 40% invested in investment-grade bonds.

How to invest in gold? Hard-core gold bugs want the actual coins (no-one can afford a full bullion bar) to rub between their fingers and keep in their own physical custody. You can buy coins from on-line dealers or local dealers. Coins are available from the U.S. Mint, but reportedly their mark-ups are often higher than on the secondary market.

An easier route for most folks is to buy into a gold-backed stock fund. The biggest is GLD, which has over $100 billion in assets. There has long been an undercurrent of suspicion among gold bugs that GLD’s gold is not reliably audited or that it is loaned out; they refer derisively to GLD as “paper gold” or gold derivatives. The fund itself claims that it never lends out its gold, and that its bars are held in the vaults of the custodian banks JPMorgan Chase Bank, N.A. and HSBC Bank plc, and are independently audited. The suspicious crowd favors funds like Sprott Physical Gold Trust, PHYS. PHYS is claimed to have a stronger legal claim on its physical gold than GLD. However, PHYS is a closed-end fund, which means it does not have a continuous creation process like GLD, an open-end ETF. This can lead to discrepancies between the fund’s share price and the value of its gold holdings. It does seem like PHYS loses about 1% per year relative to GLD.

Disclaimer: Nothing here should be taken as advice to buy or sell any security.

According to Merriam-Webster, “money” is: “something generally accepted as a medium of exchange, a measure of value, or a means of payment.” Money, in its various forms, also serves as a store of value. Gold has maintained the store of value function all though the past centuries, including our own times; as an investment, gold has done well in the past couple of decades. I plan to write more later on the investment aspect, but here I focus on the use of physical gold as a means of payment or exchange, or as backing a means of exchange.

Gold, typically in the form of standardized coins, served means of exchange function for thousands of years. Starting in the Renaissance, however, banks started issuing paper certificates which were exchangeable for gold. For daily transactions, the public found it more convenient to handle these bank notes than the gold pieces themselves, and so these notes were used instead of gold as money.

In the late nineteenth and early twentieth centuries, leading paper currencies like the British pound and the U.S. dollar were theoretically backed by gold; one could turn in a dollar and convert it to the precious metal. Most countries dropped the convertibility to gold during the Great Depression of the 1930’s, so their currencies became entirely “fiat” money, not tied to any physical commodity. For the U.S. dollar, there was limited convertibility to gold after World War II as part of the Bretton Woods system of international currencies, but even that convertibility ended in 1971. In fact, it was illegal for U.S. citizens to own much in the way of physical gold from FDR’s (infamous?) executive order in 1933 until Gerald Ford’s repeal of that order in 1977.

So gold has been essentially extinct as active money for nearly a hundred years. The elite technocrats who manage national financial affairs have been only too happy to dance on its grave. Keynes famously denounced the gold standard as a “barbarous relic”, standing in the way of purposeful management of national money matters.

However, gold seems to be making something of a comeback, on several fronts. Most notably, several U.S. states have promoted the use of gold in transactions. Deep-red Utah has led the way. In 2011, Utah passed the Legal Tender Act, recognizing gold and silver coins issued by the federal government as legal tender within the state. This legislation allows individuals to transact in gold and silver coins without paying state capital gains tax. The Utah House and Senate passed bills in 2025 to authorize the state treasurer to establish a precious metals-backed electronic payment platform, which would enable state vendors to opt for payments in physical gold and silver. The Utah governor vetoed this bill, though, claiming it was “operationally impractical.”

The new legislation, House Bill 1056, aims to give Texans the ability, likely through a mobile app or debit card system, to use gold and silver they hold in the state’s bullion depository to purchase groceries or other standard items.

The bill would also recognize gold and silver as legal tender in Texas, with the caveat that the state’s recognition must also align with currency laws laid out in the U.S. Constitution.

“In short, this bill makes gold and silver functional money in Texas,” Rep. Mark Dorazio (R-San Antonio), the main driving force behind the effort, said during one 2024 presentation. “It has to be functional, it has to be practical and it has to be usable.”

Arkansas and Florida have also passed laws allowing the use of gold and silver as legal tender. A potential problem is that under current IRS law, gold and silver are generally classified as collectibles and subject to potential capital gains taxes when transactions occur. Texas legislator Dorazio has argued that liability would go away if the metals are classified as functional money, although he’s also acknowledged the tax issue “might end up being decided by the courts.”

But as Europeans found back in the day, carrying around actual clinking gold coins for purchasing and making change is much more of a hassle than paper transactions. And so, various convenient payment or exchange methods, backed by physical gold, have recently arisen.

Since it is relatively easy and lucrative to spawn a new cryptocurrency (which is why there are thousands of them), it is not surprising that there are now several coins supposedly backed by bullion. These include include Paxos Gold (PAXG) and Tether Gold (XAUT). The gold of Paxos is stored in the worldwide vaults of Brinks, and is regularly audited by a credible third party. Tether gold supposedly resides somewhere in Switzerland. The firm itself is incorporated in the British Virgin Islands. Tether in general does not conduct regular audits; its official statements dance around that fact. These crypto coins, like bullion itself or various funds like GLD that hold gold, are in practice probably mainly an investment vehicle (store of value), rather than an active medium of exchange.

However, getting down to the consumer level of payment convenience, we now have a gold-backed credit card (Glint) and debit card (VeraCash Mastercard). Both of these hold their gold in Swiss vaults. The funds you place with these companies have gold allocated to them, so these are a (seemingly cost-effective) means to own gold. If you get nervous, you can actually (subject to various rules) redeem your funds for actual shiny yellow metal.

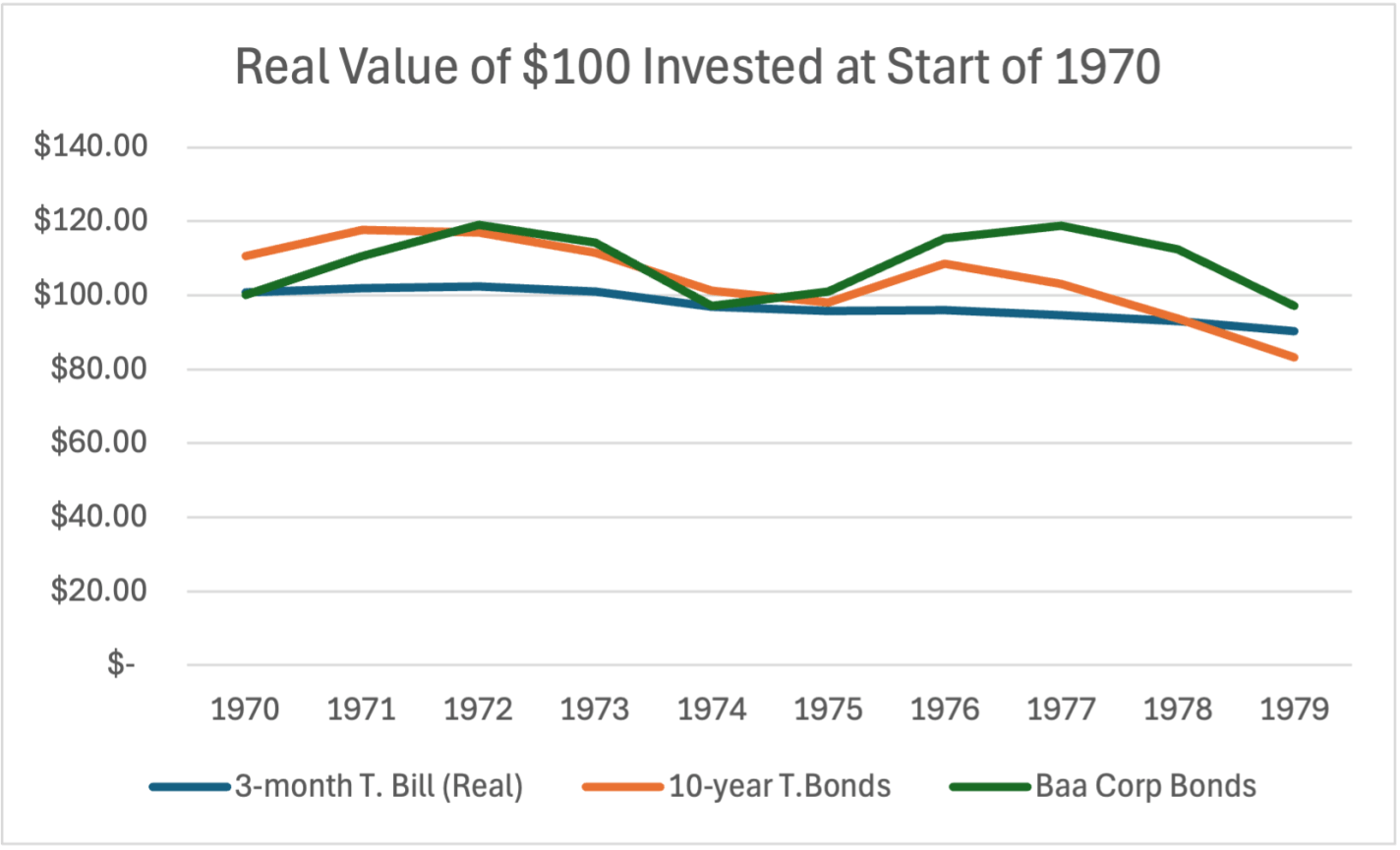

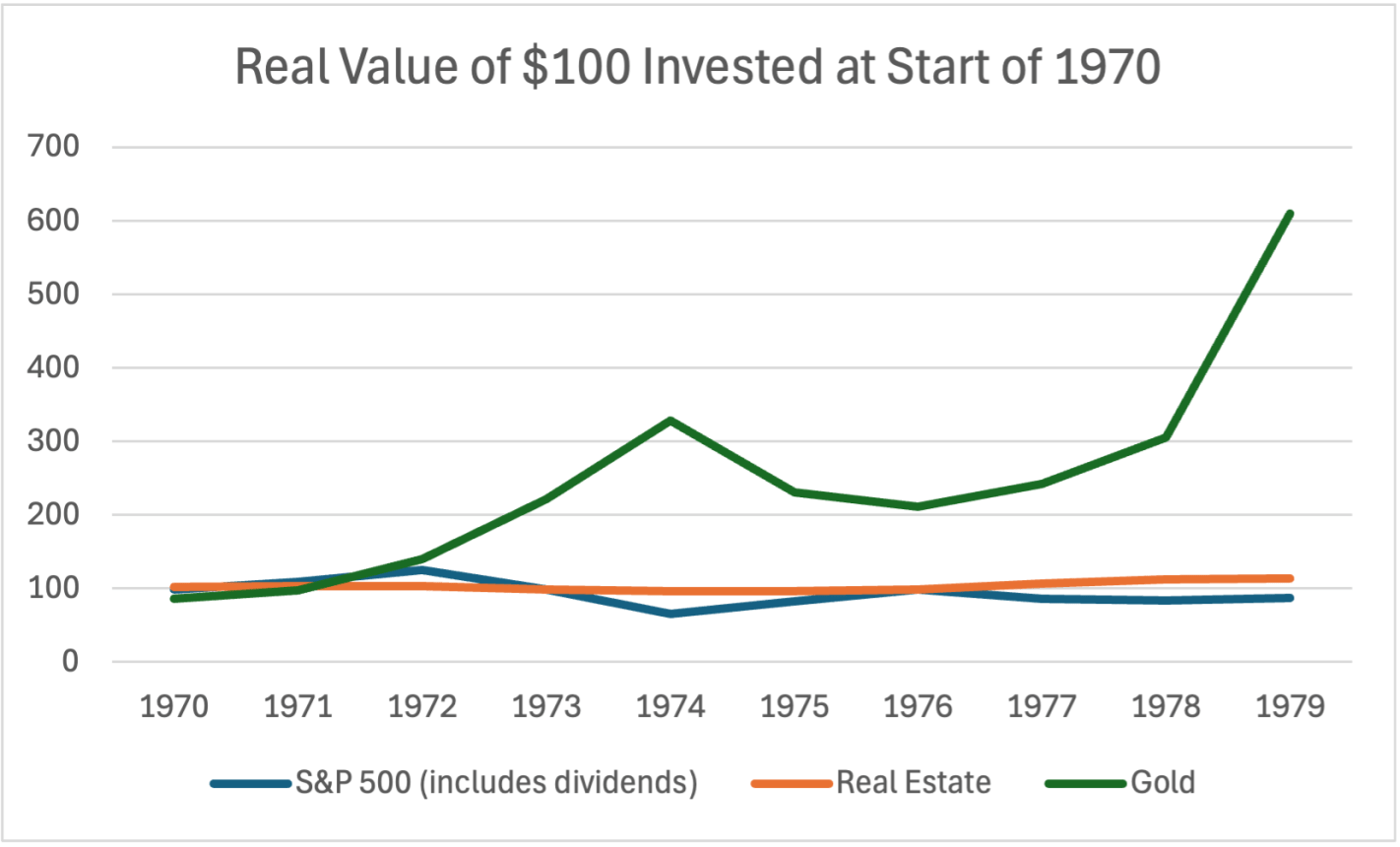

The tariffs still have me thinking about buying VIX calls and stock puts (especially when policy changes loom on certain dates like July 8th), and on the bigger question of finding the sort of investments that did well in the 1970’s, another decade of stagflation that was kicked off by a President who broke America’s commitment to an international monetary system that he thought no longer served us.

That’s how I concluded last week. So this week I’ll answer the question- what were the best investments of the 1970’s? When the dollar is losing value both at home and abroad, holding dollars or bonds that pay off in dollars does poorly:

Stocks can do alright with moderate inflation, but US stocks lost value in the stagflation of the 1970’s. Foreign stocks and commodities generally performed better. Real estate held its value but didn’t produce significant returns; gold shone as the star of the decade:

Gold is easy to invest in now compared to the 1970s; you don’t have to mess with futures or physical bullion, there are low-fee ETFs like IAUM available at standard brokerages.

Of course, while history rhymes, it doesn’t repeat exactly; this time can and will be different. I doubt oil will spike the same way, since we have more alternatives now, and if it did spike it wouldn’t hurt the US in the same way now that we are net exporters. Inflation won’t be so bad if we keep an independent Federal Reserve, though that is now in doubt. At any time the President or Congress could reverse course and drop tariffs, sending markets soaring, especially if they pivot to tax cuts and deregulation in place of tariffs ahead of the midterms.

Things could always get dramatically better (AI-driven productivity boom) or worse (world war). But for now, “1970s lite” is my base case for the next few years.

I ran across an article by Lyn Schwartzer on seeking Alpha last week, which I thought was insightful regarding investments. Here is my summary.

The article is Most Investments Are Bad. Here’s Why, And What To Do About It. The article’s first bullet point is “Historical data shows that the majority of investments, including bonds, stocks, and real estate, perform poorly.” Unpacking this, looking at various investment classes:

Bonds and Stocks

Investment-grade bonds typically pay interest rates just a little above inflation, so it’s not surprising that they have been mediocre investments over the long-term. The prices of long bonds (10 years or more maturity) tended to rise between about 1985 and 2020, as interest rates came steadily down, but that tailwind is pretty much over.

It has been known for years, e.g. from a study by Hendrik Bessembinder, that only a tiny fraction of stocks makes up the vast majority of returns in equity markets. I wrote about this a couple of years ago on this blog.:

The rise of the S&P is entirely due to huge gains by a tiny subset of stocks. The average stock actually loses money over both short and long time periods. … half of the U.S. stock market wealth creation [1926-2015] had come from a mere 0.33% of the listed companies… Out of some 26,000 listed companies, 86 of them (0.33%) provided 50% of the aggregate wealth creation, and the top 983 companies (4%) accounted for the full 100%. That means the other 25,000 companies netted out to zero return. Some gave positive returns, while most were net losers.

As investors, we of course want to know how to lock in on those few stocks that will perform well. I see two approaches here, not mentioned in the article. One is to be very good at analyzing the finances and market environments of companies, to be able to pick individual firms which will be able to grow their profits. Being lucky here probably helps, as well. An easier and very effective method is to simply invest in the S&P 500 index funds like SPY or VOO. Because these funds are weighted by stock capitalization, they inexorably increase their weighting of the more successful companies and dial down the unsuccessful companies. This dumb, automatic selection process is so effective that it is very difficult for any active stock-picking fund manager to beat the S&P 500 for any length of time.

What the article suggests in this regard is to focus on businesses that have “durable competitive advantages (network effects, powerful brands, intangible property, economies of scale, oligopoly participation, and so forth),” or to try to pick up decent/mediocre companies at a low price.

The big tech companies which are mainly listed on the NASDAQ exchange have these durable advantages, and indeed the QQQ fund which is comprised of the hundred largest stocks on the NASDAQ has far outpaced the broader-based S&P 500 fund over the last 10 or 20 years.

Real Estate

All of us suburbanites know that owning your own home has been one of the best investments you can make, over the past few decades. The article points out, however, that real estate in general has not been such a great performer. If your property is not located close to a thriving metropolitan area, where people want to live, it can be a dog. The article cites abandoned properties all around Detroit (“large once-expensive homes that are now rotting on parcels of land that nobody wants”), and notes, “In Japan, there are millions of abandoned countryside homes that are nearly free. Many of them are in beautiful and safe rural areas, and yet there is insufficient demand for them.”

And so, “Most real estate falls somewhere between those extremes. It performs decently, especially when considering that it can replace the owner’s rental income or be rented out for cashflows, but after maintenance and taxes are considered, its unlevered total return from price appreciation and cashflow generation net of maintenance leaves something to be desired relative to gold.”

Gold As a Reference

The article uses gold as, well, the gold standard of investing returns. The supply of gold creeps up roughly 1.5% per year, so after say 95 years there is four times as much physical gold as before. We find that an ounce of gold will buy more food or more manufactured goods than it did a century ago, but that is because our efficiency of producing such things has increased faster than the gold supply. On the other hand, “All government bonds have underperformed gold over the long run, and most unlevered real estate has underperformed gold as well.” Stocks in the broad U.S. market (most foreign stock markets did more poorly) greatly outperformed gold, but that is only accomplished by the top 4% of stocks. The other 96% of stocks as group did not generate any excess returns.

Owner-Operators versus Passive Investors

I am looking at these issues from the point of view of a passive investor – I have some extra cash that I want to plow into some investment, and have it return my original capital plus another say 10%/year, without me having to do extra work. It turns out that many companies, especially smaller ones, provide useful products to customers and they make enough profit to pay off the owner/operators and the employees, but not enough to reward outside passive investors, too. These companies serve an important role in society, but are not viable investment vehicles:

Being an owner-operator of a business, or a worker at a business, makes a lot of sense. However, the vast majority of businesses are not strong enough to provide good returns for outside passive investors after all expenses (including salaries) are considered.

Good returns for outside passive investors are reserved for only the best types of companies; companies that are so dominant and high-margin that even after paying all of their executives and workers, they have plenty of excess profits for outside passive investors. Although stocks from any sector can have these characteristics, Bessembinder’s research found that major outperformers were disproportionally concentrated in the technology, telecommunications, energy, and healthcare/pharmaceutical sectors. They are on the right side of an emerging tech trend, they have network effects, they have economies of scale, they have protected intangible property such as patents, or they are part of an oligopoly, and so forth.

Similarly, real estate (especially unlevered), works most easily when it is occupied or used by the owner. After all, you must live somewhere. Now, you can make money buying and renting/flipping properties, but that typically demands work on your part. You add value by fixing the tenant’s toilet or arranging for a plumber, or by scoping the market and identifying a promising property to buy, and by working to upgrade its kitchen. All this effort is not the same as just throwing money at some building as a passive investor, and walking away for five years.

Upping Returns via Leverage

This is a packed sentence: “Historically, a key way to turn mediocre investments into good investments has been to apply leverage. That’s not a recommendation; that’s a historical analysis, and it comes with survivorship bias.”

For example, banks have historically borrowed money (e.g. from their depositors) at lowish, short-term rates, and combined a lot of those funds with the bank corporate equity, to purchase and hold longer-term bonds that pay slightly higher rates. Banks are often levered (assets vs. equity) 10:1. This technique allows them to earn much higher returns on their equity than if they used their equity alone to buy bonds.

It is easy to leverage real estate. If you put 20% down and borrow the rest, bam, you are levered 5:1. Now if the value of your house goes up 6%/year while you are only paying 3% on your mortgage, the return on the actual cash (the 20% down) you put in becomes quite juicy: “After maintenance and recurring taxes, the majority of unlevered real estate, even when rented out for cashflows, doesn’t outperform gold. But unlike gold, 5-to-1 leverage makes real estate actually pretty good in many contexts, and historically allows it to outperform gold.”

Large corporations can leverage up by issuing relatively low-interest bonds: “They can borrow large amounts of money for decades at low interest rates, and use that capital to organically expand their business, buy smaller companies, or buy back their own shares. Either way, they are borrowing abundant fiat currency at low rates and using that capital to build or buy business equity, and they are arbitraging that spread for shareholders.”

Savvy firms like Warren Buffett’s Berkshire Hathaway take it a step further, by having controlling interests in insurance companies, and investing the low-cost “float” funds, as we described here. From the article:

Berkshire has also made a habit out of buying small and medium sized private businesses in full. Many of these smaller companies would have higher borrowing costs if they were independent. But Berkshire can buy a lot of them, and then issue corporate debt at the parent company level at much lower interest rates than any of them could issue on their own. So he can buy a lot of unlevered cashflow-producing small or medium-sized businesses, and turn them into a portfolio of businesses that are levered with Berkshire’s very low cost of capital.

Now other companies like Ares Management and Apollo are jumping onto this arbitrage bandwagon, buying up insurance companies to get access to their captive cash, to be used for investing.

Here is another rough example of the power of leverage. The unleveraged fund BKLN holds bank loans, and so does the closed end fund VVR. But VVR borrows money to add to the shareholders’ equity. There is more complication (discount to net asset value) with VVR which we will not go into, but the following 5-year chart of total returns (share price plus reinvested dividends) shows nearly triple the return for VVR, albeit with higher volatility:

The Changing Global Economic Landscape

The article closes with some summary observations and recommendations. The past 30-40 years have been marked by ever-decreasing interest rates, and by cooperation among nations and generally increasing globalization. It seems that these trends have broken and so what worked for the last four decades (buy stocks, shun gold) may not be as good going forward:

For equity and real estate investors, the key takeaways from this piece are 1) do not extrapolate the prior decades for a given investment and instead assess it with this context in mind, 2) try to emphasize the sectors [such as Big Tech] that Bessembinder identified as ones that disproportionally generate excess returns, and 3) look for companies that have locked in or are otherwise still able to play this arbitrage game going forward in a more difficult environment for it.

Additionally, hard monies [i.e. gold, silver] become a serious alternative once again in this context, and are worth serious consideration for a portfolio slice, because the hurdle rate for stocks to outperform them is high when there are not a lot of tailwinds at the backs of stocks.

#/media/File:RMS_Republic.jpg){kind=link}