To say Warren Buffett is not a fan of gold would be an understatement. His basic beef is that gold does not produce much of practical value. His instincts have always been to buy businesses that generate steady and growing cash by producing goods or services that people need or want – – businesses like railroads, beverage makers, and insurance companies.

Here are some quotes on the subject from the Oracle of Omaha, where I have bolded some phrases:

“Gold … has two significant shortcomings, being neither of much use nor procreative. True, gold has some industrial and decorative utility, but the demand for these purposes is both limited and incapable of soaking up new production. Meanwhile, if you own one ounce of gold for an eternity, you will still own one ounce at its end” — Buffett, letter to shareholders, 2011

“With an asset like gold, for example, you know, basically gold is a way of going long on fear, and it’s been a pretty good way of going long on fear from time to time. But you really have to hope people become more afraid in the year or two years than they are now. And if they become more afraid you make money, if they become less afraid you lose money. But the gold itself doesn’t produce anything” — Buffett, CNBC’s Squawk Box, 2011

This from when the world’s 67-cubic foot total gold hoard was worth about $7 trillion, which by his reckoning was the value of all U.S. farmland plus seven times the value of petroleum giant ExxonMobil plus an extra $1 trillion:

“And if you offered me the choice of looking at some 67-foot cube of gold … and the alternative to that was to have all the farmland of the country, everything, cotton, corn, soybeans, seven ExxonMobils. Just think of that. Add $1 trillion of walking around money. I, you know, maybe call me crazy but I’ll take the farmland and the ExxonMobils” – – Cited in https://www.nasdaq.com/articles/3-things-warren-buffett-has-said-about-gold

And my favorite:

“Gold gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head“. – – From speech at Harvard, see https://quoteinvestigator.com/2013/05/25/bury-gold/

One thing Buffett did NOT say is that gold is “barbarous relic”. That line is owned by John Maynard Keynes from a hundred years ago, referring to the notion of tying national money issuance to the number of bars of gold held in the national vaults:

“In truth, the gold standard is already a barbarous relic. All of us, from the Governor of the Bank of England downwards, are now primarily interested in preserving the stability of business, prices, and employment, and are not likely, when the choice is forced on us, deliberately to sacrifice these to outworn dogma, which had its value once” – Monetary Reform (1924)

Has Buffett’s Berkshire Hathaway Beaten Gold as an Investment?

Given all that trash talk from the legendary investor, let’s see how an investment in his flagship Berkshire Hathaway company (stock symbol BRK.B) compares to gold over various time periods. I will use the ETF GLD as a proxy for gold, and will include the S&P 500 index as a proxy for the general U.S. large cap stock market.

As always, these comparisons depend on your starting and ending points. In the 1990s and 2000s, BRK.B hugely outperformed the S&P 500, cementing Buffett’s reputation as one of the greatest investors of all time. (GLD data doesn’t go back that far). In the past twelve months, gold (up 41%) has soundly beaten SPY (up 14 %) and completely trounced BRK.A (up 9%), as of last week. A couple of one-off factors have gone into these results: Gold had an enormous surge in January-April as the world markets digested the implications of never-ending gigantic U.S. budget deficits, and the markets soured on BRK.A due to the announced upcoming retirement of Buffett himself.

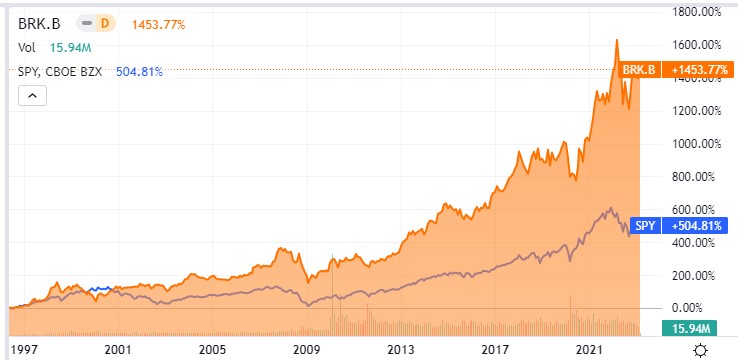

Stepping back to look over the past ten years shows the old master still coming out on top. In this plot, gold is orange, S&P 500 is blue, and BRK.A is royal purple:

Over most of this time period (through 7/21/2025), BRK.A and SP500 were pretty close, and gold lagged significantly. Gold was notably left behind during the key stock surge of 2021. Even with the rise in gold and dip in BRK.A this year, Buffett’s company (up 232%) still beats gold (198%) over the past ten years. BRK.A pulled well ahead of SP500 during the 2022 correction, and never gave back that lead. In the April stock market panic this year, BRK.A actually went up as everything else dropped, as it was seen as a tariff-proof safe haven. SP500 was ahead of gold for nearly all this period, until the crash in stocks and the surge in gold in the first half of 2025 brought them to essentially a tie for the past decade.

A big piece of news in the investment world has been the passing of Charlie Munger on Nov 28 at age 99. He was vice chair of Berkshire Hathaway, and Warren Buffett’s right-hand man there.

Munger grew up in Omaha, Nebraska, which is Warren Buffett’s hometown as well. They met at a dinner party there in 1959, and hit it off with one another personally. Munger was a really smart guy. After joining the US Army Air Corps in1943, he scored highly on an intelligence test and was sent to study meteorology at Caltech. After the war he was accepted into Harvard Law School despite lacking a formal undergraduate degree, and graduated summa cum laude.

In his 50s, Munger lost his left eye after cataract surgery failed. A doctor warned he could lose his right eye too, so he began learning braille, but the condition improved.

He entered law practice, and eventually started his own firm, but he became more interested in investing. He racked up 19.8% annual returns investing on his own, between 1962 and 1975. Buffett convince Munger to give up law and join him as vice-chairman of Berkshire Hathaway in 1978.

Perhaps Buffett’s most famous investing saying is “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price”. He credits this approach to Munger: “Charlie understood this early – I was a slow learner.” Before being influenced here by Munger, Buffett had been more inclined to buy very low-priced shares in mediocre companies.

Munger was heavily involved with Buffett’s decisions. “Berkshire Hathaway could not have been built to its present status without Charlie’s inspiration, wisdom and participation,” Buffett said following Munger’s death. That tribute is no overstatement: from the time Munger joined Berkshire Hathaway in 1978 till now, shares of the company soared 396,182% (i.e., $100 invested in Berkshire Hathaway in 1978 is worth $396,282 today). This performance dwarfs the 16,427% appreciation of the S&P 500 over the same time period. When he died, Munger was personally worth $2.6 billion.

The internet is rife with sites displaying memorable or useful quotes from Charlie Munger. For example, “I never allow myself to have an opinion on anything that I don’t know the other side’s argument better than they do”; and three rules for a career: “1) Don’t sell anything [to others] you wouldn’t buy yourself; 2) Don’t work for anyone you don’t respect and admire; and 3) Work only with people you enjoy.”

Some of these quote lists focus on sayings which provide guidance to individual investors, such as this from CNBC:

“I think you would understand any presentation using the word EBITDA, if every time you saw that word you just substituted the phrase, ‘bull—- earnings.’ ″

The 2003 Berkshire shareholder meeting was one of the many occasions Munger called out what he saw as shady accounting practices, in this case EBITDA — a measure of corporate profitability short for earnings before interest, taxes, depreciation and amortization.

In short, Munger felt that companies often highlighted convoluted profitability metrics to obscure the fact that they were severely indebted or producing very little cash.

“There are two kinds of businesses: The first earns 12%, and you can take it out at the end of the year. The second earns 12%, but all the excess cash must be reinvested — there’s never any cash,” Munger said at the same meeting. “It reminds me of the guy who looks at all of his equipment and says, ‘There’s all of my profit.’ We hate that kind of business.”

To invest like Munger and Buffett, don’t fall for the flashiest numbers in the firms’ investor presentations. Instead, dig into a company’s fundamentals in their totality. The more a company or an investment advisor tries to win you over with esoteric terms, the more skeptical you should likely be.

As Buffett put it in his 2008 letter to shareholders: “Beware of geeks bearing formulas.”

Munger’s Secret to Happiness

Out of all these witty and helpful quotes, I’ll conclude by zeroing in on what Charlie Munger thought was the single most important factor in achieving personal happiness. He said it a number of different ways:

A happy life is very simple. The first rule of a happy life is low expectations. That’s one you can easily arrange. And if you have unrealistic expectations, you’re going to be miserable all your life. I was good at having low expectations and that helped me. And also, when you [experience] reversals, if you just suck it in and cope, that helps if you don’t just stew yourself into a lot of misery.

One of Warren Buffet’s most famous quotes (channeling the venerable Benjamin Graham) is: “Price is what you pay; value is what you get.” He thus rationalizes buying top-quality companies or stocks, even if their price is not beaten down. So, allow me to explain why I put over $100 into a single, not-very-large raspberry plant.

In various earlier homes I have lived in, I have grown raspberries. To my way of thinking, this is an ideal crop for a home gardener. You can get maybe five bare-root dormant plants from a gardening supply house like Burpee in the early spring, plant them in the ground, and by that fall have a crop of sweet, flavorful berries you can eat right off the bush. And then you have a perennial bed that will fill in with even more canes each year. The “everbearing” (“fall-bearing” or primocane) varieties like Heritage or Caroline can produce from June through early October, depending on your climate zone. Not many pests attack raspberries, and the only maintenance needed is pruning, fertilizing, and watering during droughts. They do need nearly full sun, and well-drained soil.

I now live in a townhouse, However, I did want to grow raspberries, partly for the fun of growing my own food, partly out of nostalgia, and partly to give my grandson the experience of picking food from a plant instead of from a grocery store shelf.

The townhouse I live in now only gets nearly-full sunlight at one corner of the house. There is no appropriate garden bed there, so I need to use a container. Raspberries normally grow 3-4 feet tall, with roots that go down maybe two feet. I did not really have the space for a two-foot high/two-foot diameter container, and such a large container would be hard to move around. So last year I tried to grow a regular raspberry (Glencoe variety) in maybe a 14-inch x 14-inch pot. It was a total fail. The root space was just too small for this large a plant, I think.

So this year I regrouped, dug deep in my wallet, and bought a special dwarf raspberry called “Raspberry Shortcake.” This variety is bred to grow in small spaces. This plant is mostly supplied in a #1 size pot (nominally 1 quart, but actually smaller). I was impatient and wanted a larger plant that would bear fruit this year, so I spent more and bought a larger (# 2 pot) plant from Plant Addicts. It arrived in late April, and I transplanted it to a 16” x 16” (40 cm x 40 cm) plastic pot from Better Homes and Gardens. This pot is white, which I hope will reflect some of the sun’s heat during the summer.

This is a summer-bearing (floricane) raspberry, so it will only bear fruit for a few weeks in June-July. However, there is a new Asian fly pest spreading in the U.S. that attacks raspberries later in the season, so it may be best to avoid the fall-bearing varieties now anyway.

The plant had been pruned back to several slender, woody stems about ten inches high. Each of these stems has since put out several side shoots, most of which have now borne clusters of berries at their tips. I have enjoyed several dozen berries, and they are still coming. Also, I have had the pleasure of seeing my grandson pick and eat berries off the bush. I am a satisfied customer. Photos:

And close-up on the berries:

This plant cost me $72 ($57 plus $15 shipping). We got lucky with the pot, paying only about $22, when you can easily pay twice that for this sized pot. Potting soil was another $15. So about $109 all-in.

Obviously, I could have bought many little cartons of raspberries in the store instead for $109. I paid a high price for my plant, but got a value that I am satisfied with.

POSTSCRIPT: Just for completeness, to inform other would-be buyers of this plant – – it’s berry production peaked in mid-June here in U.S. growing zone 7a. It continued to produce a few berries a day till the end of the month. Since about July 1, it still produces perhaps an average of one berry a day, with 6-7 visible on the bush at any one time, but they are not ripening properly. Sometimes they just fall off before they are ripe, but most often they ripen very unevenly: some of the little “drupes” turn dark red (and then sometimes fall off) while the rest are still whitish. This may be a reaction to the heat, it is sunny and has hit 90 degrees F nearly every day, so the soil around the roots in the pot is way hotter than it would be for an in-ground planting . Anyway, none of this takes away from the satisfactory performance in June.

Post-PostScript: After watering the plant more frequently to let it transpire like crazy in the heat, and also after I loosely wrapped a 14-inch high strip of aluminum flashing around the pot to deflect some of the sun’s rays, the berries seem to be ripening better…getting 1-2 berries a day, though July 15, though they really are petering out now.

So much has been happening in the banking world it is a little hard to keep track of it. See recent articles here by fellow bloggers Mike Makowsky, Jeremy Horpedahl, and Joy Buchanan. Here is a quick guide to all the drama.

Credit Suisse Takeover by UBS

Perhaps the biggest, newest news is a shotgun wedding between the two biggest Swiss banks announced over the weekend. Credit Suisse is a huge, globally significant bank that has suffered from just awful management over the last decade. Its missteps are a tale in itself. Its collapse would be an enormous hit to the Swiss financial mystique, and would tend to destabilize the larger western financial system. So the Swiss government strong-armed a takeover of Credit Suisse by the other Swiss bank behemoth, UBS, in an all-stock transaction. The government is providing some funding, and some guarantees against losses and liability. An unusual aspect of this deal is that Credit Suisse shareholders will get some value for their stock, but a whole class of Credit Suisse bonds Is being written down to zero. Usually bond holders have strong priority over stockholders, so this may make it more difficult for banks to sell unsecured bonds hereafter.

Silicon Valley Bank Collapse: Depositors Protected

The Silicon Valley Bank (SVB) collapse is old news by now. The mismanagement there is another cautionary tale: despite having a flighty tech/venture capital deposit base, management greedily reached for an extra 0.5% or so yield by putting assets into longer-term bonds that were vulnerable to a rise in interest rates instead of into stable short-term securities.

A key step back from the brink here was the feds coming to the rescue of depositors, brushing aside the existing $250,000 limit on FDIC guarantees. That was an important step, otherwise large depositors would stampede out of all the regional banks and take their funds to the few large banks that are in the too-big-to-fail category. It is true that this new level of guarantee encourages more moral hazard, since depositors can now be more careless, but the alternative to guaranteeing these deposits (i.e. the collapse of regional banks) was just too awful. Bank shareholders and most bondholders were wiped out. Presumably that will send a message to the investing community of the importance of risk management at banks.

The actual disposition of the business parts of SVB are still being worked out. The feds originally tapped the big, well capitalized banks to see if one of them would take over SVB as a going concern. That would have been a nice, clean, thorough resolution. But the big banks all declined. I suspect the actual responses in private were unprintable. Here’s why: in the 2008 banking crisis, the Obama-Biden administration went to the big banks and encouraged them to take over failing institutions like Countrywide Mortgage, who among other things had made arguably predatory loans to subprime borrowers who had poor prospects to keep up with the mortgage payments. The Obama administration’s Department of Justice promptly turned around and very aggressively prosecuted these big banks for the sins of the prior institutions. J. P. Morgan ended up paying something like 13 billion and Bank of America paid 17 billion. So when today’s Biden administration reached out to these big banks this month to see about taking over SVB, they got no takers.

Now the assets of SVB (renamed Silicon Valley Bridge Bank) are getting auctioned off, perhaps piecemeal, but how exactly that happens does not seem so critical.

Signature Bank: Shut Down, But Sold Off Intact

Crypto-friendly Signature Bank was shuttered by New York State officials on Sunday, March 12, making this the third largest (SVB was the second largest) bank failure in U.S. history. Forbes gives the whole story. At the end of last year, Signature had over $110 billion in assets and $88 billion in deposits. Spooked by Signature’s similarities to failed banks SVB and Silvergate, customers rushed to withdraw deposits, which the bank could not honor without selling securities at huge losses. As with SVB, the feds had the FDIC insure all deposits of all sizes at Signature.

Unlike SVB, Signature has received a bid for the whole business, from New York Community Bancorp’s subsidiary Flagstar Bank. Flagstar will take over most deposits and loans and other assets, and operate Signature Bank’s 40 branches.

First Republic: Teetering on The Brink, Propped Up by Banking Consortium

First Republic is in a somewhat different class than these other troubled institutions. Its overall practices seem reasonable, in terms of equity and assets. However, it caters to a wealthy clientele in the Bay Area, with a lot of accounts over the $250,000 threshold. In the absence of a rapid and decisive move by Congress to extend FDIC protection to all deposits at all banks, somehow (I haven’t tracked what started the stampede) depositors got to withdrawing huge amounts (like $70 billion) last week. This was a classic “run on the bank.” That would stress any bank, despite decent risk management. Once confidence is lost, it’s game over, since there are always alternative places to park one’s money. Ratings agencies downgraded First Republic to junk status, and the stock has cratered.

It is in the interest of the broader banking industry to forestall yet another collapse. If folks start to generally mistrust banks and withdraw deposits en masse, our whole financial system will be in deep trouble. In the case of First Republic, the private sector is trying to prop up it up, without a government takeover. So far this has mainly taken the form of depositing some $30 billion into First Republic, as deposits (not loans or equity), by a consortium of eleven large U.S. banks led by J. P. Morgan. This is was a quick and fairly unheroic intervention, since in the event of liquidation, depositors (including this consortium) have the highest claim on assets. This intervention will probably prove insufficient. Two potential outcomes would be a big issuance of stock to raise capital (which would dilute existing shareholders), or some large bank buying First Republic. The stock rose today on reports that Morgan’s Jamie Dimon was talking with other big banks about taking an equity stake in First Republic, possibly by converting some of the $30 billion deposit into equity.

Old News: Silvergate Bank Liquidation

Overshadowed by recent, bigger collapses, the orderly shutdown of the crypto-focused Silvergate Bank is old news. It was two weeks ago (March 8) that Silvergate announced it would shut down and self-liquidate. The meltdown of the crypto financing world led to excessive loss of deposits at Silvergate. Unlike SVB and Signature, it held a lot of its assets in more liquid, short-term securities, so its losses have not been as devastating – – all depositors will be made whole, though shareholders are toast (stock is down from $150 a year ago to $1.68 at Monday’s close).

Warren Buffett To the Rescue?

Banks generally operate on the model of borrow short/lend long: they “borrow” from depositors and buy longer-term securities. Normally, short-term rates are lower than long-term rates, so banks can pay out much lower interest on their deposits than they receive on their bond/loan investments. With the Fed’s rapid increases in short-term rates this past year, however, the rate curve is heavily inverted, which is disastrous for borrow short/lend long. Fortunately for banks, many depositors are too lazy to do what I have done, which is to move most of my immediate-need money out of bank accounts (paying maybe 1%) and into T-bills and money market funds paying 4-5%.

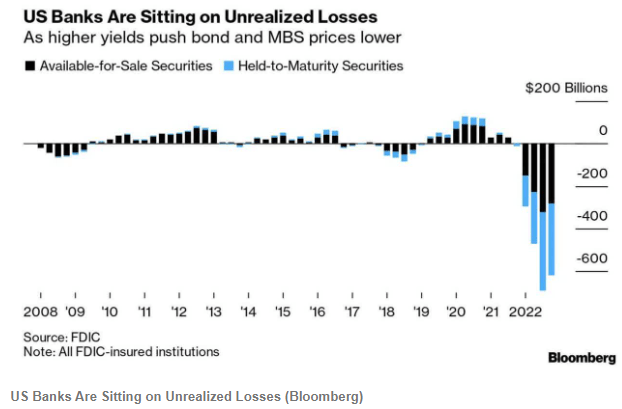

All this churn goes to highlight an inherent fragility of banks: there is typically a maturity mismatch between a bank’s deposits/liabilities (which are short-term and can be withdrawn at any time) and its assets (longer-term bonds it purchases, and loans that it makes which can be difficult to quickly liquidate). Runs on banks, where if you were late to panic you lost all your deposited money, used to be a real feature of life, as dramatized in classic films Mary Poppins and It’s a Wonderful Life. Eliminating this danger was a key reason for setting up the Federal Reserve system, and in general that has worked pretty well in the past hundred years. Banks in general (see chart above) are now carrying enormous amounts of unrealized losses on their portfolios of bonds and mortgage-backed securities (MBS) due to the increase in market rates. In addition to the existing “discount window” at which banks can borrow, the Fed has set up a new lending facility to help tide banks over if they (as in the case of SVB and Signature) get stressed by having to sell marked-down securities to cover withdrawal of deposits. Also, new measures reminiscent of 2008 were announced to extend dollar liquidity to central banks of other nations.

But when Gotham really has a problem, the Commissioner calls in the Caped Crusader. Warren Buffett has been in touch with administration officials about the banking situation. We wrote two weeks ago about Warren Buffett’s gigantic cash hoard from the float of his Berkshire Hathaway insurance businesses which allows him to quickly make deals that most other institutions cannot. Buffett rode to the rescue of large banks like Bank of America and Goldman Sachs in the 2008-2009 financial crisis. A lot of corporate jets have been noted flying into Omaha from airports near the headquarters of various regional banks. Buffett’s typical playbook in these cases is to have the troubled institution issue a special class of high yielding (with today’s regional banks, think: 9%) preferred stock that he buys, perhaps with privileges to convert into the common stock. That stock would count as much needed equity in the banks’ books.

Warren Buffett is referred to as “the legendary investor Warren Buffett” or “the sage of Omaha”. The success of his Berkshire Hathaway fund is remarkable. He is also a pretty nice guy, and every year writes (with help, I’m sure) a letter describing the activities of his fund, along with general observations on investing and the economy. His letter covering 2022 was published two weeks ago.

Buffett noted that he and his team invest in companies in two ways: by buying shares to become a partial “owner” along with thousands of other shareholders, and also by buying ownership of the whole company. They aim to hold American companies that have a good business model, and will keep growing profits for years or decades. They look for great businesses at great prices, but they would rather buy a great business at a good price, than to buy a (merely) good business at a great price.

He was refreshingly honest about his overall stock picking record:

In 58 years of Berkshire management, most of my capital-allocation decisions have been no better than so-so. In some cases, also, bad moves by me have been rescued by very large doses of luck. (Remember our escapes from near-disasters at USAir and Salomon? I certainly do.) Our satisfactory results have been the product of about a dozen truly good decisions – that would be about one every five years – and a sometimes-forgotten advantage that favors long-term investors such as Berkshire.

In 1994 they bought a then-huge stake ($ 1.3 billion) in Coca-Cola, and another $1.3 billion stake in American Express. As it turned out, these two companies had the staying power that Buffet had anticipated, and have grown enormously in value over the past three decades.

In addition to their wholesome stock-picking philosophy, the “secret sauce” of Berkshire Hathaway is having the available funds to make those great investments in those great companies. These funds came large from the “float” from their insurance businesses. In Buffett’s words:

In 1965, Berkshire was a one-trick pony, the owner of a venerable – but doomed – New England textile operation. With that business on a death march, Berkshire needed an immediate fresh start. Looking back, I was slow to recognize the severity of its problems. And then came a stroke of good luck: National Indemnity became available in 1967, and we shifted our resources toward insurance and other non-textile operations.

The insurance business is interesting, in that clients pay in money “now”, but it does not get paid out until “later”. The insurance company has the money to own and manage until there is some claim event (e.g., someone dies or gets their home flooded) perhaps many years later. The traditional, conservative way for insurance companies to manage this float money was to invest it in low-paying but ultra-safe investment grade bonds.

Buffett’s key secret to success was to realize that he could invest at least part of these float funds in stocks, which would (hopefully!) over time make much more money than bonds. That gave him the cash to make those great investments in Coke and Amex. And his fund continues to have billions in hand to make strategic investments. He has made a bundle bailing out good companies that fell into short term difficulties. In his words:

Berkshire’s unmatched financial strength allows its insurance subsidiaries to follow valuable and enduring investment strategies unavailable to virtually all competitors. Aided by Alleghany, our insurance float increased during 2022 from $147 billion to $164 billion. With disciplined underwriting, these funds have a decent chance of being cost-free over time. Since purchasing our first property-casualty insurer in 1967, Berkshire’s float has increased 8,000-fold through acquisitions, operations and innovations. Though not recognized in our financial statements, this float has been an extraordinary asset for Berkshire.

You, too, can participate in Buffett’s investing magic, by buying shares in Berkshire Hathaway. The stock symbol is BRK.B. (Disclosure: I own a few shares). Buffett has been skeptical of flashy tech stocks, and so BRK.B’s performance lagged the S&P 500 fund SPY in 2020-2021, but over the long term Berkshire (orange line in chart below) has crushed the S&P: