Warren Buffett is referred to as “the legendary investor Warren Buffett” or “the sage of Omaha”. The success of his Berkshire Hathaway fund is remarkable. He is also a pretty nice guy, and every year writes (with help, I’m sure) a letter describing the activities of his fund, along with general observations on investing and the economy. His letter covering 2022 was published two weeks ago.

Buffett noted that he and his team invest in companies in two ways: by buying shares to become a partial “owner” along with thousands of other shareholders, and also by buying ownership of the whole company. They aim to hold American companies that have a good business model, and will keep growing profits for years or decades. They look for great businesses at great prices, but they would rather buy a great business at a good price, than to buy a (merely) good business at a great price.

He was refreshingly honest about his overall stock picking record:

In 58 years of Berkshire management, most of my capital-allocation decisions have been no better than so-so. In some cases, also, bad moves by me have been rescued by very large doses of luck. (Remember our escapes from near-disasters at USAir and Salomon? I certainly do.) Our satisfactory results have been the product of about a dozen truly good decisions – that would be about one every five years – and a sometimes-forgotten advantage that favors long-term investors such as Berkshire.

In 1994 they bought a then-huge stake ($ 1.3 billion) in Coca-Cola, and another $1.3 billion stake in American Express. As it turned out, these two companies had the staying power that Buffet had anticipated, and have grown enormously in value over the past three decades.

In addition to their wholesome stock-picking philosophy, the “secret sauce” of Berkshire Hathaway is having the available funds to make those great investments in those great companies. These funds came large from the “float” from their insurance businesses. In Buffett’s words:

In 1965, Berkshire was a one-trick pony, the owner of a venerable – but doomed – New England textile operation. With that business on a death march, Berkshire needed an immediate fresh start. Looking back, I was slow to recognize the severity of its problems. And then came a stroke of good luck: National Indemnity became available in 1967, and we shifted our resources toward insurance and other non-textile operations.

The insurance business is interesting, in that clients pay in money “now”, but it does not get paid out until “later”. The insurance company has the money to own and manage until there is some claim event (e.g., someone dies or gets their home flooded) perhaps many years later. The traditional, conservative way for insurance companies to manage this float money was to invest it in low-paying but ultra-safe investment grade bonds.

Buffett’s key secret to success was to realize that he could invest at least part of these float funds in stocks, which would (hopefully!) over time make much more money than bonds. That gave him the cash to make those great investments in Coke and Amex. And his fund continues to have billions in hand to make strategic investments. He has made a bundle bailing out good companies that fell into short term difficulties. In his words:

Berkshire’s unmatched financial strength allows its insurance subsidiaries to follow valuable and enduring investment strategies unavailable to virtually all competitors. Aided by Alleghany, our insurance float increased during 2022 from $147 billion to $164 billion. With disciplined underwriting, these funds have a decent chance of being cost-free over time. Since purchasing our first property-casualty insurer in 1967, Berkshire’s float has increased 8,000-fold through acquisitions, operations and innovations. Though not recognized in our financial statements, this float has been an extraordinary asset for Berkshire.

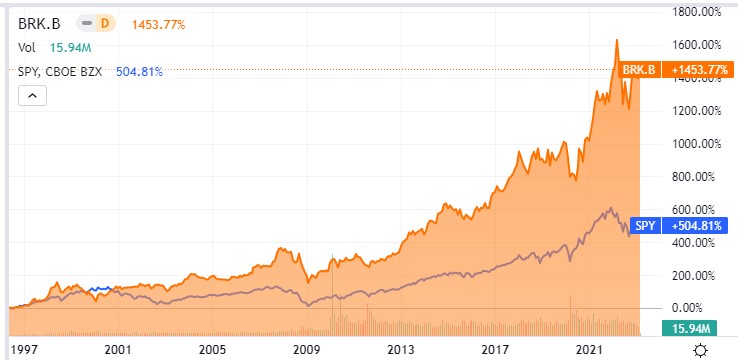

You, too, can participate in Buffett’s investing magic, by buying shares in Berkshire Hathaway. The stock symbol is BRK.B. (Disclosure: I own a few shares). Buffett has been skeptical of flashy tech stocks, and so BRK.B’s performance lagged the S&P 500 fund SPY in 2020-2021, but over the long term Berkshire (orange line in chart below) has crushed the S&P: