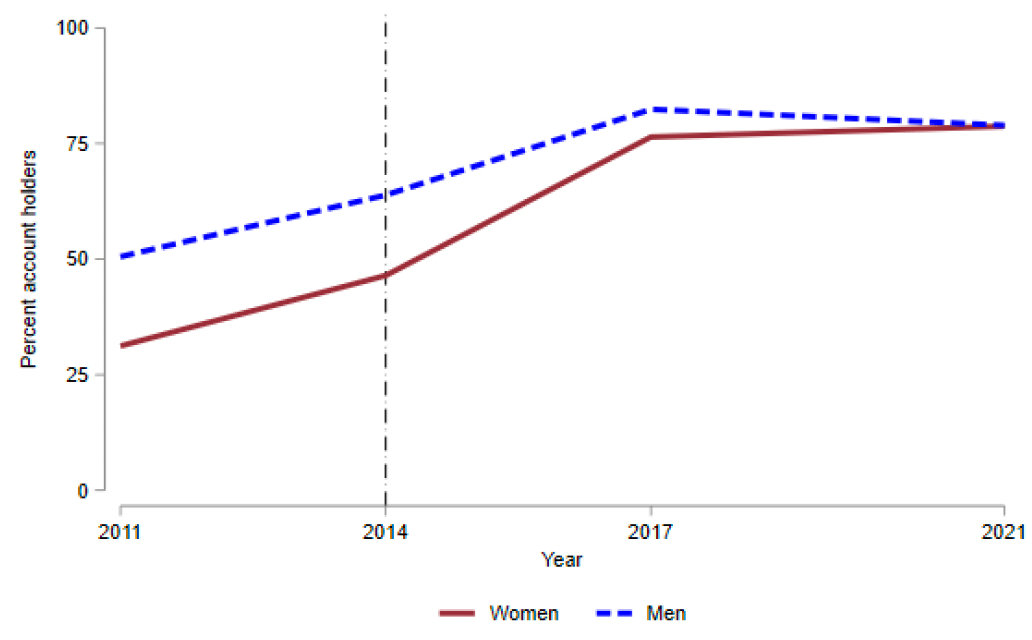

In 2014 India required banks to offer no-cost accounts. This led hundreds of millions of people to open bank accounts for the first time, and more than doubled the number of Indian women who had a bank account:

This increased households’ collective ability to save and borrow, but didn’t shift decision-making power towards women despite the larger change for them. That is the finding of a paper by Tarana Chauhan, a Brown University postdoc who is currently on the job market. The paper is a well-executed example of a difference-in-difference analysis of observational data- that is, carefully examining data that other people generated to examine events that help establish causality. But the validity of difference-in-difference strategies in separating correlation from causation can always be questioned, and always is in economics seminars.

So Dr. Chauhan, this time with coauthors Berber Kramer, Patrick Ward and Subhransu Pattnaik, followed up by directly running an experiment. They got a company to offer subsidized loans to hundreds of randomly selected Indian farmers, then surveyed the farmers to see if they behaved differently than a control group that didn’t get loans. The loans carried a 14% interest rate, which seems high to Americans but was apparently 10pp lower than the other options available in India. They wanted to know whether farmers would use the loans to improve farm productivity, and whether this would have any differential effects on women.

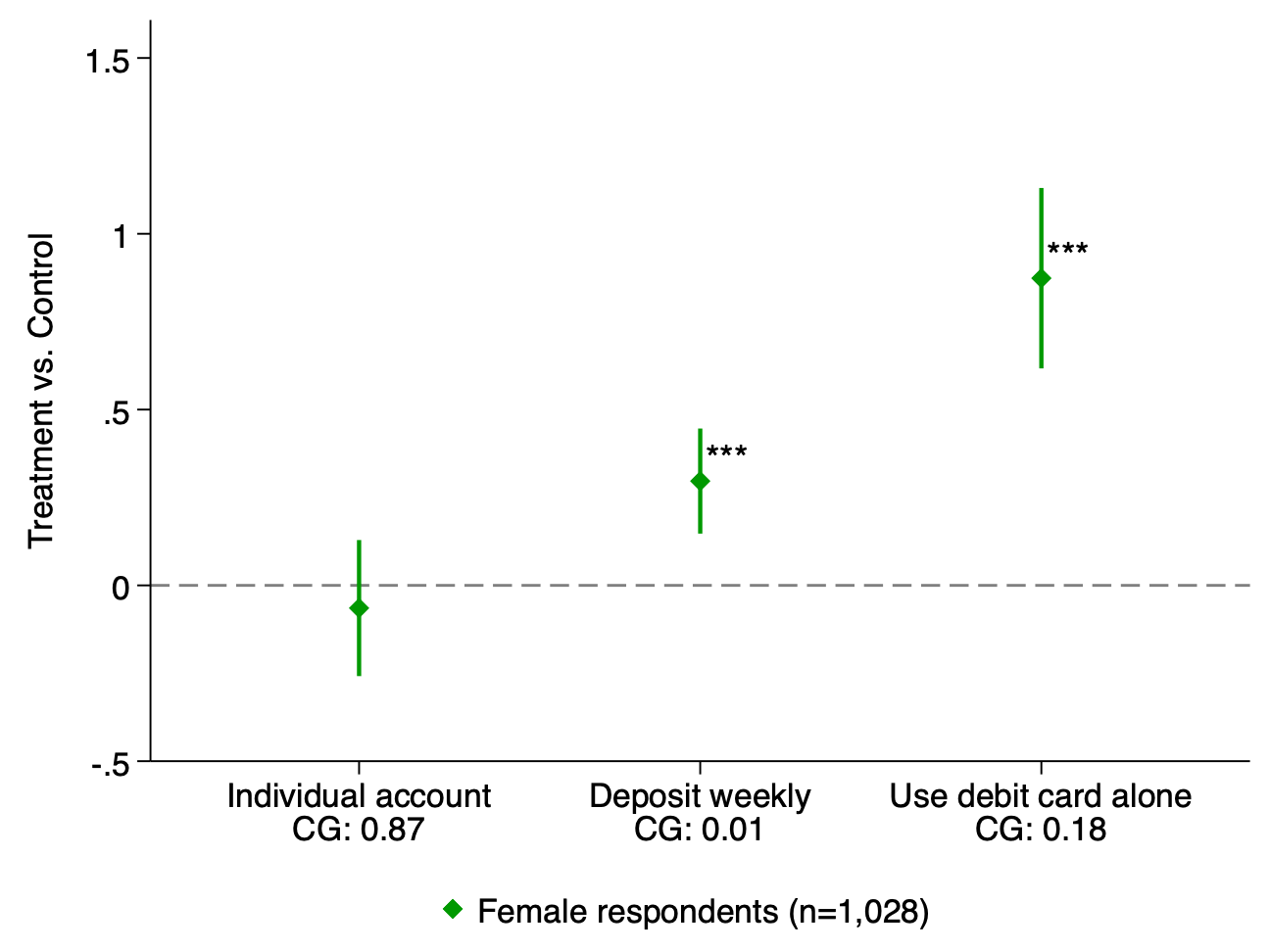

The first stage of the experiment worked: households took the loans and got more engaged with the financial system.

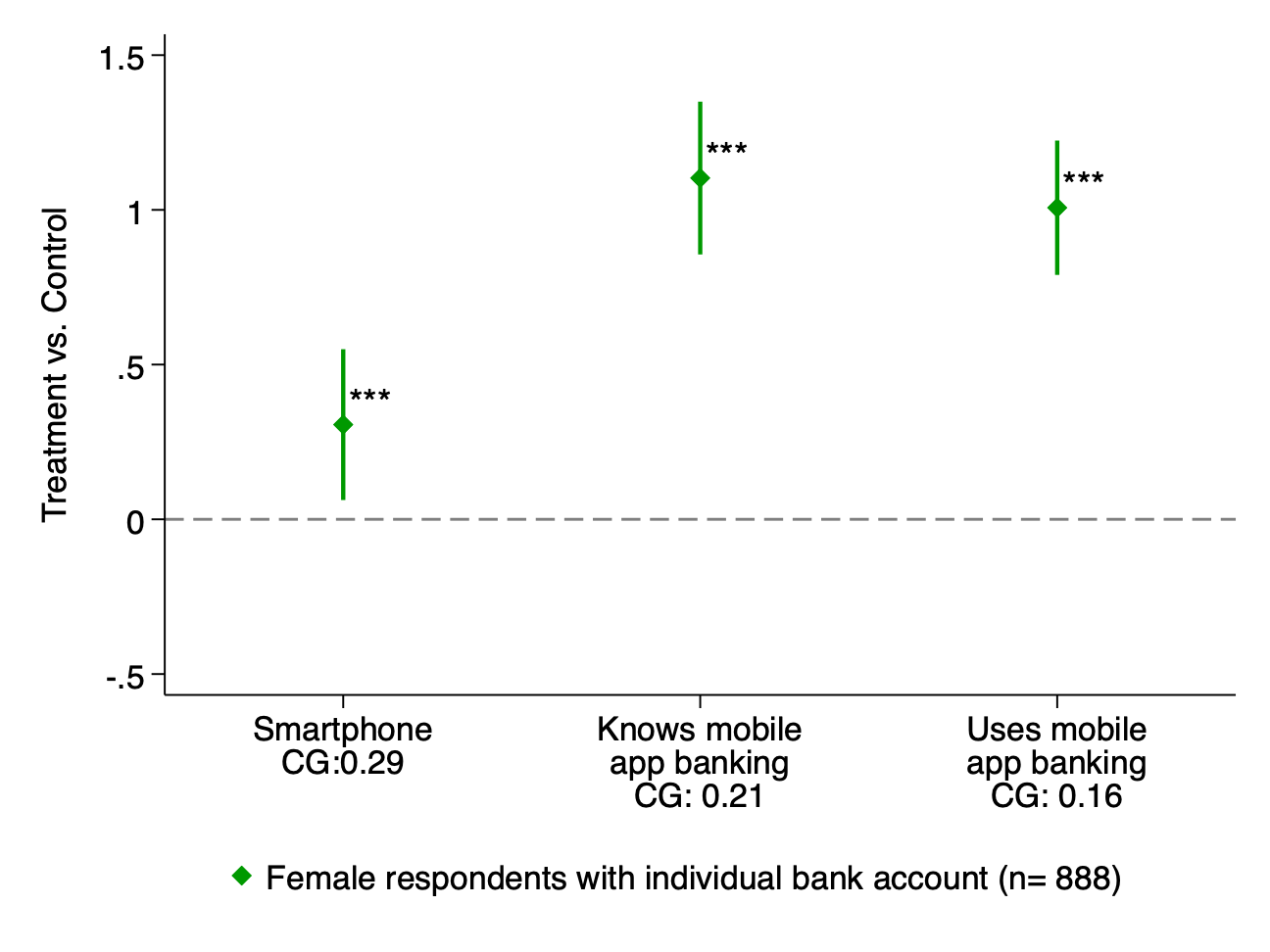

Some used the money for smartphones:

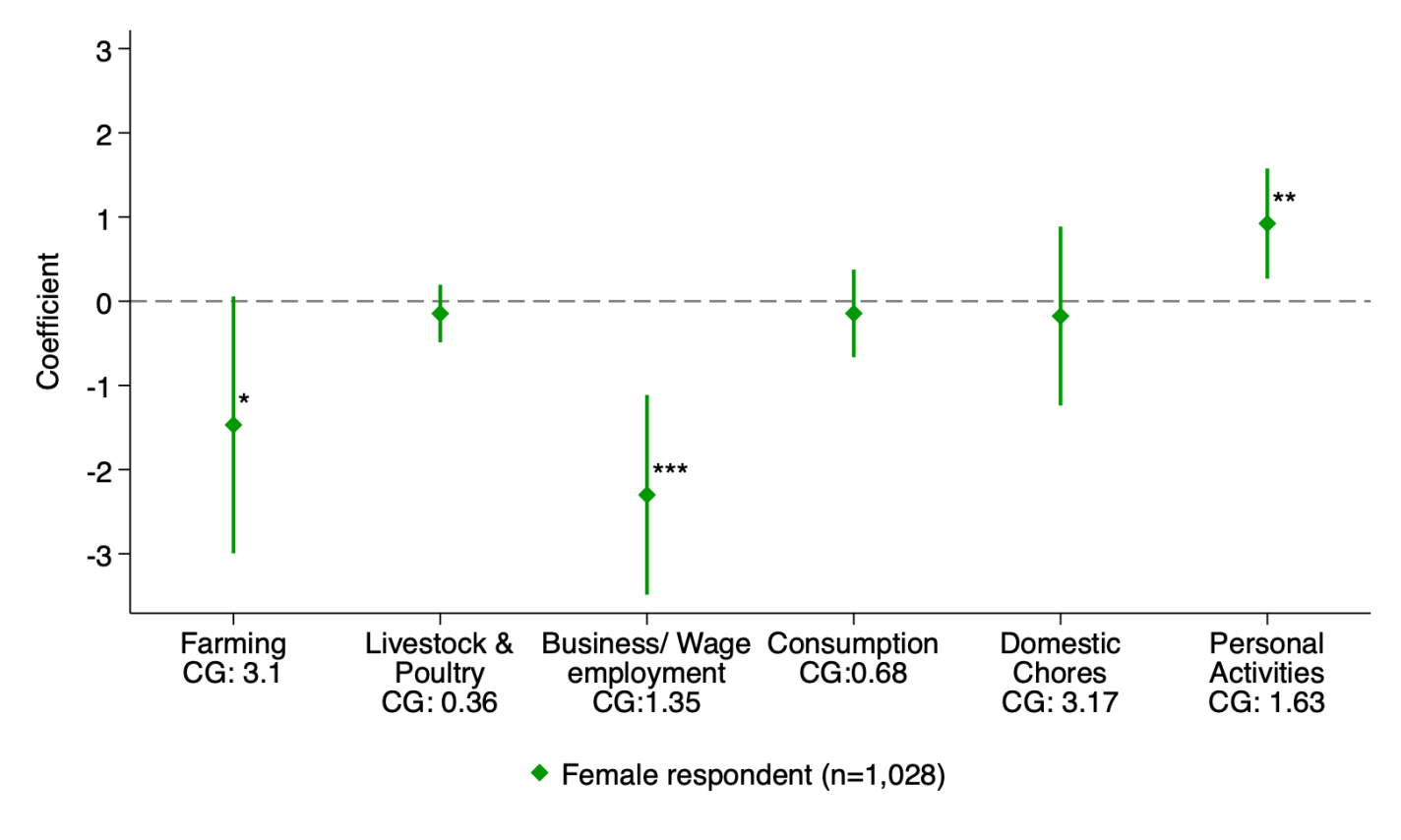

But for the most part they seem not to have spent the money on farming- they didn’t buy significantly more land, seeds, fertilizer, or farm equipment. They did spend more on “non-farm business equipment” and “large consumer durables”. Despite not producing more food themselves, they reported higher food security. Income stayed flat, but women were able to shift some time away from work and toward leisure:

I find these results surprising given how poor the households receiving the loans are. They earn the equivalent of about $1,000/yr, putting them around the global “extreme poverty” line. At that income level I’d think they would value additional income highly relative to leisure, and yet when they get the loan, work time goes down and leisure time increases. Could it really be the case that they’ve already hit their income target, and are on the backward bending part of the labor supply curve? Some other possibilities are that they don’t expect that investing in farming would increase yields enough to be worthwhile, or that they worry any increased income would be taken away through explicit or implicit taxes. But the households generally seem better off as a result of the loan.

The other surprise- enough of the loans were paid back that the lenders made a profit despite the research pushing the interest rate below-market.

So much has been happening in the banking world it is a little hard to keep track of it. See recent articles here by fellow bloggers Mike Makowsky, Jeremy Horpedahl, and Joy Buchanan. Here is a quick guide to all the drama.

Credit Suisse Takeover by UBS

Perhaps the biggest, newest news is a shotgun wedding between the two biggest Swiss banks announced over the weekend. Credit Suisse is a huge, globally significant bank that has suffered from just awful management over the last decade. Its missteps are a tale in itself. Its collapse would be an enormous hit to the Swiss financial mystique, and would tend to destabilize the larger western financial system. So the Swiss government strong-armed a takeover of Credit Suisse by the other Swiss bank behemoth, UBS, in an all-stock transaction. The government is providing some funding, and some guarantees against losses and liability. An unusual aspect of this deal is that Credit Suisse shareholders will get some value for their stock, but a whole class of Credit Suisse bonds Is being written down to zero. Usually bond holders have strong priority over stockholders, so this may make it more difficult for banks to sell unsecured bonds hereafter.

Silicon Valley Bank Collapse: Depositors Protected

The Silicon Valley Bank (SVB) collapse is old news by now. The mismanagement there is another cautionary tale: despite having a flighty tech/venture capital deposit base, management greedily reached for an extra 0.5% or so yield by putting assets into longer-term bonds that were vulnerable to a rise in interest rates instead of into stable short-term securities.

A key step back from the brink here was the feds coming to the rescue of depositors, brushing aside the existing $250,000 limit on FDIC guarantees. That was an important step, otherwise large depositors would stampede out of all the regional banks and take their funds to the few large banks that are in the too-big-to-fail category. It is true that this new level of guarantee encourages more moral hazard, since depositors can now be more careless, but the alternative to guaranteeing these deposits (i.e. the collapse of regional banks) was just too awful. Bank shareholders and most bondholders were wiped out. Presumably that will send a message to the investing community of the importance of risk management at banks.

The actual disposition of the business parts of SVB are still being worked out. The feds originally tapped the big, well capitalized banks to see if one of them would take over SVB as a going concern. That would have been a nice, clean, thorough resolution. But the big banks all declined. I suspect the actual responses in private were unprintable. Here’s why: in the 2008 banking crisis, the Obama-Biden administration went to the big banks and encouraged them to take over failing institutions like Countrywide Mortgage, who among other things had made arguably predatory loans to subprime borrowers who had poor prospects to keep up with the mortgage payments. The Obama administration’s Department of Justice promptly turned around and very aggressively prosecuted these big banks for the sins of the prior institutions. J. P. Morgan ended up paying something like 13 billion and Bank of America paid 17 billion. So when today’s Biden administration reached out to these big banks this month to see about taking over SVB, they got no takers.

Now the assets of SVB (renamed Silicon Valley Bridge Bank) are getting auctioned off, perhaps piecemeal, but how exactly that happens does not seem so critical.

Signature Bank: Shut Down, But Sold Off Intact

Crypto-friendly Signature Bank was shuttered by New York State officials on Sunday, March 12, making this the third largest (SVB was the second largest) bank failure in U.S. history. Forbes gives the whole story. At the end of last year, Signature had over $110 billion in assets and $88 billion in deposits. Spooked by Signature’s similarities to failed banks SVB and Silvergate, customers rushed to withdraw deposits, which the bank could not honor without selling securities at huge losses. As with SVB, the feds had the FDIC insure all deposits of all sizes at Signature.

Unlike SVB, Signature has received a bid for the whole business, from New York Community Bancorp’s subsidiary Flagstar Bank. Flagstar will take over most deposits and loans and other assets, and operate Signature Bank’s 40 branches.

First Republic: Teetering on The Brink, Propped Up by Banking Consortium

First Republic is in a somewhat different class than these other troubled institutions. Its overall practices seem reasonable, in terms of equity and assets. However, it caters to a wealthy clientele in the Bay Area, with a lot of accounts over the $250,000 threshold. In the absence of a rapid and decisive move by Congress to extend FDIC protection to all deposits at all banks, somehow (I haven’t tracked what started the stampede) depositors got to withdrawing huge amounts (like $70 billion) last week. This was a classic “run on the bank.” That would stress any bank, despite decent risk management. Once confidence is lost, it’s game over, since there are always alternative places to park one’s money. Ratings agencies downgraded First Republic to junk status, and the stock has cratered.

It is in the interest of the broader banking industry to forestall yet another collapse. If folks start to generally mistrust banks and withdraw deposits en masse, our whole financial system will be in deep trouble. In the case of First Republic, the private sector is trying to prop up it up, without a government takeover. So far this has mainly taken the form of depositing some $30 billion into First Republic, as deposits (not loans or equity), by a consortium of eleven large U.S. banks led by J. P. Morgan. This is was a quick and fairly unheroic intervention, since in the event of liquidation, depositors (including this consortium) have the highest claim on assets. This intervention will probably prove insufficient. Two potential outcomes would be a big issuance of stock to raise capital (which would dilute existing shareholders), or some large bank buying First Republic. The stock rose today on reports that Morgan’s Jamie Dimon was talking with other big banks about taking an equity stake in First Republic, possibly by converting some of the $30 billion deposit into equity.

Old News: Silvergate Bank Liquidation

Overshadowed by recent, bigger collapses, the orderly shutdown of the crypto-focused Silvergate Bank is old news. It was two weeks ago (March 8) that Silvergate announced it would shut down and self-liquidate. The meltdown of the crypto financing world led to excessive loss of deposits at Silvergate. Unlike SVB and Signature, it held a lot of its assets in more liquid, short-term securities, so its losses have not been as devastating – – all depositors will be made whole, though shareholders are toast (stock is down from $150 a year ago to $1.68 at Monday’s close).

Warren Buffett To the Rescue?

Banks generally operate on the model of borrow short/lend long: they “borrow” from depositors and buy longer-term securities. Normally, short-term rates are lower than long-term rates, so banks can pay out much lower interest on their deposits than they receive on their bond/loan investments. With the Fed’s rapid increases in short-term rates this past year, however, the rate curve is heavily inverted, which is disastrous for borrow short/lend long. Fortunately for banks, many depositors are too lazy to do what I have done, which is to move most of my immediate-need money out of bank accounts (paying maybe 1%) and into T-bills and money market funds paying 4-5%.

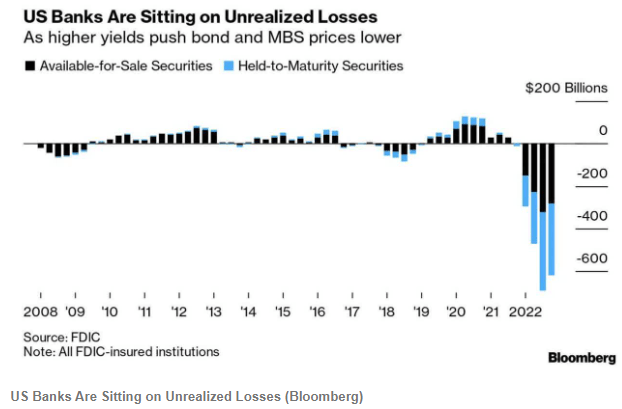

All this churn goes to highlight an inherent fragility of banks: there is typically a maturity mismatch between a bank’s deposits/liabilities (which are short-term and can be withdrawn at any time) and its assets (longer-term bonds it purchases, and loans that it makes which can be difficult to quickly liquidate). Runs on banks, where if you were late to panic you lost all your deposited money, used to be a real feature of life, as dramatized in classic films Mary Poppins and It’s a Wonderful Life. Eliminating this danger was a key reason for setting up the Federal Reserve system, and in general that has worked pretty well in the past hundred years. Banks in general (see chart above) are now carrying enormous amounts of unrealized losses on their portfolios of bonds and mortgage-backed securities (MBS) due to the increase in market rates. In addition to the existing “discount window” at which banks can borrow, the Fed has set up a new lending facility to help tide banks over if they (as in the case of SVB and Signature) get stressed by having to sell marked-down securities to cover withdrawal of deposits. Also, new measures reminiscent of 2008 were announced to extend dollar liquidity to central banks of other nations.

But when Gotham really has a problem, the Commissioner calls in the Caped Crusader. Warren Buffett has been in touch with administration officials about the banking situation. We wrote two weeks ago about Warren Buffett’s gigantic cash hoard from the float of his Berkshire Hathaway insurance businesses which allows him to quickly make deals that most other institutions cannot. Buffett rode to the rescue of large banks like Bank of America and Goldman Sachs in the 2008-2009 financial crisis. A lot of corporate jets have been noted flying into Omaha from airports near the headquarters of various regional banks. Buffett’s typical playbook in these cases is to have the troubled institution issue a special class of high yielding (with today’s regional banks, think: 9%) preferred stock that he buys, perhaps with privileges to convert into the common stock. That stock would count as much needed equity in the banks’ books.

The Renaissance in northern Italy was a period between roughly 1350 and 1550 (definitions vary) when a proto-modern outlook and culture and economy replaced feudal medieval society. We all know about the great artistic and literary and scientific advances made at this time and place. I got curious about the economics behind all this. It is clear that the cities of northern Italy, such as Florence, were extremely prosperous, otherwise they could not have funded all these artists and architects.

It has jokingly been said, “Ah, I don’t see what is so great about Shakespeare – – all he did was string together a bunch of famous quotes.” Well, since I know little about all this, what I will do here is mainly string together a bunch of relevant quotes. Let the citations begin….

This blurb from “helenlo-weebly” (?) gives a good overview, noting the importance of trade and the shift from rural barter to an urban money economy:

Trade brought many new ideas and goods to Europe. A bustling economy created prosperous cities and new classes of people who had enough money to support art and learning. Italian city-states like Venice and Genoa were located on the trade routes that linked the rest of western Europe with the East. Both these city-states became bustling trading centers. Trading ships brought goods to England, Scandinavia, and present-day Russia. Towns along trading routes provided inns and other services for traveling merchants.

The increase of trade led to a new kind of economy. During the middle ages people traded goods for other goods. During the Renaissance people began using coins to buy goods which created a money economy. Moneychangers were needed to covert one type of currency into another. Therefore, many craftspeople, merchants, and bankers became more important i society. Crafts people produced goods that merchants traded all over Europe. Bankers exchanged currency, loaned money, and financed their own business.

Some merchants and bankers grew very rich. They could afford to help make their cities more beautiful. Many became patrons and provided new buildings and art; they helped found universities. This led many city-states to become a flourishing educational and cultural center.

Bartleby.com notes technical advances in ship construction, and the rise of Florentine bankers: Genoa and Venice also made advancements in shipbuilding allowing ships to sail all year long and the increased the volume of goods that could be transported (accelerated speed)…Florentine merchants and bankers acquired control of papal banking (acting as tax collectors).

Brewminate notes the rise of modern commercial infrastructure (which depends on law and order, with contracts being honored) and the virtuous cycle of trade and urban craftsmanship promoting each other. Also, the economic and social impact of the Black Death (which is a huge topic of itself):

The Crusades had built lasting trade links to the Levant, and the Fourth Crusade had done much to destroy the Byzantine Empire as a commercial rival to Venice and Genoa. Thus, while northern Italy was not richer in resources than many other parts of Europe, its level of development, stimulated by trade, allowed it to prosper. Florence became one of the wealthiest cities of the region…

In the thirteenth century, Europe in general was experiencing an economic boom. The city-states of Italy expanded greatly during this period and grew in power to become de factofully independent of the Holy Roman Empire. During this period, the modern commercial infrastructure developed, with joint stock companies, an international banking system, a systematized foreign exchange market, insurance, and government debt. Florence became the center of this financial industry and the gold florin became the main currency of international trade.

The decline of feudalism and the rise of cities influenced each other; for example, the demand for luxury goods led to an increase in trade, which led to greater numbers of tradesmen becoming wealthy, who, in turn, demanded more luxury goods…

The Black Death [in the fourteen century] wiped out a third of Europe’s population, and the new smaller population was much wealthier, better fed, and had more surplus money to spend on luxury goods like art and architecture.

What motivated the newly rich urban elites to so assiduously patronize the arts? According to dailyhistory.org, it was largely a desire to assert one’s status and to curry favor with the local citizens:

The New Elites such as the De Medici used spectacles and display to assert themselves in society and to demonstrate their wealth. Wealthy members of the urban elite and the aristocracy were always keen to demonstrate their status. This need to publicize and affirm one’s status led to the patronage of great artists and writers to provide displays and exhibit the wealth and power of the elite. This need for others’ recognition was vital in the Renaissance, which led to the lavish patronage of the period. This led to a great deal of competition to patronize the best artists and writers.