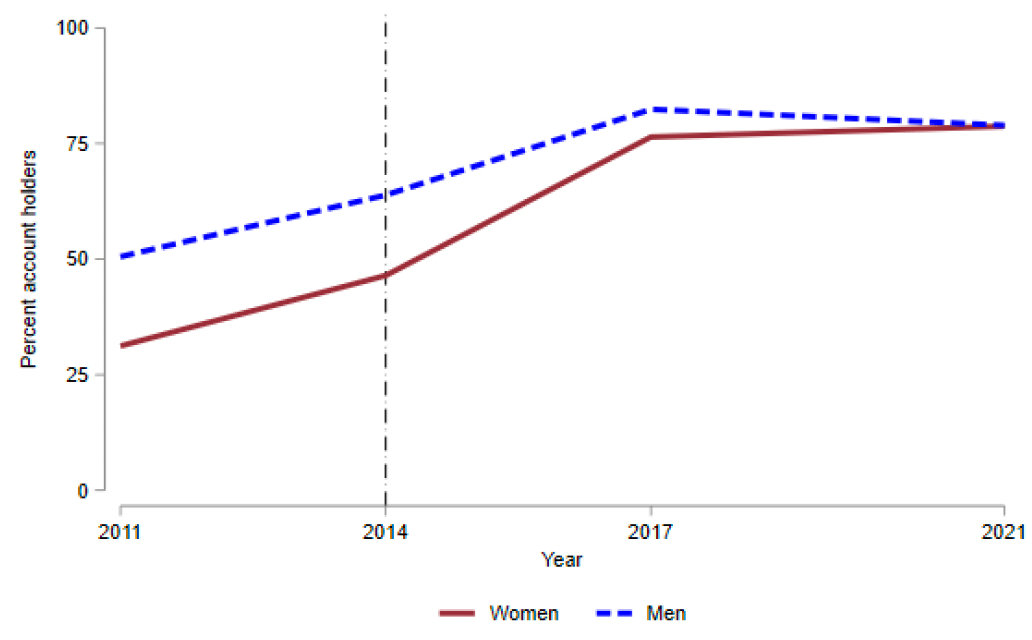

In 2014 India required banks to offer no-cost accounts. This led hundreds of millions of people to open bank accounts for the first time, and more than doubled the number of Indian women who had a bank account:

This increased households’ collective ability to save and borrow, but didn’t shift decision-making power towards women despite the larger change for them. That is the finding of a paper by Tarana Chauhan, a Brown University postdoc who is currently on the job market. The paper is a well-executed example of a difference-in-difference analysis of observational data- that is, carefully examining data that other people generated to examine events that help establish causality. But the validity of difference-in-difference strategies in separating correlation from causation can always be questioned, and always is in economics seminars.

So Dr. Chauhan, this time with coauthors Berber Kramer, Patrick Ward and Subhransu Pattnaik, followed up by directly running an experiment. They got a company to offer subsidized loans to hundreds of randomly selected Indian farmers, then surveyed the farmers to see if they behaved differently than a control group that didn’t get loans. The loans carried a 14% interest rate, which seems high to Americans but was apparently 10pp lower than the other options available in India. They wanted to know whether farmers would use the loans to improve farm productivity, and whether this would have any differential effects on women.

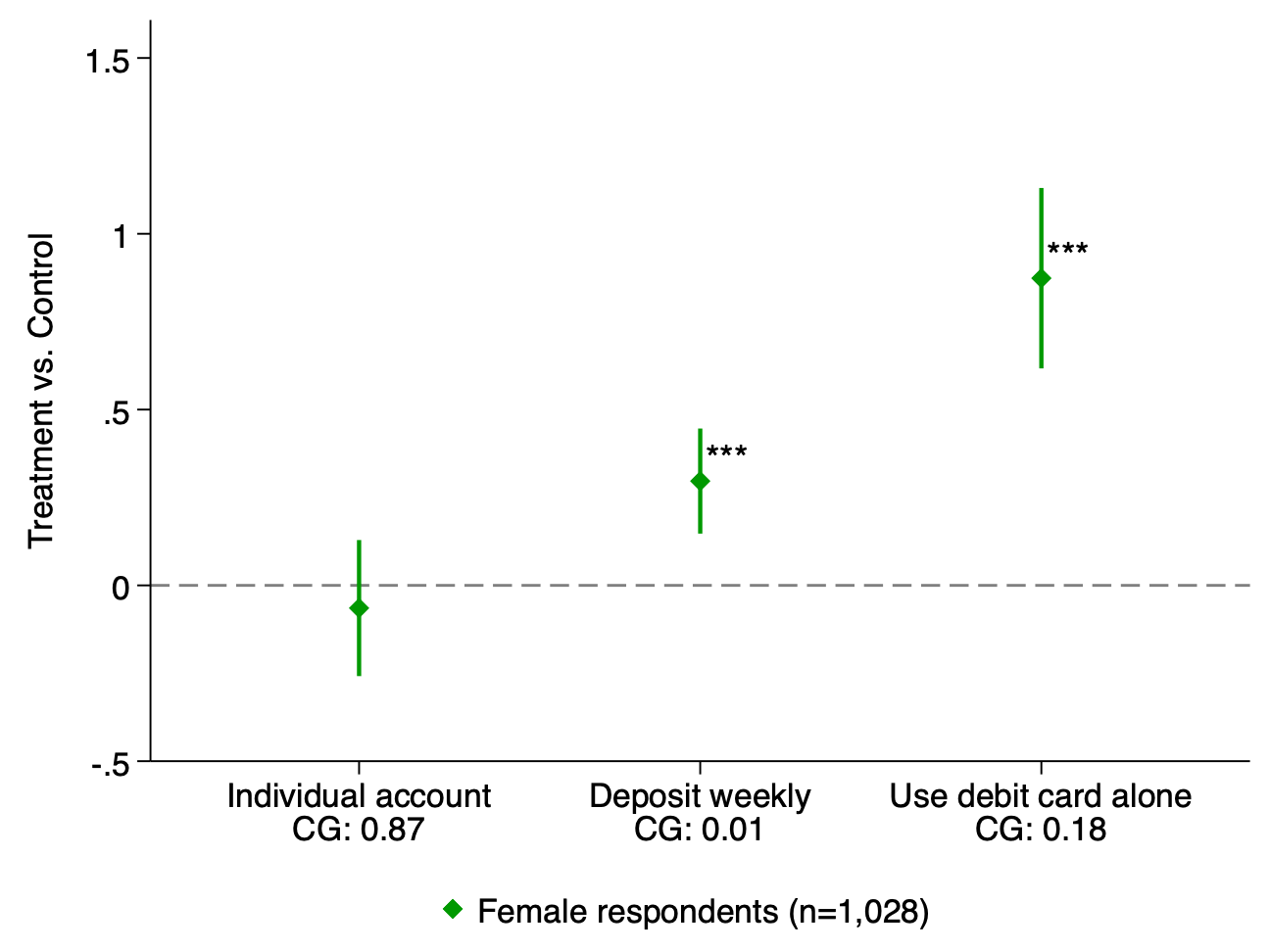

The first stage of the experiment worked: households took the loans and got more engaged with the financial system.

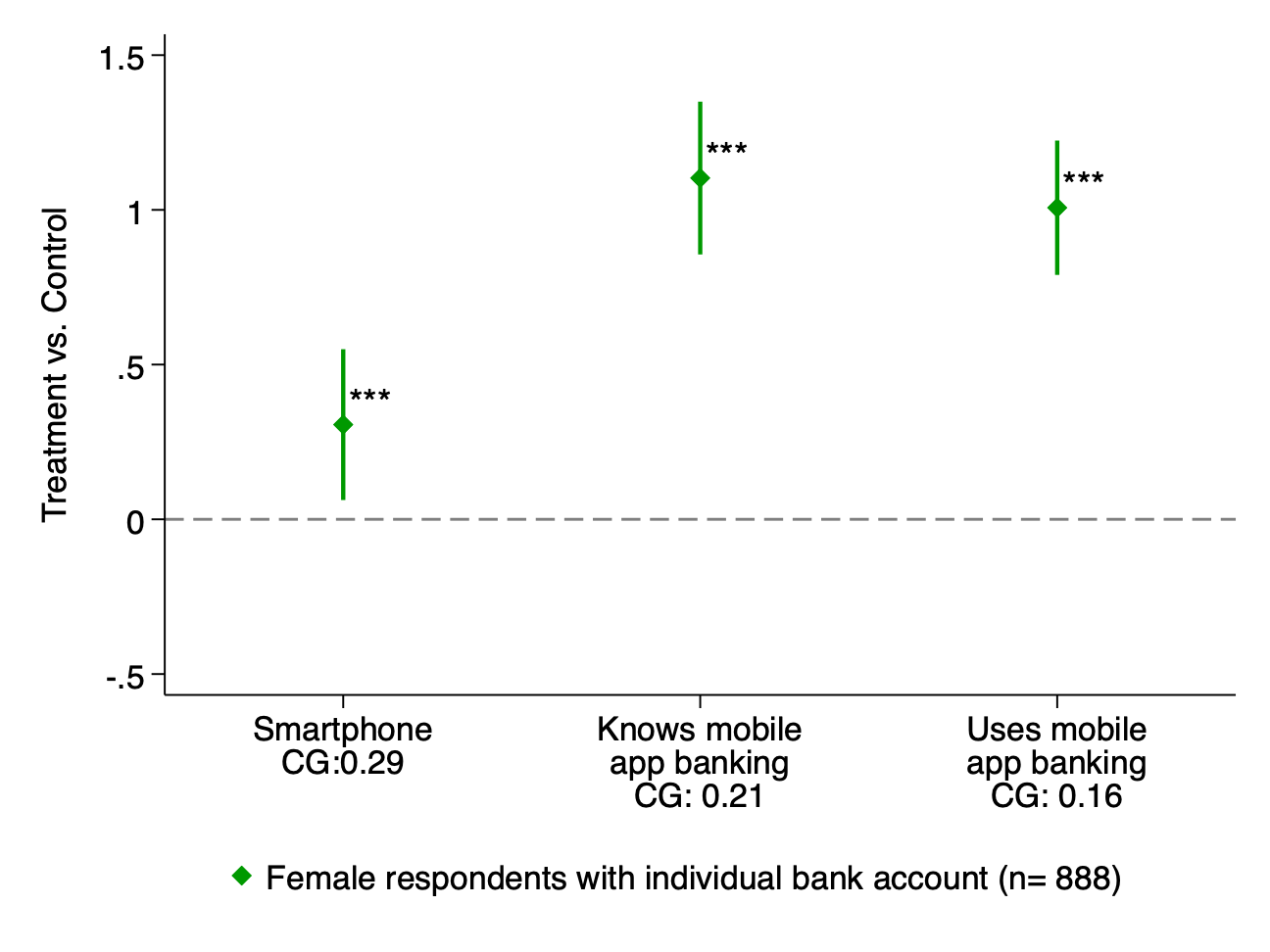

Some used the money for smartphones:

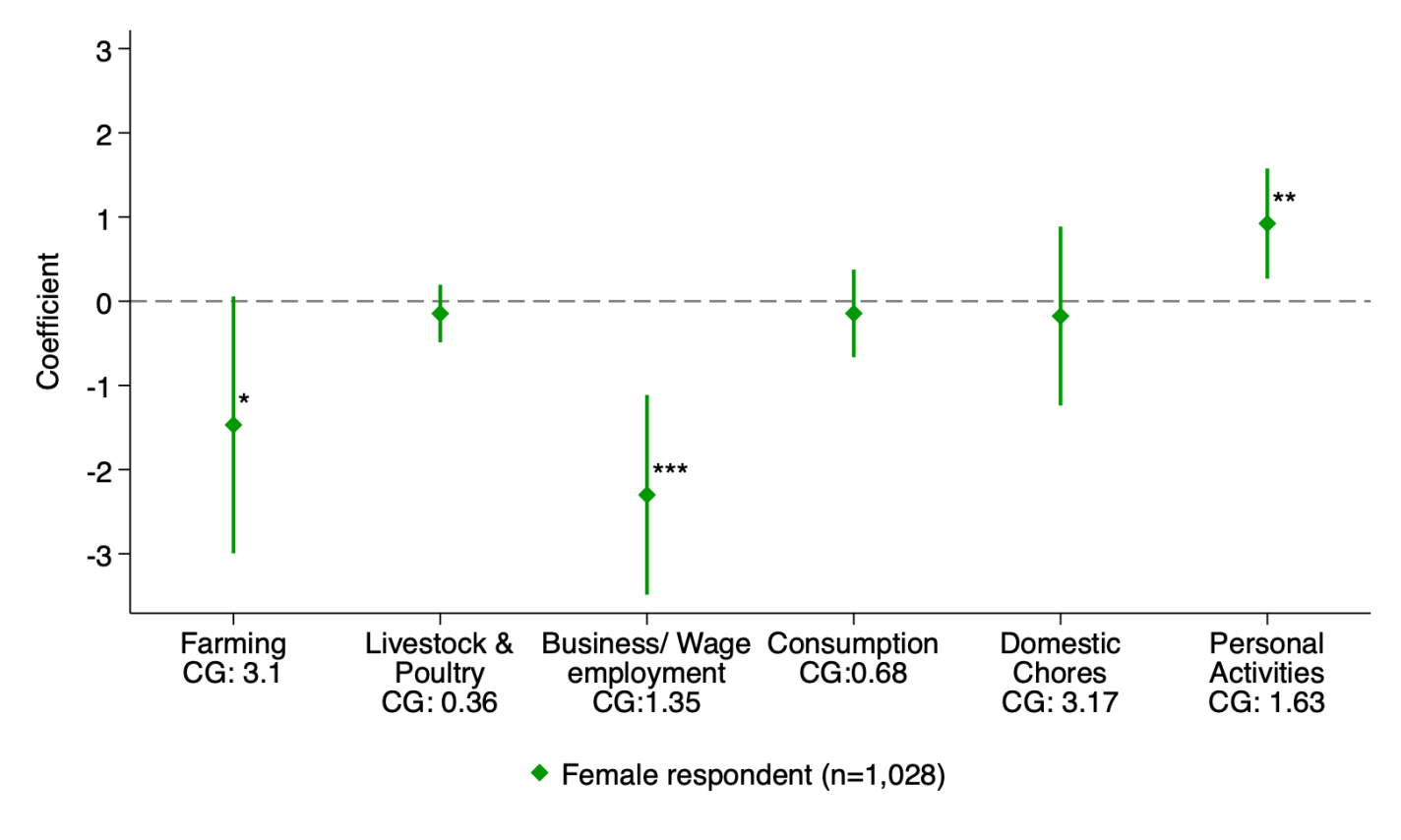

But for the most part they seem not to have spent the money on farming- they didn’t buy significantly more land, seeds, fertilizer, or farm equipment. They did spend more on “non-farm business equipment” and “large consumer durables”. Despite not producing more food themselves, they reported higher food security. Income stayed flat, but women were able to shift some time away from work and toward leisure:

I find these results surprising given how poor the households receiving the loans are. They earn the equivalent of about $1,000/yr, putting them around the global “extreme poverty” line. At that income level I’d think they would value additional income highly relative to leisure, and yet when they get the loan, work time goes down and leisure time increases. Could it really be the case that they’ve already hit their income target, and are on the backward bending part of the labor supply curve? Some other possibilities are that they don’t expect that investing in farming would increase yields enough to be worthwhile, or that they worry any increased income would be taken away through explicit or implicit taxes. But the households generally seem better off as a result of the loan.

The other surprise- enough of the loans were paid back that the lenders made a profit despite the research pushing the interest rate below-market.