The latest AI model from Anthropic is so powerful that they don’t dare release it to the public. It is such a threat that Jay Powell and Scott Bessant summoned the major bank CEOs to a meeting last week to warn them about it. In line with Anthropic’s “helpful, honest, and harmless” motto, they have released it only to their Project Glasswing partners. These are organizations like AWS, Apple, Cisco, CrowdStrike, Google, JPMorgan Chase, the Linux Foundation, Microsoft, NVIDIA, and Palo Alto Networks, who have been granted access to the model to identify and patch vulnerabilities in critical software.

Mythos is designed to identify and exploit vulnerabilities in software systems when prompted. Its specialty is identifying critical software vulnerabilities and bugs, but it can also assemble sophisticated exploits.

What makes Mythos particularly unsettling is that its most dangerous capabilities were not deliberately engineered. Anthropic’s team made it clear that they did not explicitly train Mythos to have these capabilities. Instead, they “emerged.”

Internal testing revealed that Mythos has already uncovered thousands of weak points in “every major operating system and web browser.” The implications are disturbing. Claude Mythos has autonomously discovered thousands of zero-day vulnerabilities in major operating systems and web browsers— flaws that human security researchers, working for years, had never detected. (see also here and here for examples).

Mythos can rapidly uncover hidden flaws in the codes of organizations and software development firms, but it also raises the fear that attackers could find those vulnerabilities first. Much of the underlying software that Mythos can scan supports banking, retail, airlines, hospitals, and critical utilities. Regulators worry that if Mythos, or models like it, fell into the wrong hands, “systemically important” banks and even entire financial networks could be compromised before institutions even knew they were exposed.

Anthropic launched Project Glasswing in April 2026 to collaborate with tech giants and banks to identify and fix vulnerabilities before they can be exploited. This year, organizations should expect a large influx of AI-discovered hack points in critical software. The game plan is to use AI tools to patch the vulnerabilities it discovers. Your venerable legacy system is no longer safe. What AI can expose, it can also fix. We hope.

Ray Kurzweil predicted The Singularity (when artificial intelligence growth accelerates beyond human control) would arrive in 2045, but we might be closing in on it ahead of schedule.

As you drive through cities and many suburbs near cities, you see lot and lots and lots of office buildings. Employees by the tens of millions used to get dressed and fight their way through traffic to get to these building every weekday, park, and go up to their desks to do their white-collar jobs.

The demand for new office space seemed endless, and so developers borrowed money to build more office buildings, and firms like real estate investment trusts (REITs) also borrowed money to buy such buildings in order to rent them out.

Covid changed all that. Suddenly, in early/mid 2020, nearly all office buildings went dark, and people started working from home. With affordable computers and internet access, and with Zoom and other conferencing tools, it was found that workers could get their jobs done remotely. Even after vaccines rolled out in early/mid 2021, concerns over contagious Covid variants kept offices closed. 2022 was when things started opening up again big time, and by end 2022/early 2023 there were stories in the news about companies ordering employees back to their desks.

By January, 2023 Bloomberg could report “More than half of workers in major US cities went to the office last week, the first time that return-to-office rates crossed 50% of their pre-pandemic levels.” However, that movement seems to have stalled, and has even reversed in some cases, as workers have pushed back strongly against being forced back to the cubes. Notably, Elon Musk initially banned remote work at Twitter after taking it over in November, but after rethinking the costs of maintaining offices, has shut down Twitter’s offices in Seattle and Singapore, telling employees to work from home

Per the Morning Consult, “The pandemic lockdown triggered one of the swiftest, most significant behavior changes in human history. People’s habits changed overnight, and through the successive lockdowns, shutdowns and new standards, these new habits became ingrained. The experience triggered new, positive associations with working from home, working out with virtual trainers, cooking, gardening and more. A vast web of neural pathways formed to hold these new associations – and that web runs deep.”

And thus, many office buildings remain largely empty, which in turn is resulting in rising defaults on the loans for these buildings. A number of high profile corporate owners in recent months have deliberately (in their own pecuniary interest) defaulted on their loans, forfeited their equity interest in a building , and handed the keys back to the mortgage lenders, who are now stuck with big losses on their loans and with holding a building that nobody much wants.

There are many ramifications of these trends. The one I will focus on is how this extended underutilization of offices affects the parties that lent money to build or buy these buildings. In many cases, those lenders were smaller (regional) banks. They have much greater exposure to commercial real estate loans than the larger banks, which may cause serious problems in the coming months.

Eric Basmajian calls out some key differences between large and small banks in the U.S.:

At large US banks, loans make up 51% of total assets. Small banks have 65% loans as a percentage of total assets. So small banks have a lot of loans, and large banks have a lot of cash, Treasury bonds, and MBS.

…At small US banks, loans make up 65% of assets. Of that loan portfolio, real estate is 65%, meaning a lot of real estate exposure….Within that real estate loan portfolio, almost 70% was commercial real estate lending. So small banks have a high concentration of commercial real estate loans…. Within the commercial real estate category, the highest concentration is “non-residential property,” which can include office buildings, retail stores, and data centers.

….So small banks have a potentially large problem. Deposits are starting to leave after the SVB crisis in search of more safety, but also in search of higher yields on safe assets like Treasury bills. Deposit outflows will make it hard for small banks to grow lending and may cause a deleveraging. If deposit outflows are severe, deleveraging will cause banks to sell securities or loans.

Securities can be pledged at the Fed for a relatively high-interest rate. This keeps a bank solvent but at a material hit to earnings. The loan portfolio is a much bigger problem because the value of these potentially permanently impaired assets will be called into question.

Basmajian summarizes:

There are major differences between large and small US banks.

Large banks hold a lot of reserves, Treasuries, MBS, and residential real estate loans. The asset mix at large banks is very conservative.

Small banks have most of their assets in loans, with commercial real estate holding the highest weight. Small banks appear to have outsized exposure to highly impaired office buildings which could generate significant losses.

It will be critical to monitor lending standards and availability at small banks because, in the post-2008 cycle, small banks are the lifeblood of credit to the private economy.

The Fed was founded after a spat of banking crises.

We know that the Federal Reserve also has the goals of full employment and steady, moderate inflation. Since the 1990s, that’s meant 2%. But it’s a relatively recent addition to the Fed’s policy goals. The primary purpose was initially and always has been financial system stability.

In 2008, the Fed demonstrated that it’s willing to attain financial stability at the cost of employment. After and during the financial crisis, the Fed purchased mortgage backed securities (MBS) from private banks at a time when their value was highly uncertain (and discounted). The purpose was to replace these assets of uncertain value with less risky assets. At the time, there was resentment that these security holders were insulated from losses while the homeowners whose loans composed the MBS did not get comparable relief. I remember arguing that the Fed, with the cooperation of congress, could have just paid part of the mortgages on behalf of the homeowners such that there were fewer foreclosures and fewer personal bankruptcies. That way, both the borrowers wouldn’t default and the debt holders would enjoy stable returns.

But, the primary goal of the Fed is financial system stability. Pre-financial crisis, banks had loaded-up on securities of uncertain value with the help of regulatory arbitrage and some lending shenanigans. The Fed needed to avoid the ensuing catastrophe that was a consequence of the greater-than-anticipated realized risk. Importantly, catastrophe to the Fed is financial-sector specific. Markets losing liquidity, bank-runs, and financial sector business failures all qualify as the stuff of concern (all of which occurred). While making mortgage payments for specific mortgages would have been popular amongst many debtors, it also would have taken much more time to implement. The Fed wanted to avoid more financial instability than had already occurred. And frankly, the Fed’s first priority isn’t to take care of the public. Given the alternative between a slow popular option and a quick adequate option, the Fed has demonstrated an inclination toward the latter.

It has been a tumultuous several weeks in the world of finance. Just when “soft landing” (i.e., the notion that Fed rate hikes would tame inflation without causing a nasty recession) was the meme, a string of banks went belly-up. We summarized the history and status of this dismal parade of corpses a week ago.

On Friday, Germany’s Deutsche Bank (DB) was added to the list of endangered financial species. Its share price plunged as the cost of insuring its credit swaps soared, a sign of lack of confidence in DB among other financial parties. As best I can discern, however, DB is a relatively poorly-managed bank, but not one teetering on insolvency like Credit Suisse or the smaller American banks that have collapsed.

Silicon Valley Bank Getting Sold Off, Finally

On this side of the pond, the big news is that Silicon Valley Bank (SVB), whose spectacular implosion was really what brought “crisis” to banking, will be taken over by another regional bank, First Citizens Bank of North Carolina. The first attempt to auction off SVB was a fizzle, so the feds tried again. They really, really wanted to get this kind of full takeover deal done (rather than breaking up SVB and selling off bits piecemeal), so First Citizens was able to drive a juicy bargain. First Citizens was a fairly modest-sized bank, about half the size of SVB at the end of last year. First Citizens will get SVB assets of $110 billion, deposits of $56 billion and loans of $72 billion, and will start operating the SVB branch offices again. They will pay only $55 billion for the nominal $72 billion in loans that SVB had made, a 29% mark-down. The cost to the FDIC for this deal is about $20 billion. (I don’t know how First Citizens is paying for this acquisition). First Citizens stock skyrocketed on this news, so the market sees this as a sweet deal for First Citizens.

Going forward, the FIDC has pledged to share any losses (or gains) on those loans in the future, which offers further protection to First Citizens. FDIC gets shares of First Citizens valued up to $500 million. First Citizens decided not to take an additional $90 billion in securities that the FDIC will now have to sell on its own. These are likely the long-term bonds which sunk SVB when their value cratered with rising interest rates this past year. I’m not sure how much further losses the FDIC will bear on these bonds.

Anyway, so far, so good, kind of; it is sobering to note that this $20 billion cost to the FDIC just chewed up 1/6 of its total $128 billion kitty for backstopping all qualifying deposits at all banks in America. So we can’t readily afford too many more meltdowns of this magnitude.

Bank Deposits Continue to Flee, But Slower

A worrisome trend in the past month or so has been for depositors to pull their funds from bank checking/savings accounts, and stash their money instead in higher yielding money market funds or CDs or Treasury bills. Banks have borrowed records amounts from the Fed in recent weeks, in order to have lots of cash on hand if they have to pay off departing clients. And within the banking system, about half a trillion dollars has been moved from smaller regional banks to large banks.

I can’t find the reference now, but in the past two days I read an article stating that rate of deposit withdrawals is slowing down, and will likely not of itself destabilize the system. I’m going with that narrative, for now.

An indirect fallout from all this bank turmoil is the reduced inclination of banks to extend loans to businesses. This will make for a slowdown in economic activity, which should cool off inflation – -which is exactly what Jay Powell was hoping would be the outcome of the Fed rate hikes.

So much has been happening in the banking world it is a little hard to keep track of it. See recent articles here by fellow bloggers Mike Makowsky, Jeremy Horpedahl, and Joy Buchanan. Here is a quick guide to all the drama.

Credit Suisse Takeover by UBS

Perhaps the biggest, newest news is a shotgun wedding between the two biggest Swiss banks announced over the weekend. Credit Suisse is a huge, globally significant bank that has suffered from just awful management over the last decade. Its missteps are a tale in itself. Its collapse would be an enormous hit to the Swiss financial mystique, and would tend to destabilize the larger western financial system. So the Swiss government strong-armed a takeover of Credit Suisse by the other Swiss bank behemoth, UBS, in an all-stock transaction. The government is providing some funding, and some guarantees against losses and liability. An unusual aspect of this deal is that Credit Suisse shareholders will get some value for their stock, but a whole class of Credit Suisse bonds Is being written down to zero. Usually bond holders have strong priority over stockholders, so this may make it more difficult for banks to sell unsecured bonds hereafter.

Silicon Valley Bank Collapse: Depositors Protected

The Silicon Valley Bank (SVB) collapse is old news by now. The mismanagement there is another cautionary tale: despite having a flighty tech/venture capital deposit base, management greedily reached for an extra 0.5% or so yield by putting assets into longer-term bonds that were vulnerable to a rise in interest rates instead of into stable short-term securities.

A key step back from the brink here was the feds coming to the rescue of depositors, brushing aside the existing $250,000 limit on FDIC guarantees. That was an important step, otherwise large depositors would stampede out of all the regional banks and take their funds to the few large banks that are in the too-big-to-fail category. It is true that this new level of guarantee encourages more moral hazard, since depositors can now be more careless, but the alternative to guaranteeing these deposits (i.e. the collapse of regional banks) was just too awful. Bank shareholders and most bondholders were wiped out. Presumably that will send a message to the investing community of the importance of risk management at banks.

The actual disposition of the business parts of SVB are still being worked out. The feds originally tapped the big, well capitalized banks to see if one of them would take over SVB as a going concern. That would have been a nice, clean, thorough resolution. But the big banks all declined. I suspect the actual responses in private were unprintable. Here’s why: in the 2008 banking crisis, the Obama-Biden administration went to the big banks and encouraged them to take over failing institutions like Countrywide Mortgage, who among other things had made arguably predatory loans to subprime borrowers who had poor prospects to keep up with the mortgage payments. The Obama administration’s Department of Justice promptly turned around and very aggressively prosecuted these big banks for the sins of the prior institutions. J. P. Morgan ended up paying something like 13 billion and Bank of America paid 17 billion. So when today’s Biden administration reached out to these big banks this month to see about taking over SVB, they got no takers.

Now the assets of SVB (renamed Silicon Valley Bridge Bank) are getting auctioned off, perhaps piecemeal, but how exactly that happens does not seem so critical.

Signature Bank: Shut Down, But Sold Off Intact

Crypto-friendly Signature Bank was shuttered by New York State officials on Sunday, March 12, making this the third largest (SVB was the second largest) bank failure in U.S. history. Forbes gives the whole story. At the end of last year, Signature had over $110 billion in assets and $88 billion in deposits. Spooked by Signature’s similarities to failed banks SVB and Silvergate, customers rushed to withdraw deposits, which the bank could not honor without selling securities at huge losses. As with SVB, the feds had the FDIC insure all deposits of all sizes at Signature.

Unlike SVB, Signature has received a bid for the whole business, from New York Community Bancorp’s subsidiary Flagstar Bank. Flagstar will take over most deposits and loans and other assets, and operate Signature Bank’s 40 branches.

First Republic: Teetering on The Brink, Propped Up by Banking Consortium

First Republic is in a somewhat different class than these other troubled institutions. Its overall practices seem reasonable, in terms of equity and assets. However, it caters to a wealthy clientele in the Bay Area, with a lot of accounts over the $250,000 threshold. In the absence of a rapid and decisive move by Congress to extend FDIC protection to all deposits at all banks, somehow (I haven’t tracked what started the stampede) depositors got to withdrawing huge amounts (like $70 billion) last week. This was a classic “run on the bank.” That would stress any bank, despite decent risk management. Once confidence is lost, it’s game over, since there are always alternative places to park one’s money. Ratings agencies downgraded First Republic to junk status, and the stock has cratered.

It is in the interest of the broader banking industry to forestall yet another collapse. If folks start to generally mistrust banks and withdraw deposits en masse, our whole financial system will be in deep trouble. In the case of First Republic, the private sector is trying to prop up it up, without a government takeover. So far this has mainly taken the form of depositing some $30 billion into First Republic, as deposits (not loans or equity), by a consortium of eleven large U.S. banks led by J. P. Morgan. This is was a quick and fairly unheroic intervention, since in the event of liquidation, depositors (including this consortium) have the highest claim on assets. This intervention will probably prove insufficient. Two potential outcomes would be a big issuance of stock to raise capital (which would dilute existing shareholders), or some large bank buying First Republic. The stock rose today on reports that Morgan’s Jamie Dimon was talking with other big banks about taking an equity stake in First Republic, possibly by converting some of the $30 billion deposit into equity.

Old News: Silvergate Bank Liquidation

Overshadowed by recent, bigger collapses, the orderly shutdown of the crypto-focused Silvergate Bank is old news. It was two weeks ago (March 8) that Silvergate announced it would shut down and self-liquidate. The meltdown of the crypto financing world led to excessive loss of deposits at Silvergate. Unlike SVB and Signature, it held a lot of its assets in more liquid, short-term securities, so its losses have not been as devastating – – all depositors will be made whole, though shareholders are toast (stock is down from $150 a year ago to $1.68 at Monday’s close).

Warren Buffett To the Rescue?

Banks generally operate on the model of borrow short/lend long: they “borrow” from depositors and buy longer-term securities. Normally, short-term rates are lower than long-term rates, so banks can pay out much lower interest on their deposits than they receive on their bond/loan investments. With the Fed’s rapid increases in short-term rates this past year, however, the rate curve is heavily inverted, which is disastrous for borrow short/lend long. Fortunately for banks, many depositors are too lazy to do what I have done, which is to move most of my immediate-need money out of bank accounts (paying maybe 1%) and into T-bills and money market funds paying 4-5%.

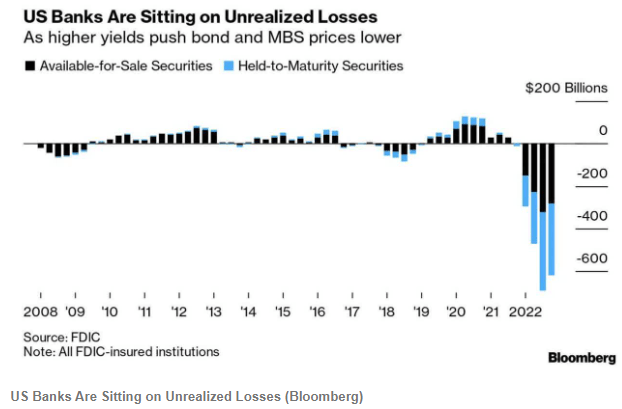

All this churn goes to highlight an inherent fragility of banks: there is typically a maturity mismatch between a bank’s deposits/liabilities (which are short-term and can be withdrawn at any time) and its assets (longer-term bonds it purchases, and loans that it makes which can be difficult to quickly liquidate). Runs on banks, where if you were late to panic you lost all your deposited money, used to be a real feature of life, as dramatized in classic films Mary Poppins and It’s a Wonderful Life. Eliminating this danger was a key reason for setting up the Federal Reserve system, and in general that has worked pretty well in the past hundred years. Banks in general (see chart above) are now carrying enormous amounts of unrealized losses on their portfolios of bonds and mortgage-backed securities (MBS) due to the increase in market rates. In addition to the existing “discount window” at which banks can borrow, the Fed has set up a new lending facility to help tide banks over if they (as in the case of SVB and Signature) get stressed by having to sell marked-down securities to cover withdrawal of deposits. Also, new measures reminiscent of 2008 were announced to extend dollar liquidity to central banks of other nations.

But when Gotham really has a problem, the Commissioner calls in the Caped Crusader. Warren Buffett has been in touch with administration officials about the banking situation. We wrote two weeks ago about Warren Buffett’s gigantic cash hoard from the float of his Berkshire Hathaway insurance businesses which allows him to quickly make deals that most other institutions cannot. Buffett rode to the rescue of large banks like Bank of America and Goldman Sachs in the 2008-2009 financial crisis. A lot of corporate jets have been noted flying into Omaha from airports near the headquarters of various regional banks. Buffett’s typical playbook in these cases is to have the troubled institution issue a special class of high yielding (with today’s regional banks, think: 9%) preferred stock that he buys, perhaps with privileges to convert into the common stock. That stock would count as much needed equity in the banks’ books.

Seventy trillion dollars is a lot of money. It is nearly three times the size of the U.S. GDP, and approaches total global GDP (around $100 trillion). That is the amount of funds that are missing from normally reported financial statistics, according to a December, 2022 report from the Bank for International Settlements. That report caused a bit of a flurry in financial circles.

It’s not that this money has been stolen, it’s just that it is not publicly known exactly where it is, i.e., how much money that which parties owe to whom. Here is the Abstract of this paper:

FX swaps, forwards and currency swaps create forward dollar payment obligations that do not appear on balance sheets and are missing in standard debt statistics. Non-banks outside the United States owe as much as $25 trillion in such missing debt, up from $17 trillion in 2016. NonUS banks owe upwards of $35 trillion. Much of this debt is very short-term and the resulting rollover needs make for dollar funding squeezes. Policy responses to such squeezes include central bank swap lines that are set in a fog, with little information about the geographic distribution of the missing debt.

Much of this money is in the form of currency swaps, especially foreign exchange (FX) swaps. Even though the U.S. economy no longer dominates the whole world, the U.S. dollar remains the premier basis for international trade and even more for foreign exchange:

As a vehicle currency, the US dollar is on one side of 88% of outstanding positions – or $85 trillion. An investor or bank wanting to do an FX swap from, say, Swiss francs into Polish zloty would swap francs for dollars and then dollars for zloty.

Who cares? Well, the incessant demand for dollars periodically leads to a dollar funding squeeze in international trade, which in turn reverberates into world GDP.

Currency Swaps as Lending Events

In many cases these currency swaps effectively amount to short-term lending /borrowing (of dollars). Much of the financial world is utterly dependent on smoothly flowing short-term funding to cover longer term debt or investments. Borrowing short-term (at usually lower interest rates) and investing or lending out longer-term (at higher rates) is how many institutions and funds exist. For instance, depositors at banks effectively lend their deposits to the bank (short-term), in return for some pitiful little interest on their checking or savings accounts, while the banks turn around and make say 5 year or 30-year loans to businesses or home-buyers. Banks earn profits on the spread between the interest rates they receive on the funds they loan out, and the typically lower rates on the short term funds they “borrow” from their depositors.

This “mismatch” between the maturities of borrowed funds (especially dollars) and invested funds can cause a complete melt-down of the financial system if holders of dollars stop being willing to lend them out, or to lend them out at less than ruinous interest rates:

The very short maturity of the typical FX swap/forward creates potential for liquidity squeezes. Almost four fifths of outstanding amounts at end-June 2022 in Graph 1.B matured in less than one year. Data from the April 2022 Triennial Survey show not only that instruments maturing within a week accounted for some 70% of FX swaps turnover, but also that those maturing overnight accounted for more than 30%. When dollar lenders step back from the FX swap market, the squeeze follows immediately.

Financial customers dominate non-financial firms in the use of FX swaps/forwards. Non-bank financial institutions (NBFIs), proxied by “other financial institutions” in Graph 1.C, are the biggest users of FX swaps, deploying them to fund and hedge portfolios as well as take positions. Despite their long-term foreign currency assets, the likes of Dutch pension funds or Japanese life insurers roll over swaps every month or quarter, running a maturity mismatch. For their part, dealers’ non-financial customers such as exporters and importers use FX forwards to hedge trade-related payments and receipts, half of which are dollar-invoiced. And corporations of all types use longer-term currency swaps to hedge their own foreign currency bond liabilities .

It is really bad if pension funds or insurance companies get starved of needed ongoing funding. Central banks, especially the dollar-rich Fed, have had to repeatedly jump in and spray dollar liquidity in all directions to mitigate these “dollar squeezes”. The BIS authors’ main concern is that these big public policy decisions are currently made in absence of data on what the actual needs and issues are. Hence, “Policy responses to such squeezes include central bank swap lines that are set in a fog.”

This all is part of the murky “Eurodollar” universe of dollar-denominated bank deposits circulating outside the U.S. (more on this some other time). Investing adviser Jeffery Snider offers the “Eurodollar University” on podcasts and on YouTube, in which he explores the many dimensions of the Eurodollar scene. He likens the Eurodollar system to a black hole: we cannot observe it directly, but we can estimate its size by its effects.

In his YouTube talk on this BIS paper, among other things Snider notes that this short-term lending associated with currency swaps functions much like repo borrowing, except the currency swaps (unlike repo) do not appear on bank or other balance sheets as assets/liabilities. That is part of the attraction of these swaps, since they are effectively invisible to regulators and are not constrained by e.g., capital requirements.

What the Fed does in a dollar squeeze is largely lend dollars to large dealer banks. But unless those other banks then lend those dollars out into the private marketplace of manufacturers and shippers and pension funds, having trillions of dollars in central bank reserves has little effect. It is not the case that “the Fed floods the world with dollars” — actually, mainstream banks get those dollars, and then lend out at high rates to the dollar-starved rest of financial world, where they can actually do something.

The result, according to Snider, is that the Eurodollar is the only functional reserve currency in existence. This is the real, effective banking system (not “reserves” sitting on some bank’s balance sheet), even though the current accounting system doesn’t show it.

Some eighteen months ago, I wrote here on “Money as a Social Construct“. Most civilizations over the millennia have found it expeditious to move from simple, immediate barter of physical objects like cows to some system involving “money”. But what is money? Wikipedia gives the following standard definition:

Money is any object or record that is generally accepted as payment for goods and services and repayment of debts in a given socio-economic context or country. The main functions of money are distinguished as: a medium of exchange; a unit of account; a store of value.

For convenience, the “thing” used as money is best if it is portable and durable and of limited amount. Gold and silver have historically served these purposes. Even though these are physical objects, their actual value in usage (e.g. how much gold does it take to buy a cow) is arbitrary. Its value in usage is whatever is agreed upon by the users.

For this system of money to work, the key players all have to believe in the value of the gold coins. Thus, money is a mainly social construct, an article of mutual faith. If people lose faith in the value of some form of non-commodity money, it will in fact become valueless.

We have moved from useful commodities like cows, to gold coins and bars, to printed dollar bills redeemable in gold, and now to fiat currencies not formally tied to any physical objects. And in the twenty-first century, most “money” is not even tangible printed bills, but is in the form of digital entries in accounts “somewhere”.

Trillions of dollars’ worth of transactions take place every year, on the supposition that the dollar you deposit in a major bank will be there next week or next year. At my own personal level, nearly all of my life savings exists in the form of investments in stocks or bonds of corporate entities, which are held in accounts that I only ever access from my computer. Thus, I rely on on-going functional, reasonably honest government to enforce rules on the stewardship of those funds at multiple levels. So I am betting everything on the supposition that law and order prevail.

Well, in war sometimes “law and order” do break down and the normal rules of stewardship are over-ridden. Such has been the case with Russian foreign reserves. The central banks of major nations hold assets in the form of accounts at other central banks. Russia, as a big net exporter, has accumulated reserves of dollars and other currencies at the central banks of various nations in the West. In the wake of Russia’s invasion of Ukraine, the Western banks froze some 630 million of Russian assets held in these banks. There has even been discussion of redeploying these assets to pay for assistance to Ukraine.

(Sadly, as I noted in How Overzealous Green Policies Force Europe to Bankroll Putin’s Military, these seemingly dramatic fund seizures and SWIFT sanctions are annoying but not crippling for Russia. Europe is still funneling billions of euros a month to Russia, because Europe has made itself utterly dependent on Russian natural gas due to prematurely chopping its own nuclear and coal power generation and banning the fracking process that has unlocked such enormous oil and gas production in the U.S.)

It is understandable why the West has taken such a step, in view of the unjustified Russian attack on Ukraine, and the ongoing atrocities such as the bombing of a maternity hospital and a clearly-marked children’s shelter. However, this action may lead to worldwide reappraisals of what is money and how net export nations choose to store their monetary surpluses.

The Wall Street Journal ran a piece called, “If Russian Currency Reserves Aren’t Really Money, the World Is in For a Shock.” It is suggested that central banks may be motivated to accumulate more of their reserves in the form of physical gold, held in their own countries, which cannot be confiscated by some outside forces. Or we may even go back to using “cows” as a store of value, with central banks gaining title to piles of useful commodities such as wheat or nickel or palladium.

Good hockey players skate to where the puck is heading. I bought into a fund of corn futures yesterday. After posting this article, I think I will log into my brokerage account and buy some shares in a fund holding physical gold.

Money can be simplistically defined as “A medium that can be exchanged for goods and services and is used as a measure of their values on the market, and/or a liquifiable asset which can readily be converted to the medium of exchange”. Earlier we described the amounts of various classes of “money” in the U.S. Here is a chart showing the amount of currency in circulation (coins and bills; lowest line on the chart) for 2005-2020, and also M1 (green), M2 (upper curve, purple) and “monetary base” (currency plus reserves at the Fed; red line).

To recap what M1 and M2 are:

M1: Physical currency circulating outside of the Fed and private banking system, plus the amount of demand deposits, travelers’ checks and other checkable deposits. This is highly “liquid” money, i.e. accepted and used for transactions in the private economy.

M2: M1 + most savings accounts, money market accounts, retail money market mutual funds, and small denomination time deposits (certificates of deposit of under $100,000).

The funds in these additional savings and money market accounts can in general be easily transferred to checkable accounts, and thus could go towards making purchases if desired.

Physical currency is made and put into circulation by the government or quasi-governmental agencies (the Treasury mints coins, and the Federal Reserve prints bills). But what about all the other money (M1, M2, etc.), which dwarfs the physical currency? How does it grow?

Without getting into all the weeds, it turns out that the major driver of money creation in modern economies is the process of bank loans. The vast majority of money in countries like the U.S. is not created directly by government or central bank operations, but is created in the private sector when commercial banks make loans. When individuals or companies decide to take out more loans (including loans for cars, houses, or business investment), the effective money supply in the nation increases. This is true for other modern economies. For instance, the Bank of England states:

There are three types of money in the UK economy:

3% Notes and coins

18% Reserves

79% Bank deposits

A typical scenario of how bank lending increases money might go something like this: Fred would like to add an enclosed back porch to his house, but doesn’t have the money in hand to pay a carpenter to build it for him. So the base case is no payment to the carpenter and no porch for Fred. However, Fred realizes he can go the bank and get a loan to pay for the porch. So he obtains a $20,000 loan from the bank, which first shows up as a $20,000 credit to Fred’s checking account. The bank credits Fred’s account, and in exchange obtains a contract from Fred promising that Fred will pay it back, with interest.

Fred writes a check for $20,000 to the carpenter, who in turn pays $10,000 to a lumberyard for materials and keeps the other $10,000 as his fee. The lumberyard is able to pay its workers for that day, and order replacement lumber from a mill. The workers spent their pay on various items. The carpenter puts $5000 of his $10,000 fee in a savings account, and pays the rest to a car dealer for a used car.

The initial loan to Fred set off a chain of spending and economic activity, which would not have otherwise occurred. Fred has his porch, the lumberyard workers continue to be employed and supporting their local merchants, the carpenter gets a second car, and this money keeps ricocheting around until it gets drained away into stagnant savings, or is used to pay down prior debt. Although they are not aware of it, part of the lumberyard workers’ pay for that day came out of the debt incurred by Fred.

The granting of that loan created $20,000 of spending capability, i.e. money. As far as the economy is concerned, that $20,000 did not exist as effective money prior to the loan. Thus, the money came into existence simultaneously with the debt associated with the loan. Fred received the capacity to spend $20,000 today, but in turn accepted the obligation to pay back this money, with interest. It is assumed that Fred had a stable income, such that he would in fact be able to pay back the loan in the future.

In general, increasing debt increases the money supply, and paying down debt extinguishes money. For simplicity, suppose Fred repays the $20,000 loan (with $2000 interest added) in one big lump, two years later. In that year, he will presumably spend into the economy something like $22,000 less than he would have otherwise. Thus, his paying down of his debt will act as a decrease in the circulating money.

In normal times, as one person is paying down his loan (and thereby shrinking the money supply), someone else is taking out a new and even larger loan, so total debt and the amount of money in circulation stays about the same, or grows somewhat. A feature of the 2008-2009 recession, however, was a big drop in consumer demand for credit; folks decided to pay down debts and not borrow so much money to buy stuff. The effect was a big drop in spending and thus in overall economic activity (GDP) and in employment.

Where was that $20,000 before Fred borrowed it? We might think that it was sitting unused in the bank vaults, just waiting to be borrowed. That turns out to be an incorrect picture of the lending process.

Bank loans differ in key ways from, say, an interpersonal loan. If I lend you money, I might draw down my checking deposit and give you a check which you would deposit in your bank account. No new money is created. You may hand me an I.O.U. slip stating when you will pay me back and with what interest, but that would still be just the same funds being traded back and forth between the two of us. I would have to have the money in my account to start with before I could loan it to you.

Bank lending is different. A bank can lend money and hence create a new deposit, which amounts to brand-new money, even if the bank does not have that money to start with. This is counterintuitive. In a later post we may flesh out this seemingly magical aspect of bank lending. See Overview of the U. S. Monetary System for a more complete discussion.

A balance sheet gives a snapshot of a corporation’s assets and liabilities. The difference between total assets and total liabilities is (by definition) the value of the equity owned by the owners or shareholders of the company.

With, say, a manufacturing firm, the assets would include tangible items such as buildings and equipment and inventory, and intangibles such as cash, bank accounts, and accounts receivable. Liabilities may include mortgages and other loans, and accounts payable such as taxes, wages, pensions, and bills for purchased goods.

The balance sheet for a bank is different. The “Assets” are mainly loans that the bank has made, plus some securities (such as US Treasury bonds) that the bank has purchased. These assets pay interest to the bank. The money the bank used to make these loans and purchase these securities came mainly from customer deposits or other borrowings by the bank (which are considered “Liabilities” of the bank), and also from paid-in capital from the bank owners/shareholders. [1] As usual, the current equity of the bank is assets minus liabilities. Thus:

The Federal Reserve System is a complex beast. We will not delve into all the components and moving parts, but just take a look at the overall balance sheet.

Unlike other banks, the Fed has the magical power of being able to create money out of thin air. Technically, what the Fed can do with that money is mainly make loans, i.e. buy interest-bearing securities such as government bonds. The Fed makes its transactions through affiliated banks, so it credits a bank’s reserve account with a million dollars, if it buys from that bank a million dollars’ worth of bonds. Those bonds then become part of the Fed’s “assets”, while the reserve account of the bank at the Fed (which is a liability of the Fed) becomes larger by a million dollars. Since the Fed is not a for-profit bank, the “Equity” entry on its balance sheet is nearly zero. Thus, total assets are essentially equal to total liabilities.

The Fed also has the power of literally printing money, in the form of Federal Reserve Notes (printed dollar bills). These, too, are classified as liabilities. Thus, you are probably carrying in your wallet right now some of the liabilities of the central bank of the United States.

Before 2008, the balance sheet of the Fed was under a trillion dollars. Nearly all the “Liabilities” were the Federal Reserve Notes and nearly all the “Assets” were US Treasury securities. The reserve accounts of the affiliated Depository Institutions was minuscule. All that changed with the Global Financial Crisis of 2008-2009. To help stabilize the financial system, the Fed started buying lots of various types of securities, including mortgage-backed securities (MBS) [2]. The Fed thus propped up the value of these securities, and injected cash (liquidity) into the system.

Here is a plot of how the assets of the Fed ballooned in the wake of the GFC, from about $ 0.9 trillion to over $ 4 trillion:

The initial purchases in 2008 were US Treasuries, which the Fed had prior authorization to do. To buy other securities, especially the mortgage products, required congressional authorization. The increased liabilities of the Fed which offset these purchases were mainly in the form of larger reserve accounts of the affiliated banks. The Fed started paying interest on these reserve accounts, to keep short term interest rates above zero at all times (otherwise the whole money market in the U.S. might implode).

With the Fed relentlessly buying the mortgage and bond products, the interest rates on long-term mortgages and bonds was kept low. This was deemed good for economic growth. The Fed tried to sell off some securities to taper down its balance sheet in 2018, but that effort blew up in its face – – the stock market started crashing in response in late 2018, and so the Fed backtracked . You can look at weekly tables of the Fed balance sheet here.

Anyway, the GFC and its aftermath provided the precedent for massive purchases of “stuff” by the Fed. When the Covid shutdown of the economy hit in March of this year, the Fed very quickly went into high gear. Its balance sheet shot up from $4 trillion to $7 trillion in just a few months. It bought not only Treasuries and MBS, but corporate bonds. This was way outside the Fed’s original charter, but the crisis was so intense that nobody seemed to care whether these actions were legal or not. And now, to finance the huge deficit spending of the federal government in the wake of the shutdowns, the Fed has been buying up nearly the entire issuance of Treasury bonds and notes.

These actions may have long term consequences we will explore in later posts [3]. For now, the Fed has made it clear that it will keep interests rates near zero for at least the next couple of years. Invest accordingly.

ENDNOTES

[1] Huge caveat: This statement gives the impression that a bank must first receive say a thousand dollar deposit before it can make a thousand dollar loan. That is not the case. The reality is just the opposite: the act of making a thousand dollar loan actually CREATES a corresponding thousand dollar deposit. This is very counterintuitive, and I won’t try to explain or justify this point here.

[2] Technically, the Fed is not “buying” the mortgage-backed security (MBS). Rather, it is making a “loan” to the bank, and holding the MBS as collateral against that loan.

[3] It is now harder to take the federal deficit seriously as a constraint on spending: the government can issue unlimited bonds to fund deficits, which the Fed will purchase to keep interest rates low. Yes, the government has to pay interest on those bonds, but the Fed has to return most of that interest to the Treasury, so the real cost to the government of that extra debt is low.