It will be interesting to see if this ends up taking a place in the set of Fed surveys that are always driving economic discussions, like the Survey of Consumer Finances and the Survey of Professional Forecasters. If they keep it up and start putting out some graphics to summarize it, I think it will. My quick impression (not yet having spoken to Fed people about it) is that it will be the “quick hit” version of the Survey of Consumer Finances. It asks a smaller set of questions on somewhat similar topics, but is released quickly after each quarter instead of slowly after each year. If they stick with the survey it will get more useful over time, as there is more of a baseline to compare to.

But a year later the survey now has what I hoped for: a solid baseline for comparisons, and pre-made graphics to summarize the results. It continues to show complex and mixed economic performance in the US. People think the economy is getting worse:

They are cutting discretionary (but not necessity) spending at record levels:

They are worried about losing their jobs at record levels:

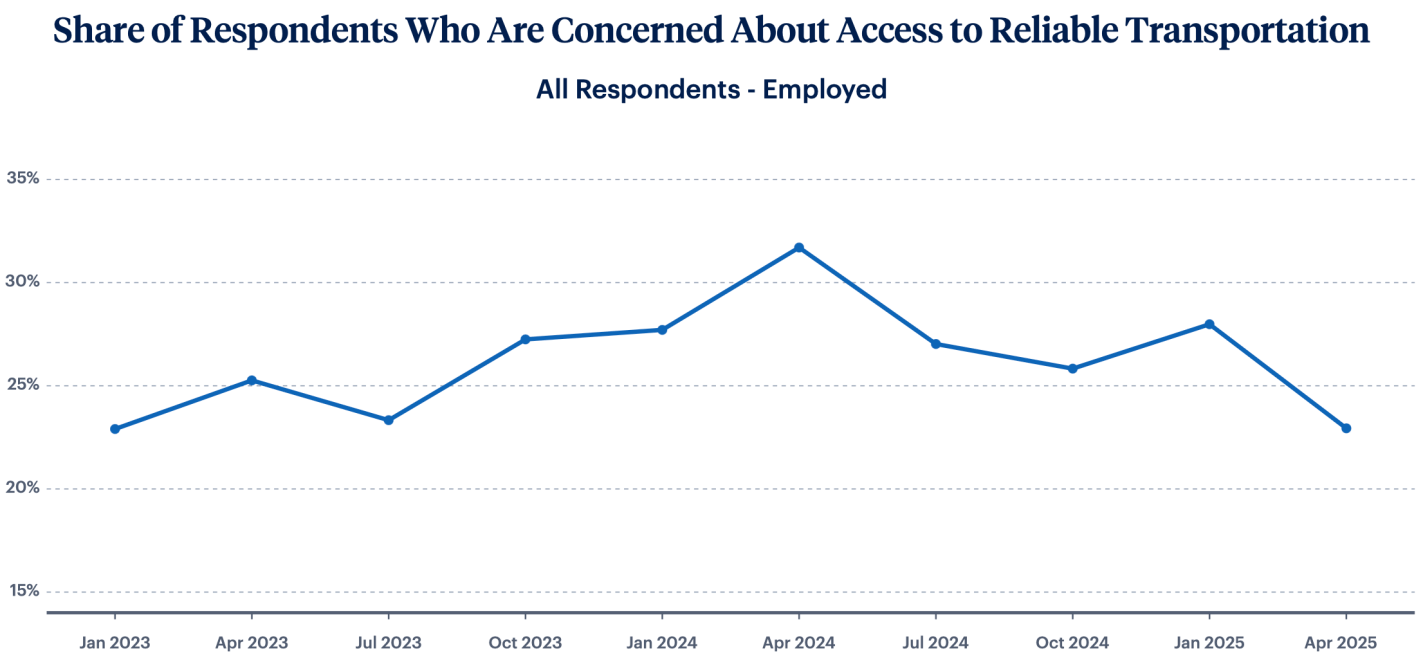

But key areas like housing, childcare, and transportation are stabilizing:

Overall I think we can synthesize these seemingly contradictory pictures by saying that Americans’ finances are fine now, but they are quite worried that things are about to get worse, perhaps due to the tariffs taking effect. You can find the rest of the LIFE survey results (including all the non-record-setting ones) here.

Small, rural, private schools stand out to me as the most likely to show up on lists of closed colleges. This summer I discussed a 2020 paper by Robert Kelchen that identified additional predictors using traditional regression:

sharp declines in enrollment and total revenue, that were reasonably strong predictors of closure. Poor performances on federal accountability measures, such as the cohort default rate, financial responsibility metric, and being placed on the most stringent level of Heightened Cash Monitoring

Kelchen just released a Philly Fed working paper (joint with Dubravka Ritter and Doug Webber) that uses machine learning and new data sources to identify more predictors of college closures:

The current monitoring solution to predicting the financial distress and closure of institutions — at least at the federal level — is to provide straightforward and intuitive financial performance metrics that are correlated with closure. These federal performance metrics represent helpful but suboptimal measures for purposes of predicting closures for two reasons: data availability and predictive accuracy. We document a high degree of missing data among colleges that eventually close, show that this is a key impediment to identifying institutions at risk of closure, and also show how modern machine learning algorithms can provide a concrete solution to this problem.

The paper also provides a great overview of the state of higher ed. The sector is currently quite large:

The American postsecondary education system today consists of approximately 6,000 colleges and universities that receive federal financial aid under Title IV of the federal Higher Education Act…. American higher education directly produces approximately $700 billion in expenditures, enrolls nearly 25 million students, and has approximately 3 million employees

Falling demand from the demographic cliff is causing prices to fall, in addition to closures:

Between the early 1970s and mid-2010s, listed real tuition and fee rates more than tripled at public and private nonprofit colleges, as strong demand for higher education allowed colleges to continue increasing their prices. But since 2018, tuition increases have consistently been below the rate of inflation

Most college revenue comes from tuition or from state support of public schools; gifts and grants are highly concentrated:

Research funding is distributed across a larger group of institutions, although the vast majority of dollars flows to the 146 institutions that are designated as Research I universities in the Carnegie classifications…. Just 136 colleges or university systems in the United States had endowments of more than $1 billion in fiscal year 2023, but they account for more than 80 percent of all endowment assets in American higher education. Going further, five institutions held 25 percent of all endowment assets, and 25 institutions held half of all assets

Now lets get to closures. As I thought, size matters:

most institutions that close are somewhat smaller than average, with the median closed school enrolling a student body of about 1,389 full-time equivalent students several years prior to closure

As does being private, especially private for-profit (states won’t bail you out when you lose money):

As do trends:

variables measuring ratios of financial metrics and those measuring changes in covariates are generally more important than those measuring the level of those covariates

When they throw hundreds of variables into a machine learning model, it can predict most closures with relatively few false positives, though no one variable stands out much (FRC is Financial Responsibility Composite):

My impression is that the easiest red flag to check for regular people who don’t want to dig into financials is “is total enrollment under 2000 and falling at a private school”.

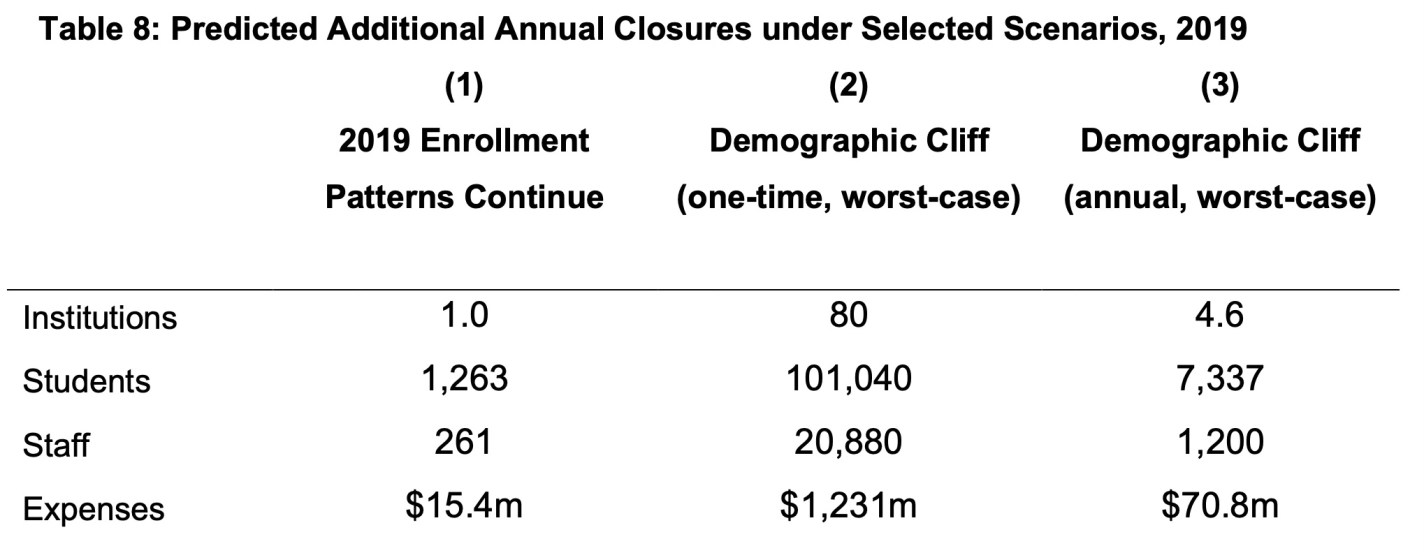

They predict that the coming Demographic Cliff (the falling number of new 18-year-olds each year) will lead to many more closures, though nothing like the “half of all colleges” you sometimes hear:

The full paper is available ungated here. I’ll close by reiterating my advice from the last post: would-be students, staff, and faculty should do some basic research to protect themselves as they consider enrolling or accepting a job at a college. College employees would also do well to save money and keep their resumes ready; some of these closures are so sudden that employees find out they are out of a job effective immediately and no paycheck is coming next month.

Yesterday Jeremy discussed what spiking car prices mean for overall inflation.

Today I’ll discuss the outlook for car prices themselves, based on what I heard at the Philly Fed’s conference on auto lending yesterday. Some (approximate) quotes:

The used market is red hot

Used prices are likely to stay elevated for a few years

Because used prices are so high, “If you can find the car you are looking for new right now, there’s a good chance it makes sense to buy it instead of going used.” But it could be hard to find that new car you want because inventories are so low, and even then you probably won’t be able to bargain the price down like you normally would- “75% of new cars now sell for MSRP or above, vs 36% last year”

The average new car now sells for $40k, partly because SUVs are increasingly popular, and partly to bother those who care about financial responsibility, like fellow Temple Econ PhD Adam Ozimek:

Spending $40,000 on a car seems like the kind of thing to me that, intuitively, you do when you have like a couple million in wealth and make $400,000 a year. But absolutely normal people do it all the time! Blows me away

Because of manufacturing disruptions from Covid and the chip shortage, “We’re at least a year out before we start to restock to normal dealer inventory levels” in the new market. Supply in the used market could stay low for 4-5 years because of the lower production of new cars and lower turnover of existing ones. Normally cars coming off lease & out of rental car fleets are a big sources of used cars for sale, but fleet purchases & leases are down from 40% of new car purchases to 25%. Reposessions, another source of used cars, actually decreased slightly through Covid despite the huge spike in unemployment.

All in all, its a good time to own a car and a bad time to try to buy one, and this state of affairs could persist for years absent an unexpected drop in demand or spike in supply.

Electric cars, though, seemed poised to take over much more of the market- the forecast was about 1/3 of new sales by 2030, driven by improvements in the technology, continued subsidies to new EV purchases & EV infrastructure, and car companies offering electric models in popular categories like SUVs and trucks where they are currently rare.