You have probably seen the latest inflation data. The headline number is 5.4% increase in prices in the past year as measured by the CPI-U. That’s a lot! Even the Core CPI (removing volatile food and energy) is up 4.5%.

If you follow the data closely, you may also have heard that a big chunk of that increase comes from prices related to automobiles: new cars, used cars, rental cars, car parts. All way up!

If you are in the market to buy a car, or if you really need a rental, it’s a bad time for prices. (Conversely, if you have an extra car sitting around, it’s a great time to sell!)

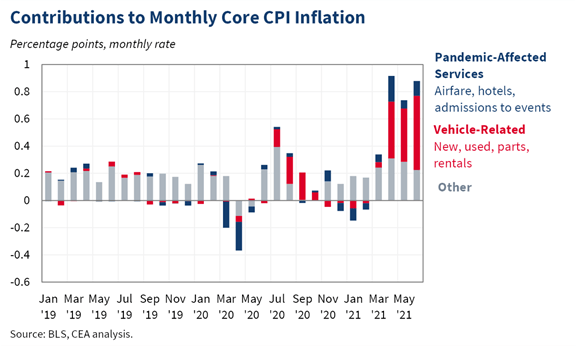

But what if you aren’t in the market for a car? What does the inflation data look like? The White House CEA tweeted out this chart to deconstruct the factors in the recent CPI release.

What does it all mean?

In short, about 60% of the increase of Core CPI is related to cars. That means the increase excluding cars in about 2.7%. That’s a little above the past decade worth of annual averages, which have been 1.7-2.2%, but on its own nothing really to be alarmed about.

But isn’t removing categories that are going up quickly “cheating” and artificially lowering the inflation rate?

Of course in some sense, yes, it is cheating. Ideally we should include all prices that a consumer faces. But if we unpack that further, perhaps it is not cheating since most consumers won’t actually face those prices.

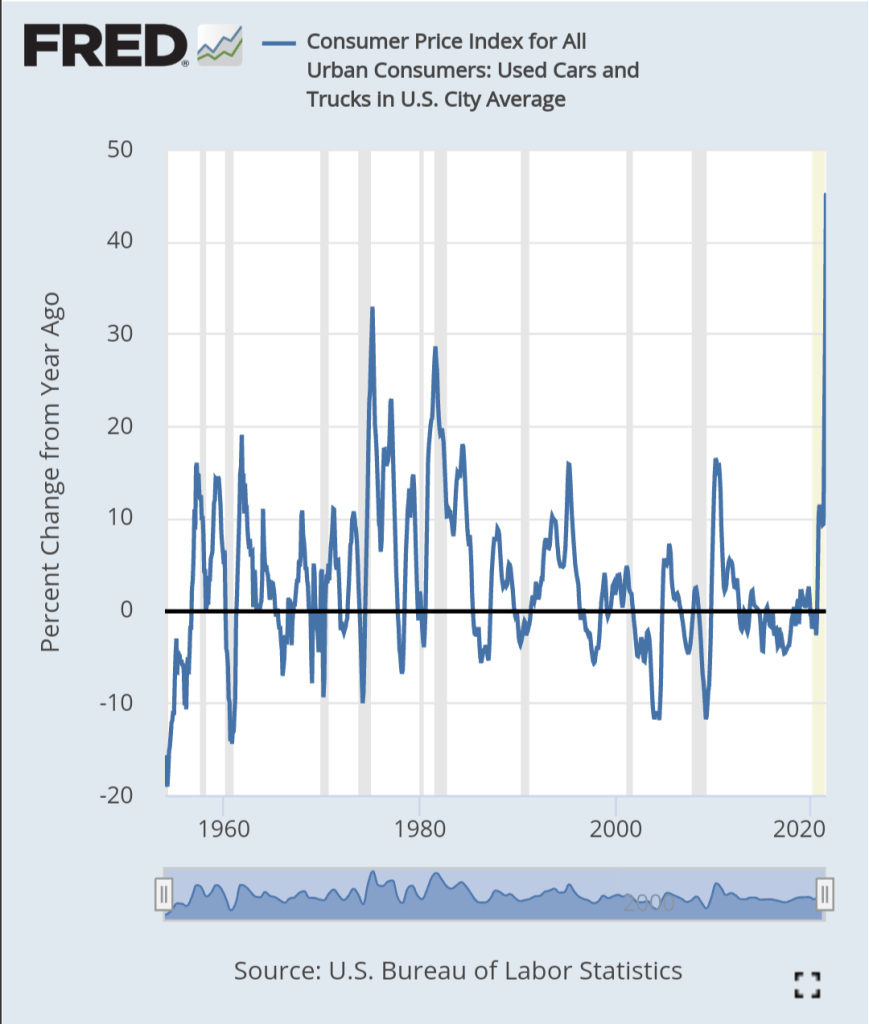

Take used cars as an example. On average, used cars are 45% more expensive than they were last June. Yikes! That’s the largest increase ever reported, going back to 1952.

We could try to dig into why prices of cars are increasing so much, but let’s do something simpler. Let’s think about how it impacts the typical consumer. (EDIT: my co-blogger Scott Buchanan had a great explanation for the price increases in cars back in March — excellent prediction.)

Used cars and trucks make up about 3% of the CPI. But not all consumers spend 3% of their total spending on used cars every month. For most of us, most months, it’s actually 0%. Of course, many households do have a car payment every month, but this payment does not go up just because current sales prices are increasing.

So if you aren’t in the market for an automobile, inflation right now is at pretty normal levels for you. This, of course, could change. Measures of the money supply are up significantly since before the pandemic — for example, M2 has increased by 32%. As that new money works its way through the economy, it would be strange if we didn’t see some broader price inflation.

Lately I have seen a lot of people quoting Milton Friedman’s famous line that “Inflation is always and everywhere a monetary phenomenon.” But keep in mind a few things. First, by “inflation” Friedman meant a “steady and sustained rise in prices.” I think so far it’s hard to describe our current situation as either “steady” or “sustained.” We’ll have to wait on that.

Perhaps more importantly, Friedman was a big believer in the Quantity Theory of Money. He even put it on the license plate of his Cadillac.

Doesn’t the Quantity Theory tell us that increases in M must, by definition, lead to increases in P? No! Because another component, velocity, could fall to offset the increase in M. And what has happened to velocity since before the pandemic? It has fallen by 22%.

(EDIT 2: Will Luther points out that I have conflated the equation of exchange with the Quantity Theory, which is an application of the equation. Duly noted! Clearly I haven’t taught macro in about 7 years.)

Bottom line: inflation isn’t here yet, but it could be coming, however the fall in velocity could offset most of the increase in the money supply.

Very interesting data on how if you strip out vehicles, this month’s inflation is no big deal. Nice.

As far as why car prices are increasing – – it is a supply issue as much as, or more than, a demand issue.

On this very blog back in March there was a (harrumph) prescient article warning, “Chip Shortages Shutting Down Auto Assembly Lines; Buy Your Car Now Or Else” ….”The bottom line: if you are planning to get a car (new or used), I suggest you act now, or else wait a year. Between the shortages and the stimulus money, prices are likely to keep rising for the next six months or so…”

And this won’t resolve itself any time soon. There is a huge lead time to expanding chip making capacity. This has exposed the fragility of our just in time, global supply chains. From today in Forbes:

https://www.forbes.com/sites/neilwinton/2021/07/14/chip-shortage-will-continue-to-stymie-muscular-auto-recovery-while-supply-gap-inspires-new-ideas/

LikeLiked by 1 person

I am not so sanguine about the inflation outlook. You dismiss the inflationary impact of recent money growth by noting that the velocity of money has fallen precipitously. But velocity is calculated as a residual, using data from the other three terms in the equation of exchange. The Quantity Theory of Money depends on two key assumptions: real economic growth is independent of monetary policy and the velocity of money is a stable function of the payments technology (at least in the long run).

So if the link between money growth and inflation is characterized by “long and variable lags,” as described by Milton Friedman, then large swings in measured velocity are an indicator of short-run disequilibrium in the money-price relationship.

There might be some plausible explanation for a decline in velocity from a technological or institutional perspective, but lacking some specific explanation why velocity is falling, a statement of “money is growing but it’s OK because velocity is falling” is nothing more than a tautology.

LikeLike