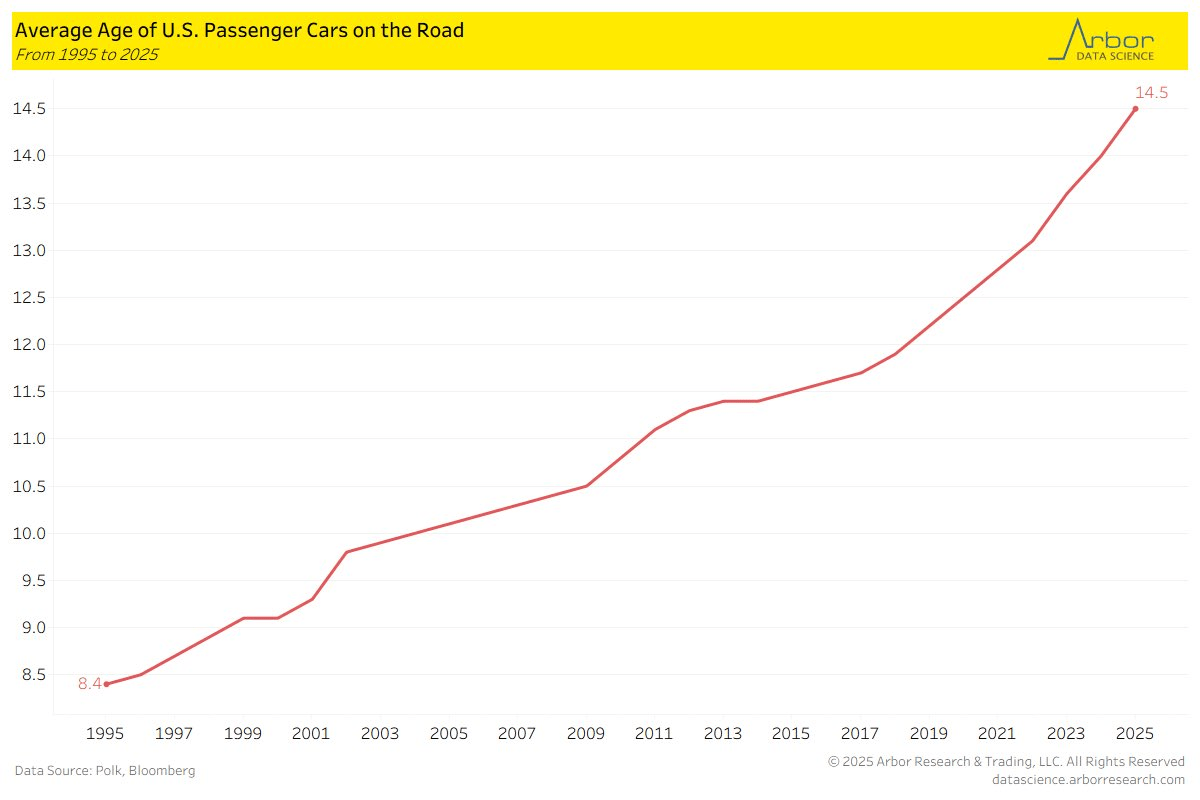

The following chart from Arbor Research shows that the average age of cars on the road in the US is 14.5 years. If we go back to 1995, it was almost half that, and the increase has been steady since over the past 30 years. Similar data from the Bureau of Transportation Statistics confirms these numbers.

Why would this be? I see two primary explanations that are possible. One is that cars are becoming more reliable (better quality), so consumers are happy to drive them longer. The other is that cars today are less affordable, so people are only hanging onto old cars because they are forced to. One of these is a happy explanation, one is consistent with a narrative of stagnation. Which is true?

On the affordability question, we do have some good data, but it points in the opposite direction: cars are much more affordable today than in 1995, or even before that.

Here is a personal economical anecdote from this week. A medium-sized dead branch fell from a tall tree and ripped off the driver side mirror on my old Honda. My local repair shop said it would cost around $600 to replace it. That is a significant percentage of what the old clunker is worth. Ouch.

They kindly noted that most of that cost would was ordering a replacement mirror assembly from Honda, which would cost over $400 and take several days to arrive. I asked if I could try to get a mirror from a junkyard, to save money. The repair guy said they would be willing to install a part I brought in, but suggested eBay or Amazon instead.

Back 20 years ago, before online commerce was so established, my local repair shop would routinely save us money by getting used parts from some sort of junkyard network. So, I started looking into that route. First, junkyards are not junkyards anymore, they are “salvage yards.” Second, it turns out that to remove a side mirror from a Honda is not a simple matter. You have to remove the inside whole plastic door panel to get at the mirror mounting screws, and removing that panel has some complications. Also, I could not find a clear online resource for locating parts at regional salvage yards. It looks like you have to drive to a salvage yard, and perhaps have them search some sort of database to find a comparable vehicle somewhere that might have the part you want.

All this seemed like a lot of hassle, so I went to eBay, and found a promising looking new replacement part there for about $56, including shipping. It would take about a week to get here (probably being direct shipped from China). On Amazon, I found essentially the same part for about $63, that would get here the next day. For the small difference and price, I went the Amazon route, partly for the no hassle returns if the part turned out to be defective and partly because I get 5% back on my Amazon credit card there. I just got the car back from the repair shop with the replacement mirror, and it works fine. The total cost, with labor was about $230, which is much better than the original $600+ estimate.

I’m not sure how broadly to generalize this experience. Some further observations:

( 1 ) For a really critical car part, I’d have to consider carefully if the Chinese knock-off would perform appreciably worse than some name-brand part – -although, I believe many repair shops often use parts that are not strictly original parts.

( 2 ) Commonly replaced parts like oil and air filters are typically cheaper to buy on-line than from your local Auto Zone or other local merchant. I like supporting local shops, so sometimes I eat the few extra $$ and shopping time, and buy from bricks and mortar.

( 3 ) Some repair shops make significant money on their markup on parts, and so they might not be happy about you bringing in your own parts. They also might decline to warrant the operation of that part. And many big box franchise repair shops may simply refuse to install customer-supplied parts.

( 4 ) For a newish car, still under warranty, the manufacturer warranty might be affected by using non-original parts.

( 5 ) Back to junk/salvage yards: there are some car parts, so-called hard parts, that are expected to last the life of the car. Things like the mounting brackets for engine parts. Typically, no spares of these are manufactured. So, if one of those parts gets dinged up in an accident, your only option may be used parts taken from a junker.

The title question may seem obvious. “We” care about inflation because, ultimately, any dollars we have saved will purchase fewer real goods and services. Additionally, we might worry that our incomes are not keeping pace with the increase in the prices of good and services that we want to purchase.

But the answer to that question is a little more nuanced. “We” also care about why prices are increasing. I keep putting “we” in quotation marks because who the we is crucial for answering the question. For example, individuals and families primarily care about inflation for the reasons I stated in the first paragraph.

But central bankers care about inflation for different reasons. In broad terms, monetary policy is an attempt to smooth out the fluctuations in the economy, especially to make recessions shorter and less deep. But monetary officials want to know: is the policy they are putting in place leading to prices rising in general? If so, especially if inflation gets above certain target levels, it may mean that monetary has been “too loose.”

However, if particular prices are rising, say the price of cars (due to a lack of computer chips), central bankers don’t really care about this: it gives them no indication of whether they’ve done “too much” or “too little” with regards to stimulating the economy. Similarly, if gasoline prices rise, consumers really care about this. Central bankers, not so much: it doesn’t really tell them much about their goal (stimulating the economy with stimulating it too much).

And because some prices are so volatile, historical context is important for understanding what a recent increase or decrease means. For example, gasoline prices are up 45% in the past 12 months. That’s a lot! But it’s an increase from a very low base, and the historical reality is that gasoline prices today (around $3.00/gallon on average) are at similar levels to what they were way back in 2006, and are lower than they were for almost all of 2011-2014. And these are all in nominal terms, median household income has gone up a lot since 2006 (up 40% in nominal terms) and even since 2014 (up 25%).

All of this is important background for thinking about the latest release of the CPI-U data this week. The headline inflation number of 5.3% is indeed startling, similar to last month. We haven’t touched that level since mid-2008, and that was only for a few months. If consumer price inflation were to stay at around 5% for a sustained period of time, it would be a new, harsh reality for most consumers today: we haven’t had a year with 5% inflation since 1990, and for the past decade the average has hung around 2%.

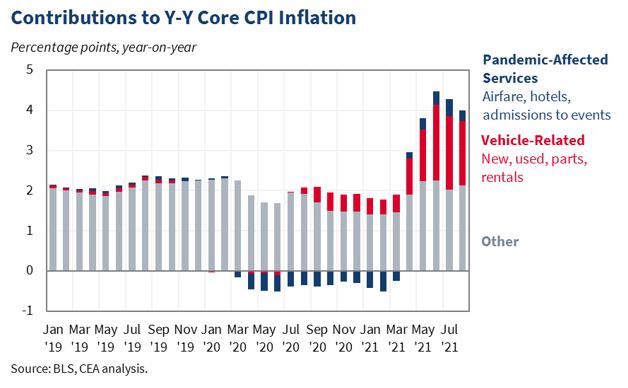

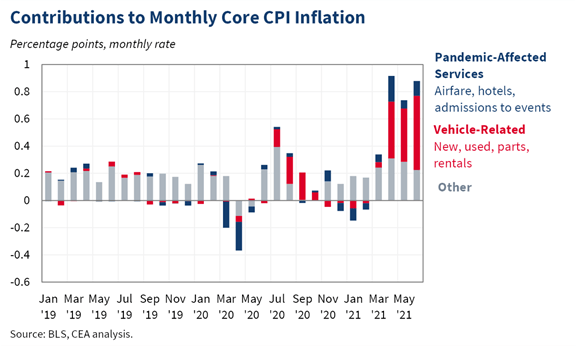

So will it stay this high? Sadly, I have no crystal ball and I will just reiterate what I said last month: the picture is just too muddled right now to say anything concrete. Perhaps by the end of the year we will have a better picture. But is there anything we can say right now even with the muddled picture? I continue to like this chart from the Council of Economic Advisors:

Bottom line: if we strip out the unusual supply chain disruptions to automobiles as well as airline/hotel prices making up for lost ground during the pandemic, inflation is at completely normal levels. It’s almost exactly 2%

But is this cheating? Can we really strip out the things that are increasing at rapid rates?

You have probably seen the latest inflation data. The headline number is 5.4% increase in prices in the past year as measured by the CPI-U. That’s a lot! Even the Core CPI (removing volatile food and energy) is up 4.5%.

If you follow the data closely, you may also have heard that a big chunk of that increase comes from prices related to automobiles: new cars, used cars, rental cars, car parts. All way up!

If you are in the market to buy a car, or if you really need a rental, it’s a bad time for prices. (Conversely, if you have an extra car sitting around, it’s a great time to sell!)

But what if you aren’t in the market for a car? What does the inflation data look like? The White House CEA tweeted out this chart to deconstruct the factors in the recent CPI release.

Global supply chains and just in time inventory work great – – until they don’t. Every car these days is a rolling computer, with semiconductors in every vehicle. No chips, no cars. For various reasons, there is a big worldwide shortfall in the chips needed for cars and trucks, which is causing auto assembly lines to shut down for extended periods. Car prices are already rising in response.

Chip production as a whole was slowed down this past year because of Covid effects at the factories. More importantly, chip production was switched away from automobiles to lighter consumer products. Auto assembly lines were curtailed due to the virus, resulting in reduced demand for those specific chips in 2020. The thinking among chip makers was that in the midst of a deadly pandemic, consumers would be sitting home ordering goodies from Amazon or Alibaba, rather than cruising car dealers or spending on travel. Indeed, U. S. spending on durable goods exploded in 2020, fueled in part by generous unemployment and stimulus payments, and this has soaked up existing chip production.

However, car buying has come back earlier than expected. Chip manufacturing is a lengthy process, taking some 26 weeks from start to finish. Chip makers are scrambling to add new capacity and to reconfigure their manufacturing lines for autos, but this shortage will not resolve until later in the year.