If you’ve ever been vegetarian or if you have ever spoken to a vegetarian about their diet, then you have probably heard or asked “How do you get enough protein?”. While it’s important for health and economic achievement to get adequate protein, not too long after comes the questions about types and sources of protein. This question is relevant for vegetarians and vegans, but also people with meat allergies and people with religious dietary guidelines that prohibit meat always or seasonally. Let’s break it down.

Some omnivores are incredulous that vegetarianism can provide adequate protein or protein quality. But protein itself is relatively easy to get and any judgmental attitudes on both sides are mostly just vibes. Legumes and nuts tend to have a lot of protein. But relative to what?

The World Health Organization recommends that an 80-kilogram (176 lb) adult should get 66.4 grams of protein per day (0.83g per kg). That’s the protein content of about a 9oz of peanuts. Protein is super important and it’s luckily not that hard to get if you eat a variety of foods. Even if you’re trying to consume double the WHO recommended daily intake (RDI), it’s an easy feat.

Below is a table of some popular protein sources. The table includes the grams of protein per 100 grams of food, which makes the protein content a percent. The table also includes the number of grams needed in order to achieve the WHO protein RDI of 66.4 grams. The last column is for our American readers who need the serving to be in ounces.

Have you heard the hubbub about eggs? People say that they’re expensive. My wife told me that if she’s going to pay an arm and a leg, then she may as well get the organic, pasture raised eggs. Absolutely. That’s what the substitution effect predicts. As the price ratio of low-quality to high-quality eggs rises, we’re incentivized to consume more of the high-quality version. It has to do with opportunity costs.

Consider a world in which the low-quality eggs cost $2 and the high-quality eggs cost $6 per dozen. Every high-quality egg costs 3 low-quality eggs. You might still choose the high-quality option, but you know that you’re giving up a lot by doing so. Consider the current world where low-quality eggs are priced on par with high-quality eggs. Now, the opportunity cost of consuming the fancy, pasture-raised eggs has fallen. When consuming one high-quality egg costs you one low-quality egg, it’s much easier to opt for the high-quality version. You’re not giving up as much when you purchase it.

For vegetarians, the recent price swing has probably been rough. Not eating meat, they’re facing the price squeeze more so than their omnivorous counterparts. Through the magic of math, median wages, and average retail prices, the figure below charts the affordability of eggs and dairy products.* The median person has been facing falling egg affordability for two decades. Indeed, it’s only been the past few years, punctuated by the Covid crisis, that consumers experienced more affordable eggs.

Dairy products, however, have become much more affordable. The median American can now afford 50% more of their namesake cheese. Further, we can afford 20-25% more whole milk and cheddar cheese. So, the vegetarians are not so poorly off after all.

The title question may seem obvious. “We” care about inflation because, ultimately, any dollars we have saved will purchase fewer real goods and services. Additionally, we might worry that our incomes are not keeping pace with the increase in the prices of good and services that we want to purchase.

But the answer to that question is a little more nuanced. “We” also care about why prices are increasing. I keep putting “we” in quotation marks because who the we is crucial for answering the question. For example, individuals and families primarily care about inflation for the reasons I stated in the first paragraph.

But central bankers care about inflation for different reasons. In broad terms, monetary policy is an attempt to smooth out the fluctuations in the economy, especially to make recessions shorter and less deep. But monetary officials want to know: is the policy they are putting in place leading to prices rising in general? If so, especially if inflation gets above certain target levels, it may mean that monetary has been “too loose.”

However, if particular prices are rising, say the price of cars (due to a lack of computer chips), central bankers don’t really care about this: it gives them no indication of whether they’ve done “too much” or “too little” with regards to stimulating the economy. Similarly, if gasoline prices rise, consumers really care about this. Central bankers, not so much: it doesn’t really tell them much about their goal (stimulating the economy with stimulating it too much).

And because some prices are so volatile, historical context is important for understanding what a recent increase or decrease means. For example, gasoline prices are up 45% in the past 12 months. That’s a lot! But it’s an increase from a very low base, and the historical reality is that gasoline prices today (around $3.00/gallon on average) are at similar levels to what they were way back in 2006, and are lower than they were for almost all of 2011-2014. And these are all in nominal terms, median household income has gone up a lot since 2006 (up 40% in nominal terms) and even since 2014 (up 25%).

All of this is important background for thinking about the latest release of the CPI-U data this week. The headline inflation number of 5.3% is indeed startling, similar to last month. We haven’t touched that level since mid-2008, and that was only for a few months. If consumer price inflation were to stay at around 5% for a sustained period of time, it would be a new, harsh reality for most consumers today: we haven’t had a year with 5% inflation since 1990, and for the past decade the average has hung around 2%.

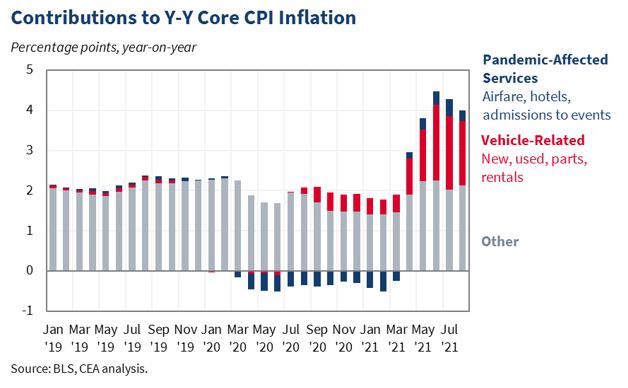

So will it stay this high? Sadly, I have no crystal ball and I will just reiterate what I said last month: the picture is just too muddled right now to say anything concrete. Perhaps by the end of the year we will have a better picture. But is there anything we can say right now even with the muddled picture? I continue to like this chart from the Council of Economic Advisors:

Bottom line: if we strip out the unusual supply chain disruptions to automobiles as well as airline/hotel prices making up for lost ground during the pandemic, inflation is at completely normal levels. It’s almost exactly 2%

But is this cheating? Can we really strip out the things that are increasing at rapid rates?