The title question may seem obvious. “We” care about inflation because, ultimately, any dollars we have saved will purchase fewer real goods and services. Additionally, we might worry that our incomes are not keeping pace with the increase in the prices of good and services that we want to purchase.

But the answer to that question is a little more nuanced. “We” also care about why prices are increasing. I keep putting “we” in quotation marks because who the we is crucial for answering the question. For example, individuals and families primarily care about inflation for the reasons I stated in the first paragraph.

But central bankers care about inflation for different reasons. In broad terms, monetary policy is an attempt to smooth out the fluctuations in the economy, especially to make recessions shorter and less deep. But monetary officials want to know: is the policy they are putting in place leading to prices rising in general? If so, especially if inflation gets above certain target levels, it may mean that monetary has been “too loose.”

However, if particular prices are rising, say the price of cars (due to a lack of computer chips), central bankers don’t really care about this: it gives them no indication of whether they’ve done “too much” or “too little” with regards to stimulating the economy. Similarly, if gasoline prices rise, consumers really care about this. Central bankers, not so much: it doesn’t really tell them much about their goal (stimulating the economy with stimulating it too much).

And because some prices are so volatile, historical context is important for understanding what a recent increase or decrease means. For example, gasoline prices are up 45% in the past 12 months. That’s a lot! But it’s an increase from a very low base, and the historical reality is that gasoline prices today (around $3.00/gallon on average) are at similar levels to what they were way back in 2006, and are lower than they were for almost all of 2011-2014. And these are all in nominal terms, median household income has gone up a lot since 2006 (up 40% in nominal terms) and even since 2014 (up 25%).

All of this is important background for thinking about the latest release of the CPI-U data this week. The headline inflation number of 5.3% is indeed startling, similar to last month. We haven’t touched that level since mid-2008, and that was only for a few months. If consumer price inflation were to stay at around 5% for a sustained period of time, it would be a new, harsh reality for most consumers today: we haven’t had a year with 5% inflation since 1990, and for the past decade the average has hung around 2%.

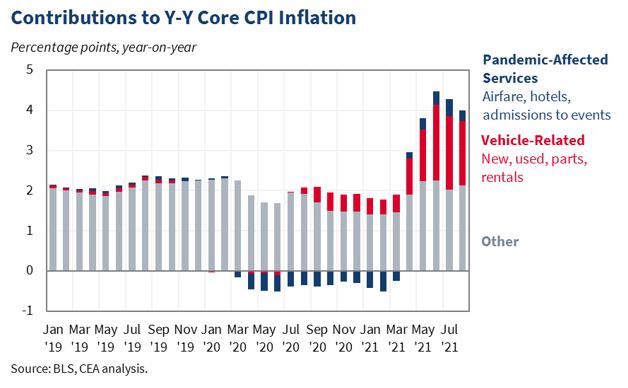

So will it stay this high? Sadly, I have no crystal ball and I will just reiterate what I said last month: the picture is just too muddled right now to say anything concrete. Perhaps by the end of the year we will have a better picture. But is there anything we can say right now even with the muddled picture? I continue to like this chart from the Council of Economic Advisors:

Bottom line: if we strip out the unusual supply chain disruptions to automobiles as well as airline/hotel prices making up for lost ground during the pandemic, inflation is at completely normal levels. It’s almost exactly 2%

But is this cheating? Can we really strip out the things that are increasing at rapid rates?

To answer this, we need to go back to what I said at the beginning of this post: who is the “we”? If the “we” is consumers that have recently purchased a car or plan to purchase one soon, then 5.3% is probably a relevant number to them. But when one item like cars, which comprises about 7% of the overall CPI, is pulling almost half of the overall increase, we need to provide that context.

Historical context is also important on particular prices. Take airline fares. Compared with August 2020, airline fares are up sharply: 6.7%. But keep in mind that airline fares are were significantly down for most of 2020. We are starting from a lower base. Airline fares are still well below the pre-pandemic levels (down 18% since February 2020). And when we examine the full historical series, we see that airline prices are right about where they were in 1999. In nominal terms!! Median household income is up 66% in nominal terms since 1999. Should we be concerned that airline prices are higher than a year ago? Perhaps in some sense. But: A) this has almost nothing to do with monetary policy; and B) compared to median household income, airline fares are the lowest they have ever been.

Here’s one more example of stripping out a few prices. The National Economic Council put out a report that about half of recent grocery price increases are due to just three items: beef, pork, and poultry. Conservatives mocked the idea of taking out these foods, presumably because lots of people like to eat meat! Which is true. But the NEC is trying to make a point that these increases are not due to general monetary inflation, but instead due to some other factor, in this case concentration in the meat-processing industry. I won’t comment on whether that is necessarily the cause, or whether it’s another pandemic anomaly, but the underlying point is similar to the other examples I have discussed. These price increases might have a specific explanation that is unrelated to monetary or fiscal policy. When just 15% of the grocery prices are driving 50% of the increases, you

Of course, just because we have a good explanation for particular price increases, doesn’t mean they don’t impact consumers. They do! And meat price increases certainly do impact most consumers, since only about 5% of Americans are vegetarians. And unlike used cars prices, most of us do buy meat every week. So we should not dismiss this price increase, but once again it’s important to contextualize it.

And it’s important to contextualize price increases because if we think there is some public policy way to address them, we need to know the cause. For example, if you think that price increases “can be traced back to government policies like the Federal Reserve’s printing of trillions of new dollars to fund COVID ‘stimulus’ efforts,” then the solution is obvious: the government must stop spending so much and printing money to fund that spending! But if most of the inflation is due to a chip shortage for new cars (which then impacts the used car market too), the public policy response is less clear. Airline fares returning to pre-pandemic levels? Again, there is not much that policy can or should do here (and it’s completely expected). Concentration in meat packing? The policy solution here could be anti-trust action, but that’s conditional on the NEC’s explanation being correct (given pandemic price uncertainties, I would wait to hold off judgment on meat prices for now).

Attempting to understand why particular prices are increasing is not an attempt to “explain away” or downplay price increases. Rather, it’s an attempt to better understand how public policy should (or shouldn’t) react to these prices increases.

Why bother having a CPI basket if economists are just going to post hoc rationalize the results?

Inflation exceeded the expectations of allegedly important economists. And many credible market participants. Either those expectations matter as a falsifiable assertion around policy implications or they don’t.

If you want to church it up with Nuance (TM) and Context (TM), fine, but at the end of the day inflation exceeds the expectations of a market filled with plenty of information.

LikeLike

Very well explained! Thank you.

LikeLike