The author of The Psychology of Money, Morgan Housel, has a new book “The Art of Spending Money” out this month. Its main point is that people tend to be happier spending money on things they value for their own sake- rather than things they buy to impress others, or piling up money as a yardstick to measure themselves against others (this is repeated with many variations).

Overall it is well-written at the level of sentences and paragraphs with well-chosen stories and quotes, but I’m not sure what it all adds up to. The main points seem obvious to me, though maybe that’s my fault for reading a book titled this when I’m already fairly happy with how I spend money. I think I err a bit on the frugal side, but I just don’t see many opportunities to turn money into happiness by spending it- I was maybe hoping for ideas on that front but I got none from the book. After reading it I don’t plan to do anything differently and don’t find myself thinking about spending differently.

Still, some highlights. The book is full of well-chosen quotes from others:

To say Warren Buffett is not a fan of gold would be an understatement. His basic beef is that gold does not produce much of practical value. His instincts have always been to buy businesses that generate steady and growing cash by producing goods or services that people need or want – – businesses like railroads, beverage makers, and insurance companies.

Here are some quotes on the subject from the Oracle of Omaha, where I have bolded some phrases:

“Gold … has two significant shortcomings, being neither of much use nor procreative. True, gold has some industrial and decorative utility, but the demand for these purposes is both limited and incapable of soaking up new production. Meanwhile, if you own one ounce of gold for an eternity, you will still own one ounce at its end” — Buffett, letter to shareholders, 2011

“With an asset like gold, for example, you know, basically gold is a way of going long on fear, and it’s been a pretty good way of going long on fear from time to time. But you really have to hope people become more afraid in the year or two years than they are now. And if they become more afraid you make money, if they become less afraid you lose money. But the gold itself doesn’t produce anything” — Buffett, CNBC’s Squawk Box, 2011

This from when the world’s 67-cubic foot total gold hoard was worth about $7 trillion, which by his reckoning was the value of all U.S. farmland plus seven times the value of petroleum giant ExxonMobil plus an extra $1 trillion:

“And if you offered me the choice of looking at some 67-foot cube of gold … and the alternative to that was to have all the farmland of the country, everything, cotton, corn, soybeans, seven ExxonMobils. Just think of that. Add $1 trillion of walking around money. I, you know, maybe call me crazy but I’ll take the farmland and the ExxonMobils” – – Cited in https://www.nasdaq.com/articles/3-things-warren-buffett-has-said-about-gold

And my favorite:

“Gold gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head“. – – From speech at Harvard, see https://quoteinvestigator.com/2013/05/25/bury-gold/

One thing Buffett did NOT say is that gold is “barbarous relic”. That line is owned by John Maynard Keynes from a hundred years ago, referring to the notion of tying national money issuance to the number of bars of gold held in the national vaults:

“In truth, the gold standard is already a barbarous relic. All of us, from the Governor of the Bank of England downwards, are now primarily interested in preserving the stability of business, prices, and employment, and are not likely, when the choice is forced on us, deliberately to sacrifice these to outworn dogma, which had its value once” – Monetary Reform (1924)

Has Buffett’s Berkshire Hathaway Beaten Gold as an Investment?

Given all that trash talk from the legendary investor, let’s see how an investment in his flagship Berkshire Hathaway company (stock symbol BRK.B) compares to gold over various time periods. I will use the ETF GLD as a proxy for gold, and will include the S&P 500 index as a proxy for the general U.S. large cap stock market.

As always, these comparisons depend on your starting and ending points. In the 1990s and 2000s, BRK.B hugely outperformed the S&P 500, cementing Buffett’s reputation as one of the greatest investors of all time. (GLD data doesn’t go back that far). In the past twelve months, gold (up 41%) has soundly beaten SPY (up 14 %) and completely trounced BRK.A (up 9%), as of last week. A couple of one-off factors have gone into these results: Gold had an enormous surge in January-April as the world markets digested the implications of never-ending gigantic U.S. budget deficits, and the markets soured on BRK.A due to the announced upcoming retirement of Buffett himself.

Stepping back to look over the past ten years shows the old master still coming out on top. In this plot, gold is orange, S&P 500 is blue, and BRK.A is royal purple:

Over most of this time period (through 7/21/2025), BRK.A and SP500 were pretty close, and gold lagged significantly. Gold was notably left behind during the key stock surge of 2021. Even with the rise in gold and dip in BRK.A this year, Buffett’s company (up 232%) still beats gold (198%) over the past ten years. BRK.A pulled well ahead of SP500 during the 2022 correction, and never gave back that lead. In the April stock market panic this year, BRK.A actually went up as everything else dropped, as it was seen as a tariff-proof safe haven. SP500 was ahead of gold for nearly all this period, until the crash in stocks and the surge in gold in the first half of 2025 brought them to essentially a tie for the past decade.

Warren Buffett is referred to as “the legendary investor Warren Buffett” or “the sage of Omaha”. The success of his Berkshire Hathaway fund is remarkable. He is also a pretty nice guy, and every year writes (with help, I’m sure) a letter describing the activities of his fund, along with general observations on investing and the economy. His letter covering 2022 was published two weeks ago.

Buffett noted that he and his team invest in companies in two ways: by buying shares to become a partial “owner” along with thousands of other shareholders, and also by buying ownership of the whole company. They aim to hold American companies that have a good business model, and will keep growing profits for years or decades. They look for great businesses at great prices, but they would rather buy a great business at a good price, than to buy a (merely) good business at a great price.

He was refreshingly honest about his overall stock picking record:

In 58 years of Berkshire management, most of my capital-allocation decisions have been no better than so-so. In some cases, also, bad moves by me have been rescued by very large doses of luck. (Remember our escapes from near-disasters at USAir and Salomon? I certainly do.) Our satisfactory results have been the product of about a dozen truly good decisions – that would be about one every five years – and a sometimes-forgotten advantage that favors long-term investors such as Berkshire.

In 1994 they bought a then-huge stake ($ 1.3 billion) in Coca-Cola, and another $1.3 billion stake in American Express. As it turned out, these two companies had the staying power that Buffet had anticipated, and have grown enormously in value over the past three decades.

In addition to their wholesome stock-picking philosophy, the “secret sauce” of Berkshire Hathaway is having the available funds to make those great investments in those great companies. These funds came large from the “float” from their insurance businesses. In Buffett’s words:

In 1965, Berkshire was a one-trick pony, the owner of a venerable – but doomed – New England textile operation. With that business on a death march, Berkshire needed an immediate fresh start. Looking back, I was slow to recognize the severity of its problems. And then came a stroke of good luck: National Indemnity became available in 1967, and we shifted our resources toward insurance and other non-textile operations.

The insurance business is interesting, in that clients pay in money “now”, but it does not get paid out until “later”. The insurance company has the money to own and manage until there is some claim event (e.g., someone dies or gets their home flooded) perhaps many years later. The traditional, conservative way for insurance companies to manage this float money was to invest it in low-paying but ultra-safe investment grade bonds.

Buffett’s key secret to success was to realize that he could invest at least part of these float funds in stocks, which would (hopefully!) over time make much more money than bonds. That gave him the cash to make those great investments in Coke and Amex. And his fund continues to have billions in hand to make strategic investments. He has made a bundle bailing out good companies that fell into short term difficulties. In his words:

Berkshire’s unmatched financial strength allows its insurance subsidiaries to follow valuable and enduring investment strategies unavailable to virtually all competitors. Aided by Alleghany, our insurance float increased during 2022 from $147 billion to $164 billion. With disciplined underwriting, these funds have a decent chance of being cost-free over time. Since purchasing our first property-casualty insurer in 1967, Berkshire’s float has increased 8,000-fold through acquisitions, operations and innovations. Though not recognized in our financial statements, this float has been an extraordinary asset for Berkshire.

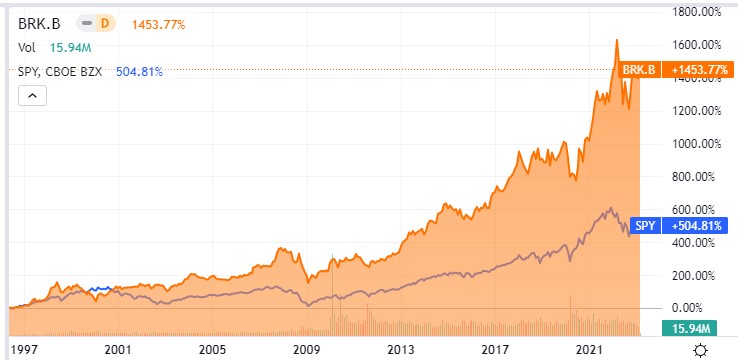

You, too, can participate in Buffett’s investing magic, by buying shares in Berkshire Hathaway. The stock symbol is BRK.B. (Disclosure: I own a few shares). Buffett has been skeptical of flashy tech stocks, and so BRK.B’s performance lagged the S&P 500 fund SPY in 2020-2021, but over the long term Berkshire (orange line in chart below) has crushed the S&P: