Some equations or relations in economics are inspired guesswork, which may or may not precisely describe the real world. There are other equations which always hold, since they are simple accounting identities. The Kalecki Profit Equation is of the latter type. It describes precisely the factors which determine corporate profits. Knowing this relation can give investors a leg up in predicting earnings.

This relation may be stated as:

Profits = Investment – Household Saving – Foreign Saving – Government Saving + Dividends

There are a lot of terms here, so we will break this down a bit to try to make sense of it. This relation should more properly be referred to as the Levy-Kalecki Profit Equation, since Jerome Levy was the first to develop this, in 1908. However, he was relatively unknown at the time, and Polish Marxist economist Michal Kalecki got most of the credit when he independently derived this equation decades later. We won’t show a derivation here. Wikipedia discusses Kaleki’s approach, while this essay from the Jerome Levy Forecasting Center gives a more detailed analysis of these factors.

By “Profits” here we mean profits after taxes (i.e. net profits). “Investment” here does NOT mean financial investment like buying stocks or bonds. It means purchasing some (typically real, physical) asset, like a building or new machine in a factory, which will have some enduring value and which will be useful in further production. More specifically, we mean net investment, after subtracting out depreciation on previously purchased assets. “Dividends” can include stock buybacks as well as plain cash payouts.

To develop a little intuition around this, let’s consider a simplified economy with no government or foreign sector, and where households spend all they earn (no household savings). Then we have:

Profits = Investment + Dividends

“Profits”, on the left hand side, is simply the income of the business sector as a whole. The right hand side show how business can deploy this income, either as investment or paying out dividends. Now, this equation (with the simplifying assumptions) must be precisely accurate. However, the causalities may not always be clear, and turn out to be somewhat counterintuitive. As analyzed by the Levy Forecasting Center, it turns out that businesses can’t directly control the left hand side, but they have at least some control over both factors on the right hand side (Investment and Dividends), so decisions by individual companies to invest can give increased profits for the overall business sector: “Investment sets in motion flows of funds that become— indeed, cause—profits”. Also, whatever money is paid out as dividends to the household sector (in our simplified system) comes right back to business as increased revenues, without any additional expenses (in conventional accounting).

If we now relax our simplifying assumptions so we are back to the full equation,

Profits = Investment – Household Saving – Foreign Saving – Government Saving + Dividends

it can be seen that if the nonbusiness parts of the economy (household, government , or foreign segments) do net savings, that cuts into business profits. For instance, if business pays households $1000 in wages, but households save $100 (and thus spend $900 instead of $1000 on further purchases from business), that directly cuts into business revenue and hence profits. Conversely, if households go $100 deeper into debt and spend $1100, that will boost corporate profits. Positive Government Savings (budget surpluses) decreases profits, whereas negative Government Savings (i.e. deficit spending) increases profits. “Foreign Savings”, which is roughly equivalent to the trade deficit, directly subtracts from domestic corporate profits.

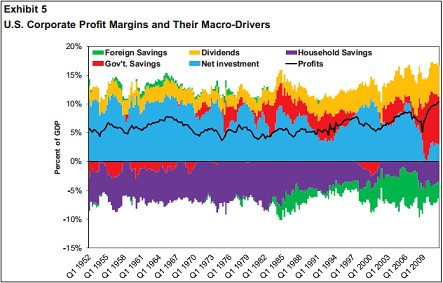

Here is a plot of how all this shook out between 1952 and 2011. The black line is total corporate profits, which is the sum of the various colored other factors, both positive and negative:

“Gov’t Savings” in this chart is actually deficit spending (negative “savings”). For most of this time period, corporate investment (blue) was the biggest positive factor, offset by household savings (purple). After 2000, “Foreign Savings” (green) took off, due mainly to the growing trade deficit with China. Household Savings dropped as folks took on debt to build new houses. During the 2008-2009 Global Financial Crisis (GFC), investment plunged, but Government deficit spending (red) exploded and drove corporate profits to new heights, despite the hit to GDP and household incomes. Since then, business investment has remained subdued, and profits have largely been propped up by ongoing government deficits which remained large by historical standards.

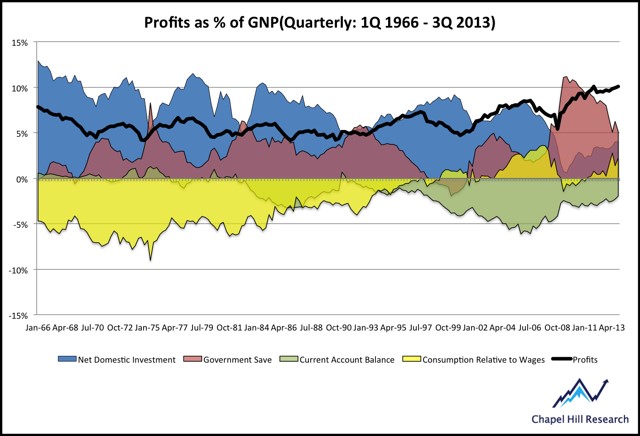

For comparison, here is a similar chart from a different source, and perhaps employing somewhat different definitions or data sources, running from 1966 to 2013. This is a little less clear, since some colors are overlaid instead of stacked. Here, “Current Account Balance” corresponds to Foreign Savings (roughly, the trade deficit) and “Consumption Relative to Wages” seems to correspond to the sum of dividends plus household increase in debt (negative household savings). Again, we see the great increase in government deficit spending in 2008-2009, which quickly boosted profits to new heights.

With the Covid shutdowns in 2020, investment dropped by about $ 600M from Q4 2019 to Q2 2020, and profits dropped by about $ 400M. The unprecedented blast of deficit spending for Covid relief (unemployment benefits, stimulus checks) quickly lifted corporate profits to full recovery by Q4. Some of those payments to households went into household savings and some went into increasing the trade deficit (people sitting home ordering made-in-China goodies on Amazon). But corporate profits hit an all-time high of $ 2.02 trillion in the fourth quarter of 2020.

Stock prices may be considered as: Earnings x Price/Earnings (P/E) . Here we explicated how deficit spending boosts corporate earnings. Last week, we posted on how the low interest rates and the asset purchases by the Fed have served to increase the P/E for stocks. All this goes a long way in explaining why stock prices have soared in 2020, despite a dismal overall economy, as measured by normal economic activity. Assuming a larger stimulus program is passed in the new administration, we expect (barring some geopolitical crisis) ongoing high stock prices in 2021 thanks in part to the effect of government deficits on profits.

Some notes:

( 1 ) The Levy-Kalecki profit equation is “true” by virtue of how all its quantities are defined. As noted, however, some of the causal relations are complex. Also, this equation is only valid for the business sector as a whole, not for an individual firm. Normally a given corporation only invests in assets that will genuinely help in production, so it cannot just invest like crazy and expect to boost its own profits to the moon. But increased investment by businesses as a whole will (all else being equal) make for increased profits for the business sector as a whole.

( 2 ) The equation deals with “flow” (over some defined time period) quantities, rather than underlying “stock” quantities. Of itself, the equation does not define the consequences of increased indebtedness, whether increased government debt to finance deficit spending, or increased debt to finance investments or dividends/stock buybacks. We wonder whether making corporate profits dependent on government deficit spending rather than on investing in productive assets is a one-way journey to mediocrity. It is argued that the only way to increase profits is to increase debt (expand balance sheets), somewhere in the global system, and that the explosion in both government and corporate debt in recent years has now made the system dependent on low interest rates from now on:

Where do profits come from then?

The answer is in net investment, which is a positive sum game. If we divide the economy into our four aggregate entities (1) US Corporations (2) Households (3) All levels of US Government and (4) the Rest of the World (RoW) and look at them as a whole, there needs to be net positive investment as a whole for there to be profits.

This means that an economy’s ability to produce profits comes down to the net expansion of the aggregate balance sheet in the macro accounting identity. For instance, if the US Government is running a budget surplus (shrinking its balance sheet), like it did in the late 90’s. Then either the Household, Corporate, or the RoW needs to take up the slack and expand their balance sheets to make up for the fall in demand. Or else demand will fall and profits will contract.

…Profits are essentially the result of expanding balance sheets (increases in debt). The more balance sheets expand the lower interest rates need to drop in order to decrease debt servicing costs and keep the cost of capital down for marginally profitable firms — essentially keep the economy from going into free fall.

{kind=link}

Hi, all this seems very reasonable but I just dont get the numbers to match. Investments c:a 17% (Residential & non Res) of GDP, and then 6% deficit more or less cancels out savings (3% ish) & trade deficit (also 3% ish), i.e ex dividends profits would be around 17% of GDP (if you ADD dividends they are 23% of GDP). But NIPA/GDP is approx 10% i.e about the same as SPX net margin. Is this due to time lags, are my numbers incorrect or have I misunderstood something? All the best & thx in advance, Johan

LikeLiked by 1 person

I am sorry, I don’t have the expertise in economic data to meaningfully help you here. There are probably subtleties in the definitions of the quantities, as well as the time lag factor you mention. If you want to drill down deeper into this, my best suggestion is to look at the Levy references above, they are probably the most detailed.

I come at finance as more of an investor than an economist, so I found this concept helpful especially in the dark days of mid 2020. With the economy shut down, it seemed on the surface that corporate profits would tank. But armed with the Kalecki concept, and knowing that the U.S. government was deficit spending trillions of dollars, I knew profits must roar back and so I was able to resist the market panic.

LikeLike

2 parenthetical things:

1) that NIPA profit figure of 10% is a non mean reverted record high nonetheless! (see the latest “odd lots” podcast w/ Montier, on BB/youtube).

2) NIPA profit ≠ GAAP profit of S&P.

The main reason, is probably that BANKS are completely missing in the Kalecki equation. Banks create money when businesses borrow.

LikeLiked by 1 person