Oil money has flooded into soccer/football,golf, and a host of sporting events. The prevailing term is “sportswashing” i.e. the attempt to reinvent the public image of the Saudi Royal Family, United Arab Emirates, Qatar, and anything petro-state adjacent. Partners in these endeavors can be found regularly providing sound bites praising parties whose records in human rights are less than sterling.

I just want to point out one thing: when your extended family’s net worth is $1.4 trillion (with a `T’, not a typo), your public image remains important, but nonetheless a potentially second order concern. What is a first-order concern is maintaining that wealth for the generations to come. When it comes to the oil-based wealth, the sun is setting. Not in terms of calendar months (not yet), but certainly in terms of generations. Oil, as the fulcrum of geopolitical history, is in it’s final period. Which is simply a long-winded way of saying that if a petro-state magnate cares profoundly about the global standing of their grandchildrens’ grandchildren, they’re looking for ways to move away from oil.

Oil is one of those special commodities that is of interest to economists because it enjoys high demand, has few substitutes, and it’s supply is relatively inelastic. You can’t merely will oil into existence. So if your family happened to enjoy high status and power over a previously low-value plot of land that an ocean of oil randomly happened to exist beneath, you could parlay that into tremendous wealth and power in the world. And they did.

With solar power setting the sun on oil (I am so sorry), you can’t blame oil magnates for looking for the next thing to tie their wealth to. What’s interesting is that the lesson they appear to have learned is the importance of hard-to-reproduce commodities. They fell into the first, now they are actively looking for the second.

You know what’s hard to reproduce? Status. Prestige. History. Identity networks. You know what characterizes those exact things? Sports teams and luxury brands. I fully expect oil money to keep pouring into soccer teams and handbags. Watches and sports cars. The kind of products that are grown and historically selected for across multiple generations, in processes that often take more than a century. Production processes that are less engineering than social geology.

Petro states and families have been tied to oil for 100 years, but now they want out. And we should let them, encourage them even. The fewer forces there are in the world working to continue fossil fuel dependence, the better. The more they tie themselves to products where labor holds more leverage than capital i.e. sports, the better. If you’re waiting for fossil fuel money, or human rights abusers, to get their come-uppance, prepare yourself for disappointment. But if you’re excited to the see a better world with cleaner air and a better climate future, then don’t be surprised if it’s first harbinger isn’t solar farms in Texas, but princes in stadium press boxes sponsored by Rolex.

In November 1738, clothier Henry Coulthurst informed weavers that he was cutting their piecework rates and would henceforth pay them in goods rather than cash. Needless to say, they were upset. Food prices were rising, and lower wages meant hunger and want.

Over three days in December, the weavers rioted. They smashed Coulthurst’s mill, wrecked his home, and “drank, carried out, and spilt, all the Beer, Wine and Brandy in the cellars.” They returned the following day to demolish Coulthurst’s house…

Wow. Our paper on cutting nominal wages is called “If Wages Fell During a Recession” We ran an experiment in which workers could retaliate if they experienced a nominal wage cut. They did! They couldn’t smash their employer’s house, but some of the slighted workers dropped their effort level down to the minimum level which meant that their employer made no more money in the experiment.

In my talk at IUE (show notes here and YouTube video), I connect the wage cut paper to another experiment on beliefs. One wonders, considering how serious the consequences turned out to be for Henry Coulthurst, why he was not able to anticipate the backlash against wage cuts. Being wrong was costly for him.

People are not always good at appreciating how strongly others have become attached to their own reference points. That’s why the paper on beliefs is called “My Reference Point, Not Yours“

Road signs on private land are often not legally enforceable by the police. You can ignore right-of-way and most signage in a parking lot or a parking-lot-adjacent path. I’m not saying that signs don’t serve a useful function. The stop in front of a Target or Publix is there to help coordinate drivers and pedestrians. It’s mostly a prudential matter. If it’s crowded, then those signs act coordinate us where norms might differ. But, if it’s late and no one is around, then you can safely run all of the parking lot stop signs with impunity. Be careful, however. The police can’t get you. But if you harm someone or something, then you can still be liable for neglect in a civil suit. That’s because neglect is contextual and expectations matter. If people treat parking lot signs like there are real road signs, then flaunting them can be construed as neglect.

You Can Park in Handicap Spaces.

If you’re *really* anti-social, then you should look up your local or state handicap accessible parking rules. Usually, police do have the power to ticket vehicles lacking the proper disability tags. BUT, the handicap parking space must conform to specifications. Where I live, for example, there must be an minimum sized sign that stands completely above 5 feet high in order to clearly demark the space. Therefore, if you see a handicap spot that is only noted by asphalt paint, then you’re free to park there.

Return your Shopping Cart… Or Don’t

Nothing says that you must return your shopping cart to an outdoor, covered, or indoor corral. People say that they have strong feelings about this (it’s not clear to me that they actually do). I say it’s not a fruitful exhortation. Let’s consider multiple perspectives and set aside the issue of civil liability due to neglect that I outlined above.

Getting long-run historical PE ratios of US stocks by industry seems like the kind of thing that should be easy, but is not. At least, I searched for an hour on Google, ChatGPT, and Bing AI to no avail.

I eventually got monthly median PEs for the Fama French 49 industries back to 1970 from a proprietary database. I share two key stats here: the average of median monthly industry PE 1970-2022, and the most recent data point from late 2022.

Industry

Long Run Mean

End 2022

AERO

12.14

19.49

AGRIC

10.75

9.64

AUTOS

9.65

17.52

BANKS

10.38

10.46

BEER

15.23

35.70

BLDMT

12.00

15.41

BOOKS

12.95

17.60

BOXES

12.18

10.69

BUSSV

12.07

13.03

CHEMS

12.40

19.26

CHIPS

10.48

17.47

CLTHS

11.45

10.94

CNSTR

8.98

4.58

COAL

8.04

2.92

DRUGS

1.14

8.01

ELCEQ

10.78

17.85

FABPR

10.28

19.40

FIN

11.16

12.97

FOOD

14.30

25.03

FUN

9.10

21.06

GOLD

3.18

-5.95

GUNS

11.50

5.05

HARDW

7.96

19.16

HLTH

11.91

6.09

HSHLD

12.60

20.15

INSUR

10.95

16.33

LABEQ

13.46

25.18

MACH

12.51

20.27

MEALS

13.83

19.19

MEDEQ

6.81

27.64

MINES

8.06

16.27

OIL

6.96

9.00

OTHER

12.20

27.68

PAPER

12.50

16.69

PERSV

12.86

-0.65

RLEST

8.13

-0.30

RTAIL

12.26

8.58

RUBBR

12.11

12.81

SHIPS

9.79

17.42

SMOKE

11.74

17.79

SODA

12.38

32.09

SOFTW

8.21

-2.85

STEEL

8.18

4.30

TELCM

6.75

9.58

TOYS

9.18

-1.32

TRANS

11.25

13.11

TXTLS

9.43

-49.00

UTIL

12.34

17.41

WHLSL

11.08

13.13

Mean Industry Median

10.52

12.73

One obvious idea for what to do with this is to invest in industries that are well below their historical price, and avoid industries that are above it (not investment advice). Looking just at current PEs is ok, but a stock with a PE of 8 isn’t necessarily a good value if its in an industry that typically has PEs of 6.

By this metric, what looks overvalued? Money-losing industries (negative current earnings): Gold, Personal Services, Real Estate, Software, Toys, and Textiles. Making money but valuations 19+ above historical average: Medical Equipment, Beer, Soda. Most undervalued relative to history: Guns, Health, Coal, Construction, Steel, Retail (all 3+ below the historical average).

Of course, I don’t recommend blindly investing in these “undervalued” industries- not just for legal reasons, but because sometimes the market prices them low for a reason- that earnings are expected to fall. The industry may be in secular decline due to new types of competition (coal, steel, retail). Or investors may expect it to get hit with a big cyclical decline in an upcoming recession or rotation from the Covid goods/manufacturing economy back to services (guns, construction, steel, retail). Health services (as opposed to drugs and medical equipment) stands out here as the sector where I don’t see what is driving it to trade at barely half of its usual PE.

I’d still like to get data on long run market-cap weighted mean PE by industry, as opposed to the medians I show here. The best public page I found is Aswath Damodaran’s data page, which has a wide variety of statistics back to about 1999. Some of the current PEs he calculates are quite different from those in my source, another reason to tread carefully here. I’m not sure how much of this is mean vs median and how much is driven by different classification of which stocks fit in which industry category.

This gets at a big question for anyone trying to actually trade on this- do you buy single stocks, or industry ETFs? Industry ETFs make sense in principle (since we’re talking about industry level PEs overall) and also add built-in diversification. But the PE for the ETF’s basket of stocks likely differs from that of the industry as a whole. It would make more sense to compare the ETF’s current PE to its own historical PE, but most industry ETFs have very short track records (nothing close to the 53 years I show here). PE is also far from the only valuation metric worth considering.

All this gets complex fast but I hope the historical PE ratio by industry makes for a helpful start.

Two recent essays push back against the concept of “disinformation” in thoughtful but, I believe, ultimately incorrect ways.

Martin Gurri is primarily concerned with government trying to stamp out what it views as disinformation. I am concerned about that too, but there are ways for private actors to correct bad information too.

Dan Klein (my friend and professor in grad school) argues that most labeling of “disinformation” or “misinformation” is not really about information, but instead about knowledge. I agree that sometimes this is true. But sometimes it is not true. Sometimes we really are talking about information. And sometimes the information is about extremely important topics.

As I search through my own Twitter history for these terms, I see that there is overwhelmingly one period of time and one piece of information that I used them for: the total number of deaths in the United States in 2020. If you can think way back to the fall and winter of 2020/early 2021, you might recall that we were just finishing up the first year of the pandemic, and we were also going through one of the worst periods in the pandemic. Vaccines were now starting to become widely available as we got into 2021, and people were starting to make person decisions about whether to “get the jab.”

The number of total deaths in 2020 was an important number. There was still a lot of uncertainty about exactly how bad the pandemic was, or (to a small but vocal minority) whether the pandemic was even “real.” The data was crucial to this debate. Of course, once we have the data, we must interpret it. This is one of Klein’s main points, and a good one. But if we aren’t starting from a common baseline of true information, there is really no point in discussions based on interpretations of those different apparent realities. We will, by definition, be “talking past each other.”

So what were people saying about total deaths in 2020 during this moment of importance in late 2020/early 2021?

I really don’t like the time and effort wasted in cleaning crudded-up frying pans, so I appreciate non-stick coatings. I have a small diameter Gotham ceramic pan that works well, and I was thinking of getting a larger one for cooking bigger loads. As usual, I went to the internet for wisdom on preferred ceramic pans to buy.

However, in the course of trying to get a fix on how they work, I fell down a rabbit hole. It turns out that this subject is complex and controversial. I will try to summarize my understanding in a brief post, with the caveat that I am not sure of everything here.

First of all, the “ceramic” coating is not really ceramic. Typical ceramics are made from firing powders of inorganic materials like silicon/aluminum oxides (including clays) at extremely high temperatures to where the particles fuse together. For the ceramic coatings on pans, this is not the case. I looked pretty hard on line without success to pin down the actual process or composition of the pan coating. It seems to involve some sort of silicone or silica polymer, applied using a sol-gel process. (Silica is just silicon and oxygen – quartz and white sand are pure silica – while silicone is typically a Si-O-Si-O-Si polymer with two extra hydrocarbon side groups attached to each Si).

100% silicone, in the form of rubbery sheets or cupcake papers for cooking on or in, is known to give a non-stick cooking surface. The “ceramic” coating in pans appears to be a solid equivalent of silicone cookware. A key factor mentioned in why it is slick and why it loses its slickness is that (supposedly) a thin layer of silica or silicone comes off with each cooking episode, and that thin layer is what gives the non-stick effect. (I would not mind ingesting a little adventitious silica, but eating random silicone worries me a little – but I don’t know if all this is actually true).

See this link for further discussion of the safety of ceramic versus teflon coatings. Be aware that makers of teflon coatings often choose names for their coatings that include the words “stone” or “granite”, perhaps to make the unwary consumer believe that these are ceramic coatings. My teflon pans have usually started to flake (into my food!) after a couple years’ use. A happy exception is a newer electric skillet which has temperature control so it never gets above about 425 F (high temperature destroys teflon). We do keep it oiled in use. Its teflon coating is still good as new after two years.

There seems to be general agreement that ceramic pans start off super slick, that fried eggs slide right out, but that after some months of use, food starts sticking noticeably. It helps to use a little oil every time you cook, and to avoid using metal utensils or abrasive cleaning pads, and to avoid very high temperatures or the use of cooking sprays (which deposit something harmful to the ceramic coating) or olive oil (which can burn on). Some users say it is important to clean the pan well between uses, e.g., using salt as a mild abrasive.

Why Do Ceramic Pans Lose Their Non-Stickiness?

There seem to be two main schools of thought as to the deterioration of performance. One school points to the (alleged) continual loss of silica particles or (presumably oily) silicone from the surface; perhaps once this surface layer is depleted, it’s game over. Another camp points to the buildup of burned-on deposits, even very thin, nearly invisible deposits, that then become a locus of food sticking.

What Can Be Done to Restore a Ceramic Pan Coating?

It is common to read that you just have to be prepared throw the pan away every 1-2 years. However, this does not seem economical. Can these pans be salvaged? One author claims that slickness can be restored by “seasoning” a ceramic pan, similar to how cast-iron pans are treated: after cleaning the pan, rub a very thin layer of a recommended oil (e.g. soybean oil, not olive oil) on the pan and then heat it to the smoke point. This should bond a polymerized oil layer to the surface. I have not tried this, but it might be worth a try.

A diametrically opposite approach is recommended by the maker of GreenPan ceramic pans. Here the theory is that if an offending film of cooked-on crud is removed, the native, clean ceramic layer beneath will once again be non-stick. A wet Magic Eraser type cleaning pad is recommended.

A similar remedy touted on the internet (e.g. here and here) is to rub with coarse salt (for long time, but not too hard) to get down to a pristine ceramic surface. Good results are claimed.

As a (retired) experimental scientist, I was itching to try something like this. At a family member’s house, I found an older ceramic pan that was not in really bad shape, but had lost its primal non-stick.

The BEFORE picture is above. There was a persistent brown film in parts of the pan, and cooked omelets (my test vehicle) did not simply slide out. I cleaned the pan with soap and water and a sponge, then went at it with a wetted Magic Eraser. I got the brown film off, though you could still see some pitting in the coating due to the use of metal utensils.

The AFTER picture is below. This is after cooking yet another omelet (with oil), and just wiping the pan with paper towel afterward. I can’t say that it was a night and day difference, but the Magic Eraser treatment definitely seemed to improve the performance. Score one for sustainability.

APPENDIX: Finally Understanding What Make Ceramic Pan Coatings Non-Stick

As noted in the original article above, I was puzzled over how the ceramic coatings worked. The descriptions in articles I could find on-line talked of forming these coatings from sol-gel solutions, using ingredients such as tetraethoxysilane. Without going into details, my chemical intuition led me to believe that, yes, you could form a dense silica pan coating from that, but the final outer surface would have Si-OH groups, like quartz or glass or ordinary “enamel” ceramic pan coatings. This would not give the oily, silicone-like surface that is evident with the nonstick ceramic pan coatings.

My “Aha” moment came when examining a patent application ( United States Patent Application No. 20180170815) for making a GreenPan ceramic pan coating. Among the ingredients for making the coating is methyltrimethoxysilane (MTMS). And THAT should give Si-CH3 groups on the outer surface, which is exactly the type of oil-like outer surface that silicone has. (The -CH3 methyl group is a fairly nonpolar, “oily” hydrocarbon type group).

A restless itch has now been scratched. I think I now understand why fresh ceramic pan coating can have such fine non-stick properties, and perhaps why they might be vulnerable to losing their non-stick properties. With Teflon type pan coatings, it is plasticky, oily Teflon all the way down, so if you abrade off a hundred molecular layers, it should make no difference. But with the ceramic coatings, it is not clear to me whether the oily Si-CH3 groups are only in the topmost atomic layer; maybe if that gets abraded off, there is only the quartz-like Si-OH groups to be found; or maybe there is a substantial (in atomic terms) topmost layer rich in Si-CH3 groups. Anyway, it makes sense to keep using oil when cooking on ceramic pans, to keep a hydrocarbon-type surface coating going there, and to avoid using metal utensils that can scrape and scratch the coating.

Let’s take the findings at face value, and say that all faculty at the various stages of tenured and tenure-track academic appointments work within a monopsonistic market. Let’s also accept that it is reducing not just wages, but total compensation inclusive of all benefits and compensating wage differentials. What’s the solution?

I mean, so much of the monopsony literature circles back to the policies and industrial institutions that researchers, wonks, and advocates think will improve worker welfare. Well, if *we*, the researchers in question are so confident in our findings, our models, and our policy recommendations, what have we done to improve our own market? Have we done anything? Can we do anything?

I heard someone in the back yell “We unionized!” Okay, that’s great. I just I could say “More unions” and end the post, but I’m not confident that this is a problem that unionization, absent additional innovation, is going to solve. Don’t worry, I have an idea.

Release sheets. I’ll explain.

At the moment, the majority of academics opearate under administrative regimes that think the best way to keep faculty costs down is leverage employee exit costs to the absolute hilt. That means, more than anything else, that the only way to get a non-trivial raise is to have a formal letter offering you a job at another university, with a start date, salary, and benefits all enumerated. Only then will the department/college/university consider offering you a “retention” raise. The administration’s hope is the the cost of pursuing an outside offer combined with the cost of moving to a new area (“local” outside options are almost non-existent in academia) will deter you from pursuing them, reducing the probability of receiving one.

The problem with this tactic is that it discourages faculty from contributing, participating, and investing in all of the public goods that make a department and university successful. Every investment ties the researcher to the school and community, raising their exit costs and, in turn, lowering their expected probability of pursuing and receiving an outside offer. Contributing to public goods reduces expected future wages. “Retention raises only” insititutions undermine the mission of their own faculty by incentivizing their faculty to be as independent, aloof, and myopically selfish as possible.

Now, the obvious solution here for universities is to simply preempt the market by raising salaries to better match their market value, but that would require both having a clear and unified vision of what their product and mission are (good luck) and not giving in to the overwhelming temptation to capture rents on labor wherever they can (fat chance). If there is one unifying attribute of bad managers everywhere, its conflating rent maximizing with profit maximizing. Yes, I know there is definitional overlap, but we’ve all known a manager that confuse percentage returns for absolutes, acting as if paying $3 for $5 of marginal labor product is better than paying $8 for $11.

If you want faculty to contribute to public goods, you’re going to have to give them something as compensation for their higher exit costs. I suggest exchanging reduced asymmetric information for enduring higher exit costs. How? The two-part release sheet.

The idea is actually pretty straight forward. Part one: every employee contract includes a release sheet that includes a retention ceiling that the university promises it will not make a retaining offer in excess of. If you have a retention ceiling at $200k a year, then another school can come and offer that with absolute confidence that they will have a real shot at landing the employee. This encourages rival schools to make the investment in scouting and recruitment. It lowers the cost of making offers that will raise someones income. More offers, more raises, less rents.

Part two: the merit raise ladder. Between the employee’s current salary and their retention ceiling is a schedule of merit raises. At each step of the ladder, the department evaluates the employee’s revealed productivity since their last evaluation and decides whether to give a raise. The tartgeted amount of the raise is pre-determined. If the employee receives an amount less than the pre-determined full target raise amount, the difference is subtracted from their retention ceiling. Let’s go through an example:

Contract A: $150k/ year. 6 year contract. $10k raises at years 2 and 4. Retention ceiling: $225k/year.

That means that after year 2, the department can give a raise. If they raise their salary by $7k a year (total 157k), then their retention ceiling is lowered (7-10 = -3) to $222k. After 6 years the two parties have the option to renegotiate the whole package. If both parties can’t agree, then they simply project the old schedule forward, $10k every two years, differences lowering the retention ceiling. If salaries are frozen it’s entirely possible for the retention ceiling to drop below their actual salary.

I see a lot of benefits here, and not just for faculty. Everyone benefits from reduced assymetric information. A high retention ceiling doesn’t actually bind anyone’s hands – a rival university can still show up with any offer they like, the current employer simply retains the right to make an equal or higher retaining offer. Failure to keep up with employee market value, however, will quickly result in the vultures circling your best employees. At the same time, employees have greater incentive to continue contributing in every possible way to the department, and not just those that are visible on the outside. Departments will know that they have to keep salaries commensurate with total productivity or they will forfeit their right to make competitive retention offers.

We already have a central hub in academic economics: the AEA-JOE. We post job openings and vitaes on the JOE, we coordinate letters of references. Posting our retention ceilings alongside our vitaes would be a nearly costless addition.

Would their be other consequences? Almost without question. This is a blog post not a theory paper. But if we’re going to complain about monopsonistic markets, we should probably consider taking steps to fix our own.

Abstract: We create a set of prompts from every Journal of Economic Literature (JEL) topic to test the ability of a GPT-3.5 large language model (LLM) to write about economic concepts. For general summaries, ChatGPT can perform well. However, more than 30% of the citations suggested by ChatGPT do not exist. Furthermore, we demonstrate that the ability of the LLM to deliver accurate information declines as the question becomes more specific. This paper provides evidence that, although GPT has become a useful input to research production, fact-checking the output remains important.

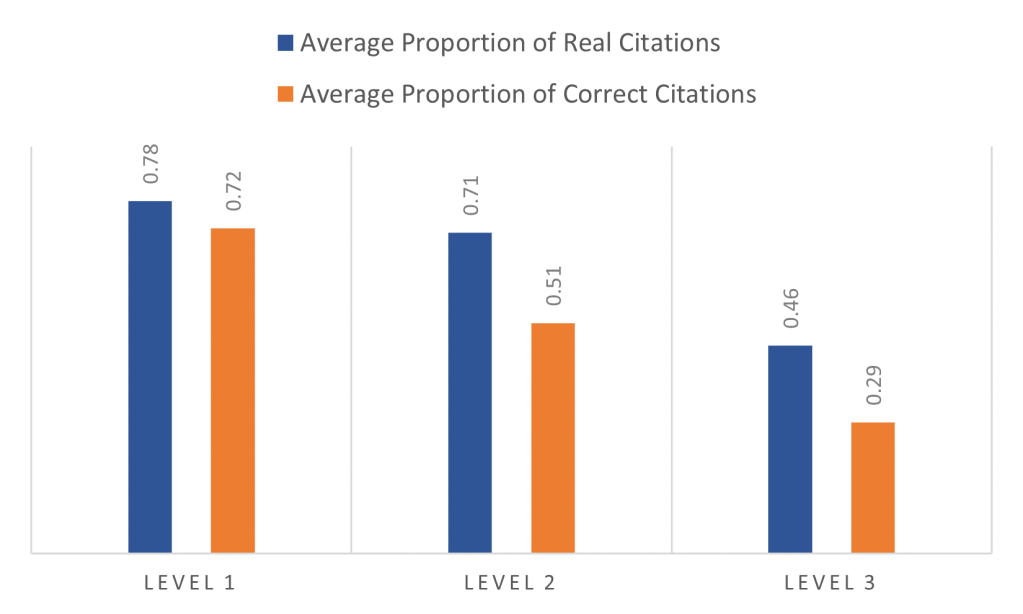

Figure 2 in the paper shows the trend that the proportion of real citations goes down as the prompt becomes more specific. This idea has been noticed by other people, but I don’t think it has been documented quantitatively before.

We asked ChatGPT to cover a wide range of topics within economics. For every JEL category, we constructed three prompts with increasing specificity.

Level 1: The first prompt, using A here as an example, was “Please provide a summary of work in JEL category A, in less than 10 sentences, and include citations from published papers.”

Level 2: The second prompt was about a topic within the JEL category that was well-known. An example for JEL category Q is, “In less than 10 sentences, summarize the work related to the Technological Change in developing countries in economics, and include citations from published papers.”

Level 3: We used the word “explain” instead of “summarize” in the prompt, asking about a more specific topic related to the JEL category. For L we asked, “In less than 10 sentences, explain the change in the car industry with the rising supply of electric vehicles and include citations from published papers as a list. include author, year in parentheses, and journal for the citations.”

The paper is only 5 pages long, but we include over 30 pages in the appendix of the GPT responses to our prompts. If you are an economist who has not yet played with ChatGPT, then you might find it useful to scan this appendix and get a sense of what GPT “knows” about varies fields of economics.

In the tapestry of human progress studies, two authors, Adam Smith and Virginia Postrel, have left their mark on the story of productivity and innovation. Their books, written centuries apart, both explore the power of specialization and the division of labor.

Part of the reason this came out this week is that I’m reading The Fabric of Civilization. So good! It had come highly recommended before, but I finally have an excuse to read it because I’m working on an article about fashion.

When I was a graduate student, I paid for my tuition by tutoring for the university athletics department. I tutored stat, math, micro, macro, excel, and finance. I tutored the same students each week, so I got to know them pretty well over the course of the semester. I also got to know their strengths and weaknesses. It was at this time that I realized most quantitative or even analytical ideas could be described in 4 potentially equivalent ways:

Mathematically

Using logic in English

Graphically

With a Table

In this post I want to share the Supply & Demand cheat-sheet that I use to help my students learn about the effects of supply and demand.