The following are notable posts from 2024, in descending order by the number of views this year.

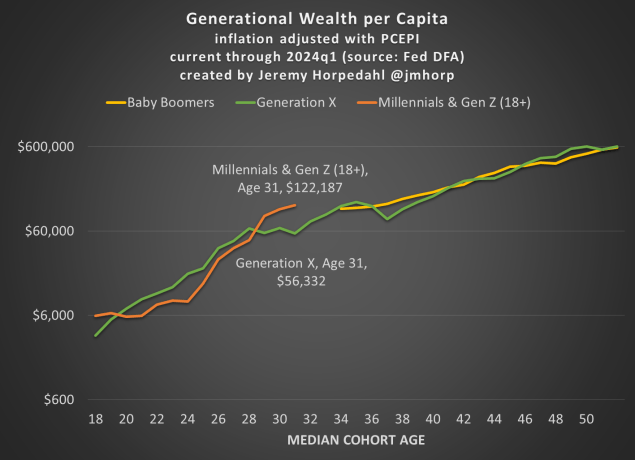

- Young People Have a Lot More Wealth Than We Thought Jeremy Horpedahl was first to this scene. American Millennials, on average, have money. Perhaps this is becoming common knowledge now among folks that read The Economist. The US is getting gradually richer, and the average young adult is benefiting. You can see more from Jeremy by following him on Twitter/X.

- Civil War as radical literalism Mike Makowsky writes, “There’s a million war movies, most of which have arcs and metaphors strewn throughout. The problem with making a moving about a hypothetical civil war in the modern United States is that the audience will spend so much time looking for the heroes, villains, and associated opportunities to feel morally superior that it seems almost impossible to deliver an effective portrayal of what it might actually feel like to wake up to a US civil war…”

- Is “Rich Dad Poor Dad” a Fraud? Scott explores whether a popular finance book is based on a false premise.

- Is the Universe Legible to Intelligence? I (Joy) do philosophy. It also has practical implications. Can machines outsmart us, for better or worse? How smart can anything physical be. Maybe, as @sama says, “intelligence is an emergent property of matter…” However, maybe “intelligence” only goes so far. We have many posts on artificial intelligence this year.

- How To Drive a Turbocharged Car, Such as a Honda CR-V This is one of those pieces by Scott that people find through search engines when they are looking for help.

- Grocery Price Nostalgia: 1980 Edition You can use our search function to find everything from this year about the topic of inflation.

- The US Housing Market Is Very Quickly Becoming Unaffordable

- Predicting College Closures James reflects on closing universities and what indicators might help stakeholders like parents and faculty anticipate the next event.

- Counting Jobs (Revisited) Jeremy did something that might have sounded boring at the time. Yet, soon afterwards there was serious interest in the question of : Did 818,000 jobs vanish?

- Why Avocado on Toast? As an avocado toast person, I loved this. I’m glad many other people found Zachary’s post interesting.

- Recovering My Frozen Assets at BlockFi, Part1. How Sam Bankman-Fried’s Fraud Cost Me.

- Why Don’t Full Daycares Raise Prices? The cost of childcare is an important issue. James wrote this from personal experience, and I pointed out something similar before.

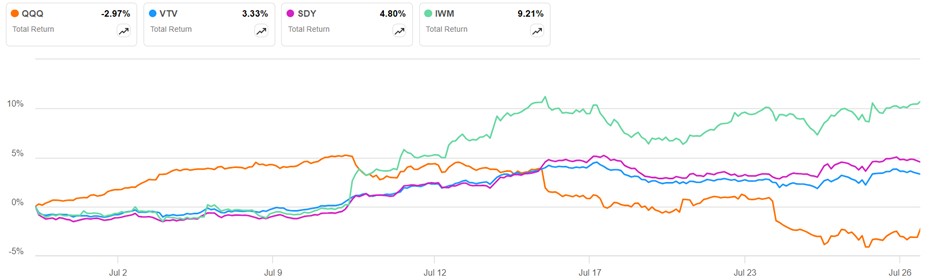

- This post only got medium traffic in terms of the number of views this summer. Now that we know who the candidate will be, it’s interesting to look back and see a vindication of betting markets. Who Will Be the Democratic Presidential Candidate? Follow the Money (Betting Markets)

- Honorable mention to Mike’s post from 2022 that continues to get many search hits: Why Agent-Based Modeling Never Happened in Economics

At this point, the EWED authors have each written enough words to constitute a book. Watching this blog grow and flux with the rest of the internet has been fascinating.

You can subscribe to our WordPress site to get posts sent to your email. The widget for putting your email in should be on the right side of your screen on a computer, or you can find it by scrolling to the bottom of the home page on a mobile device. WordPress will let you customize your preferences so that you get emails batched once a week if you prefer that to Every Day.