What, you think I’m going to pretend anyone is paying attention to anything but the trainwreck on Wall Street? As of 10:15AM this morning, the market is down 8% in 5 days, almost 20% off it’s peak, and is still falling. It’s entirely attributable to a unfathomably stupid trade war that has been forecast for months, if not years. This is the kind of probabalistic event that is usually internalized within the market in advance, which suggests that either very few people thought Trump a) was telling the truth, b) would be able to execute, or c) other forces within government would be able to stop him.

The legislative branch has largely ceded power to the executive, with only the judicial hanging on as some check against power. The open question, then, is at what level of damage will the legislative branch find incentive to reassert itself against an executive that (probably) doesn’t have the constraint of a future electoral victory to pursue? Will the destruction of great swaths of the US and global economy warrant reclaiming of power or impeachment of an executive?

Myself and a student coauthor worked hard on our article that is now published in Social Science History. It’s the first modern statistical analysis of the historical deaf population. We bring an economic lens and statistical treatment to a topic that previously included much anecdotal evidence and case study. We hope that future authors can improve on our work in ways that meet and surpass the quantitative methods that we employed.

Our contributions include:

A human capital model of deafness that’s agnostic about its productivity implications and treats deaf individuals as if they made decisions rationally.

A better understanding of school attendance rates and the ages at which they attended.

Deaf children were much more likely to be neither in school nor employed earlier in US history.

The negative impact of state ‘school for the deaf’ availability on subsequent economic outcomes among deaf adults. We speculate that they attended schools due to the social benefits of access to community.

Deaf workers did not avoid occupations where their deafness would be incidentally detectable by trade partners, implying that animus discrimination was not systemically important for economic outcomes.

I’m finally watching the Ken and Sarah Burns documentary on Da Vinci. It is, predictably, excellent. If you are heavily read on Da Vinci then there probably isn’t much that will be new to you, but the visual composition really adds something to what is less a propulsive story and more an attempt to capture the raw capaciousness of this person’s mind. It’s breathtaking, humbling, and inspiring.

There is a temptation to marvel at his dedication, ability to learn, and breadth. To relegate his accomplishments to the realm of outlier genius. Fight that temptation. Instead, take a moment to consider how dedicated he was to being unencumbered. To finding projects and patrons that would service to subsidize his pursuits in totality.

More than anything, observe a brilliant person for whom both the prospect and opportunity of boredom led him to follow his curiousity into whatever intellectual avenues it wanted to pursue, and then turning his imagination into product manifest in text and on canvas.

Boredom is an opportunity we increasingly don’t afford ourselves nearly enough of. We are starved for boredom. Allow for its sustenance.

“In a room sit three great men, a king, a priest, and a rich man. Between them stands a sellsword. Each of the great ones bids him slay the other two. Who lives and who dies?”

…“Power is a curious thing, my lord. Perchance you have considered the riddle I posed you that day in the inn?” “It has crossed my mind a time or two,” Tyrion admitted. “The king, the priest, the rich man—who lives and who dies? Who will the swordsman obey? It’s a riddle without an answer, or rather, too many answers. All depends on the man with the sword.” “And yet he is no one,” Varys said. “He has neither crown nor gold nor favor of the gods, only a piece of pointed steel.” “That piece of steel is the power of life and death.” “Just so… yet if it is the swordsmen who rule us in truth, why do we pretend our kings hold the power? Why should a strong man with a sword ever obey a child king like Joffrey, or a wine-sodden oaf like his father?” “Because these child kings and drunken oafs can call other strong men, with other swords.” “Then these other swordsmen have the true power. Or do they?” Varys smiled. “Some say knowledge is power. Some tell us that all power comes from the gods. Others say it derives from law. Yet that day on the steps of Baelor’s Sept, our godly High Septon and the lawful Queen Regent and your ever-so-knowledgeable servant were as powerless as any cobbler or cooper in the crowd. Who truly killed Eddard Stark, do you think? Joffrey, who gave the command? Ser Ilyn Payne, who swung the sword? Or… another?” Tyrion cocked his head sideways. “Did you mean to answer your damned riddle, or only to make my head ache worse?” Varys smiled. “Here, then. Power resides where men believe it resides. No more and no less.” “So power is a mummer’s trick?” “A shadow on the wall,” Varys murmured, “yet shadows can kill. And ofttimes a very small man can cast a very large shadow.” Tyrion smiled. “Lord Varys, I am growing strangely fond of you. I may kill you yet, but I think I’d feel sad about it.”

My first reaction is that, at the current state of technology, I feel like wishing for more IVF on women is cruel. If someone you love has gone through it, you wouldn’t wish it on more people. Supporting the careers of women who want to have children while they are young seems preferable and lower cost to society. The problem is that supporting mothers is a tricky collective action problem, so we seem stuck with this.

“The egg freezing process is also expensive, costing between $8,000 to $15,000 per cycle. Fortunately, more and more women are being covered by insurance plans that offer free egg freezing. According to a 2021 survey, 20 percent of American companies with over 20,000 employees and 11 percent of smaller companies offer such benefits – an increase from six and five percent respectively in 2015. But most women still have to pay out of pocket.” $15,000 is sort of a lot. It’s cheaper than a year of paid maternity leave for a PhD student, but the total cost of a “medical baby to an older couple” is pretty high.

Some of the technology Rux described was new to me and encouraging. If babies and birth becomes much more medicalized (and civilization doesn’t end), then I could imagine a world where most couples look like Simone and Malcolm Collins by choice with designer babies on demand after having a carefree childfree decade.

“The main advantage of IVM is that it allows immature eggs to be collected instead of mature ones, which significantly reduces the burden of hormonal stimulation.” Exciting! Think of how far we’ve come with cancer treatments or treating AIDS. If enough research goes into this, then potentially the cutting, injecting, pill popping hell that women have to go through for IVF could become smaller and more focused on exactly what is near certain to work.

Someone’s going to come along and grumble and say nature is better, but recall from earlier: “Supporting the careers of women who want to have children while they are young seems preferable and lower cost to society. The problem is that… “

On an optimistic note, I am witnessing a beautiful success story of embryo adoption among my relatives. It worked. A wonderful couple has twins now, and those twins are experiencing love and contact from both their birth family and genetic parents. That technology only became available in the late ’90s. Expect more stories like this.

We might even be close to AI childcare that works. Imagine a daycare where robots do 100% of the food and cleaning work so that the humans in the room can focus exclusively on emotional and relational work with the kids. That could make daycare better or cheaper or both.

The simple technology of food and grocery delivery has already helped parents. The founder of Shipt, Bill Smith, got the idea for grocery delivery by experiencing how hard it is to do grocery shopping with his young children. Guess what? We don’t have to take toddlers to the grocery store anymore, unless we want to.

Will they be subpoenaed? If yes, will they comply? If they comply will they be arrested? If arrested will they be tried and convicted? If convicted will they be pardoned? If pardoned will he be impeached? If at any point your deductive reasoning concludes with a “no”, then you can reason backwards inductively to why this is happening.

Homan: "We're not stopping. I don't care what the judges think. I don't care what the left thinks. We're coming."

Trade. Diplomacy. Aid. National Defense. Social Security. Medicaid. National Institute of Heatlh.

These are big things and they are under duress at best, out right attack at worst. It’s useful to when observers point out that bad policies are bad, that people are getting hurt, that there are consequences in play that have not been in play in since the early days of the Union. It’s useful, but what’s the next step? What is actionable?

I’m curious about the political incentives for damage control. Is there credit to be had for politicians who lay themselves on the tracks in front of an administration that seems to run on spite, to draw the kind of attention that will lead to retribution against their districts and states? Are we seeing so little action on the part of the opposition party because there is no political incentive to take action?

Put another way, how do you sell opposition to constituents as they begin the feel the pain of new policy regimes? Is it simply going on TV to lay the blame ex post or do you tell them the pain is coming in advance? Is it good politics to serve as the messenger of doom for someone else’s policies?

This isn’t building up to a big observation. I don’t know. These are just the questions I’m walking around with. There’s something about the current administration that makes political opposition feel like punching a cloud. No one is sure what the adminstration can and can’t get away with. What the courts will strike down or hold up. What the next hour’s executive order will be. How do you oppose chaos if chaos is the sole (governance) objective?

The simple answer may simply be to begin building institutions at the subnational level. That takes time, and tax dollars, to be sure, but sometimes you have to plant trees whose shade you will never sit in. It doesn’t just have to be single states, either. Why can’t New York, California, and Massachusetts have their own health consortium to prepare flu vaccines and fund research? Why can’t Texas, Oklahoma, New Mexico, and Arizona set aside resources to grow solar power generation? I don’t know how you escape federal tariffs legally, but such considerations don’t seem to be slowing down the executive branch. Why can’t California or Michigan play the same game?

I don’t know where this is going, and the entire political landscape may shift the first time Social Security checks go out a week late, but at some point the opposition will have to pivot from anger and resistance to building for a new and different governance landscape, and that will include rebuilding newer, perhaps more resilient or even redundant institutions. It’s all pie in the sky until it isn’t.

It’s hard to keep up with all of the Trump administration’s activities. There is such a flurry of activity related to funding, regulations, and executive actions that no one can keep up with everything. Individuals and news outlets have scarce resources and attention. There’s the added typical challenge of filtering out fact from analysis. If only there was way to summarize the administration’s activities in an objective and meaningful sense.

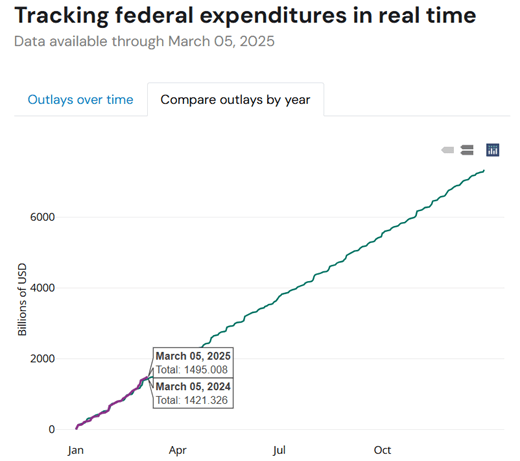

Luckily, numbers don’t lie – and the federal government publishes a lot of numbers. Specifically, they publish the Daily Treasury Statement which identifies each day’s various categories of outlays. We can look at the raw number of spending to get a sense for where and whether Trump is changing spending within the federal government.

Lauren Bauer at The Hamilton Project noticed that the US Treasury has an API for those daily statements. She created a nice online tool at Brookings that is relatively user friendly. Individuals can visit and see each day’s spending or the cumulative spending throughout the year. Below is the cumulative federal spending for 2024 and 2025. As of March 5th, the US has spent a total of 5.2% more in 2025 than in the year prior (that’s on track with the growth rate of GDP). Importantly, she makes all of the data available for download so that individuals can conduct their own analysis. I lean on her data here.

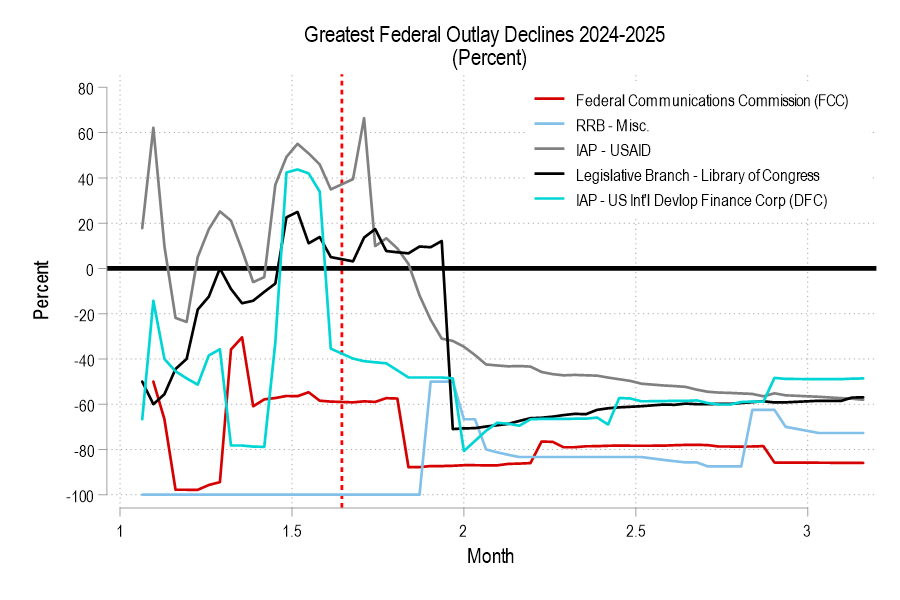

Where have the cuts been happening? The below graph includes the 5 spending areas that have been most deeply cut relative to the same day in 2024.* The red line denotes inauguration day. The USAID cuts made big news, and it seems like they knew something was happening around the time of inauguration. It looks like they were trying to get spending out the door before the taps were shut off. The FCC and the Library of Congress were also affected by the funding freeze that was announced in late January.

President Trump claims to have made cutting waste a priority. With Elon Musk in tow, the administration has made waves by disrupting USAID, the NSF, and federal payroll. We’re 45 days into the administration. We can use the data provided by the Treasury and made accessible by Bauer to evaluate how the Trump administrations has been spending and cutting according to the numbers.

One way to evaluate spending is to compare the cumulative spending over the course of 2024 and 2025. That is, spending on the 45th day of the year should be more or less comparable in 2024 vs 2025. It’s still early in the year and since various payments can be quite irregular, there’s a lot of noise in the data so far. But we should be able to see big changes. Smaller changes will be easier to see as the year goes on.

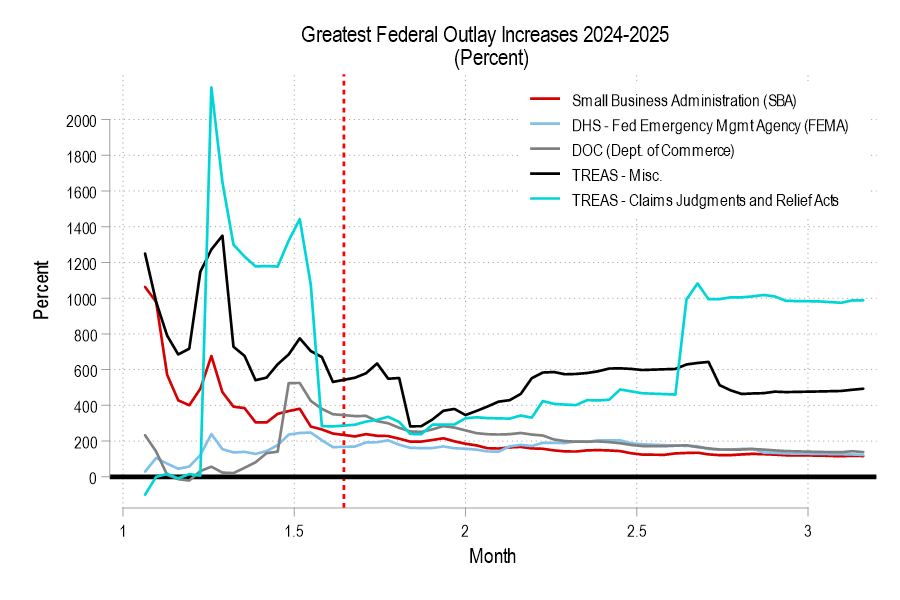

The 5 areas of greatest cumulative spending growth relative to 2024 are graphed below.* It does look like some funding was trying to get out of the door prior to Trump taking office, but that’s just speculation on my part. FEMA spending was up, likely due to the fires in California. Much more US Treasury spending is happening, specifically for Claims, Judgments, & Relief. We might see that remain elevated as the new administration keeps ‘trying’ things and then being stopped by injunctions, being the subject of lawsuits, and owing compensation.

While big percent changes in outlays can have massive implications for individual programs, Musk and Trump will need to cut huge amounts in order to claim any kind of victory over profligate spending. (Just so we’re all on the same page, they will fail if they refuse to touch old-age entitlements.) Where have the biggest spending cuts happened as measured by actually dollars? See below.*** The deepest and most consistent cuts are coming from the reductions in federal employee insurance payments. Similarly, the USAID and FCC cuts amount to a $2 billion cut from this time last year. Department of Education spending and the hospital insurance trust fund are down, but are also more volatile in their expenditures. Those one-time spikes in the data are due to pay dates between 2024 and 2025 being offset by a day or two.

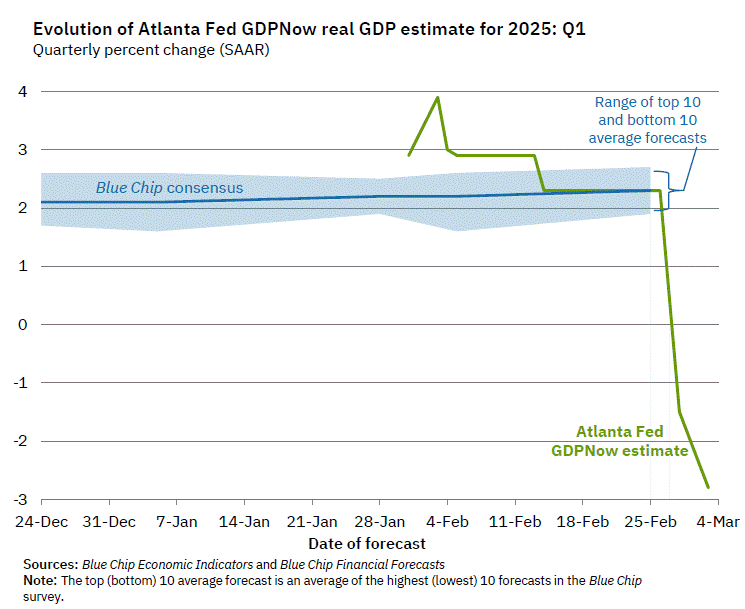

The chart comes from the Atlanta Fed’s GDPNow model, which tries to estimate GDP growth each quarter as data becomes available. The sharp drops in their Q1 forecast for 2025, based on the last two data updates, look pretty shocking. Should we be worried?

First, it’s useful to ask: has this model been accurate recently? Yes, it has. For Q4 of 2025, the model forecast 2.27% growth — it was 2.25%. For Q3 of 2024, the model forecast 2.79% growth — it was 2.82%. Those are very accurate estimates. Of course, it’s not always right. It overestimated growth by 1 percentage point in Q1 of 2024, and it underestimated growth by 1 percentage point the quarter before that. So pretty good, but not perfect. Notable: during the massive decline in Q2 2020 at the start of the pandemic, it got pretty close even given the strange, uncertain data and times, predicting -32.08% when it was -32.90% (that’s off by almost 1 percentage point again, but given the highly unusual times, I would say “pretty good”).

OK, so what can we say about the current forecast of -2.8% for Q1 of 2025? First, almost all of the data in the model right now are for January 2025 only. We still have 2 full months in the quarter to go (in terms of data collection). Second, the biggest contributor to the negative reading is a massive increase in imports in January 2025.

To understand that part of the equation, you have to think about what GDP is measuring. It is trying to measure the total amount of production (or income) in the United States. One method of calculation is to add up total consumption in the US, including by final consumers, business investments, and government purchases and investments. But this method of calculation undercounts some US production (because exports don’t show up — they are consumed elsewhere) and overcounts some US production (because imports are consumed here, but not produced here). So to make GDP an accurate measure of domestic production, you need to add in exports, and subtract imports.

Keep in mind what we’re doing in this calculation: we aren’t saying “exports good, imports bad.” We are trying to accurately measure production, but in a roundabout way: by adding up consumption. So we need to take out the goods imported — not because they are bad, but because they aren’t produced in the US.

The Atlanta Fed GDPNow model is doing exactly that, subtracting imports. However, it’s likely they are doing it incorrectly. Those imports have to show up elsewhere in the GDP equation. They will either be current consumption, or added to business inventories (to be consumed in the future). My guess, without knowing the details of their model, is that it’s not picking up the change in either inventories or consumption that must result from the increased imports. It’s also just one month of data on imports.

As always, we’ll have to wait for more data and then, of course, the actual data from BEA (which won’t come until April 30th). More worrying in the current data, to me, is not the massive surge in imports — instead, it’s that real personal consumption expenditures and real private fixed investment are currently projected to be flat in Q1. If consumption growth is 0% in Q1, it will be a bad GDP report, regardless of everything else in the data.