The author of The Psychology of Money, Morgan Housel, has a new book “The Art of Spending Money” out this month. Its main point is that people tend to be happier spending money on things they value for their own sake- rather than things they buy to impress others, or piling up money as a yardstick to measure themselves against others (this is repeated with many variations).

Overall it is well-written at the level of sentences and paragraphs with well-chosen stories and quotes, but I’m not sure what it all adds up to. The main points seem obvious to me, though maybe that’s my fault for reading a book titled this when I’m already fairly happy with how I spend money. I think I err a bit on the frugal side, but I just don’t see many opportunities to turn money into happiness by spending it- I was maybe hoping for ideas on that front but I got none from the book. After reading it I don’t plan to do anything differently and don’t find myself thinking about spending differently.

Still, some highlights. The book is full of well-chosen quotes from others:

One of the likely effects of the federal government shutdown is that recipients of SNAP benefits (what used to be officially called “food stamps,” a term still used by the general public, especially those that dislike the program) may lose their benefits next month. This would obviously be a hardship for those that depend on this program, but it has also led to bad claims being made about the program, from both supporters and opponents of the program.

Let’s start from the political right: Matt Walsh makes the claim that by subsidizing food consumption “obviously drives up the cost” of groceries.

The number one thing that artificially inflates the price of groceries is the food stamp program. The federal government is subsidizing groceries for 40 million people which obviously drives up the cost. That's why the increase in the cost of groceries tracks exactly with the…

As with all bad claims, there is a nugget of truth baked into them. If the government subsidizes anything, we would expect demand to increase, and thus unless supply is perfectly elastic, there will be some effect on prices. However, we need to think more carefully about the nature of the subsidy.

The way SNAP works is that beneficiaries receive an electronic voucher to spend at the grocery store, which is about $300 per month on average for a household. That $300 must be spent on groceries. However, if that household had already planned to spend $300 or more on groceries, it is unlikely they will spend all of the additional $300 on food. In the limit, it’s entirely possible they will spend no additional money on groceries, merely reducing their out-of-pocket spending on groceries by $300. They will then effectively have $300 more to spend on other goods. More likely is that they will spend some of the additional $300 on groceries, and some of it on other goods.

Many studies have tried to look at the extent to which SNAP benefits affect household spending, but these were mostly observational studies. There was no treatment and control group. But a 2009 paper titled “Consumption Responses to In-Kind Transfers: Evidence from the Introduction of the Food Stamp Program” has a better approach to studying the question. Since the original Food Stamp program was slowly rolled out across the country over more than a decade, you can compare counties that entered the program first to counties that entered it later. By doing so, Hilary Hoynes and Diane Schanzenbach find out some first interesting things about the causal effects of SNAP benefits.

For the claim by Walsh in his Tweet, the most relevant result from the paper is that food stamps impact household spending similarly to a cash transfer. Yes, the program increases household spending on groceries, but it also increases spending on other goods and services. And it does so almost identically to how cash transfers impact household spending. In other words, while pitching the program as assistance for buying groceries may make it more politically palatable, SNAP benefits are no different from a similarly-sized cash transfer for the average recipient. If they do cause any inflation, they do so in the same way as a cash transfer would, and thus there is no specific impact on food inflation.

A second bad claim about SNAP comes from the political left, in this case Minnesota Governor Tim Walz:

This is the third in a series of occasional blog posts on individual initiatives that made a strategic (not just tactical) difference in the course of the second world war.

World War II was not only the biggest, bloodiest conflict, in human history. It played a definitive role in giving us the world we have today. Everyone can find something to complain about in the current state of affairs, but think for a moment what the world would be like if the Axis powers had prevailed.

Having control of the air became crucial in the second world war. It meant you could drop bombs on enemy soldiers, ships, tanks, cities, factories, etc., etc. The Germans showed early on how important that can be. Their terror bombing of the Dutch city of Rotterdam compelled the Netherlands to surrender to spare other cities from being likewise bombed, even though the Dutch armed forces could have held out for some time longer. The German breakthrough in their invasion of France in 1940 was facilitated by a concentrated Stuka dive bombing attack on a key sector of the French front lines. The 1940 Battle of Britain was an air war, where the Germans hoped to whittle the British Air Force capability down enough to permit them to invade across the English Channel. And so on.

The main German fighter plane at first was the Messerschmidt Me 109. It was a good plane, although by 1941 the British Spitfire had become a match for it. Both the Me 109 and the Spitfire were designed around in-line engines, where the cylinders were arranged in two long rows in the engine block. That gave a narrow engine, and hence a skinny profile to the airplane, which tended to reduce wind resistance and make for higher speeds. A weak point of all in-line engines is that they need to have a circulating coolant system, going through a radiator, to cool down the engine block from the heat of the internal combustion. This makes for more complicated maintenance and is very vulnerable to being damaged by enemy fire,

Just when the Brits were starting to wrest air superiority back from the Germans, the FW 190 appeared in the skies over France. Allied pilots were shocked. The new German fighter could out-climb, out-roll, and in many cases out-fight the current Spitfire models. This so-called “butcher bird” gave air superiority back to the Germans.

Its remarkable performance was the result of one man’s engineering philosophy and persistence: Kurt Tank, chief designer at the German aircraft manufacturer Focke-Wulf. Tank was a pilot as well as an engineer, with long and varied prior military experience. He chose a radial engine for his plane, to make it more rugged and easy to maintain. With a radial engine, the individual cylinders all stick out from a central crankcase; airflow past the fins on the cylinders cools the engine. Hence, no vulnerable cooling system and radiator. The conventional thinking was that a radial engine was so fat that an airplane using it would have a wide, draggy profile. His ingenious design features allowed him to make a fast, agile plane. However, was an uphill job for Tank to sell his concept to the German military establishment. Eventually, his results spoke for themselves and the Fw 190 was produced. With its critical spots armored, the Fw 190 was hard to kill. Tank deliberately gave a wide stance and long travel to the landing gear, to allow deployment in rough frontline airfields.

The Fw 190 was a superb low-medium altitude fighter, and was also widely pressed into service (due to its rugged design) as a precision bomber on the front lines. Around 20,000 Fw 190s were produced. They shot down many thousands of Allied planes, killed untold thousands of Allied airmen and soldiers, and destroyed thousands of Allied vehicles, mainly on the Eastern Front. It was not enough to change the ultimate outcome of the war, but Tank stretched it out appreciably, by (largely single-handedly) giving the Germans such a versatile and deadly weapon.

Sports gambling is entering it’s first series of major crises since widespread legalization. While there is the typical handwringing around the intersection of vice and broad entertainment, there is also the added dimension of the role that insider information can and should play within any speculative market. Those arguments, conducted earnestly, are of course completely valid, but I think they are not giving enough attention to a key distinction in the online incarnation of sports gambling.

Speculating on sports outcomes produces the same elicitation and aggregation of information as a more traditional speculative market, such as commodities futures or stock equity markets. Information, acted upon through purchase, reveal each individual’s beliefs about the true value of a contract paid upon the conclusion of a sporting event or the price of agricultural commodity at a given date and time. The market exchange of these contracts aggregates these beliefs into a collective piece of information in the form of a market price. Some contract holders get richer, some poorer, and the broader world benefits from the distillation of private information into public prices. The problems within sports gambling stem from the second channel through which entertainment is provided and paid for: random outcome generation.

Sports match outcomes are something you speculate on. Random outcomes are something you gamble on. Yes, there is random chaos in sports the same way there is random weather in agriculture. There is no speculating on a roulette wheel, however, that’s a pure gamble. I believe the major sports leagues and the online gambling companies they partner with have made a grievous error allowing their sites to offer (nearly) pure gambles.

Think about how much casinos invest in the integrity of their games as pure and fair gambles. Dice are rigorously inspected and routinely replaced. Roulette wheels are engineered with astounding tolerances. Card games occur under multiple layers of scrutinous observation. Manipulation under such conditions is sufficiently costly such that it is almost never worth undertaking.

How do you go about making similar investments in monitoring 6 inches of horizontal manipulation of the first pitch of a baseball game? Of a marginal player taking himself out of a game injured a few minutes early? The answer is you largely can’t. So now you have human roulette wheels who can decide what number they land on. Which brings us to the second, closely related problem in the new regime of sports gambling: inframarginal game outcomes. Once a game is probabalistically decided before its official conclusion, teams will often play their substitutes to finish out the formality in order to rest their main players and protect them from injury. These players typically earn smaller salaries, often over far shorter careers, with less scrutiny over their quality of play. These are the exact players for whom a couple hundred thousand dollars may be worth incurring a small amount of risk. The product of their play in terms of success (i.e. scoring, hitting, etc) is still highly conditional on their ability relative to their opposition, but the play itself (i.e. shooting, swinging, pitching choices, fouling, etc) is entirely within their control. It may be less purely random, but it is nonetheless sold to gambling customers as fair.

Whether the outcomes in question are quasi-random outcomes or merely inframarginal, what matters is that they are not joint products of competition. To significantly manipulate these outcomes does not require the explicit or implicit coordination of multiple individuals across competing teams. Yes, one player can tilt the odds, but if you are looking to make significant money manipulating sports gambling, you can’t just tilt the odds a few percentage points. There’s a reason the Black Sox Scandal of 1919 involved eight players (seven if you consider Buck Weaver innocent, which I do).

As I love to point out, coordination across individuals is very difficult. Crimes involving coordination are, in turn, far easier to monitor. Online gambling massively reduced the transaction costs in sports gambling, opening the door for orders of magnitude increases in the number and variety of bets that could be taken. There’s obviously demand for pure gambling alongside outcome speculation, and that demand could now be met through random and inframarginal in-game player outcomes.

The danger, of course, is that few of these events are truly inframarginal. Every pitch and available player counts towards the outcome. Enough manipulation by enough players will graze away the integrity of the core product. The subsidy of lower end players through gambling will change how they approach their careers and how management approaches their employment. Fans will react accordingly as well, adjusting how they view outcomes. We’re already seemingly hardwired to view everything as causal and conspiratorial, overestimating bias in refereeing and player preferences. This will only stoke those fires further.

Organized crime famously offered a “numbers game” prior to state lotteries. Desperate for a credibly random outcome, a common mechanism was to use the middle three digits of the number of shares traded on the NYSE as the winning number. There are no shortage of lotteries now, but there obviously remains latent demand, and customers clearly enjoy bundling gambling with a product far more entertaining to consume than scratching off a ticket. Pro sports was unable to deny the profits from exactly such a bundling, but the cross contamination with their core product may prove to be of greater cost.

I’m not businessman, just a lowly economist and sports fan, but if I were running a $11.3 billion per year firm, I would be far more risk averse.

Since the great depression is over, what are the big events of the 21st century for macroeconomics?

9/11 and shoring up bank confidence subsequently

The Great Recession and preceding mortgage crisis

Covid and subsequent stimulus

This conversation is a tour of the trade offs under consideration at the Central Bank at these pivotal moments in the 21st century.

Beckworth: I think this is where it’s important to do the right counterfactual. What could have been could have been far worse, right? If there hadn’t been these interventions, so it’s easy to criticize from the outside, and there’s a lot of criticisms the Fed received at this time. Not to say we would have gone all the way to the Great Depression, but the fact that it was possible, right, this financial system was crashing.

Talk to some economists and they’ll tell you that exchange rates aren’t economically important. They say that exchange rates between countries are a reflection of supply and demand for one another’s stuff. So, at the macro, it’s a result and not a determinant of transnational economic activity.

For individual firms at the micro level, it’s the opposite. They don’t affect the exchange rate by their lonesome and are instead affected by it. If you have operations in a foreign country, then sudden changes to the exchange rate can cause your costs to be much higher or lower than you had anticipated. The same is true when you sell in a foreign country, but for revenues. This type of risk is called ‘exchange rate risk’ since it’s possible that none of the prices in either country changed and yet your investment returns change merely because of an appreciated currency.

Supply & Demand

Exchange rates are determined by supply and demand for currencies. Demand is driven by what people can do with a currency. If a country’s goods become more attractive, then demand for those goods rise and demand for the currency rises. After all, most retailers and wholesalers in the US require that you pay using US dollars. Importantly, it’s not just manufacturing goods that drive demand for currency. Demand for services, real estate, and financial assets can also affect the supply and demand for currency. In fact, many foreigners are specifically interested in stocks, bonds, US treasuries, and other investments. The more attractive all of those things are, the more demand there is for them.

Of course, the market for currency also includes suppliers. Who does that? Answer: Anyone who holds dollars and might buy something. Indeed, all buyers of goods or financial products are suppliers of their medium of exchange. In the US, we pay in dollars. Especially since 1972, suppliers have also included other central banks and governments. They treat the US currency as if it’s a reserve of value, such as gold, that can be depended upon if they need a valuable asset (hence the name, “Federal Reserve”). This is where the term ‘reserve currency’ comes from – not from the dollar-denominated prices of some internationally traded commodities. Though, that’s come to be an adopted meaning.

Another major supplier of currency is the US central bank. It has the advantage of being able to print US dollars. But it doesn’t have an exchange rate policy. So, it’s not targeting a particular price of the US dollar versus any other currency. The Fed does engage in some international reserve lending, but it’s not for the purpose of supplying currency to foreign exchange markets.

The US Exchange Rate in 2025

One of the reasons that the US has such popular financial assets is that we have highly developed financial markets and the rule of law. People trust that, regardless of the individual performance of an asset, the rules of the game are mostly known and evenly applied. For example, we have a process to follow when bond issuers default. So, our popularity is not merely because our assets have higher returns. Rather, US investment returns have dependably avoided political risk – relative to other countries anyway.

LinkedIn has its problems, but so does every other social network.

I joined LinkedIn out of college because it seemed like something you were supposed to do if you want a job someday, but I never checked it because the academic job market makes little use of LinkedIn. In 2013 LinkedIn added social media features like a newsfeed, but I still never spent time there. Facebook and Twitter seemed more interesting, and like many people I’ve always been allergic to “networking” or other social settings where one person is just trying to get something from another. It seemed like a recipe for posts that are cringe, soulless, or desperate.

But over the past couple years, I’ve found myself spending more time there- and not because I’m looking for a job or looking to hire. Some of the posts are genuinely interesting, and it is a nice way to keep up with what people I know are up to. Either LinkedIn got better or I got worse.

I find that LinkedIn is particularly good for staying in touch with my old students. I always told my students they could still e-mail me or stop by my office after the semester is over, but they almost never do; that takes a lot of thought and energy. Social networks are the ideal way to keep in touch with “weak ties“, but you have to find the right one. Facebook was the best for this when it was ubiquitous, but now it is becoming more common for Americans not to have or not to check Facebook, especially young ones (plus it was always a bit too personal for former students). Twitter has never been something that most people have, and the more popular networks are either too personal (Instragram, Snap et c) or too impersonal where almost all content users see comes from people they don’t know (TikTok, Youtube, et c).

LinkedIn by contrast is ubiquitous and just the right amount of personal. It also seems to be increasingly a good place to share interesting writing. I like much of what I read there, and my writing gets a good reception; I tend to get more engagement for EWED posts on LinkedIn than on X and Facebook despite having fewer connections there than Facebook friends or Twitter followers. Yes, you’ll still see some cringe posts there, but it beats the angry political posts that are ubiquitous on Facebook and especially X.

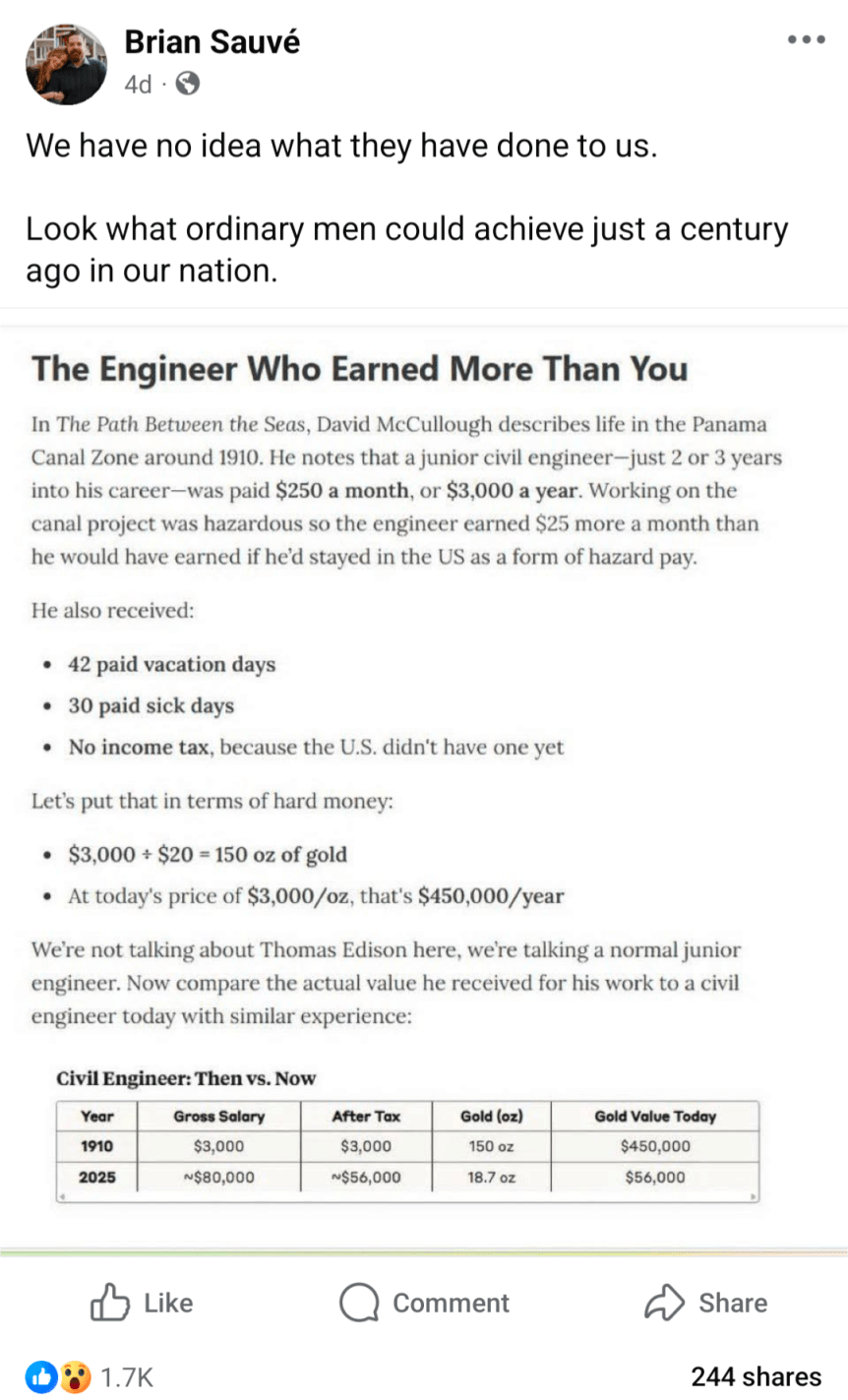

Inflation adjusting income and prices from the past is a common theme in my blog posts, including fact checking of other attempts to do these adjustments. But here is a really novel one, in a viral post from Facebook (which comes from this essay), which claims that a civil engineer earned the equivalent of $450,000 in today’s terms:

Can this be correct? If so, it would represent massive stagnation in incomes over time. Thankfully, there are two major errors, or at least misleading aspects to the calculation.

The listed salary was not one of an “ordinary man” — far from it.

Using gold prices to inflation adjust the incomes is very misleading.

First, the salary: $3,000 per year was definitely not what ordinary men earned. The average wage, for example, for a production worker in manufacturing was 18 cents per hour. You would need to work almost 17,000 hours to earn $3,000 at that wage, which of course is not possible. In reality, the average worker put in 57 hours per week — which means they earned about $500 if they were able to work 50 weeks per year (most probably didn’t). So already we see that the civil engineer working on the Panama Canal is making about 6 times as much as an “ordinary man.” Agricultural workers, the other main industry of 1910, earned about $28 per month ($22 if they also received board) — even less than manufacturing, and only about 1/10 of the engineer

Second, the gold price adjustment is misleading. Yes, in 1910, gold was how we defined currency in the US. But you can’t eat gold, and most people only keep a little gold on hand that can be described as providing services for them (such as jewelry). What people really wanted were real goods and services, and mostly goods. Around 1910, the average American household spent about 40% of their income on food, 23% on housing, and 15% on clothing. Comparing standards of living over time requires us to look at what people spend their money on, not what the currency is denominated in. And that’s what a good consumer price index does: it compares the prices of all consumer spending at different points in time, not just one thing like gold, allowing us to make rough comparisons of income over time.

Using the Measuring Worth historical CPI (which extends the BLS CPI back before 1913), we see that the index was 9.21 in 1910, and it stands at 323.364 in August 2025. So the 18-cent manufacturing wage from 1910 is roughly equivalent to $6.32 in current dollars. The average manufacturing wage today? Around $29. And of course, workers today have a whole range of fringe benefits, worth roughly another $13.58 for private sector workers. This means that an “ordinary man” today working in manufacturing can buy 5-7 times as many real goods and services as his 1910 counterpart for each hour he works. And the work is, of course, much safer today: BLS reports 23,000 industrial deaths in 1913 (61 deaths per 100,000 workers), but only 391 manufacturing deaths in 2023 (0.003 deaths per 100,000 workers).

But what about that extraordinary man in 1910, the civil engineer? How was he doing compared with today? Using the same historical CPI, we can see that $3,000 in 1910 is roughly equivalent to $105,000 today. Not bad! That’s almost exactly the median pay for civil engineers today. But keep in mind the civil engineer working in Panama was an unusually highly paid position. A 1913 report from the American Society of Civil Engineers suggests that most early career civil engineers were making closer to $1,500 per year — half of the Panama engineer. Engineers were also a highly skilled, very rare profession in 1910. And don’t forget that about 10% of the American workers on the Canal died in the construction, mostly from disease so the engineers were probably just as susceptible to death as the laborers.

Finally, we might ask a different question: what if you had held onto gold since 1910? Let’s say your great-great grandfather was a civil engineer, and managed over the course of a few years to save one year’s salary in gold. He even managed to hide it during the 1930s-1970s, when private holding of gold was generally illegal in the US.

How much would that 150 ounces of gold be worth today? That answer is simple: about $615,000 today (gold has gone up a bit just since that calculation was done in May!). But was that a good investment? Not really. A $3,000 investment in the stock market from 1910 to 2024 would be worth about… $120 million (it’s actually a bit more than that, since the market continued to rise after January 2024). Of course, that would have required a bit of active management, since index funds don’t come along until much later. But your great-great grandfather would have been much wiser to set up a trust for you and have it actively managed to approximate the entire US stock market, rather than to bury 150 ounces of gold in his backyard.

Even assuming you lost half the value to management fees, the stock portfolio today would be worth at least 100 times as much as the gold.

This is the second of a series of occasional posts on observations of how some individual initiatives made strategic impacts on World War II operations and outcome. While there were innumerable acts of initiative and heroism that occurred during this conflict, I will focus on actions that shifted the entire capabilities of their side.

It’s the summer of 1941. The war in Europe between mainly Germany and Britain had been grinding on for around two years, with Hitler in control of nearly all of Europe. The Germans then attacked the Soviet Union, and quickly conquered enormous stretches of territory. It looked like the Nazis were winning. Relations with Japan, which aimed to take over the eastern Pacific region were uneasy. The Japanese had already conquered Korea and coastal China, and were eyeing the resource-rich lands of Southeast Asia and Indonesia. It was a tense time.

The Japanese military had been building up for decades, preparing for a war with the United States for control of the eastern Pacific. They developed cutting edge military hardware, including the world’s biggest battleships, superior torpedoes and a large, well-trained aircraft carrier force. They also produced a new fighter plane, dubbed the “Zero” by Western observers.

Intelligence reports started to trickle in that the Zero was incredibly agile: it could outrun and out-climb and out-turn anything the U.S. could put in the air, and it packed a wallop with twin machine cannons. Its designers achieved this performance with a modestly-powered engine by making the airframe supremely light.

As I understand it, the U.S. military establishment’s response to this intel was fairly anemic. It was such awful news, that seemingly they buried their heads in the sand and just hoped it wasn’t true. Why was this so disastrous? Well, since the days of the Red Baron in World War I, the way you shot down your opponent in a dogfight was to turn in a narrower circle than him, or climb faster and roll, to get behind him. Get him in your gunsights, burst of incendiary machine-gun bullets to ignite his gasoline fuel tanks, and down he goes. If the Zero really was that agile, then it could easily shoot down any U.S. plane with impunity. Even if you started to line up behind a Zero for a shot, he could execute a tight turning maneuver, and end up on your tail, every time. Ouch.

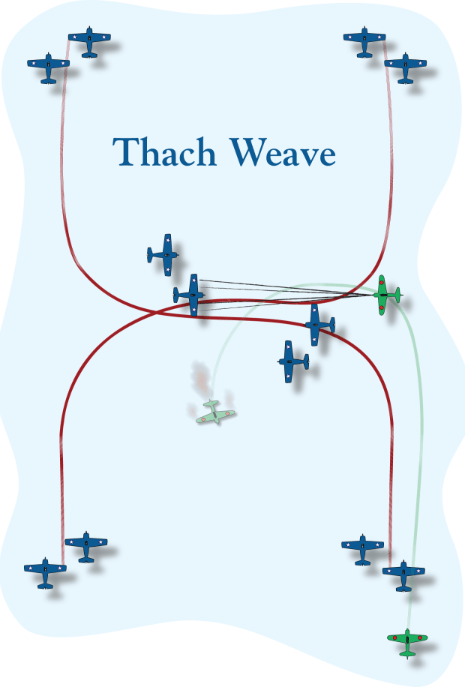

A U.S. Navy aviator named John Thatch from Pine Bluff, Arkansas did take these reports on the Zero seriously. He racked his brains, trying to figure out a way for the clunky American Wildcat fighters to take on the Zeros. He knew the American pilots were well-trained and were good shots, if only they could get some crucial four-second (?) windows of time to line up on the enemy planes.

So, he spent night after night that summer, using matchsticks on his kitchen table, trying to invent tactics that would neutralize the advantages of the Japanese fighters. He found that the standard three-plane section (one leader, two wingmen) was too clumsy for rapid maneuvering. He settled on having two sections of two planes each. The two sections would fly parallel, several hundred yards apart. If one section got attacked, the two sections would immediately make sharp turns towards each other, and cross paths. The planes of the non-attacked section could then take a head-on shot at the enemy plane(s) that were tailing the attacked section.

The blue planes are the good guys, with a section on the left and on the right. At the bottom of the diagram, an enemy plane (green) gets on the tail of a blue plane on the right. The left and the right blue sections then make sudden 90 degree turns towards one another. The green plane follows his target around the turn, whereupon he is suddenly face-to-face with a plane from the other section, which (rat-a-tat-tat) shoots him down. In a head-to-head shootout, the Wildcat was likely to prevail, since it was more substantial than the flimsy Zero. Afterwards, the two sections continue flying parallel, ready to repeat the maneuver if attacked again. And of course, they don’t just fly along hoping to be attacked, they can make offensive runs at enemy planes as well, as a unified formation. This technique was later dubbed the “Thatch weave”.

Thatch faced opposition to his unorthodox tactics from the legendary inertia of the pre-war U.S. military establishment. Finally, he and his trained team submitted to a test: their four-plane formation went into mock combat against another four planes (all Wildcats), but his planes had their throttles restricted to maximum half power. Normally that would have made them toast, but in fact, with their weaving, they frustrated every attempt of the other planes to line up on them. This demonstration won over many of the actual pilots in the carrier air force, though the brass on the whole did not endorse it.

By some measures the most pivotal battle in the Pacific was the battle of Midway in June, 1942. The Japanese planned to wipe out the American carrier force by luring them into battle with a huge Japanese fleet assembled to invade the American-held island of Midway. If they had succeeded, WWII would have been much harder for the U.S. and its allies to win.

The way that battle unfolded, the U.S. carriers launched their torpedo planes well before their dive bombers. The Japanese probably feared the torpedo planes the most, and so they focused their Zeros on them. Effectively only Thatch and two other of his Wildcats were the only American fighter protection for the slow, poorly-armored torpedo bombers by the time they got to their targets. Using his weave maneuver for the first time in combat, he managed to shoot down three Zeros while not getting shot down himself. This vigorous, unexpectedly effective defense by a handful of Wildcats crucially helped to divert the Japanese fighters and kept them at low altitudes, just in time for the American dive bombers to arrive and attack unmolested from high altitude.

In the end, four Japanese fleet carriers were sunk by the dive-bombers at Midway, at a cost of one U.S. carrier. That victory helped the U.S. to hang on in the Pacific until its new carriers started arriving in 1943. Thatch’s tactic made a material difference in that battle, and was quickly promulgated throughout the rest of the U.S. carrier force. It was not a complete panacea, of course, since the once the enemy knew what you were about to do, they might be able to counter it. However, it did give U.S. fighters a crucial tool for confronting a more-agile opponent, at a critical time in the war. Thatch went on to train other pilots, and eventually became an admiral in the U.S. Navy.

Universities continue to turn down the “Trump Compact”. The intitial nine schools targeted with an “invitation” were from a seemingly curated list of elite institutions, though some are perhaps notably less wealthy or more aspirational than the others. I can’t help but think there was some attempt to create a prisoner’s dilemma situation, where one more eager or fearful university might start a domino effect by committing first. That has not occurred.

What I do expect at some point in the coming weeks is a broadened offering of the compact to schools across the country. I expect messaging that specifically targets large public universities in states with Republican-controlled state legislatures that will be leveraged to pressure schools to sign on to the compact in hopes of currying favor with the administration and their voter base. I expect several schools to sign.

Here’s why I think that would be a grave mistake.

The compact comes with promises of “most-favored” status for applicants to federal grants through institutions such as the NIH, NSF, and Department of Defense. The thing is, they can promise that all they want. They don’t actually have that much influence over the review process. They’ll no doubt work to tip the scales on a few grants and promote them heavily, but the media coverage will vastly outweigh the dollars being shifted by the compact. It will, as always, be theater first and governance last.

But let’s say your school does procure several grants. Perhaps you’re a school that has in the past carried $20 to $30 million in active grants from the NIH and NSF, amounting to roughly $5 million per year in operating expenses. That sounds like a lot, but it’s not. Johns Hopkins University, by comparison, had $843 million in just NIH grants active in 2023. If you’re operating with $5 million a year in grant money, you have an office of sponsored projects, an Internal Review Board for human subjects research, and maybe an office for industry sponsorship. That maybe amounts to 15 to 20 personnel. What happens if the Trump administration comes through, putting its thumb on the scale for you, doubling or tripling your active grants within two years?

Chaos. Institutional chaos.

Sponsored research requires capital, personnel, and resource management. It requires legal compliance, doubly so if you’re spending federal money. It requires experienced leadership and management that know how to check boxes, file reports, track money, review protocols, and continuously train ever-churning research personnel.

But hey, that’s the point, you might be saying. We want to be ambitious and grown, we want to hire new and experienced personnel. We want to grow into an important research institution and this is our big chance! Be careful what you wish for. It’s one thing to incrementally grow over years and decades. It’s a whole other thing to try to do it in reaction to a sudden influx of money. Which, to be clear, isn’t just money. It’s an obligation. An expectation to produce scientific contributions on the US taxpayers’ dime. Obligations come with many things, but patience with incompetence borne of growing pains isn’t one of them.

But none of that is the problem. The real problem. Thetrap.

The trap is that this money isn’t going to stick around. This regime isn’t permanent. They aren’t invested in any way in scientific public goods or even science as a conept. This is, again, theater. They will move on to other things the instant it fails to the get the traction they want. They will lose elections, political tides will turn, etc. And what your institution will be left with is the reputation you earned.

And what will that reputation be? One of compliance with an anti-science, anti-public health, anti-intellectual regime. Further, you will judged on the fruits of that compliance. At the margin, it will be science that was undersupported, delayed in launch, stalled in execution, and eventually delivered short of expectations. You will have sold your reputation for a ticket on a ride you weren’t tall enough to be on yet. Grants will dry up, returning to previous levels or worse, leaving you with a bloated staff you no longer need, trying to find ways to lay off employees with all the protections of state government labor regulations.

There is no getting rich quick in academic research. There’s only avenues of over-reaching impatience ending in tears.