No, according to a new paper from the University of Georgia’s Michael Kotrous.

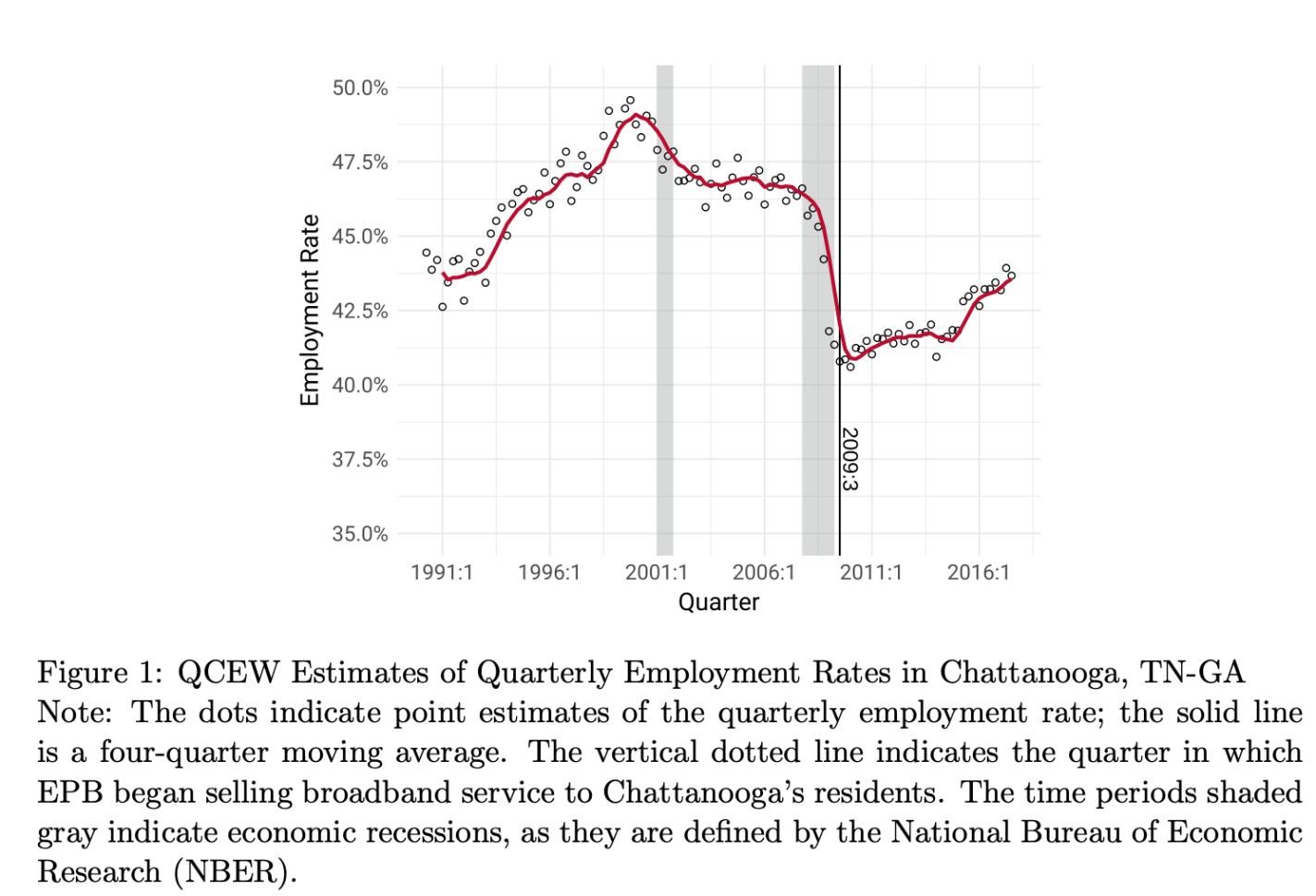

Many people expected it to, partly by thinking about the jobs that could benefit from faster internet, and partly by looking at the experience of Chattanooga, Tennessee. Chattanooga was the first major city to get gigabit-speed broadband, and they did see a huge improvement in the labor market right afterwards:

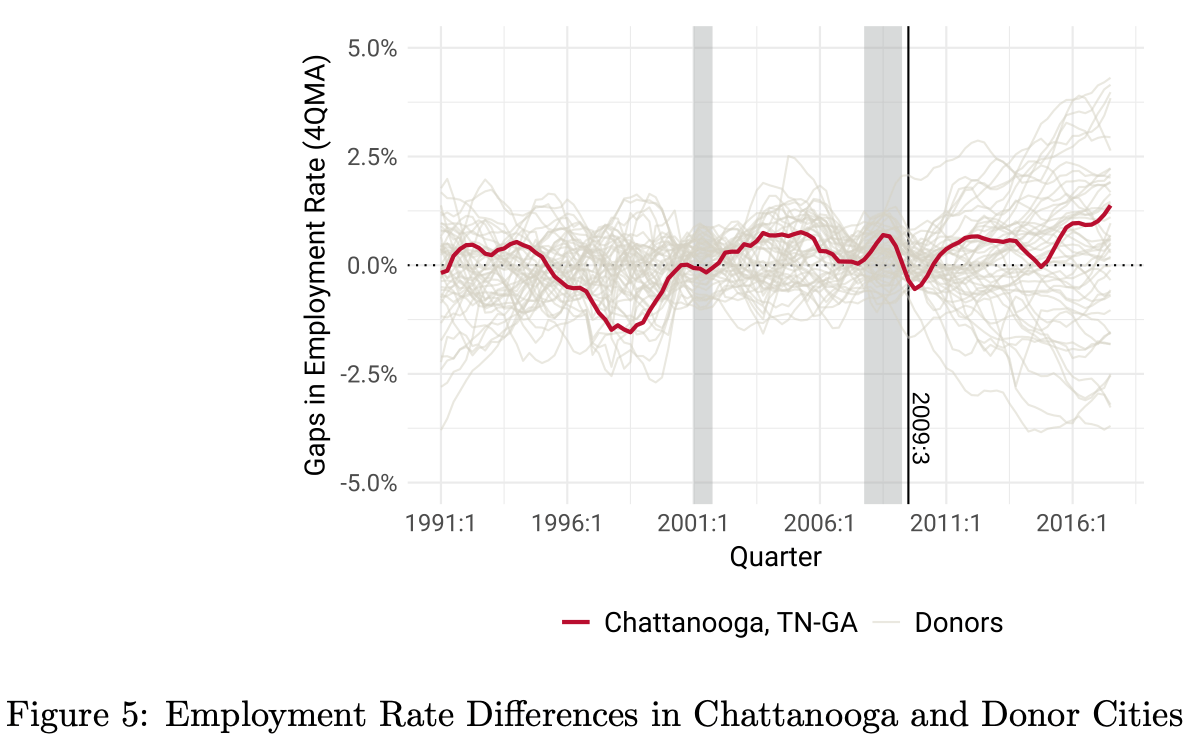

But as the graph shows, the introduction of broadband there coincides with the end of the nationwide Great Recession. Was the boom in jobs after 2009 because of the broadband, or would it have happened anyway as party of the recovery from recession? A synthetic control strategy shows that Chattanooga’s recovery was pretty typical for cities like it, so the broadband angle probably didn’t do much:

This might seem like a historical curiosity about one city, but the federal government is currently trying to spend $42 billion to expand broadband to more places, partly motivated by the idea of bringing jobs. I thought the Broadband Equity Access and Deployment Program‘s big problem is how slow it is- Congress created with the Infrastructure Investment and Jobs Act of 2021, but money didn’t start getting sent out until late 2025, and it could be many more years before it leads to any useable broadband. Even then it now seems unlikely to bring jobs, though there could be other benefits.

This paper’s author Michael Kotrous is currently on the economics job market. As his former professor and coauthor, I recommend hiring him if your school gets the chance.

The Iran regime’s military strategy seems to be that by bombing the oil infrastructure of their neighbors and neutral shipping, US gasoline prices will go so high that Americans will demand an end to the war.

How many Americans would be willing to pay $6/gallon gas for months for a ~50% chance of toppling a regime that oppresses 90 million people and destabilizes its region on the other side of the world? Probably only a minority of voters, especially when the President didn’t make the case to the American people or Congress beforehand.

But the US produces more than enough oil for its own needs. Why does the Strait of Hormuz being closed mean higher gas prices here? Only because US oil companies can sell to global markets, and they won’t choose to sell a barrel of oil to a US refiner for $60 when they could sell it to a foreign refiner for $100. If the government took away the foreign option, US oil producers would sell to US refiners at prices consistent with pre-war sub-$3/gallon gasoline.

Naturally there would be costs to an export ban. US oil producers would miss out on windfall profits, while Russian producers would benefit. Foreign customers of US oil, many of them in allied countries, would be angered by the missed shipments and global oil prices would soar further.

But if the US administration wants to avoid a midterm wipeout driven by high gas prices, I see only 3 options:

Get lucky and see the Iranian regime fall quickly

Negotiate an end to the war quickly (which might itself be unpopular if they can’t get a good deal) or just declare victory and go home (but its not clear whether Iran would re-open the strait now just because the US stopped bombing)

Restrict Exports

I say “restrict” not “ban” because I don’t think a complete export ban is necessary to stabilize US prices. You could instead do an export tax (high enough to stop many exports but low enough to allow the buyers with the highest values / fewest alternatives to stay in the market), or you could do a ban but allow a few export waivers for favored buyers or sellers (which seems like Trump’s style), or similarly a quota limiting exports to a certain number (say, limit each company’s monthly exports to 90% of their volume in the same month last year).

This has an obvious precedent: the Biden administration stopped issuing new permits to export liquified natural gas in 2024 to prevent prices spiking here during the Ukraine war (which led to even higher prices for our European allies). But a total ban on oil exports would be a much bigger deal.

Will the Trump administration actually try something like this? It will be an interesting test of US political economy to see what happens when the interests of the military-industrial complex conflict with the interests of oil producers.

We’re bombing Iran, and Iran is now bombing most of its neighbors. Oil prices are up ~20% since the bombing began last weekend, and stocks are down.

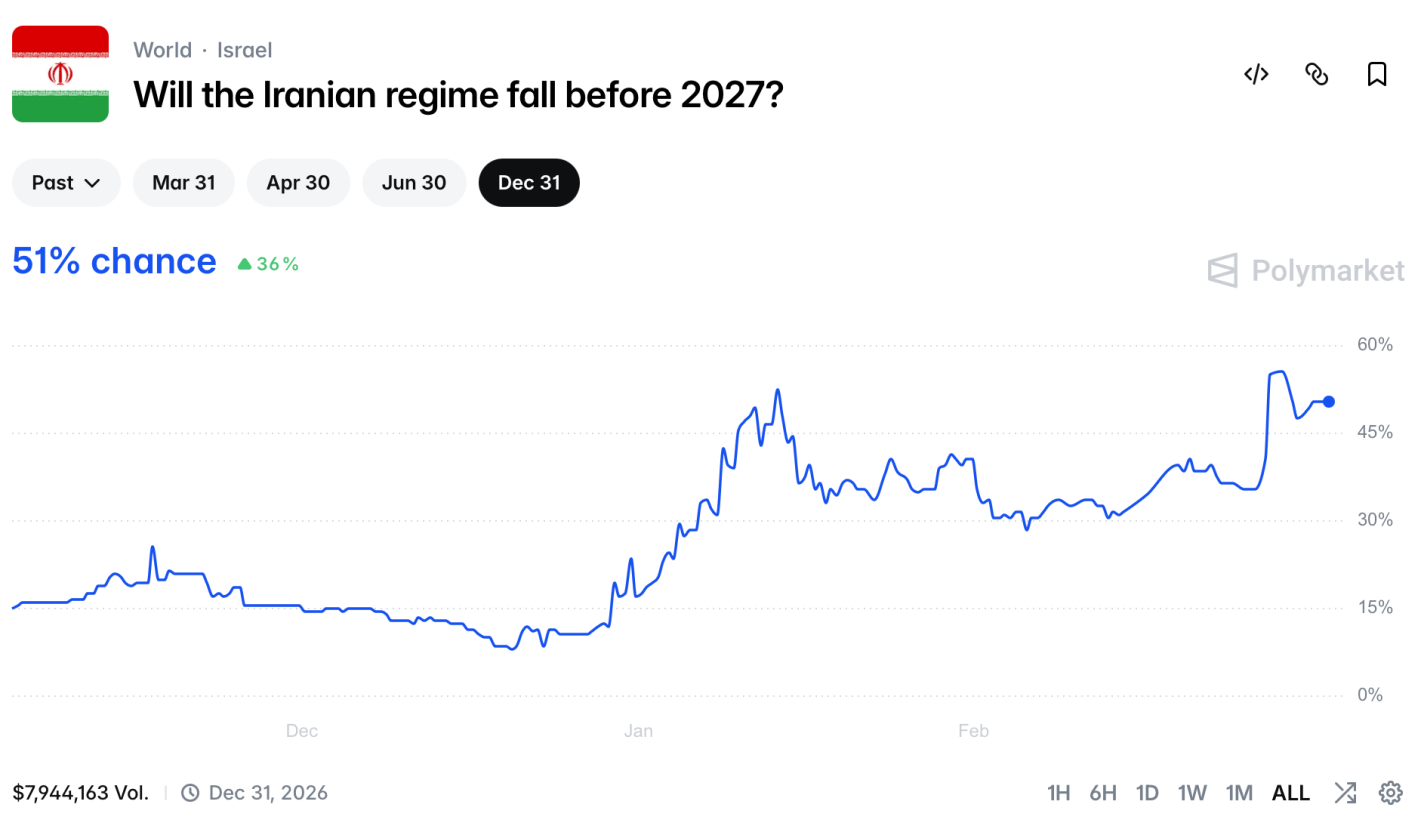

Iranian “Supreme Leader” Khamenei is now dead. Prediction markets sort of saw this coming; I mentioned here a month ago that markets thought it more likely than not that Khamenei would be “out of office” this year.1

Real-money US-regulated exchanges can’t directly cover the war, but others can and do, such as the international Polymarket:

Polymarket’s argument for why they offer these markets

This market shows that regime change is likely, but will take time- a 51% chance by the end of the year, but only a 13% chance by the end of the month.

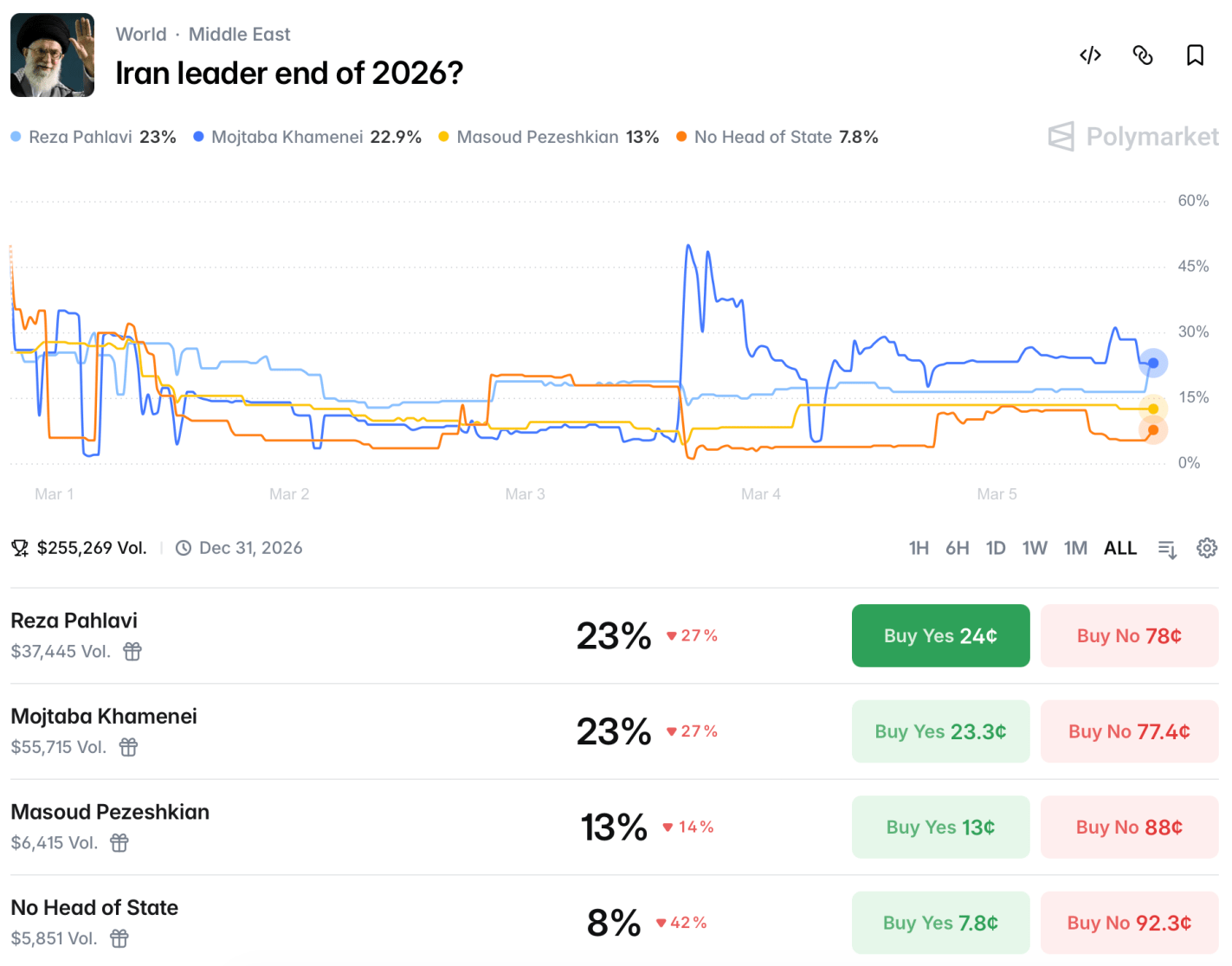

How would this be achieved? Markets see a 60% chance that there will be US troops in Iran this year, though this market could be triggered by just a few special forces operators, or by troops visiting for humanitarian purposes after domestically-driven regime change. There will likely be a US-Iran ceasefire by the end of May. It’s not clear at all who will be running Iran at the end of the year:

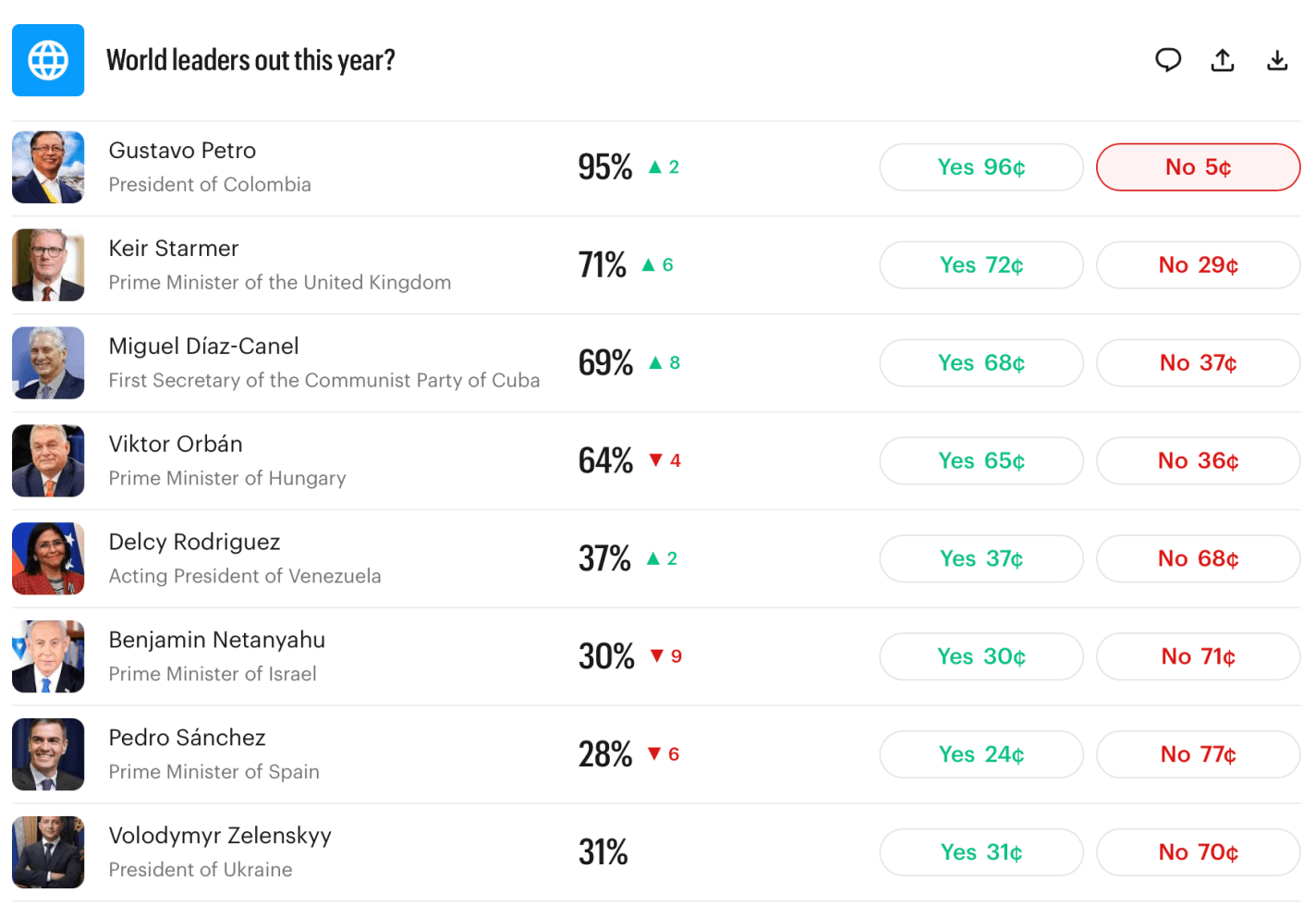

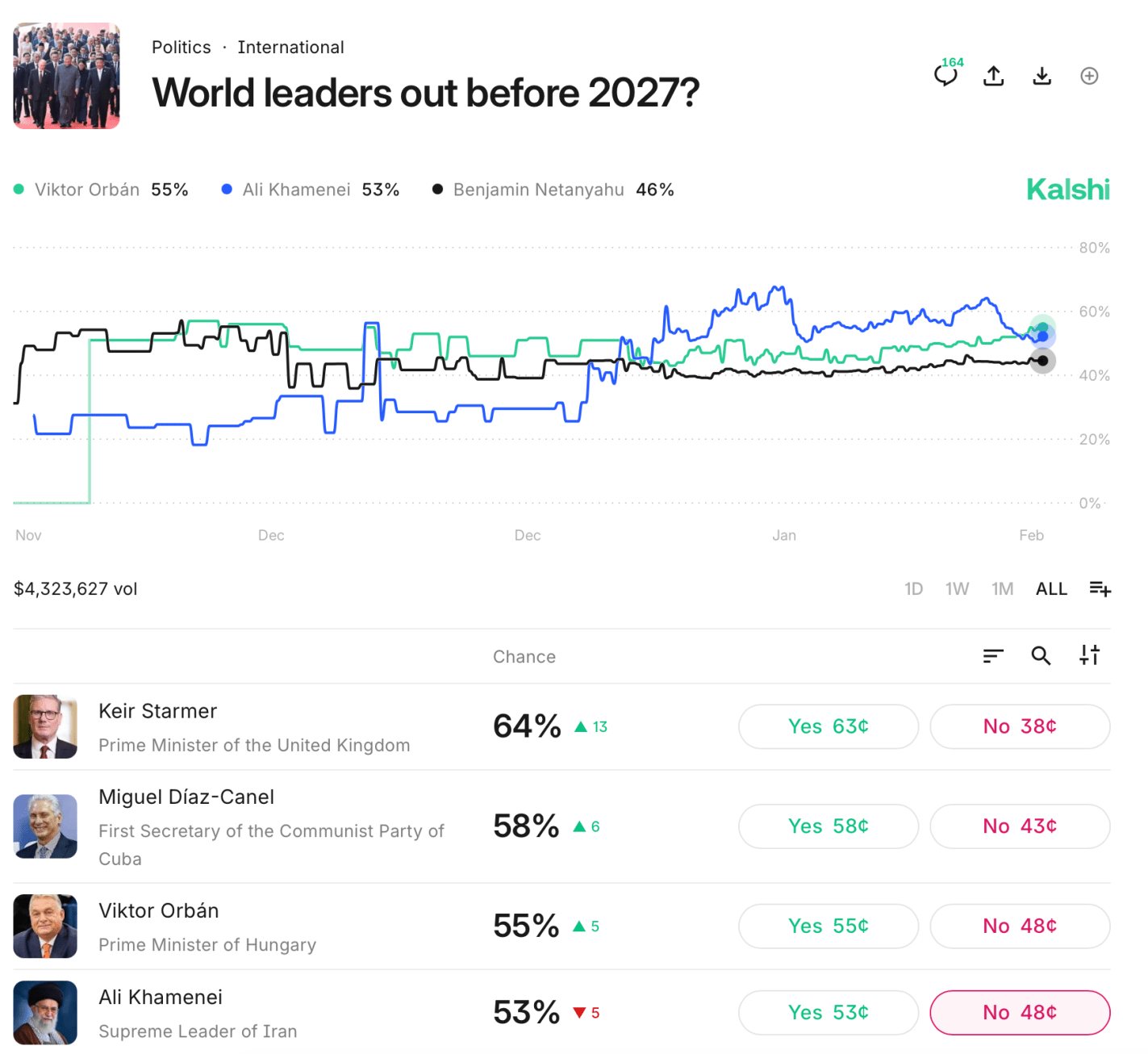

Iran is far from the only country whose future leadership is unclear. Last month I noted that the current leaders of Britain, Hungary, and Cuba would likely be out of office by year end. These are all now looking even more likely than they did a month ago:

So I’ll repeat:

Myself, I find most of these market odds to be high, and I’m tempted to make the “nothing ever happens” trade and bet that everyone stays in office. But even if all these markets are 10pp high, it still implies quite an eventful year ahead. Prepare accordingly.

US-regulated exchanges can’t offer markets on death. Kalshi’s rules stated that if Khamenei died, the market would refund everyone at current prices rather than paying as if he were “out of office”. When he died many people got mad at Kalshi- some who had bet he’d be “out of office” and were mad that they weren’t paid at 100%, others that Kalshi was offering something too close to a death market- “how else would he lose power” (even though Maduro and Assad provide clear recent examples) ↩︎

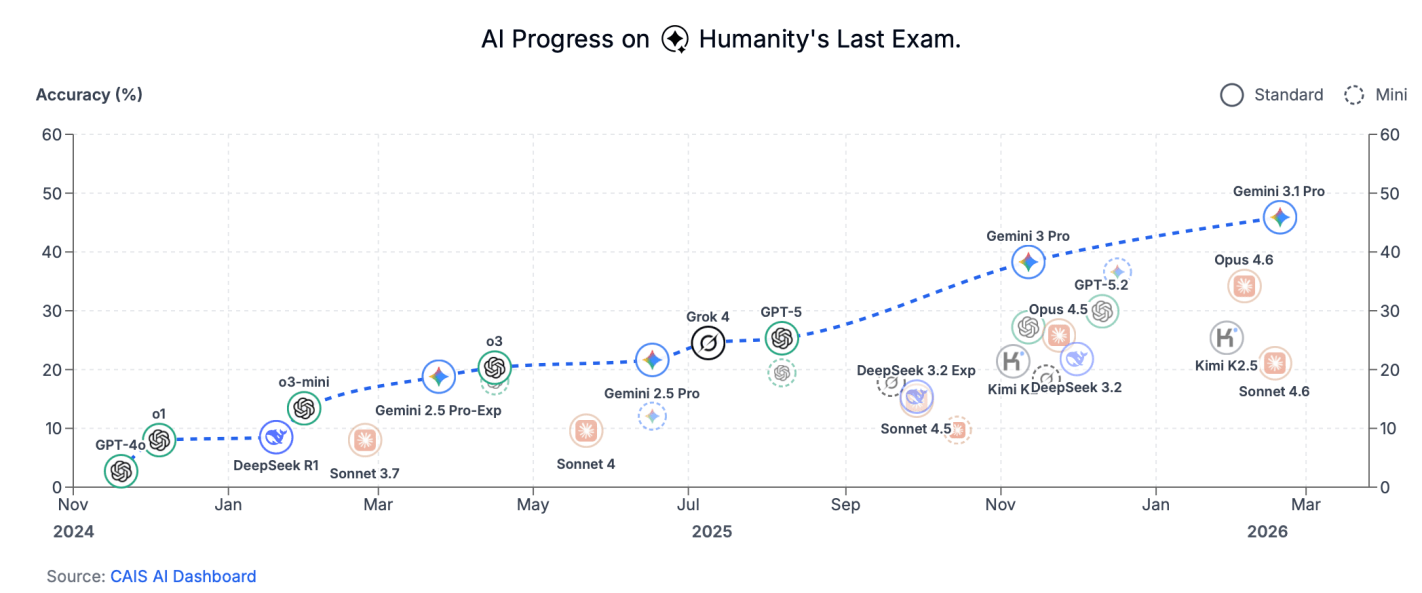

Last July I wrote here about “Humanity’s Last Exam”:

When every frontier AI model can pass your tests, how do you figure out which model is best? You write a harder test.

That was the idea behind Humanity’s Last Exam, an effort by Scale AI and the Center for AI Safety to develop a large database of PhD-level questions that the best AI models still get wrong.

One the one hand, it makes sense that the core author groups at the Center for AI Safety and Scale AI didn’t keep every coauthor in the loop, given that there were hundreds of us. On the other hand, I’m part of a different academic mega-project that currently is keeping hundreds of coauthors in the loop as it works its way through Nature. On the third, invisible hand, I’m never going to complain if any of my coauthors gets something of ours published in Nature when I’d assumed it would remain a permanent working paper.

What do we do when it can answer all the questions we already know the answer to? We start asking it questions we don’t know the answer to. How do you cure cancer? What is the answer to life, the universe, and everything? When will Jesus return, and how long until a million people are convinced he’s returned as an AI? Where is Ayatollah Khamenei right now?

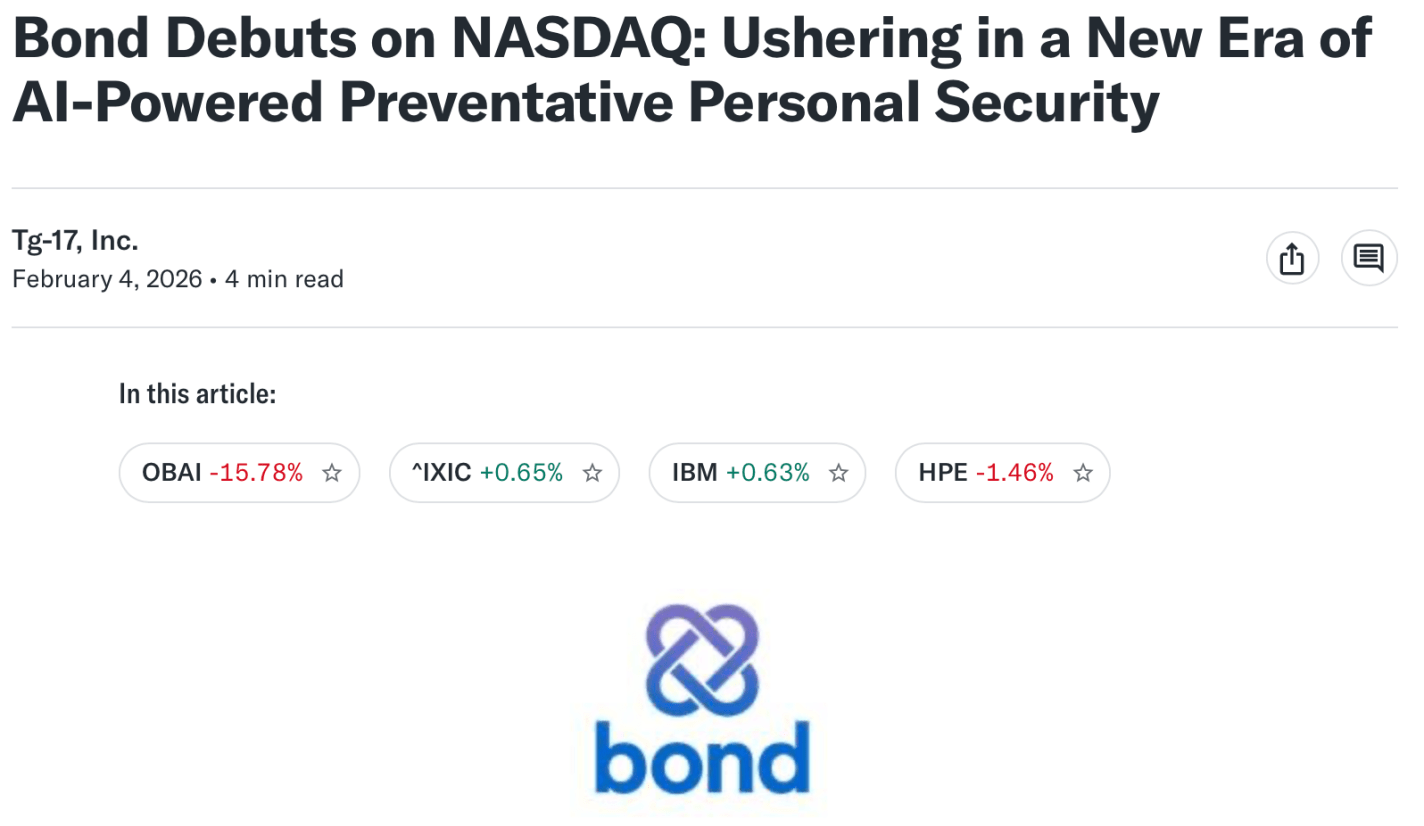

I invested in my first private company in 2022; my first opportunity to cash out of a private investment came this year when Our Bond did an IPO, now trading on Nasdaq as OBAI.

I’m happy to get a profitable exit less than 4 years after my first investment, given that I’m investing in early-stage companies. Venture funds tend to run for 10 years to give their companies time to IPO or get acquired, and WeFunder (the private investment platform I used) says that “On average, companies on Wefunder that earn a return take around 7 years to do so.” The speed here is especially striking given that I didn’t invest in Our Bond itself until April 2025.

Most private companies that raise money from individual investors are very early stage, what venture capitalists would call “pre-seed” or “seed-stage” companies looking for angel investors. Later-stage companies often find it simpler to raise their later stages (Series B, et c) from a few large institutional investors. But a few choose to do “community rounds” and allow individuals to invest later. This is what Our Bond did right before their IPO, allowing me to exit in less than a year.

This helps calm my biggest concern with equity crowdfunding- adverse selection:

The companies themselves have a better idea of how well they are doing, and the best ones might not bother with equity crowdfunding; they could probably raise more money with less hassle by going to venture funds or accredited angel investors.

My guess is that the reason some good companies bother with this is marketing. Why did Substack bother raising $7.8 million from 6000 small investors on WeFunder in 2023, when they probably could have got that much from a single VC firm like A16Z? They got the chance to explain how great their company and product is to an interested audience, and to give thousands of investors an incentive to promote the company. Getting one big check from VCs is simpler, but it doesn’t directly promote your product in the same way.

All this is enough to convince me that the equity crowdfunding model enabled by the 2012 JOBS Act will continue to grow.

Still, things could have easily gone better for me, as these markets are clearly inefficient and have complexities I’m still learning to navigate. Profitability is not just about choosing the right companies to invest in, but about managing exits. I expected the typical IPO roadshow would give me months of heads-up, but Our Bond surprised its investors with a direct listing. The first thing I heard about the IPO was a February 4th email from “VStockTransfer” that I thought was a scam at first, since it was a 3rd-party company I’d never heard of asking me to pay them money to access my shares. But Our Bond confirmed it was real- VStockTransfer was the custodian for the private shares, and charges $120 to “DRS transfer” them to a brokerage of your choice where they can be sold.

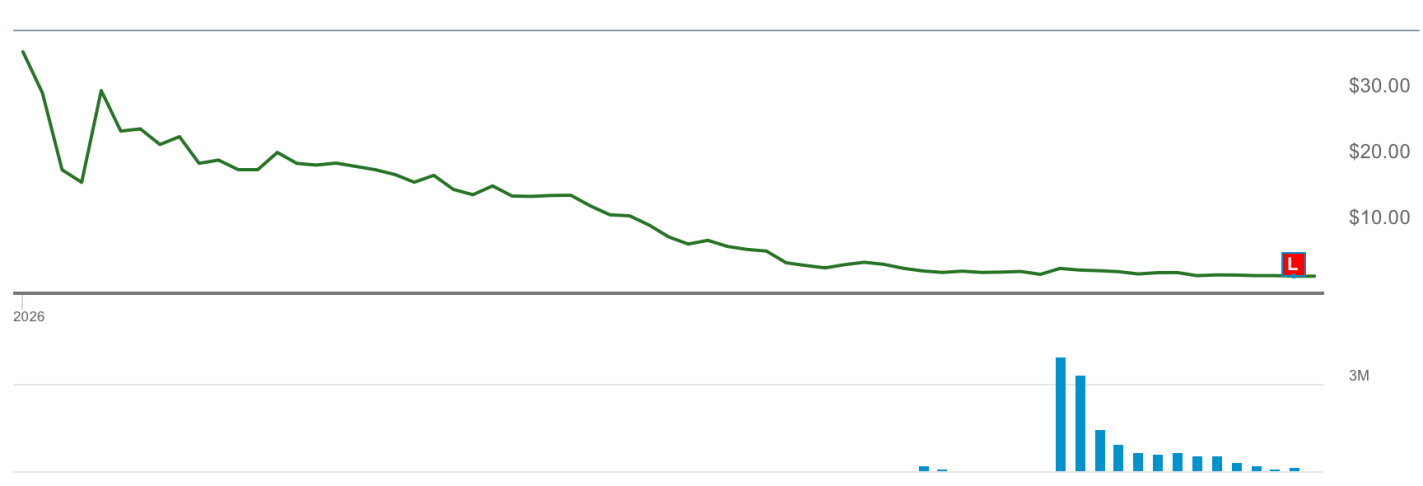

I submitted the request to move the shares to Schwab the same day, but Schwab estimated it would take a week to move them. Neither Schwab nor VStockTransfer ever sent me a notification that the shares had been transferred, and by the time I noticed they had moved a week later, the stock price had fallen dramatically:

As I write this on February 18th, the OBAI price represents a 1.3x return on the price I invested in the private company at last April. When I was first able to sell some stock on February 11th, the price represented a 3x return; if I’d been able to sell right away on the 4th without waiting for the brokerage transfer process, it would have been a 10x return.

By the Efficient Market Hypothesis this timing shouldn’t be so critical, but I knew there would be a rush for the exits as lots of private investors would want to unload their shares at the first opportunity, an opportunity some would have waited years for. Sometimes old-fashioned supply and demand analysis is a better guide to markets than the EMH: demand for OBAI stock had no big reason to change in February, but freely floating supply saw a big increase as private shares got unlocked and moved to brokerages.

Getting a 10x return vs a 1.3x return on one of your winners is the difference between a great early investor and a bad one. I always thought such differences would be driven by who picks the best companies to invest in, but at least in this case it could be driven by who is fastest on the draw with brokerage transfers.

If I ever find myself holding shares in another company that does a direct listing, I’ll be doing whatever I can to make sure the transfer goes as fast as possible (pick the fastest brokerage, check on the transfer status every day, et c). This process also seems like one reason to do fewer, larger private investments- a fixed $120 transfer fee is a big deal if the initial investment was in the low hundreds but wouldn’t matter much for a larger one.

Being accredited would help there, allowing access to additional later-stage, less-risky companies. But I’ll call OBAI a win for equity crowdfunding, and a big win for asset pricing theories based on liquidity and flows over efficient estimation of the present discounted value of future cashflows.

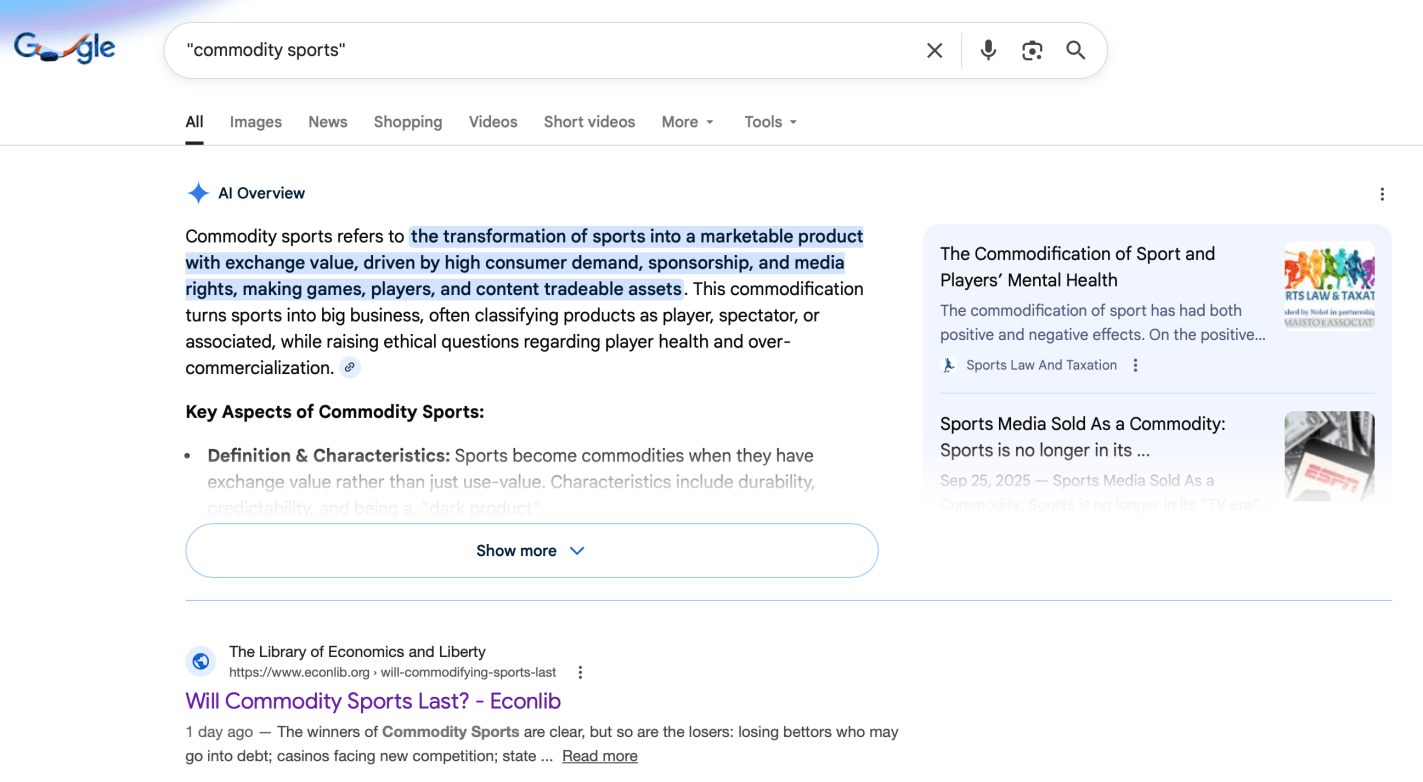

I’m trying to coin “Commodity Sports” as the term to refer to sports betting that takes place on exchanges regulated by the US Commodity Futures Trading Commission, as opposed to sports betting that takes place through casinos regulated by state gaming commissions. So far it seems to be working alright, I haven’t convinced Gemini but have got the top spot in traditional Google search:

That article- Will Commodity Sports Last?– is my first at EconLog. I’m happy to get a piece onto one of the oldest economics blogs, one where I was reading Arnold Kling’s takes on the Great Recession in real time, where I was introduced to Bryan Caplan’s writing before I read his books, and where Scott Sumner wrote for many years (though I started reading him at The Money Illusion before that).

The key idea of the piece, other than the legal oddity of sports betting sharing a legal category with corn futures, is that the Commodity Sports category is being pioneered by prediction markets like Kalshi. As readers here will know, I like prediction markets:

I love that CFTC-regulated exchanges like Kalshi and Polymarket are bringing prediction markets to the mainstream. The true value of prediction markets is to aggregate information dispersed across the world into a single number that represents the most accurate forecast of the future.

But I’m not so excited to see them expanding into sports:

Although I see huge value in prediction markets when they are offering more accurate forecasts on important issues that help policymakers, businesses, and individuals make more informed plans for our future (e.g., Which world leaders will leave office this year?, or Which countries will have a recession?)… I see much less value in having a more accurate forecast of how many receptions Jaxon Smith-Njigba will have.

Like Robin Hanson, I worry that the legal battles against Commodity Sports and the brewing cultural backlash against sports betting risk taking the most informative prediction markets down along with it.

May you live in interesting times – apocryphal Chinese curse

In early 2025 I shared forecasts about the economy that turned out to be pretty good. This year, economic forecasts center around a boringly decent year (2.6% GDP growth, inflation below 3%, unemployment stays below 5%, no recession), though with high variance. But forecasts about politics and war foretell a turbulent year.

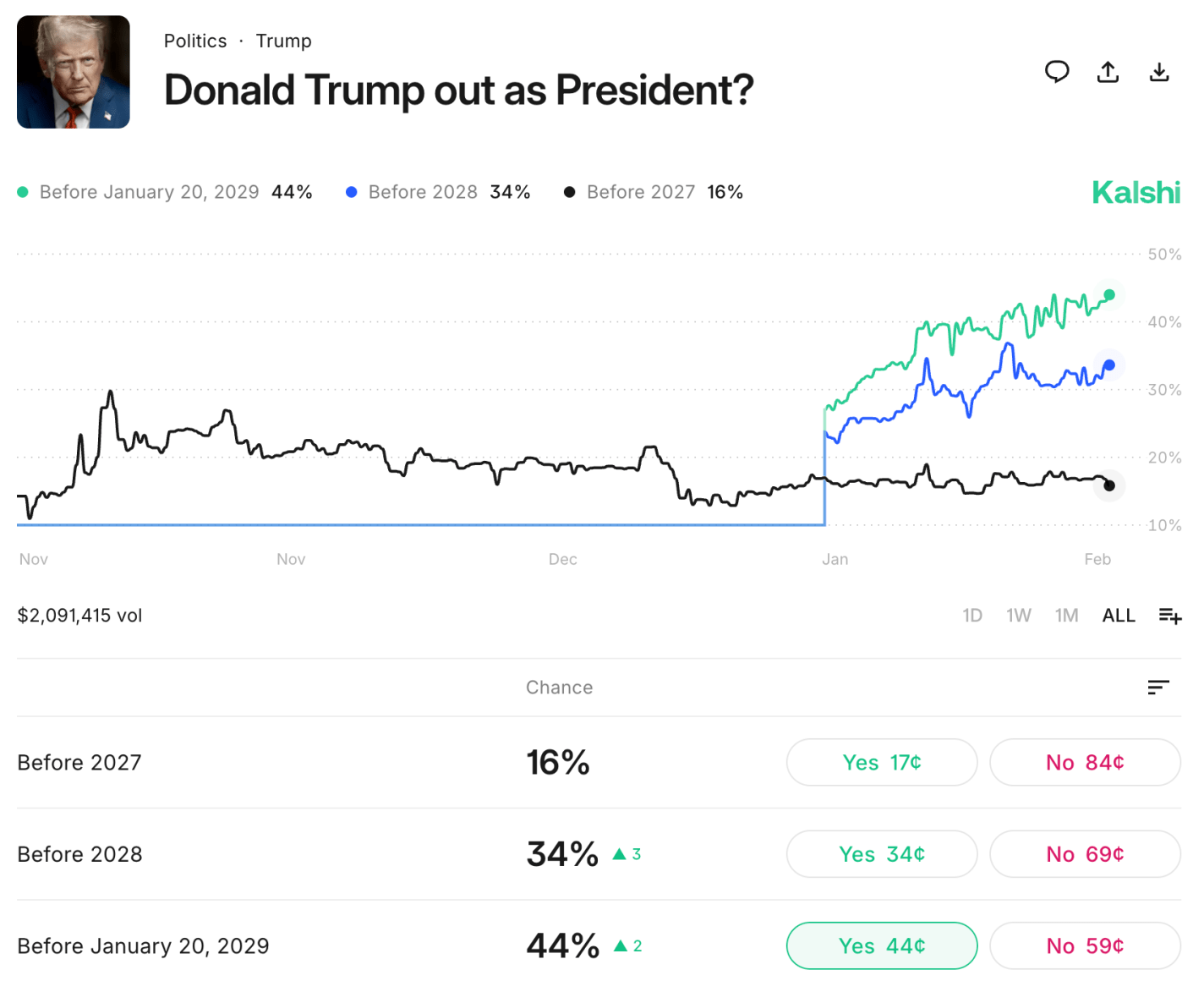

In the US, midterm elections have a 78% chance to flip control of the House and 35% chance to flip the Senate despite a tough map for Democrats. A midterm wave for the out-of-power party is typical in the US, given that the party in power always seems to over-play their hand and voters quickly get sick them. More surprising is that forecasters give a 44% chance that Donald Trump leaves office before his term is up, and a 16% chance that he leaves office this year. Markets give a 20% chance that he will be removed from office through the impeachment process, so the rest of the 44% would be from health issues or voluntary resignation.

Forecasters at Kalshi predict a greater than even chance that 4 notable world leaders leave office this year:

I find this especially notable because Viktor Orban is the only one who would be removed through regularly scheduled elections. In the UK, Keir Starmer was just elected Prime Minister in 2024 and doesn’t have to face reelection until 2029; but he is so unpopular that his own Labor Party is likely to kick him out of office if local elections in May go as badly as polls indicate. If so, he would join Boris Johnson and Liz Truss as the third British PM in four years to leave office without directly losing an election. The leaders of Cuba and Iran don’t face real elections and would presumably be pushed out by a popular uprising orUS military action.

Some other important world leaders will probably stay in office this year, but forecasters still think there is a significant chance they leave: Israel’s Netanyahu (49%), Ukraine’s Zelenskyy (32%), and Russia’s Putin (14%). For the latter two, this belief could be tied to the surprisingly high odds given to a ceasefire in the Russia-Ukraine war this year (45%). Orban leaving office could be tied into this, as Hungary has often vetoed EU support for Ukraine.

Myself, I find most of these market odds to be high, and I’m tempted to make the “nothing ever happens” trade and bet that everyone stays in office. But even if all these markets are 10pp high, it still implies quite an eventful year ahead. Prepare accordingly.

The Wealth Ladder is a 2025 personal finance book from data blogger Nick Maggiulli. The core idea is good: that the best financial strategies will be different based on your current wealth level. Maggiulli divides people into 6 net worth levels based on orders of magnitude, from less than $10K to over $100M. The middle of the book has separate chapters with advice for people in each level, so a book that is already a fairly quick and easy read as a whole could be even quicker if you skipped the chapters about levels other than your own.

The beginning of the book tries to develop some simple rules phrased in a way that they can apply across every level, because they are based on a percentage of your net worth. I like the idea but don’t think it really worked. His “1% Rule” says you should only accept an opportunity to earn money if it will increase your net worth by at least 1%. But in practice, whether an earning opportunity is worth your time depends less on how many absolute dollars in generates as a % of your net worth, and more on how many $ per hour it generates. The “0.01% Rule” (don’t worry about spending money on anything that costs less than 0.01% of your net worth) is better. But whether it is a good rule for you will depend on your age and income.

In short, while tailoring his advice in 6 different ways for the 6 wealth levels of his ladder is an improvement on one-size-fits all personal finance books, even this much tailoring isn’t enough. Having a $1 million net worth is normal for a household in their 60s but would be exceptional for one in their 20’s; and vice-versa for a household with under $10k net worth. Chapter 10 explains the data on this well, but it kind of undermines the ideas of the previous chapters. Households with the same net worth should be making very different decisions in their 20s vs 60s.

The strongest part of the book is the use of data from the Survey of Consumer Finances and the Panel Study of Income Dynamics to show how people differ by wealth level and how people move from one level to another. For instance, he shows that the poor have most of their wealth in cash and vehicles; the middle class in homes; the wealthy in retirement accounts and stocks; the very rich in private businesses. Americans tend to climb the wealth ladder slowly but steadily; over 10 years they are twice as likely to move up the ladder as to move down; over 20 years, 3 times as likely. The median person who made it to one of the top 3 rings (i.e. the median millionaire) is in their 60s.

If you get ahold of a copy of the book it’s definitely worthwhile to flip through all the tables and figures, but I won’t be adding to to my short list of the best personal finance books. The core metaphor of the ladder carriers the implicit assumption that everyone should be trying to get to the top of the ladder. But if someone is satisfied with less than $10 million, why should they take on lots of time and effort and risk to start a business for a small chance to go over $100 million?

The title is excellent, given that the author Brad Jacobs did in fact make a few billion dollars.

The book itself is fine to read, but also fine to skip if you aren’t yourself burning to build a billion dollar company through excellent management and mergers and acquisitions. I certainly don’t care to, which Jacobs says would make me a bad hire for one of his companies:

I only hire people who are motivated to make a lot of money…. If an candidate says to me ‘I’m not motivated by money’, I suspect either they’re not being candid or they lack the hunger that’s necessary to succeed

The book has plenty of hard-driving sentiments like this that you’d expect from a self-made billionaire:

Fire C players

For the first time ever, an American company, Exxon, had reported quarterly earnings in excess of $1 billion. The words “obscene profits” flashed on my TV screen, and I remember thinking “That sounds pretty good! Maybe I ought to check out the oil sector.” [This part I agree with, economic theory predicts that entrepreneurs will enter the sectors with the highest profits and its what I’d do if I wanted to make money, though in practice I think it is surprisingly rare for would-be entrepreneurs to choose this way -JB]

“The CEO trait most closely correlated with organizational success is high IQ” [specifically more important than EQ]

But Jacobs balances these ideas with some surprisingly hippy-like attitudes. Jacobs went to Bennington College and almost had a career as a jazz keyboardist. Chapter 1 is titled “How to Rearrange Your Brain”, and emphasizes the importance of meditation. Page 21 is basically “have you ever really looked at your hands, man… do it, it’s a trip”

I don’t want to spend even one hour around people who are unkind. An organization is like a party. You only want to invite people who bring the vibe up

Though perhaps this hippy/anti-hippy balance shouldn’t be surprising for someone who says one of the main things he asks about potential hires is “can this person think dialectically”.

Strongly recommend the book if you want to follow Jacobs’ path; weakly recommend it as a general management/self-help book or way to learn about markets.

Even before Elon Musk gutted X’s content moderation, James Bailey was tired of the shouting. “It’s like a cursed artifact that gives you great power to keep up with what’s going on, but at the cost of subtly corrupting your soul,” said the 38-year-old Providence College economics professor.

He retreated. This year, he realized he was spending five to 10 minutes a day on a site he used to ignore.

The WSJ reporter contacted me after seeing my previous post about LinkedIn here, explaining how I think LinkedIn has improved as a way to share and read articles, and was always good as a way to keep up with former students. Just in the short time since the WSJ article came out, I finally used LinkedIn for one of its official purposes, hiring, where it worked wonders helping to fill a last-minute vacancy.

If you don’t trust me or the WSJ to identify the hot social network, lets see what the actual cool kids are up to