Corporations raise money in various ways to invest in their operation. A company may sell common stock to the public; the shareholders are not guaranteed any particular return on their investment, but if the company does well, the share price and the dividends paid by the stock can be expected to go up.

Preferred stock falls in between common stock and bonds. Investors mainly buy preferred stock for its dividends. Typically, the price of the preferred stock doesn’t go up like common stock can, but the company cannot pay any dividends on the common unless all of the promised dividends on the preferred are paid up.

CORPORATE BONDS: INVESTMENT GRADE AND JUNK

Companies can sell bonds to raise money. Bonds are somewhat standardized securities, which are marketed to the broad investing community. The company is legally bound to pay the interest, and eventually the principal, of a bond. Bonds are senior to stocks in case of extracting value from a company that has gone bankrupt. Some bonds are more senior than others, depending on the “covenants” in the fine print of the bond description (debenture). For smaller, less stable companies, the only way they may get someone to buy their bonds is to agree to certain conditions that make it more likely the bond will be repaid. For instance, the company selling the bond might be restricted from issuing more than a certain amount of total debt relative to its earnings, or from taking on additional debt which might be senior to its existing debt.

Bonds are rated by agencies such as Moody’s and Standard and Poor’s. Large, stable companies get high ratings (e.g. AA), and can pay lower interest. You, the public, can buy into investment grade bonds through funds such as iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD). This fund currently pays about 2.6%, but most of the returns in the past several years have been from an increase in the price of the fund shares. (For longer term bonds, the market price of a previously-issued bond increases as market interest falls, which it has in recent years).

The lowest investment grade is BBB. The bonds of shakier companies are rated at BB or lower, and have pay higher interest. This is called high yield debt or junk bonds. You can invest in junk bonds through funds such as JNK and HYG.

CORPORATE BANK LOANS

Companies also obtain loans from banks. Banks scrutinize the operations of the company to decide whether they want to risk their money in making a loan. Banks usually demand restrictions and guarantees to help ensure the loan will paid back. These restrictions are called covenants. Sometimes the payback of the loan is tied to a specified asset. For instance, if the income of a company falls below a certain level (which might imperil paying off the loan), the covenant may require the company to give ownership of some asset, like a building or a set of oil wells, to the bank, so the bank can sell it to pay back the loan immediately, before economic conditions worsen.

This graphic shows some of the conditions a company might have to sign to in order to get a loan from a bank:

Here is a summary of the differences between bonds and loans, courtesy of WallStreetMojo (slightly edited):

The main difference is that a bond is highly tradeable. If you purchase a bond, there is usually a market place where you can trade it. It means you can even sell the bond, rather than waiting for the end of the thirty years. In practice, people purchase bonds when they wish to increase their portfolio in that way. Loans tend to be the agreements between borrowers and the banks. Loans are generally non-tradeable, and the bank will be obliged to see out the entire term of the loan.

In the case of repayments, bonds tend to be only repaid in full at the maturity of the bond – e.g., 10, 20, or 30 years. With bank loans, both principal and interest are paid down during the repayment period at regular intervals (like a home mortgage).

Issuing bonds give the corporations significantly greater freedom to operate as they deem fit because it frees them from the restrictions that are often attached to the loans that are lent by the banks. Consider, for example, that lenders or the creditors often require corporates to agree to a variety of limitations, such as not to issue more debt or not to make corporate acquisitions until their loans are repaid entirely.

The rate of interest that the companies pay the bond investors is often less than the rate of interest that they would be required to pay to obtain the loan from the bank. Sometimes the interest on the loan is not a fixed percent, but “floats” with general short-term interest rates.

A bond that is traded in the market possesses a credit rating, which is issued by the credit rating agencies, which starts from investment grade to speculative grade, where investment-grade bonds are considered to be of low risk and usually have low yields. On the contrary, a loan don’t have any such concept; instead, the creditworthiness is checked by the creditor.

LEVERAGED LOANS

The rough equivalent of a junk bond in the world of corporate loans is called a “leveraged loan”. A leveraged loan is a type of loan that is extended to companies or individuals that already have considerable amounts of debt or poor credit history. Lenders consider leveraged loans to carry a higher risk of default, and so they demand higher interest on the loan. Leveraged loans and junk bonds play a key role in helping smaller or struggling companies achieve their financial goals. Leveraged loans are widely used to fund mergers and acquisitions.

Because the company itself is considered shaky, creditors typically require that the company offers some specific asset for collateral to “secure” the loan. Also, the loan is typically written to be “senior” to other debt, including bonds, in case of bankruptcy. Historically, the recovery rate for such senior secured loans has been about 80%, as compared to a recovery of about 40% for unsecured bonds, if the company goes bankrupt.

Typically, a bank would not want to take all the risk of such a loan upon itself. Therefore, for a leveraged loan, the bank arranges for a syndicate of multiple banks or other financial institutions to own pieces of the loan. You, too, can get a piece of this action by buying shares of the fund Invesco Senior Loan ETF (BKLN), which is currently yielding 3.2%.

S&P Global Market Intelligence offers a primer on leveraged loans, complete with tutorial videos. As shown below, the market for leveraged loans in the U.S. is now over $ 1 trillion:

John Steinbeck’s The Grapes of Wrathdetails the impoverished circumstances of the fictional Joad family during the Great Depression and the Dust Bowl. Initially, the Joads are tenant farmers in Oklahoma, but due to the consolidation and mechanization of agriculture during the 1920s, they are displaced from their farm and without many options. After receiving a leaflet that promises abundant jobs and housing, the family follows in the path of many of their neighbors that have already left for California in search of more opportunity. Yet the hardships continue for the Joads. The grandfather dies on the arduous trip and find that they have been misled about the availability of jobs and the conditions of the squalid camps.

According to Steinbeck, the introduction of the tractor and the power of the bank are responsible for their initial misfortunes. The tractor makes farming easier and more efficient, but leaves families without work including the Joads. In an encounter with a tractor driver, a tenant farmer without work asks, “what you doing this kind of work for—against your own people?” (pg. 25). The tractor driver is seen as treasonous because he improves his own standing while a hundred other people—his people— are left without a means to provide for their own families. But the tractor driver doesn’t revel in his improved circumstances, instead he is blunt about all of their predicaments, “crop land isn’t for little guys like us anymore” (pg.25). This assessment indicates that despite their divergent trajectories, neither the tractor driver nor the tenant farmers have any influence, but they are both pawns of a larger power. Steinbeck insinuates that both individuals—the tenant farmer and the tractor driver– is largely expendable. If the driver leaves another tractor driver would gladly accept the job; if that one left, still another one would come along. The greater enemy is the big-wigs in ‘the East’ who give orders to ‘the bank,’ who are ultimately responsible for displacing the farmers.

The increasing efficiency of agriculture and its effect on the fictional Joad family illustrates what many families have faced due to the increasing efficiency of manufacturing. For the Joads, there is a strong sense of alienation. Their family home is damaged by a tractor, the neighbors are leaving, and there is no work available. Similarly, as factories and plants that were economic drivers have shuttered in rust belt towns, other main street staples such as the barber shop, the diner, and the hardware store can’t afford to stay open. As a result, formerly vibrant communities are emptied. Individuals are faced with the reality that the relatively straight-forward path to the middle class afforded to their parents will not be the same for them as options diminish for blue-collar work. The next steps for people, specifically without a college education, may not seem clear or within reach.

The monsters outlined in the first section of The Grapes of Wrath— the bank and the tractor—could be subbed in for the current monsters in our current political and economic discourse—automation and trade. The novel picks up on some of our current anti-establishment rhetoric as individuals in ‘the East’ that run the bank profit handsomely while families such as the Joads have their lives uprooted. The bank and the people in the East create a new class of winners and losers as well. The winners in this case are the tractor drivers who can now afford to give their kids shoes for the first time; the losers are the tenant farmers who have no income for food. The income inequality between the tractor driver and the tenant farmers is a microcosm of increasing income inequality in the U.S. as a result of rapidly increasing productively for a small sector of the labor force. In Average is Over, Tyler Cowen illustrates how low-skilled laborers face a similar scenario to the tenant farmer of the 1920s: individuals who are a complement to innovative technology are richly rewarded, but unskilled labor that can be replaced by it will struggle to find work in the knowledge economy.

The Grapes of Wrath demonstrates how creative destruction brought about by innovation and technology is an enduring phenomenon. Yet the characterization of this trend in The Grapes of Wrath seems prescient given the sentiments of many Americans that computers, automation, and globalization are richly benefitting a small portion of Americans that can harness these technologies at the drastic expense of many Americans that have been automated or outsourced out of their jobs.

Hannah Florence is a student at Samford University, where she studies economics, political science, and data analytics. She is currently a Young Scholar for the American Enterprise Institute’s Initiative on Faith and Public Life. After graduation, she hopes to continue her public policy research as she begins a career in Washington, D.C.

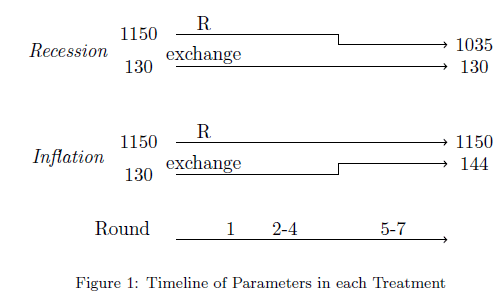

The title comes from Bewley’s famous book “Why Don’t Wages Fall During a Recession?” In that book, Truman Bewley asks managers why they do not cut wages in a recession when equilibrium analysis tells us that the price of labor should fall.

We run an experiment in which employers and workers encounter a recession. The employers could cut wages, or they could keep them rigid as we normally observe during recession. The concept of a “cut” assumes a reference point from which to go down from. We establish that reference point by letting the employer set a wage before the recession and repeating that payment to workers for 3 rounds.

We use a Gift Exchange (GE) Game to model the relationship between employers and workers. Employers offer a wage that is guaranteed to the worker. Employers have to trust that workers will not shirk. We do observe a few subjects shirking, and those people are not very interesting to us. We are interested in the workers who respond with positive reciprocity because that means there is “good morale” in the “workplace”. The employers interviewed by Bewley were afraid that wage cuts would damage the good morale that is necessary for a business to run.

After three rounds, there was a recession. The total surplus available in the GE game shrank by 10%. In the Inflation treatment, the exchange rate of tokens to dollars increased, such that if firms kept nominal wages rigid there would in fact be a 10% real wage cut.

If workers resent nominal wage cuts, then firms should keep wages rigid in a recession. If worker morale falls and workers decrease effort, then firms will be hurt more by the fall in productivity than by a large real wage cost.

In fact, about half of the firms did cut wages. So, we did not observe wage rigidity and we’d like to do follow-up research on that point. It did mean that we had variation and could observe the counterfactual that we were interested in.

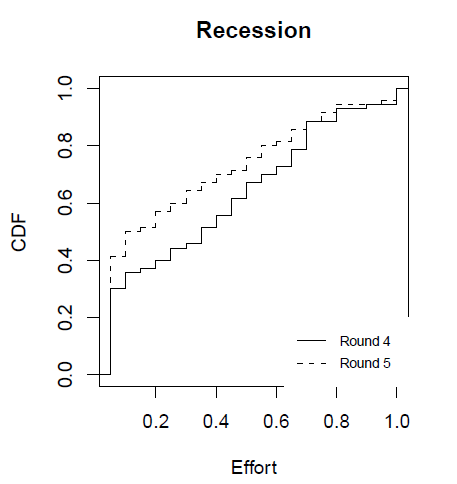

Workers don’t like wage cuts. Workers who had been selecting an effort level near the middle of the feasible range dropped their effort significantly if they experienced a wage cut. The real wage cuts under Inflation did not have as sharp of an effect on effort, which suggests some nominal illusion.

Here’s a cumulative distribution of effort choices among workers (Recession treatment had no inflation). After half of the workers experienced a wage cut, the effort distribution moves toward 0.05, the minimum effort level.

We measured loss aversion at the end. We can’t say that loss averse workers resent wage cuts, because everyone resents wage cuts. There’s maybe some evidence that loss averse employers are less likely to cut wages. Thanks for reading! Please reach out through my Samford email if you’d like to know more.

The relationship between loss aversion and wage rigidity deserves more attention from behavioral economics.

Special thanks to Misha Freer, Cesar Martinelli, and Ryan Oprea for conversations that helped us. Also, we are indebted to everyone that we cited, of course, and to all the people we failed to cite.

The big news in our world is that the Nobel Prize was announced today for economists. (We call it “the Nobel Prize”.)

Paul Milgrom and Robert Wilson win for 2020. They are known for auction theory and design. Here is a popular introduction from the Nobel Committee.

This prize is special to me because auction design was one of the very first practical problems that presented me with a chance to put economic ideas into practice. As an undergraduate at Chapman University, I had the privilege to spend time talking with people like Vernon Smith and Dave Porter. Some people think of Vernon Smith as being someone who “does things in the lab”. The thing that he actually did was often auctions.

My master’s thesis at Chapman University was a project on auctions. A practical problem to motived our inquiry. Students at Chapman were upset about the way that the most convenient parking spots were allocated. Concerns about parking showed up in quantitative student satisfaction surveys.

We designed an auction to price and allocate the most coveted parking spots. In this scenario, multiple items are being sold because the parking lot has many spots. Hence the “multi-unit” in the title of our paper Information Effects in Uniform Price Multi‐Unit Dutch Auctions.

We had an important question, since we were actually going to run an auction that would affect people’s lives. How to we choose from among the different possible auction formats?

Paul Milgrom (with Robert J. Weber) provided guidance to us in their 1982 paper in Econometrica.

Among other things, in that paper, they compare the revenue properties of English auctions and Dutch auctions. In an English auction, the price starts low and bidders compete to out-bid each other until the price is so high that only one bidder remains. That is the popular conception of an auction. There is another mechanism class (Dutch) in which the price starts higher than anyone wants to pay and drops until a buyer jumps in. Once you start thinking about how many ways one could run an auction, then you need some way to decide between all the mechanisms.

Theory can help you predict who will be better off under different formats. And, in my case, needing to figure out the revenue properties of different auction formats can help you learn economic theory!

Sometimes I remark to my students, “This is why economists don’t get invited to cocktail parties.” This post is about that.

From 2008 – 2011 I taught a course at Florida State called “Economics of Compassion”. It is a course co-designed with my mentor Mark Isaac. The class discusses historical and contemporary problems related to poverty, both at the domestic and international levels. Having heard about the course, the Social Justice Living Learning Community at Florida State wanted me to teach the course to their incoming freshman.

It was quite different from other courses they were taking that seemed to talk in terms of solutions without regard for scarcity. My role was to put parameters on their utopia and get the students to think carefully about a couple questions related to issues they care about:

Compared to what?

What happens next?

The students seemed to like the class, but, for a committed group of people who want to change the world it was also quite a downer. It was a downer for them the same way economics is a downer for people at cocktail parties.

We start with scarcity. Scarcity is a fact of life. There are never enough resources to satisfy everyone and there will always be unmet desires. For the economist, the notion of trade-offs — you must give up one thing to get another — flow from this scarcity. It means that anytime a solution to a problem is attempted you are always giving something up.

For example, the death of George Floyd this summer sparked conversation about how to reduce police violence. One approaching to curbing this important social problem is to eliminate or reform qualified immunity (QI). This is a legal doctrine intended to protect police and others from frivolous lawsuits. The problem is that QI has made accountability extremely difficult. The logic of reforming QI is that doing so will increase accountability, raise the cost of police violence, and therefore lead to less police violence. That’s good economics.

But, remember there are trade-offs. In a new world where police are opened up to lawsuits, local government might need to increase police compensation to retain or attract qualified men and women. Where does the money come from? Can you reduce the number of police and/or will you have to raise taxes? There are other trade-offs too. Will police become more reluctant to enter dangerous neighborhoods? After all, there is a greater chance that inserting themselves into a risky situation will lead to financial ruin.

Moving from heavy to light. If you haven’t seen Yoram Bauman’s comedic schtick on Principles of Economics Translated, take five minutes and check it out here. As he illustrates, “economic profit” depends on alternatives: A Snickers bar valued at one dollar with no alternative implies an economic profit of $1. However, if the alternative was M&Ms that you value at 70 cents then your economic profit is 30 cents … Your profit from pursuing one course action declines as the value of the alternative increases.

By accounting for trade-offs the net benefit of a course of action goes down. When we bring up trade-offs in conversation, economists effectively eat into people’s mental profits for some course of action.

Another thing to consider, when you’re intervening, that intervention can sometimes have dramatic side effects that you didn’t even think about. You cannot merely move people around as if they’re pieces on a chessboard (head nod to Adam Smith).

For example, it is possible that eliminating qualified immunity leads to less police violence but more neighborhood violence overall if police decide not to insert themselves into situations that could be more costly. Beyond this hypothetical example I have been using, there are loads of other unintended consequences economists talk about.

Thinking in this way is the bread and butter of economists. This is how we see the world. But, don’t try this in social settings. As EconTalk host Russ Roberts once commented (this podcast), a pleasant picnic veered into chilly company when he pointed out someone’s proposed minimum wage could have negative employment effects. The others at the picnic started to inch away from him on the picnic blanket. At parties, I’ve had people talk about the idea that a tax won’t effect them because it is only on sellers, homeowners, etc. I’ve had to ask myself, “Is it worth it to bring up that the tax is likely to be passed through?”

So while my last couple posts sing the praises of economics, I should let you know, at cocktail parties people don’t like to think about scarcity, tradeoffs, and unintended consequences. Economists like to think about the seen and unseen. Many others, especially in social settings, would rather the unseen remain unseen.

Last week I posted about Bart Wilson’s talk on his new book “The Property Species” and promised to share a class demonstration about the emergence of property rights in the classroom. But first let me tell you why I did this demonstration.

When I was a student I hated assignments that go through the motions of learning, but provide no learing. Building a paper maché volcano, while fun for some, teaches little about volcanic eruptions. Shaking and opening a soda bottle (pop?) is more instructive: it’s the fall in pressure as the bottle is opened that leads to the rapid release of the gas disolved in the liquid, the same thing happens to magma. And while being able to algebraically solve for the equilibrium price given supply and demand functions is a very necessary evil (to a point), it teaches little about the process of competition and price formation.

This is why I was reluctant to having my first Intro to Economics class write their own version of “I pencil”, quite a few years ago. Driving the point of how largely anonymous exchange and specialization, coordinated peacefully through property, prices, and profits and loss makes the modern world possible is very important. But how much can you really learn about this by watching and transcribing an episode of “How It’s Made”? For most students, not much at all. Partly in dread of reading and grading 80 versions of “I whiteboard marker”, or “I toothbrush”, and partly following my conscience I decided to throw in a twist.

The twist may seem evil and arbitrary at first. Students still had to choose a good and write their own version of “I _____” , but if two students wrote about the same good I would divide their grade by 2. If three students wrote about the same good I would divide their grade by 3 and so on. I did not give any additional prompts about how they should sort out potential conflicts or coordinate amongst themselves. These were just the rules of the assignment.

Without this seemingly arbitrary grading rule, goods to write about were not scarce. By changing the grading rules, goods to write about became scarce. While there are many more goods to write about than students, certain goods stand out in the mind, and extra effort must be devoted in thinking up a new good, and finding out if someone had already looked around their room and chosen the same good. Now students also had to coordinate amongst themselves or run the risk of a fairly severe penalty to their grade.

As expected, I have never had to enforce the the harsh grading penalties (anecdotal, I know). Students always find a way to coordinate and establish property rights over suddenly scarce goods. The point of the assignment was no longer about I pencil, but about the emergence of property rights and social coordination (and hopefully a little bit about I pencil as well). I didn’t act as a central authority that imposed and enforced property rights. I merely changed the incentives and constraints, hoping that the costs of coordinating and setting up agreements was smaller than the costs of not doing this.

When they turned in their assignment, we discussed how they had actually coordinated. Over the years I have seen multiple ingenious mechanisms. From class forums using the university platform, to a simple spreadsheet circulated amongst the students via email or WhatsApp. In the good old times before the pandemic they would sometimes meet after class and sort it out in person. Sometimes they created a common pool of goods and one of their classmates is chosen to distribute them among their peers. Leaders emerge to fill various roles from dispute resolution to registering claims. How this person is chosen also varies from class to class. Some students volunteer, others have it thrust upon themselves. The use of a homesteading rule is fairly common, first to choose gets the good in cases where there are multiple claims. In class we discuss why they use this rule, rather than last to choose gets the good, and the problems this alternative would entail.

I have only had one instance of a strong and contested dispute among “property owners”. That semester students had to not only write but present their work. Two groups (that semester “I _____” was a group assignment) wanted to do a good they thought would be amusing to present in class. I’ll leave it up to your imagination what good students in their late teens and early twenties might find to be amusing to present in class. The two groups of students underwent a rather complicated dispute resolution system with the rest of the class playing the role of arbiters of the multiple claims to the same good. Neither group wanted to budge, but one group ended up ceding the rights in the end.

What I like about this little classroom demonstration is that it makes it easier to teach the emergence of institutions as the products of human action but not human design. Order without design is a difficult concept to grasp, but maybe even more importantly it is a concept that is difficult to accept. But after this demonstration, not anymore, students experience the emergence of property rights. An added bonus is that in this case scarcity is clearly a product of the relation between their minds and how they relate to the world, not about objective quantities of goods.

I later learned of the fish game (I am not an experimentalist). But, no disrespect intended, it seems a little contrived. I still like my assignment better. While the goldfish game teaches the tragedy of the commons, the “I _____” assignment teaches how the tragedy can be solved without a centralized authority by having students solve if for themselves and come to grips with the real limitations and problems they faced, albeit on a much smaller scale. I am still hoping for an experimentalist that thinks something serious can be made out of my little classroom demonstration.

The sudden shutdown of much of the economy of the U.S. and of the world starting in February and March of 2020 led to deep concern, if not panic, in world financial markets. Millions of people were suddenly unemployed or furloughed, millions of small businesses faced bankruptcy, and stocks plunged some 30% in the fastest fall of global markets in history. Demand collapsed, and prices for nearly all financial assets fell. Trillions of dollars of financial transactions were in danger of unravelling.

The Federal Reserve immediately rode to the rescue, slashing interest rates and buying up all kinds of financial assets. These purchases of bonds and similar products injected cash into the markets to provide much-needed liquidity, and kept the system on track. In late March, the U.S. federal government authorized trillions of dollars of payments to individuals and businesses to stave off bankruptcy, and forbade foreclosures on mortgages, to keep people from losing their homes (at least in the near term). Banks and governments in other nations took similar measures. By May, it was clear that the worst scenarios had been averted, even though there will be significant lingering consequences of the Covid shutdowns.

The speed and scale of the Fed and government responses in March, 2020, may be attributed in part to learnings from the 2008-2009 Global Financial Crisis (GFC). In that crisis, the severity of the problem was not understood at first. There was naturally reluctance to take unprecedented actions to do what was perceived as bailing out of irresponsible banks and other companies. Over a period of many months, various measures were implemented to address some immediate needs, but then more and more problems kept cropping up. It was a macroeconomic game of whack-a-mole.

As a bit of a history lesson, here is a timeline of the main financial events of January-September, 2008. These descriptions are taken, with only minor editing, from an article by Kimberly Amadeo in The Balance.

Easy credit and expectations of always-increasing home prices led to a speculative run-up in housing in 2002-2006. Mortgages were given to people who really could not afford them, and billions of dollars of those unsound sub-prime mortgages were repackaged and sold into the broad financial system. That all began to unravel in 2006-2007. In response to a struggling housing market, the Federal Market Open Committee began lowering the fed funds rate. It dropped the rate to 3.5% on January 22, 2008, then to 3.0% a week later. Economic analysts thought lower rates would be enough to restore demand for homes.

February 2008: Bush Signs Tax Rebate as Home Sales Continue to Plummet

President Bush signed a tax rebate bill to help the struggling housing market. The bill increased limits for Federal Housing Administration loans and allowed Freddie Mac to repurchase jumbo loans.

February’s homes sales fell 24% year-over-year. It reached 5.03 million according to the National Association of Realtors. The median resale home price was $195,900, down 8.2% year-over-year. Foreclosures were up.

March 2008: Fed Begins Bailouts

The Fed Chair realized the Fed needed to take aggressive action. It had to prevent a more serious recession. Falling oil prices meant the Fed was not concerned about inflation. When inflation isn’t a concern, the Fed can use expansionary monetary policy. The Fed’s goal was to lower the LIBOR benchmark interest rate, and keep adjustable-rate mortgages affordable. In its role of “bank of last resort,” it became the only bank willing to lend.

It increased its Term Auction Facility program to $50 billion. It also initiated a series of term repurchase transactions. These were 28-day term repurchase agreements with primary dealers. The Fed’s goal was to pump $100 billion into the economy.

No one knew who had the bad debt or how much was out there. All buyers of debt instruments became afraid to buy and sell from each other. No one wanted to get caught with bad debt on their books. The Fed was trying to keep liquidity in the financial markets.

But the problem was not just one of liquidity, but also of solvency. Banks were playing a huge game of musical chairs, hoping that no one would get caught with more bad debt. The Fed tried to buy time by temporarily taking on the bad debt itself. It protected itself by only holding the debt for 28 days and only accepting AAA-rated debt.

March 14: The Federal Reserve held its first emergency weekend meeting in 30 years. On March 17, it announced it would guarantee Bear Stearns‘ bad loans. It wanted JP Morgan to purchase Bear and prevent bankruptcy. Bear Stearns’ had about $10 trillion in securities on its books. If it had gone under, these securities would have become worthless. That would have jeopardized the global financial system.

March 18: The Federal Open Market Committee (FOMC) lowered the fed funds rate by 0.75% to 2.25%. It had halved the interest rate in six months. That put downward pressure on the dollar, which increased oil prices.

That same day, federal regulators agreed to let Fannie Mae and Freddie Mac take on another $200 billion in subprime mortgage debt. The two government-sponsored enterprises would buy mortgages from banks. This process is known as buying on the secondary market. They then package these into mortgage-backed securities and resell them on Wall Street. All goes well if the mortgages are good, but if they turn south, then the two GSEs would be liable for the debt.

The Federal Housing Finance Board also took action. It authorized the regional Federal Home Loan Banks to take an extra $100 billion in subprime mortgage debt.The loans had to be guaranteed by Fannie and Freddie Mac.

Fed Chair Ben Bernanke and U.S. Treasury Secretary Hank Paulson thought this would take care of the problem. They underestimated how extensive the crisis had become. These bailouts only further destabilized the two mortgage giants.

April – June: Fed Lowers Rate and Buys More Toxic Bank Debt

April 30: The FOMC lowered the fed funds rate to 2%.

April 7 and April 21: The Fed added another $50 billion each through its Term Auction Facility.

May 20: The Fed auctioned another $150 billion through the Term Auction Facility.

By June 2, the Fed auctions totaled $1.2 trillion. In June, the Federal Reserve lent $225 billion through its Term Auction Facility. This temporary stop-gap measure of adding liquidity had become a permanent fixture.

July 11, 2008: IndyMac Bank Fails

July 11: The Office of Thrift Supervision closed IndyMac Bank. Los Angeles police warned angry IndyMac depositors to remain calm while they waited in line to withdraw funds from the failed bank. About 100 people worried they would lose their deposit. The Federal Deposit Insurance Corporation (FDIC) only insured amounts up to $100,000. This was later raised to $250,000.

July 23: Treasury Secretary Paulson made the Sunday talk show rounds. He explained the need for a bailout of Fannie Mae and Freddie Mac. The two agencies themselves held or guaranteed almost half of the $12 trillion of the nation’s mortgages.

Wall Street’s fears that these loans would default caused Fannie’s and Freddie’s shares to tumble. This made it more difficult for private companies to raise capital themselves. Paulson reassured talk show listeners that the banking system was solid, even though other banks might fail like IndyMac.

July 30: Congress passed the Housing and Economic Recovery Act. It gave the Treasury Department authority to guarantee as much as $25 billion in loans held by Fannie Mae and Freddie Mac.

September 7: Treasury Nationalizes Fannie and Freddie

The FHFA placed Fannie and Freddie under conservatorship. It allowed the government to run the two until they were strong enough to return to independent management.

The FHFA allowed Treasury to purchase preferred stock of the two to keep them afloat. They could also borrow from the Treasury. Last but not least, Treasury was allowed to purchase their mortgage-backed securities.

The Fannie and Freddie bailout initially cost taxpayers $187 billion. But over time, they two paid back all costs plus added $58 billion in profit to the general fund.

September 15, 2008: Lehman Brothers Bankruptcy Triggered Global Panic

Paulson urged Lehman Brothers to find a buyer. Only two banks were interested: Bank of America and British Barclays.

Bank of America didn’t want a loan. It wanted the government to cover $65 billion to $70 billion in anticipated losses. Paulson said no. The U.S. Treasury had no legal authority to invest capital in Lehman Brothers, as Congress hadn’t yet authorized the Troubled Asset Relief Program. Barclays announced its British regulators would not approve a Lehman Brothers deal.

Since Lehman Brothers was an investment bank, the government could not nationalize it like it did government enterprises Fannie Mae and Freddie Mac. For that same reason, no federal regulator, like the FDIC, could take it over. Moreover, the Fed couldn’t guarantee a loan as it did with Bear Stearns. Lehman Brothers didn’t have enough assets to secure one.

When Lehman’s declared bankruptcy, financial markets reeled. The Dow fell 504 points, its worst decline in seven years. U.S. Treasury bond prices rose as investors fled to their relative safety. Oil prices tanked.

Later that day, Bank of America announced it would purchase struggling Merrill Lynch for $50 billion.

September 16, 2008: Fed Buys AIG for $85 Billion

The American International Group Inc. turned to the Federal Reserve for emergency funding. The company had insured trillions of dollars of mortgages throughout the world. If it had fallen, so would the global banking system. Bernanke said that this bailout made him angrier than anything else. AIG took risks with cash from supposedly ultra-safe insurance policies. It used it to boost profits by offering unregulated credit default swaps.

October 8, 2008: The Federal lent another $37.8 billion to AIG subsidiaries in exchange for fixed-income securities.

November 10, 2008: The Fed restructured its aid package. It reduced its $85 billion loan to $60 billion. The $37.8 billion loan was repaid and terminated.The Treasury Department purchased $40 billion in AIG preferred shares. The funds allowed AIG to retire its credit default swaps rationally, stave off bankruptcy, and protect the government’s original investment.

September 17, 2008: Economy Almost Collapsed

Due to losses from Lehman’s bankruptcy, investors fled money market mutual funds. That’s where companies obtain their short-term cash.

September 16: The Reserve Primary Fund “broke the buck.” It didn’t have enough cash on hand to pay out all the redemptions that were occurring.

September 17: The attack spread. Investors withdrew a record $172 billion from their money market accounts. During a typical week, only about $7 billion is withdrawn. If it had continued, companies couldn’t get money to fund their day-to-day operations. In just a few weeks, shippers wouldn’t have had the cash to deliver food to grocery stores. We were that close to a complete collapse.

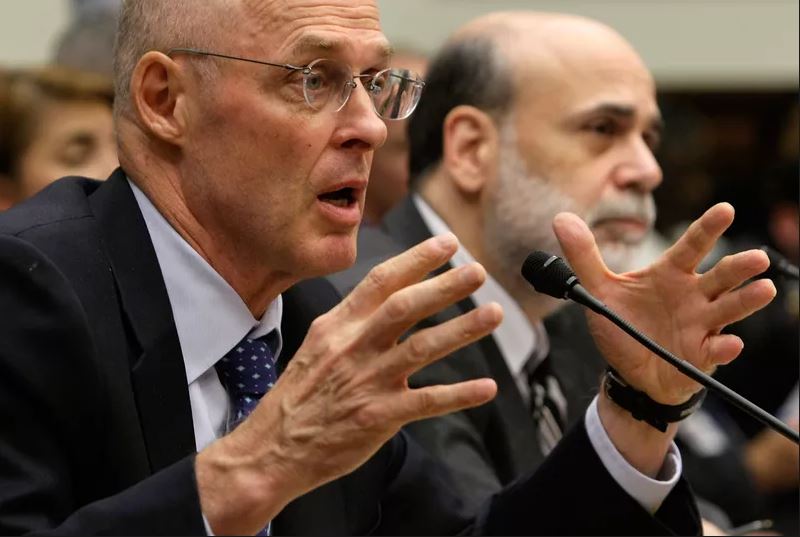

September 19, 2008: Paulson and Bernanke Meet with Congress

U.S. Treasury Secretary Henry Paulson (L) speaks as Federal Reserve Board Chairman Ben Bernanke (R) listens during a hearing before the House Financial Services Committee on Capitol Hill September 24, 2008 in Washington, DC. Photo: Alex Wong/Getty Images

September 19: Paulson and Bernanke met with Congressional leaders to explain the crisis. Republicans and Democrats alike were stunned by the somber warnings. They realized that credit markets were only a few days away from a meltdown.

The leaders were prepared to work together in a bipartisan fashion to craft a solution. But many rank-and-file members of Congress were not on board.

Bernanke announced the Fed would lend the money needed by banks and businesses to operate so they wouldn’t have to pull out the cash in money market funds. This, along with the announcement of the bailout package, calmed the markets enough keep the economy functioning.

September 20, 2008: Treasury Submits Legislation to Congress

On September 20, Paulson submitted a three-page document that asked Congress to approve a $700 billion bailout. Treasury would use the funds to buy up mortgage-backed securities that were in danger of defaulting. By doing so, Paulson wanted to take these debts off the books of banks, hedge funds, and pension funds that held them.

When asked what would happen if Congress didn’t approve the bailout, Paulson replied, “If it doesn’t pass, then heaven help us all.”

September 21, 2008: The End of the “Greed Is Good” Era

Goldman Sachs and Morgan Stanley, two of the most successful investment banks on Wall Street, applied to become regular commercial banks. They wanted the Fed’s protection.

September 26, 2008: WaMu Goes Bankrupt

Washington Mutual Bank went bankrupt when its panicked depositors withdrew $16.7 billion in 10 days. It had insufficient capital to run its business. The FDIC then took over. The bank was sold to J.P. Morgan for $1.9 billion.

September 29, 2008: Stock Market Crashes as Bailout Rejected

A trader gestures as he works on the floor of the New York Stock Exchange September 29, 2008 in New York City. U.S. stocks took a nosedive in reaction to the global credit crisis and as the U.S. House of Representatives rejected the $700 billion rescue package, 228-205. Photo by Spencer Platt/Getty Images

The stock market collapsed when the U.S. House of Representatives rejected the bailout bill. Opponents were rightly concerned that their constituents saw the bill as bailing out Wall Street at the expense of taxpayers. But they didn’t realize that the future of the global economy was at stake.

To restore financial stability, the Federal Reserve doubled its currency swaps with foreign central banks in Europe, England, and Japan to $620 billion. The governments of the world were forced to provide all the liquidity for frozen credit markets.

[Again, these descriptions are taken nearly verbatim from 2008 Financial Crisis Timeline, by Kimberly Amadeo. See her article for coverage of the rest of 2008, and the ending of the recession in 2009.]

I love the Gastropod podcast. The hosts do a great job of trying to explain the historical debates concerning food in a charitable and careful manner. Their guests also tend to be very careful.

But the guest from the September 15th, 2020 episode about beef in the US was not nearly so careful. It’s a curse, really, to listen to a great podcast, only to have a portion of an episode ruined because a guest was allowed to spout on a topic outside of their expertise.

John Specht, a history professor at Notre Dame, committed such an offense that irked the heck out of me:

“Any reform is likely to make beef more expensive. So what that means is, I think, to avoid a charge of elitism, we have to recognize that changing how we produce our food has to happen in concert with building a more just society. We need to think of ways to make people better able to afford better-produced food. And we can’t just focus on one facet of that story. We have to think holistically about that. And what that means is that this is an even bigger challenge of what already was a big challenge. But it’s also perhaps even more powerful and even more important.”

Let me first say that I have no doubts concerning Dr. Specht’s knowledge concerning the history of beef in the US. If it’s like the rest of his Gastropod interview, I look forward to reading his book and I suspect that it is stellar. But the above quote has nothing to do with history and everything to do economics, public choice, and political economy. The above quote is why I can’t take seriously many people’s claims about what the ‘good’ is and how to achieve it.

Any regulation or legislation that introduces additional requirements for beef producers will, almost certainly, increase production costs. I’m not sure what a ‘just society’ means to Dr. Specht, but I’m sure that it’s not an objective thing (knowable or not) that aids in analysis.

“We need to think of ways to make people better able to afford better-produced food.” Luckily *we* don’t need to think of that. We don’t have the local knowledge of the beef market, nor the potential markets that beef-processing laborers face as alternatives (it’s different for everyone). The age-old, classical econ answer for improving people’s real incomes is to increase their productivity. Even if the labor supply for beef processing is perfectly elastic, and all increases in productivity accrue to the firm, the result of constant wages is a *partial* equilibrium conclusion. In general equilibrium, beef processing skills are probably partial substitutes for some other labor activity. This means that skilled employees can move to other sectors, employers, and industries. *We* don’t have much say aside from policy that makes productive innovation and skill accumulation easier.

Dr. Specht makes the problem out to be worse than it is and the solution to be more difficult than it is. We don’t need to reform an entire social and economic system. We don’t need a new political system that somehow, against all incentives, reflects compassion for beef processing laborers. That’s more than government can achieve.

Government *can* get out of the way. It can ease pathways to working legally in the US, which would reduce the labor abuses in which beef firms can indulge. Legal employment alternatives increases the opportunity cost of laborers. Government can stop subsidizing cattle hydration through water subsidies to ranchers. Reducing the number of cattle, and demand for meat processing laborers would cause fewer of these workers to be employed in what many consider an unpleasant job. With perfectly elastic labor supply, there is no decrease in wages. In general equilibrium, the decline in wages is small if there are many other firms that would demand the unemployed manual labor. Further, the decline in the quantity of beef produced would make the marginal carcasses more valuable. Employers will likely desire more skilled and better-compensated labor to carve the more valuable inputs. Importantly, the better compensation comes, not from a re-orientation of societal values, rather, from the higher opportunity cost enjoyed by labor that is more skilled.

But removing subsidies and permitting more foreign-born workers aren’t the reforms that are proposed by the likes of do-gooders. Do-gooders want to feel responsible for their good. It’s not enough for them to get out of the way – no one receives praise for permitting others to engage in hard work. Typically, it’s the hard-workers who get that credit. Do-gooders mistake proactivity with good intentions. The result is a desire to employ government in activities that are doomed to failure due to imperfect design and adverse incentives. The incentives provided by markets are inadequate – not for firms, but for the people who desire a prominent role as caring managers.

I have been reading Matt Yglesias’s book. I’m going to quote his podcast with Tyler here:

I also think that a lot of the way society is structured disincentivizes educated professional people from having a second or third child, even though it’s not that the objective financial cost of doing it is so high. But you think about Democratic Party micro-targeting of everything. They’ll say, “Well, okay. If this little extra boost will help lift some people over the poverty line, we should do that. But if you’re making $140,000 a year, you don’t ‘need’ help with your childcare costs.” That’s how the people in the think tanks think.

Matt Y

On the margin, people who don’t live in poverty still feel financial pressure. They still worry about whether they can “afford” more children.

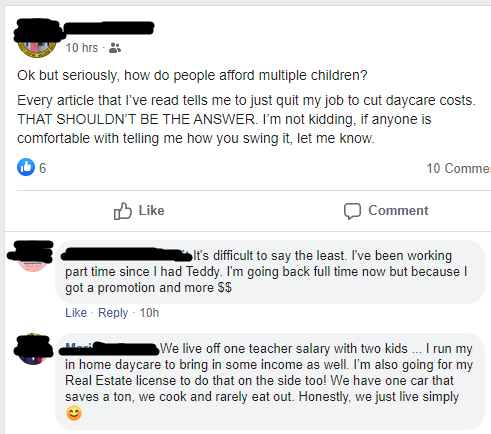

The following Facebook post stood out to me yesterday. I went to high school with this woman (call her Rachel). She teaches at a public elementary school in New Jersey. She is married with one daughter.

It sounds like Rachel wants another child, a sibling for her daughter. As a working mom, I can sympathize with her desire to not quit her job.

More answers from her peers include “I’ve been also looking for this answer. Anyone I know who has had more than one, one usually stays home and the partner works. I don’t know how people do it!” and “I have to say this month has been TERRIBLE! Paying $250 a month for my baby at daycare and then having my oldest there a few days a week bc my in-laws can’t handle zoom 😳 I’m literally working for health benefits.”

This response is probably from someone who is one stage of life ahead of Rachel, “It was hard but we lived off one salary till the kids were 5 years old. We didn’t go out or do much at all. Cost of daycare for twins was insane. Once they were in school most of the day I got my job…”

Matt Yglesias wants Rachel to have another child, and a third if she wants a “big family”. That’s not how we get to one billion Americans, it’s simply how we avoid population shrinkage.

I’ll probably deal with more of Matt’s ideas in future posts. Even if you disagree with all his policy recommendations, it’s a great book to get you thinking.

I did some quick Googling and it seems like Rachel’s job pays over $40,000 per year. It wouldn’t be crazy to assume that Rachel’s household income is “6 figures”. If their daughter is currently in daycare and they have a second child who needs daycare, then they could be looking at a daycare bill over $20,000 per year during the crunch time. That crunch time wouldn’t last very long, BUT that is a daunting bill to pay when you are also paying for rent and diapers and don’t want to eat beans every day. New Jersey has relatively high property taxes, rents, and daycare costs.

In Ecuador we bullfight with cars, literally. It’s not a game, its the name we give to the strategy we use when we cross the street. As in a bullfight, you stand on the edge of the curb, waiting for the car/bull to pass and then run behind the passing car to succesfully cross the street.

This is true no matter what the right of way legislation says (pedestrians have the right of way, de jure, in Ecuador as elsewhere), and as such is a very useful example to teach the difference between law and legistlation when talking about institutions. Although the actual phrase has fallen out of fashion lately, along with the falling popularity of bullfights (cue nostalgic music for dying traditions), the strategy remains as strong as ever.

Both pedestrians and drivers are familiar enough with the strategy that it is not uncommon to see pedestrians motioning angrily at the innocent driver that stops at a crosswalk, usually a foreigner, so that the car can pass and they can safely cross the street. Drivers speed up at crosswalks where people are waiting to cross, not in attempt to run them over, but as a courtesy, so as to get out of pedestrian’s way faster (at least many people I’ve talked to have shamefully confessed that is why they do this!). When a driver does stop at a crosswalk to give the people on the sidewalk the right of way there is a marked delay and drivers and pedestrians are incovenienced by the delay.

From conversations I have had with people from other developing nations, the strategy used by drivers and pedestrians to cross the street is nearly identical to bullfighting with cars we use in Ecuador. Although it’s not the best possible strategy for coordinating street crossing, it is an effective strategy that allows for social coordination since everyone knows that game that is being played. It is an institution of the developing world.

Moving to the US for my undergraduate degree, many years ago, I packed this institutional baggage along with me, which led me to be late for the first class of the semester. When I arrived at the crosswalk in front of a big red brick building in Boston’s suburbs, a car pulled up to the stop sign and stopped. My mind was lost thinking about what college in the US would be like, as I patiently waited at the edge of the curb for the car to pass so that I could bullfight the car to cross the street. A sudden honk of the horn startled me as I looked around to see an angry driver waving for me to cross the street. Partly because I was startled, but also because I was used to bullfighting with cars, instead of jumping out immediatly to cross, my feet began to do an akward one-step-forward one-step-back shuffle. It wasn’t until I made eye contact with the now exasperated driver, that I was confident enough I wouldn’t be run over to gathered my courage, break out of my developing-country meet developed-country shuffle, and finally cross the street.

Talking to a classmate from Central America later that day, he told me that he was all too familiar with what had happened to me, and with the one-step-forward one-step-back shuffle being discovered by tourists, immigrants, and foreing students all over the developing world. Many years later I have informally confirmed the shuffle still exists in conversations with students that have traveled abroad to the US and Europe.

When I tell this story in class, the question of how to switch to the obviously superior institutions of the US and Europe for street crossing, where pedestrians have the right of way, de jure and de facto always comes up. For institutional change to succeed without pedestrian bloodshed, the new institution would need to become common knowledge rather quickly. In more technical language, bullfighting with cars is the equilibrium now in the developing world, and we know a better equilibrium exists, but the path to the new equilibrium is difficult to traverse.

When I ask what students would do to change to this superior equilibrium, the most common first response is very economic in orientation. Increase monitoring and impose larger fines they say. But given the costs of these policies in an already poor and corrupt institutional environment, I doubt this is necesarily the path to superior institutions, for street crossing or anything else. This is especially true when we consider the relative cost effectiveness of changing this institution vs. other potential institutional investments in the developing world.

I also doubt that larger fines and increased monitoring are the main reasons that superior institutions for street crossing have emerged in the developed world. I have rarely seen police monitoring crosswalks (with the excpetion of school crossings) in the US and Europe, and while fear of punishment is definately an important influence, I don’t know how heavily the expectation of punishment weighs on the minds of drivers in developed countries.

Institutions are important for development but we know very little about how to change them. More thoughtfull students also suggest that a superior institutional arrangement could be reached by convincing people to change their perceived payoffs of playing different strategies. The hard and long process of social entrepreneurship, seems more effective and conducive to robust success.