A week ago, we described commercial loans in general, and how they differ from bonds. Companies nearly always need money to make money, and thus have to borrow money in addition to selling stock shares. Companies that are new or smaller or doing poorly or have already borrowed a lot can still get loans, but these loans typically come with stringent conditions and require paying relatively high interest. These “leveraged loans” are the loan equivalent of “junk” bonds. When a bank lends money as a “Senior Secured Loan”, this entails agreements (“covenants”) which may specify that in event of default, this loan gets paid off ahead of any other creditor, and also that some specific asset held by the company, such as a building or an oil field, will be given over to the bank.

Financial institutions like insurance companies and pension funds are hungry for “investment grade” securities like bonds rated BBB or higher. Normally, these institutions would not consider buying into the senior loan marketplace, since these instruments are not considered investment grade.

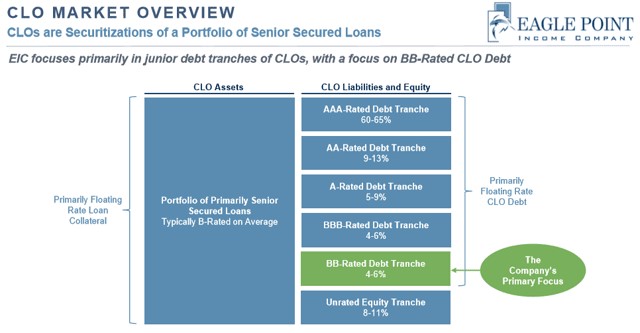

Enter “Collateralized Loan Obligations” (CLOs). With a CLO, 200 or so loans which have been made by banks and then sold off into the market are bundled together, and then the cash flow from the interest paid on these loans plus the principal paid back is repackaged into slices or “tranches”. The highest level tranches get first dibs on being paid from the overall CLO cash flow, then the lower and lower tranches. The majority of bank loans today end up being packaged into CLOs. CLOs are an example of a lucrative operation known as “securitization”: “Securitization is the process of taking an illiquid asset or group of assets and, through financial engineering, transforming it (or them) into a security” (per Investopedia).

The rate of loan defaults in recent years has been only 3-4%, and on average the recovery on a given defaulted senior secured loan has been around 80%. So the actual losses (e.g. 4% x 20%, or 0.8% net) have been quite low. The highest annual default rate in recent memory was about 10%, in the Global Financial Crisis of 2008-2009.

The theory is that, although any particular loan has a nontrivial chance of defaulting, it is unthinkable that more than say 20% of all loans would default; and even if a full 20% of the loans did default, we would expect that the actual losses after liquidating the pledged collateral would be more like 4% of the entire loan portfolio (i.e. 20% defaults x 20% loss per default). This means that the top 95% or so of CLO cash flow should be considered very secure, and the top 60-70% are utterly secure.

Thus, the top 60-65% of the CLO cash flow is packaged as super secure, relatively low-yielding AAA rated debt, and as such is bought up by conservative financial institutions, including banks. This arrangement keeps those institutions happy, and also facilitates the making of loans to the needy companies who are taking out the underlying loans.

The figure below from an Eagle Point Investment Company presentation depicts typical CLO tranches:

The lower the position in the CLO cash flow “waterfall”, the higher the yield and the higher the risk of non-payment. The AA, A, and BBB debt tranches are all considered investment grade, though with higher risk and higher yields than the AAA tranche. The Eagle Point Investment Company happens to buy into the BB-rated debt tranche, which is just below investment grade. You, the public, can buy shares Eagle Point Investment (stock symbol EIC). These shares pay about 7% yield, after hefty management fees have been subtracted.

The equity tranche lies at the very bottom of the CLO heap. If there were, say, 20% loan defaults with only 50% recovery of the loans, the equity tranche might get completely wiped out. So these are more risky investments. As usual, there is high reward along with the risk. Oxford Lane Capital (OXLC) deals in CLO equity, and it will pay you about 15% per year, which is huge in today’s low-interest world. But….you need to be prepared to have the stock value cut in half every ten years or so, whenever there is a big hiccup in the financial world.

Anyone who was an economics-savvy adult during the GFC should be asking, “But, but, but…aren’t these CLOs essentially the same thing as the collateralized debt obligations (CDOs) that blew up the world in 2008?” The answer is partly yes, in that in both cases a bunch of loans get bundled together and then resliced into tranches. That said, we hope that the underlying loans in today’s CLOs are more robust than the massively shady home mortgage loans of 2003-2008 that fed into those CDOs. Back then, unscrupulous banks and mortgage companies handed out thousands of housing loans to ill-informed private individuals who did not remotely qualify for them, and then the banks dumped these loans out into the broader financial markets via CDOs. The bank loans behind today’s CLOs are more sober, serious, vetted affairs than those ridiculous subprime home mortgages.

This past summer, in the thick of the Covid shutdowns which have stressed small businesses, The Atlantic published a dire assessment of the potential for CLOs to sink the system, with the catchy title The Looming Banks Collapse . The article noted, fairly enough, that there has been a trend in the past few years to weaken the covenants on loans which would normally protect the lender against losses. Most loans these days are considered “covenant-lite”, compared to several years ago. There is genuine concern that the recovery on these loans might be more like 40-50%, instead of the historic 70-80%. On the other hand, the looser requirements on these loans may mean that fewer of them will technically violate these looser covenants and thus fewer companies will actually default. A recent survey estimates that the default rate in the $ 1.2 trillion dollar leveraged loan universe will peak at only 6.6% in 2021.

Also, today’s CLOs seem to be rated by the major ratings agencies more responsibly than the notoriously optimistic ratings given to CDO’s back in 2008. “CLOs are usually rated by two of the three major ratings agencies and impose a series of covenant tests on collateral managers, including minimum rating, industry diversification, and maximum default basket”, according to an article by S&P Global Market Intelligence. That article has a good description of CLOs, including a brief tutorial video on the nuts and bolts of how they work.