In some quarters there is a sense that quantitative easing (QE), the massive purchase of Treasury and other bonds by the Fed, is something embarrassing or disreputable – – an admission of failure, or an enabling of profligate financial behaviors. For months, pundits have been smacking their lips in anticipation of QE-like Fed actions, so they could say, “I told you so”. In particular, folks have predicted that the Fed would try to disguise the QE-ness of their action by giving some other, more innocuous name.

Here is how liquidity analyst Michael Howell humorously put it on Dec 7:

All leave has been cancelled in the Fed’s Acronym Department. They are hurriedly working over-time, desperately trying to think up an anodyne name to dub (inevitable) future liquidity interventions in time for the upcoming FOMC meeting. They plainly cannot use the politically-charged ‘QE’. We favor the term ‘Not-QE, QE’, but odds are it will be dubbed something like ‘Bank Reverse Management Operations’ (BRMO) or ‘Treasury Market Liquidity Operations’ (TMLO). The Fed could take a leaf from China’s playbook, since her Central Bank the PBoC, now uses a long list of monetary acronyms, such as MTL, RRRs, RRPs and now ORRPs, probably to hide what policy makers are really doing.

And indeed, the Fed announced on Dec 10 that it would purchase $40 billion in T-bills in the very near term, with more purchases to follow.

But is this really (the unseemly) QE of years past? Cooler heads argue that no, it is not. Traditional QE has focused on longer-term securities (e.g. T-bonds or mortgage securities with maturities perhaps 5-10 years), in an effort to lower longer-term rates. Classically, QE was undertaken when the broader economy was in crisis, and short-term rates had already been lowered to near zero, so they could not be lowered much further.

But the current purchases are all very short-term (3 months or less). So, this is a swap of cash for almost-cash. Thus, I am on the side of those saying this is not quite QE. Almost, but not quite.

The reason given for undertaking these purchases is pretty straightforward, though it would take more time to explicate it that I want to take right now. I hope to return to this topic of system liquidity in a future post.Briefly, the whole financial system runs on constant refinancing/rolling over of debt. A key mechanism for this is the “repo” market for collateralized lending, and a key parameter for the health of that market is the level of “reserves” in the banking system. Those reserves, for various reasons, have been getting so low that the system is getting in danger of seizing up, like a machine with insufficient lubrication. These recent Fed purchases directly ease that situation. This management of short-term liquidity does differ from classic purchases of long-term securities.

The reason I am not comfortable saying robustly, “No, this is not all QE” is that the government has taken to funding its ginormous ongoing peacetime deficit with mainly short-term debt. It is that ginormous short-term debt issuance which has contributed to the liquidity squeeze. And so, these ultra-short term T-bill purchases are to some extent monetizing the deficit. Deficit monetization in theory differs from QE, at least in stated goals, but in practice the boundaries are blurry.

A black swan is a crisis that comes out of nowhere. A gray rhino, by contrast, is a problem we have known about for a long time, but can’t or won’t stop, that will at some point crash into a full-blown crisis.

The US national debt is a classic gray rhino. The problem has slowly been getting worse for 25 years, but the crisis still seems far enough off that almost no one wants to incur real costs today to solve the problem. During the 2007-2009 financial crisis and the 2020-2021 Covid pandemic we had good reasons to run deficits. But we’ve ignored the Keynesian solution of paying back the deficits incurred in bad times with surpluses in good times.

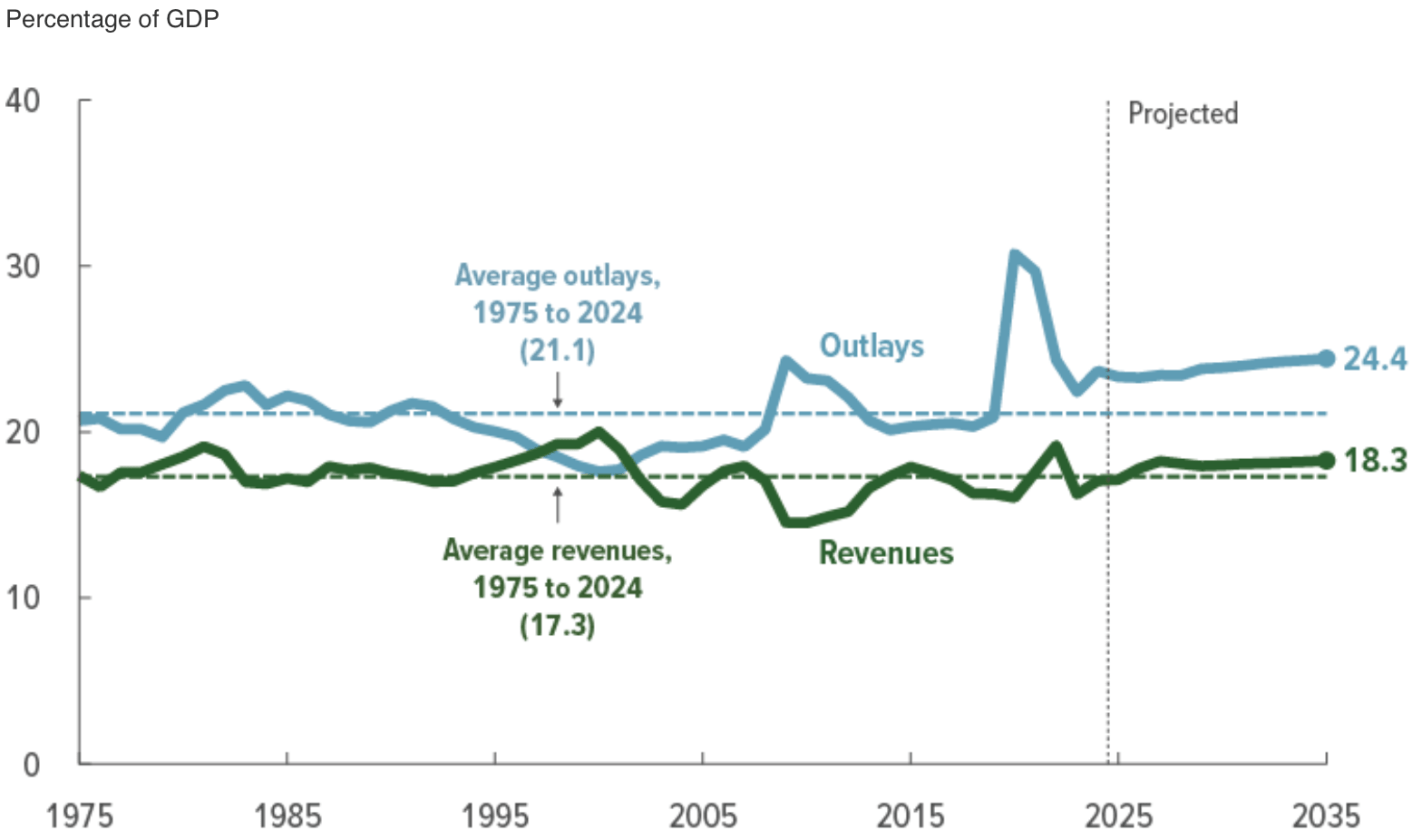

We are currently in reasonably good economic times, but about to pass a mega-spending bill that blows the deficit up from its already-too-high-levels. At a time when we should be running a surplus, we are instead running a deficit around 6% of GDP:

Source: Congressional Budget Office

Our ‘primary deficit’ is lower, a more manageable 3% of GDP. But if interest rates go higher, either for structural reasons or because of a loss of confidence in the US government’s willingness to pay its debts, the total deficit could spiral higher rapidly. The CBO optimistically assumed that the interest rate on 10-year treasuries will fall below 4% in the 2030s, from 4.3% today:

Source: Congressional Budget Office

But their scoring of H.R. 1 (“One Big Beautiful Bill Act”) shows it adding $3 trillion to the debt over the next 10 years, increasing the deficit by ~1% of GDP per year.

I already suspected this gray rhino would eventually cause a crisis, but this bill and the milieu that produced turn it into a near guarantee- nothing stops the deficit train until we hit a full blown crisis. That crisis is no longer just a long-term issue for your kids and grandkids to worry about- you will see it in 7 years or so. Unfortunately, that is still far enough away that current politicians have no incentive to take costly steps to avoid it. In fact, deficits will probably make the economy stronger for a year or two before they start making things worse- convenient for all the Congresspeople up for election in less than 2 years.

Here are the ways I see this playing out, from most to least likely:

By around 2032, either the slowly aging population or a sudden spike in interest rates forces the government to touch at least one of the third rails of American politics: cut Social Security, cut Medicare, or substantially raise taxes on the middle class (explicitly or through inflation).

We get bailed out again by God’s Special Providence for fools, drunks, and the United States of America. AI brings productivity miracles bigger than those of computers and the internet, letting GDP grow faster than our debts.

We default on the national debt (but this is a risky option because we will still want to run big deficits, and lenders will only lend if they expect to get paid back).

We do all the smart policy reforms that economists recommend in time to head off the crisis and stop the rhino. Medical spending falls without important services being cut thanks to supply-side reforms or cheap miracle drugs (GLP-1s going off patent?).

I’m hoping of course for numbers 2 and 4, but after this bill I’m expecting the rhino.

Typically, the federal government spends more than it takes in. This has been going on for decades. At moderate levels, i.e. moderate debt/GDP ratios, this is not cause for concern. Presumably the national economy will grow enough to service the debt.

Historically, deficit spending would temporarily increase during some crisis like a major recession or major war, then it quickly tapered back down again. There was a general understanding, it seems, among most voters and most politicians that huge deficits were not healthy; one would not want to burden future generations with a lot of debt.

During the 2020-2021 epidemic experience, however, politicians found they got instant popularity by handing out trillions in stimulus money; anyone who squeaked that we couldn’t afford this much largesse got run over. And this spend-big, tax-small mentality has now become entrenched. Both presidential candidates have been traversing the nation promising juicy tax cuts. Apparently, we the people have decided to vote ourselves lots of free money right now, and the heck with future generations.

Here is a forecast from the Congressional Budget Office, with the optimistic assumption that we will never get another recession, showing that the recent levels of deficit are much higher than historical norms:

This is just the yearly deficit, not the exponentially-growing accumulated debt. The influence of the total debt may be seen in the mushrooming interest outlays. Below is another chart with data from the St Louis Fed, displaying both deficit level and unemployment over the past 80 years. Again, deficit spending would ramp up during recessions, due to reduced tax revenue and increased spending on unemployment benefits, etc., but then it would ramp right back down again. It failed to come back down completely after the 2008-2009 recession, and indeed started ramping up around 2016, even with low unemployment.

I don’t see this trend changing, and so investors need to take this into account. Here I will summarize some key points from analyst Lyn Alden Schwartzer in her article on the Seeking Alpha investing site titled Why Nothing Stops The Fiscal Train.

She notes that besides the primary deficit, the interest paid on the federal debt is a transfer of money to mainly the private sector, and so is further stimulus. This is one factor that has helped keep the economy stronger, and inflation higher, than it would otherwise be.

Some key bullet points in the article are

The U.S. faces structurally high fiscal deficits driven by unbalanced Social Security, inefficient healthcare spending, foreign adventurism, accumulated debt interest, and political polarization.

Investment implications suggest favoring equities and scarce assets over bonds, with defensive positions in T-bills, gold, and inflation-protected Treasury notes.

Fiscal dominance will likely lead to persistent inflation, asset price volatility, and potential stagflation, making traditional recession indicators less reliable.

A neutral-to-negative outlook on U.S. stocks in inflation-adjusted terms, with better prospects for international equities and cyclical mid-sized U.S. stocks.

She suggests looking to the recent histories of emerging economies to see what happens in nations with perhaps stagnating real economies kept afloat by ongoing federal deficits. Her tentative five-year outlook for investing is bearish on the major U.S. stock indices (gotten overpriced) and on government bonds (real returns, in light of anticipated ongoing inflation, will be low), but bullish on international stocks, inflation-protected bonds, short-term T-bills, gold, and bitcoin (again, all mainly driven by expected stubborn inflation as the money supply keeps growing):

-For U.S. stocks, I have a neutral-to-negative view on the major U.S. stock indices in inflation-adjusted terms. They’re starting from an expensive baseline, and with a high ratio of household investable assets already stuffed into them. However, I do think that among the universe of more cyclical and/or mid-sized stocks that make up smaller portions of the U.S. indices, there are plenty of reasonably priced ones with better forward prospects.

-For international stocks, I think the 2024-2025 Fed interest rate cutting cycle is one of the first true windows for them to have a period of outperformance relative to U.S. stocks for a change. It doesn’t mean that they certainly will follow through with that, but my base case is for a meaningful asset rotation cycle to occur, with some of the underperforming international equity markets having a period of outperformance. At the very least, I would want some exposure to them in an overall portfolio, to account for that possibility.

-For developed market government bonds, like the U.S. and elsewhere, I don’t have a positive long-term outlook in terms of maintaining purchasing power. A ten-year U.S. Treasury note currently yields about 3.7%, while money supply historically grows by an average of 7% per year, and $20 trillion in net Treasury debt is expected to hit the market over the next decade. So I think the long end of the curve is a useful trading sardine, but not something I want to have passive long exposure to.

-A five-year inflation-protected Treasury note, however, pays about 1.7% above CPI, and I view that as a reasonable position for the defensive portion of a portfolio. T-bills are also useful for the defensive portion of a portfolio. They’re not my favorite assets, but there are worse assets out there than these.

-Gold remains interesting for this five-year period, although it might be tactically overbought in the near-term. It has had a nice breakout in 2024, but is still relatively under-owned by most metrics, and should benefit from the U.S. rate cutting cycle. So I’m bullish as a base case.

-Bitcoin has been highly correlated with global liquidity, and I expect that to continue. My five-year outlook on the asset is very bullish, but the volatility must be accounted for in position sizes for a given portfolio and its requirements.

I’ll add two comments on this list. First, the bond market is usually pretty good about figuring things out, and has evidently realized that endless huge deficits mean endless huge bond issuance and ongoing inflation. Thus, even though the Fed is lowering short-term rates, bond buyers have started demanding higher rates on long-term bonds. And so long-term government bonds may not be as bad as Schwartzer thinks.

Second, for reasons described in The Kalecki Profit Equation: Why Government Deficit Spending (Typically) MUST Boost Corporate Earnings, when you work through the various sectoral balances in the macro economy, most of the huge deficit spend dollars will end up in either corporate earnings or in the foreign trade deficit. So the ongoing deficits will continue to buoy up U.S. corporate earnings, and hence U.S. stock prices.

I’ve written about government spending before. But not all spending is the same. Building a bridge, buying a stapler, and taking from Peter to pay Paul are all different types of spending. I want to illustrate that last category. Anytime that the government gives money to someone without purchasing a good or service or making an interest payment, it’s called a ‘transfer’. People get excited about transfers. Social security is a transfer and so is unemployment insurance benefits. Those nice covid checks? Also transfers.

Here I’ll focus on Federal transfers, though the data on all transfers is very similar if you include states in the analysis. Let’s start with the raw numbers. Below is data on GDP, Federal spending, and federal transfers. Suffice it to say that they are bigger than they used to be. They’ve all been growing geometrically and they all exhibit bumps near recessions.

I have a list of economics topics that I like to teach about because they conflict with the biases of my average student. The list includes fiat currency, inflation, deficits, net exports, and immigration. The list also includes the importance – or lack thereof – of the federal government’s debt. This post walks through a few graphs to do a gut-check of what we think is true and how it compares to reality. For example, do you have a sense of when the debt grew historically and when it was constant? Do you have a sense for when it shrank?

Is the federal government spending at a faster rate? Your answer probably has more to do with your biases than with anything else. Most people don’t know the numbers or they imagine some more appropriate past. Below is logged current federal expenditures (this does not include government fixed investment, only consumption. Yes, we can argue about measures. This doesn’t include transfers).

The line of best fit is about 1.6% per quarter or 6.4% per year. Golly! Our spending is rising so fast! But, US federal spending grew relatively slowly in the 90s – maybe due to that fiscal conservative, Bill Clinton. And our federal spending grew even more slowly between 2010 and 2016 – maybe due to that other fiscal conservative, Barack Obama.

But, inflation varied over this period. What about real, inflation adjusted federal spending? See Below.

Last week President Biden released his Fiscal Year 2023 budget proposal. The annual release of the budget proposal is always exciting for economists that study public finance. The president’s proposal is the first step in the federal budgeting process, which in some cases leads to the full passage of a federal budget by the start of the fiscal year in October (though perhaps surprisingly, the process rarely works as intended).

This year’s budget is especially interesting to look at because it gives us our first look at what post-pandemic federal budgeting might look like. And while the budget has a lot of detail on the administration’s priorities, I like to go right to the bottom line: does the budget balance? What are total spending and revenue levels?

The bottom line in the Biden budget this year is that permanently large deficits are here to stay. Keep in mind that a budget proposal is just a proposal, but it’s reasonable to interpret it as what the president wants to see happen with the budget over the next 10 years (even if Congress might want something different). Over the next 10 years, Biden has proposed that budget deficits remain consistently right around 4.5% of GDP, with no plan to balance the budget in the near future.

How does this compare to past budget proposals? For comparison, I looked at the final budget proposals of Biden plus his two predecessors. I start Obama’s in 2021 to match Trump’s first year, and all three overlap for 2023-2026. I put these as a percent of GDP so we don’t have to worry about inflation adjustments (though we might worry about optimistic GDP forecasts, see below).

While I was listening to The New Bazaar and enjoying an episode with Tim Harford, I was reminded that economists don’t just have the job of understanding the world. We have a responsibility to our fellow man of keeping fallacy and economic misunderstanding at bay (a Sisyphean task). That doesn’t mean that we just teach economic theory. We can and should advocate for good economic policy ideas and try to think up some policy alternatives that fit our political climate.

Here I was sitting, being grumpy at the US Federal deficit, when an idea came to me. I am full of ideas. Especially unpopular ones. So, I especially like ideas that make political sense to me given that the political parties care about their policy values and re-election. Asserting that people in congress actually care about policy apart from re-election is kind of a pie-in-the-sky assertion. But, here we go none the less.

Mancur Olson liked to emphasize the role of concentrated benefits and diffused costs in political decision making. Economists point to it and explain the billion-dollar federal subsidies that go to interest groups. A favorite example is Sugar subsidies. As of 2018 there were $4 billion in subsidies and sugar growers earned $200k on average. The typical family of four pays about $50 more in subsidies each year as a result. The additional tax burden of higher sugar prices is also relatively small. Therefore, says the economist, the few sugar beet and sugar cane farmers have a large incentive to ensure the subsidy’s survival while others pay a relatively small cost to maintain it. That small cost means that there is little money saved and little gain for any individual who might try to fight the applicable legislation.

That’s the standard story. But it’s so much worse than a story of concentrated benefits and diffused costs. The laity don’t know how the world works in two important ways. First, many people will simply say that they are happy to protect American producers for an additional $50 per year. That’s a small price to pay for ensuring the employment and production of our fellow Americans, they say. An economist might reply, in a manner that so automatic that it appears smug, that that $50 would instead go to producers of other goods and that our economy would be more productive if the sugar-producing resources were diverted elsewhere. This is Bastiat’s seen and unseen. Honestly, I suspect that neither economists nor non-economists can adopt the idea without a little bit of faith.

Secondly, people don’t know what causes a particular price to change. Hayek painted this characteristic as a feature of the price system. We are able to communicate information about value and scarcity without evaluating the values of others or the actual quantity of an available resource. However, lacking causal knowledge of prices makes for some bad policies. Say that the subsidies and protections subsided and the price of US sugar declined. The consumer would likely not know anything about the subsidies in the first place, much less that they were rescinded. Further, the world is a complicated place and people are apt to thank/blame irrelevant causes otherwise (corporate greed, anyone?).

When economists blame concentrated benefits and diffused costs, they often assume that there is perfect information. THERE ISN’T. People don’t know how the world works well enough to predict with confidence what will happen in an alternate version of reality without subsidies. Nor do they understand the particular determinants of prices in our current world. Half the battle is a lack of knowledge about the functioning of the world – not just that the costs and benefits fail to provide a strong enough incentive for legislative change.