We’re bombing Iran, and Iran is now bombing most of its neighbors. Oil prices are up ~20% since the bombing began last weekend, and stocks are down.

Iranian “Supreme Leader” Khamenei is now dead. Prediction markets sort of saw this coming; I mentioned here a month ago that markets thought it more likely than not that Khamenei would be “out of office” this year.1

Real-money US-regulated exchanges can’t directly cover the war, but others can and do, such as the international Polymarket:

Polymarket’s argument for why they offer these markets

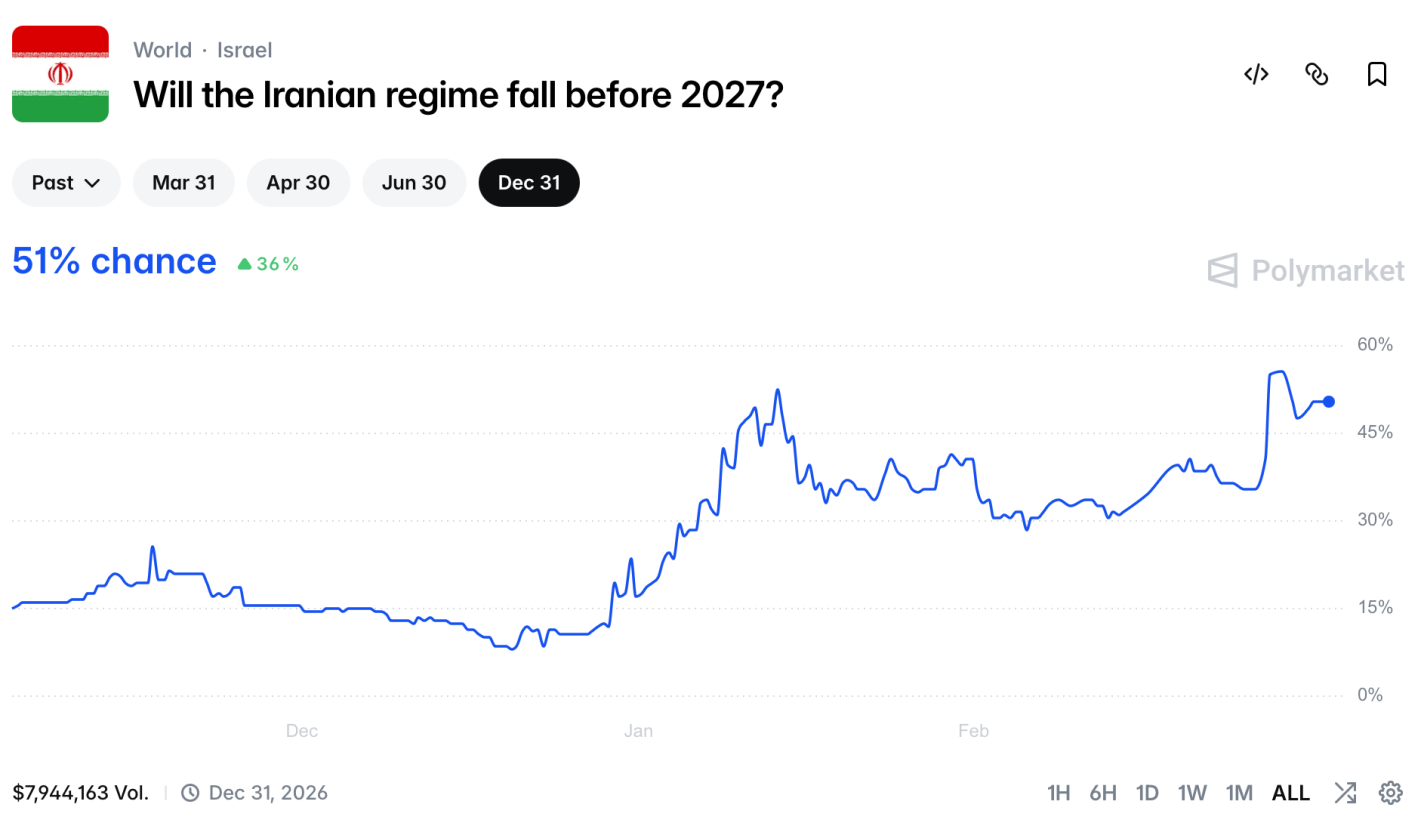

This market shows that regime change is likely, but will take time- a 51% chance by the end of the year, but only a 13% chance by the end of the month.

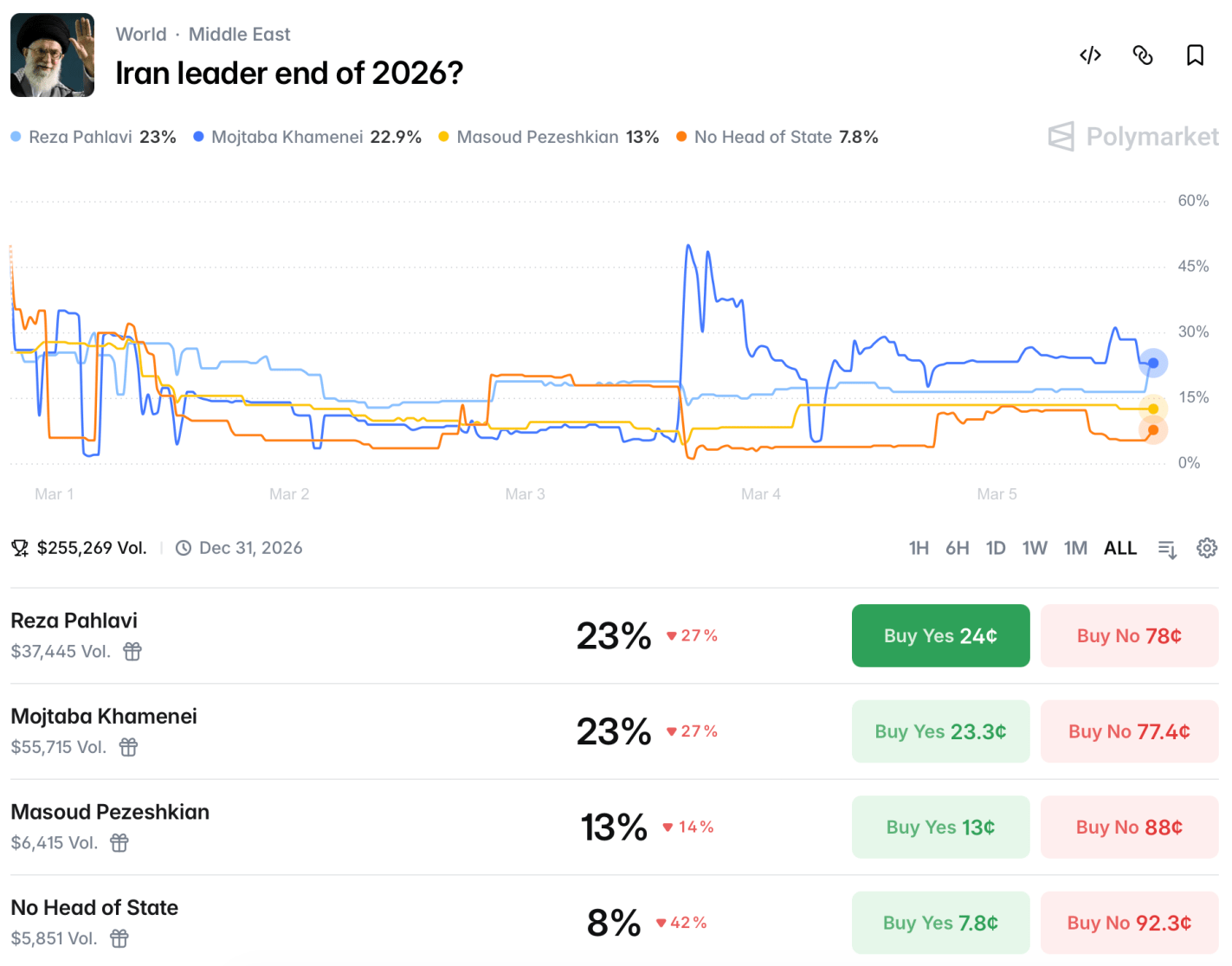

How would this be achieved? Markets see a 60% chance that there will be US troops in Iran this year, though this market could be triggered by just a few special forces operators, or by troops visiting for humanitarian purposes after domestically-driven regime change. There will likely be a US-Iran ceasefire by the end of May. It’s not clear at all who will be running Iran at the end of the year:

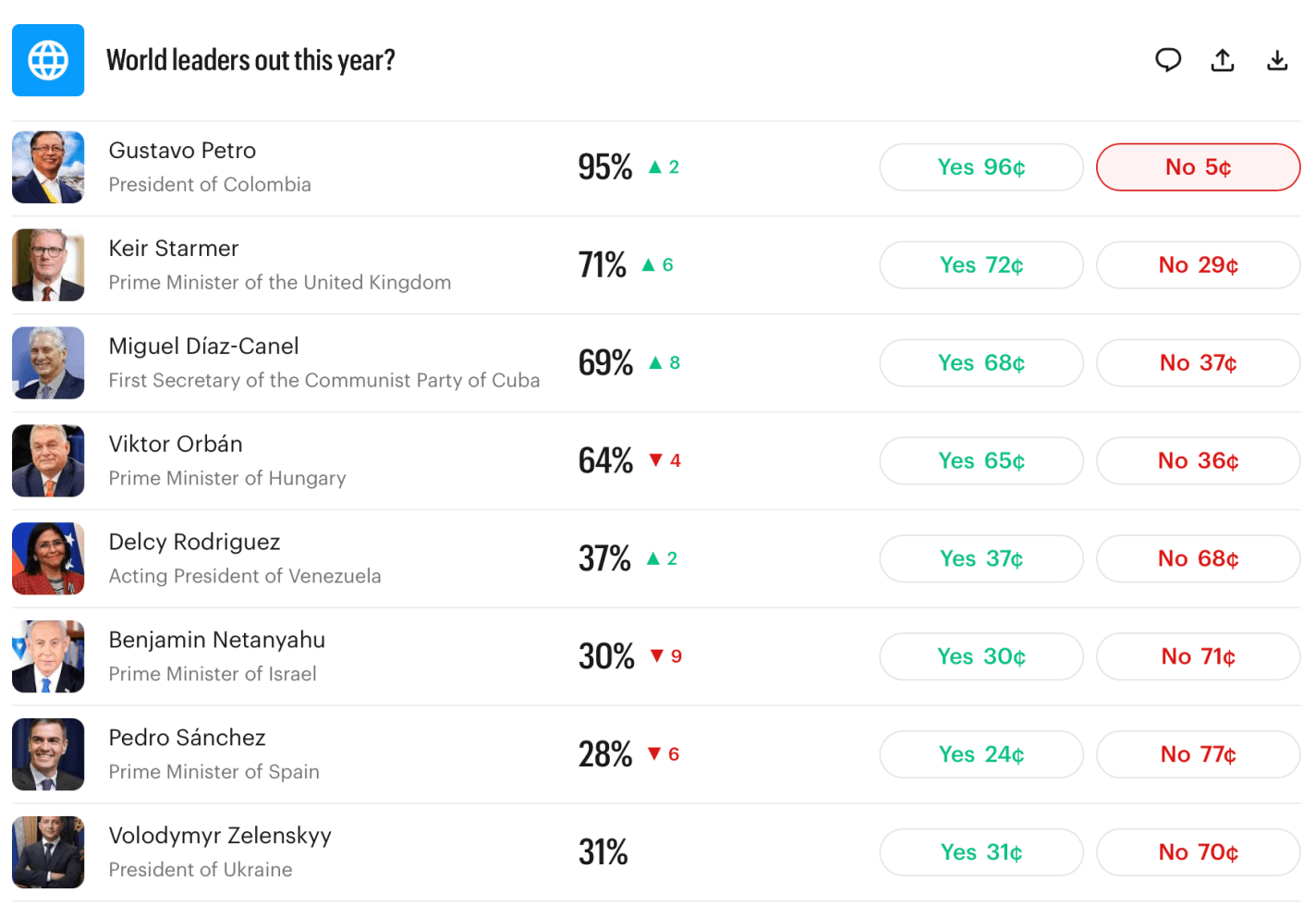

Iran is far from the only country whose future leadership is unclear. Last month I noted that the current leaders of Britain, Hungary, and Cuba would likely be out of office by year end. These are all now looking even more likely than they did a month ago:

So I’ll repeat:

Myself, I find most of these market odds to be high, and I’m tempted to make the “nothing ever happens” trade and bet that everyone stays in office. But even if all these markets are 10pp high, it still implies quite an eventful year ahead. Prepare accordingly.

US-regulated exchanges can’t offer markets on death. Kalshi’s rules stated that if Khamenei died, the market would refund everyone at current prices rather than paying as if he were “out of office”. When he died many people got mad at Kalshi- some who had bet he’d be “out of office” and were mad that they weren’t paid at 100%, others that Kalshi was offering something too close to a death market- “how else would he lose power” (even though Maduro and Assad provide clear recent examples) ↩︎

I’m trying to coin “Commodity Sports” as the term to refer to sports betting that takes place on exchanges regulated by the US Commodity Futures Trading Commission, as opposed to sports betting that takes place through casinos regulated by state gaming commissions. So far it seems to be working alright, I haven’t convinced Gemini but have got the top spot in traditional Google search:

That article- Will Commodity Sports Last?– is my first at EconLog. I’m happy to get a piece onto one of the oldest economics blogs, one where I was reading Arnold Kling’s takes on the Great Recession in real time, where I was introduced to Bryan Caplan’s writing before I read his books, and where Scott Sumner wrote for many years (though I started reading him at The Money Illusion before that).

The key idea of the piece, other than the legal oddity of sports betting sharing a legal category with corn futures, is that the Commodity Sports category is being pioneered by prediction markets like Kalshi. As readers here will know, I like prediction markets:

I love that CFTC-regulated exchanges like Kalshi and Polymarket are bringing prediction markets to the mainstream. The true value of prediction markets is to aggregate information dispersed across the world into a single number that represents the most accurate forecast of the future.

But I’m not so excited to see them expanding into sports:

Although I see huge value in prediction markets when they are offering more accurate forecasts on important issues that help policymakers, businesses, and individuals make more informed plans for our future (e.g., Which world leaders will leave office this year?, or Which countries will have a recession?)… I see much less value in having a more accurate forecast of how many receptions Jaxon Smith-Njigba will have.

Like Robin Hanson, I worry that the legal battles against Commodity Sports and the brewing cultural backlash against sports betting risk taking the most informative prediction markets down along with it.

May you live in interesting times – apocryphal Chinese curse

In early 2025 I shared forecasts about the economy that turned out to be pretty good. This year, economic forecasts center around a boringly decent year (2.6% GDP growth, inflation below 3%, unemployment stays below 5%, no recession), though with high variance. But forecasts about politics and war foretell a turbulent year.

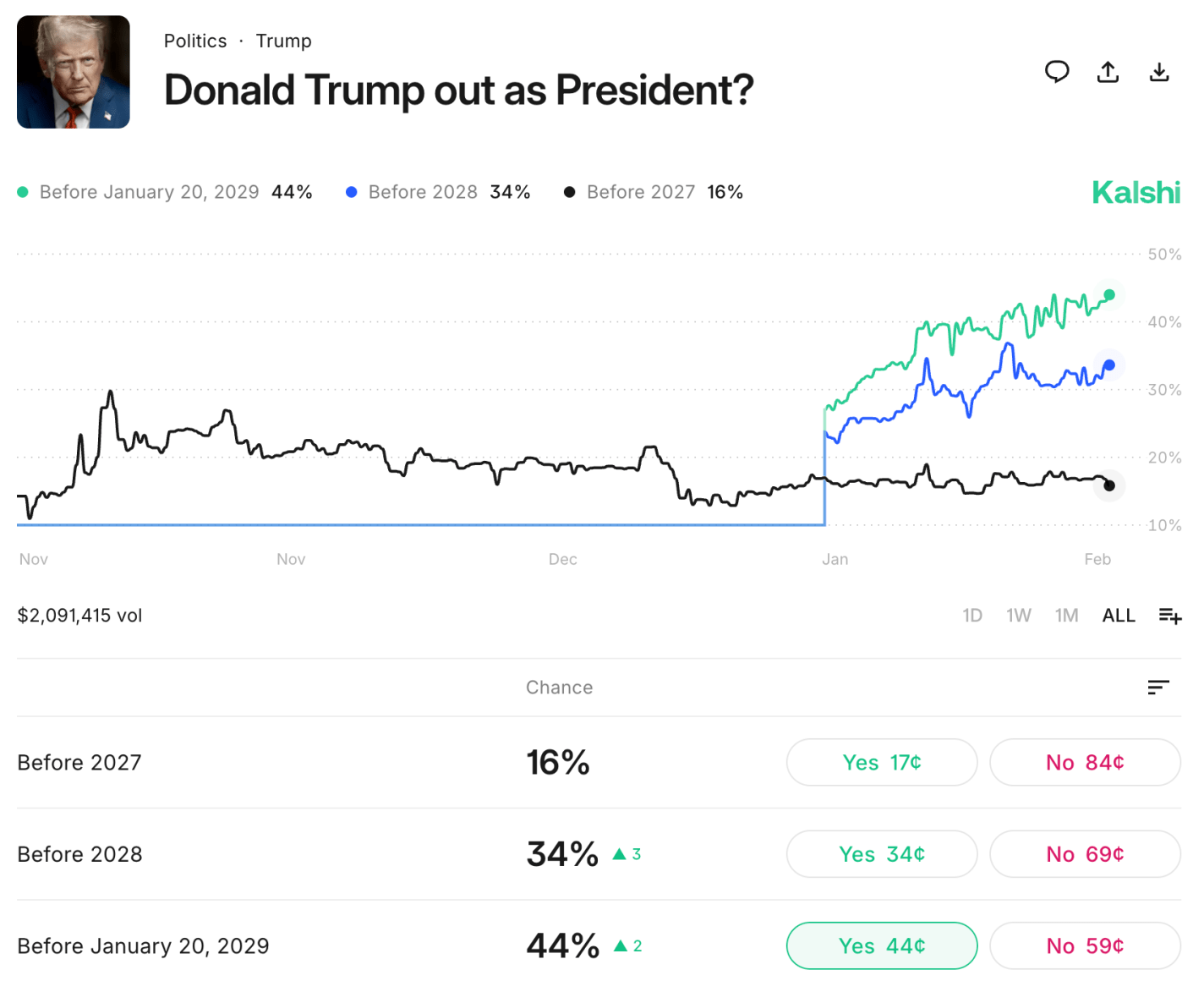

In the US, midterm elections have a 78% chance to flip control of the House and 35% chance to flip the Senate despite a tough map for Democrats. A midterm wave for the out-of-power party is typical in the US, given that the party in power always seems to over-play their hand and voters quickly get sick them. More surprising is that forecasters give a 44% chance that Donald Trump leaves office before his term is up, and a 16% chance that he leaves office this year. Markets give a 20% chance that he will be removed from office through the impeachment process, so the rest of the 44% would be from health issues or voluntary resignation.

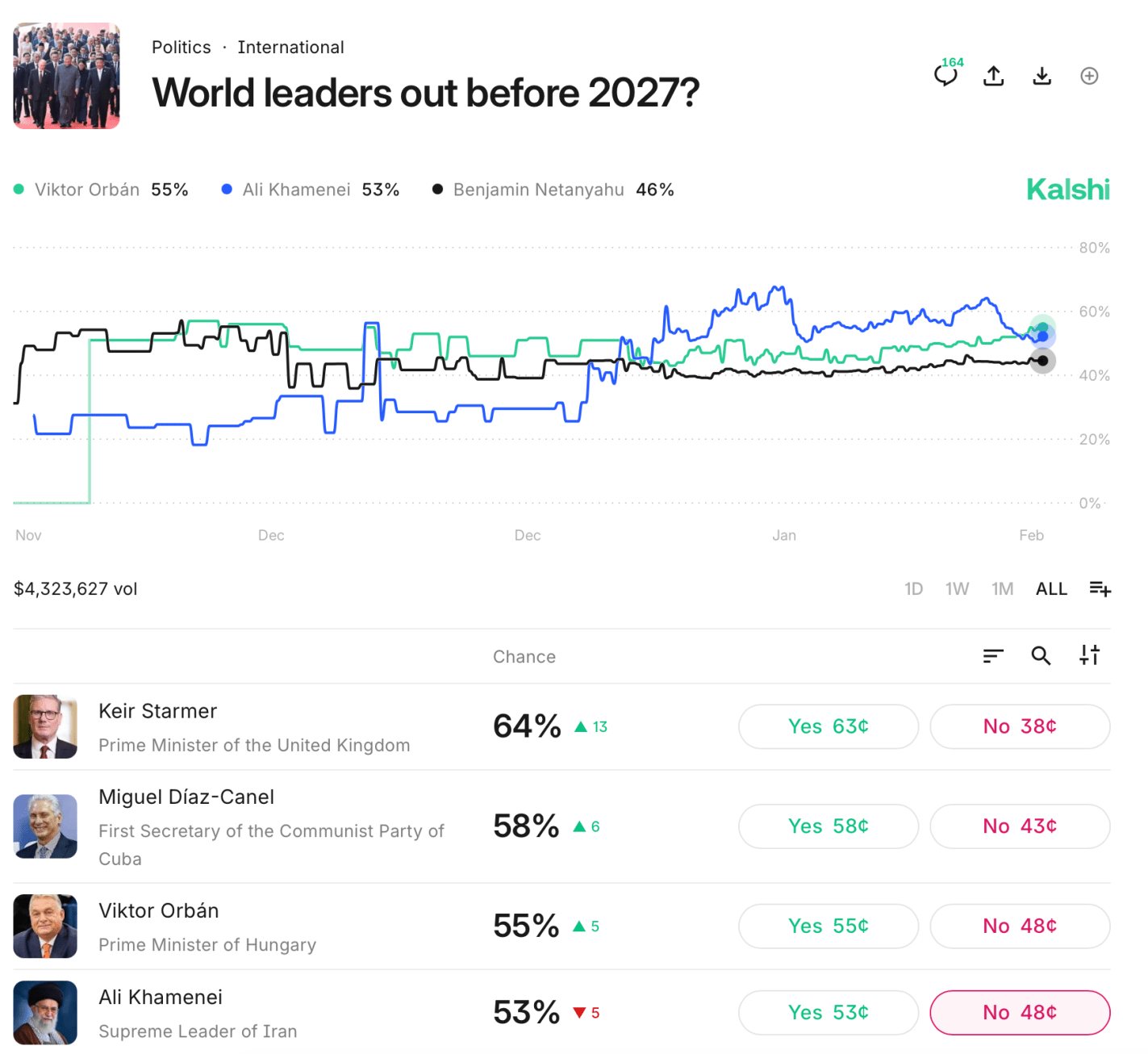

Forecasters at Kalshi predict a greater than even chance that 4 notable world leaders leave office this year:

I find this especially notable because Viktor Orban is the only one who would be removed through regularly scheduled elections. In the UK, Keir Starmer was just elected Prime Minister in 2024 and doesn’t have to face reelection until 2029; but he is so unpopular that his own Labor Party is likely to kick him out of office if local elections in May go as badly as polls indicate. If so, he would join Boris Johnson and Liz Truss as the third British PM in four years to leave office without directly losing an election. The leaders of Cuba and Iran don’t face real elections and would presumably be pushed out by a popular uprising orUS military action.

Some other important world leaders will probably stay in office this year, but forecasters still think there is a significant chance they leave: Israel’s Netanyahu (49%), Ukraine’s Zelenskyy (32%), and Russia’s Putin (14%). For the latter two, this belief could be tied to the surprisingly high odds given to a ceasefire in the Russia-Ukraine war this year (45%). Orban leaving office could be tied into this, as Hungary has often vetoed EU support for Ukraine.

Myself, I find most of these market odds to be high, and I’m tempted to make the “nothing ever happens” trade and bet that everyone stays in office. But even if all these markets are 10pp high, it still implies quite an eventful year ahead. Prepare accordingly.

Last January I shared a roundup of forecasts for the year from markets and professional economists. Were they any good? Here was their prediction for the US economy:

WSJ’s survey of economists reports that inflation expectations for 2025 were around 2% before the election, but are closer to 3% now. Their economists expect GDP growth slowing to 2%, unemployment ticking up slightly but staying in the low 4% range, with no recession. The basic message that 2025 will be a typical year for the US macroeconomy, but with inflation being slightly elevated, perhaps due to tariffs.

The verdicts (based on current data, which isn’t yet final for all of 2025):

Inflation: Nailed it exactly (2.7%)

GDP: We’re still waiting on Q4, but 2025 as a whole is on track to be a bit above the 2.0% forecast.

Unemployment: 4.6% as of November 2025, a bit above the 4.3% forecast

Recession: Didn’t happen, making the 22% chance forecast look fine

So the professional forecasters were probably a bit low on GDP and unemployment, but overall I’d say they had a good year. What about prediction markets?

For those who hope for DOGE to eliminate trillions in waste, or those who fear brutal austerity, the message from markets is that the huge deficits will continue, with the federal debt likely climbing to over $38 trillion by the end of the year. This is one reason markets see a 40% chance that the US credit rating gets downgraded this year.

While the US has only a 22% chance of a recession, China is currently at 48%, Britain at 80%, and Germany at 91%. The Fed probably cuts rates twice to around 4.0%.

Deficits: Nailed it, the federal debt is currently around $38.4 trillion.

US Credit Downgrade: It’s hard to score a prediction of a 40% chance of a binary event happening, but in any case Moodys downgraded the US’ credit rating in May, so that all three major agencies now rate it as not perfect.

The Fed: Cut rates a bit more than expected.

Foreign Recessions: China and Britain avoided recessions. Germany had a recession by the technical definition of Kalshi’s market, but not really in practice (FRED shows -0.2% Real GDP growth in Q2 followed by 0.00000% growth in Q3). Britain avoiding recession when markets showed an 80% chance was the biggest miss among the forecasts I highlighted.

Overall though, I’d say forecasters did fairly well in predicting how 2025 turned out, in spite of curveballs like the April tariff shock.

If you think the forecasters are no good and you can do better, you have more options than ever. Prediction markets are getting more questions and more liquidity if you’re up for putting your money where your mouth is; if you don’t want to put your own money at risk, there are forecastingcontests with prizes for predicting 2026.

WSJ’s survey of economists reports that inflation expectations for 2025 were around 2% before the election, but are closer to 3% now. Their economists expect GDP growth slowing to 2%, unemployment ticking up slightly but staying in the low 4% range, with no recession. The basic message that 2025 will be a typical year for the US macroeconomy, but with inflation being slightly elevated, perhaps due to tariffs.

Kalshi has a lot of good markets up that give more detailed predictions for 2025:

For those who hope for DOGE to eliminate trillions in waste, or those who fear brutal austerity, the message from markets is that the huge deficits will continue, with the federal debt likely climbing to over $38 trillion by the end of the year. This is one reason markets see a 40% chance that the US credit rating gets downgraded this year.

While the US has only a 22% chance of a recession, China is currently at 48%, Britain at 80%, and Germany at 91%. The Fed probably cuts rates twice to around 4.0%.

Will wage growth keep pace with inflation? It’s a tossup. Corporate tax cuts are also a tossup. The top individual rate probably won’t fall below it’s current 37%.

If you want to make your own predictions for the year, but don’t want to risk money betting on Kalshi, there are several forecasting contests open that offer prizes with no risk:

ACX Forecasting Contest: $10,000 prize pool, 36 questions, must submit predictions by Jan 31st

Bridgewater Forecasting Contest: $25,000 prize pool, half of prizes are reserved for undergraduates. Register now to make predictions between Feb 3rd and March 31st. Doing well could get you a job interview at Bridgewater.

Last week I laid out my own expectations for what economic policy would look like in a Trump or Harris presidency. Now after yesterday’s market reaction, we can infer what market participants as a whole expect by roughly doubling the size of yesterday’s market moves. Prediction markets had a 50-60% change of Trump winning as of Tuesday morning’s market close, which moved to a 99+% chance by Wednesday morning. Look at how other markets moved over the same time, multiply it by 2-2.5x, and you get the expected effect of a Trump presidency relative to a Harris presidency. So what do we see?

Stocks Up Overall: S&P 500 up 2%, Dow up 3%, Russell 2000 (small caps) up 6%. My guess this is mostly about avoiding tax increases- the odds that most of the Tax Cuts and Jobs Act gets renewed when it expires in 2025 just went way up. Lower corporate taxes boost corporate earnings directly, while lower taxes on households mean that they have more money to spend on their stocks and their products. Lower regulation and looser antitrust rules are also likely to boost corporate earnings.

Bond Prices Down (Yields Up): 10yr Treasury yields rose from 4.29% to 4.4%. This is the flip side of the tax cuts- they need to be paid for, and markets expect they will be paid for through deficits rather than cutting spending. The government will issue more bonds to borrow the money, lowering the value of existing bonds.

Dollar Up: The US dollar is up 2% against a basket of foreign currencies. I think this is mostly about the expected tariffs. People like the sound of the phrase “strong dollar” but it isn’t necessarily a good thing; it makes it cheaper to vacation abroad, but makes it harder to export, even before we consider potential retaliatory tariffs.

Crypto Way Up: Bitcoin went up 7% overnight, Ethereum is now 15% up since Tuesday. Crypto exchange Coinbase was up 31%. Markets anticipate friendlier regulation of crypto, along with a potential ‘strategic Bitcoin reserve’.

Single Stock Moves: Private prison stocks are up 30%+. Tesla is up 15%, mostly due to Elon Musk’s ties to Trump, but also due to tariffs. Foreign car companies were way down on the expectation of tariffs- Mercedes-Benz down 8%, BMW down 10%, Honda down 8%.

Sector Moves: Steel stocks are up on the expectation of tariffs, while solar stocks (which can’t catch a break, doing poorly under Biden despite big subsidies and big revenue increases) were down 12% in the expectation of falling subsidies. Bank stocks did especially well, with one bank ETF up 12%. This gives us one hint on what to me is now the biggest question about the second Trump administration- who will staff it? I could see Trump appointing free-market types, or wall-streeters in the mold of Steve Mnuchin, or dirigiste nationalist conservatives in the JD Vance / Heritage Foundation mold, or an eclectic mix of political backers like Elon Musk and RFK Jr, or a combination of all of the above. The fact that bank stocks are way up tells me that markets expect the free-marketers and/or the Wall-Street types to mostly win out.

Just Ask Prediction Markets: If you want to know what markets expect from a Presidency, you can do what I just did, look at moves the big traditional markets like stocks and bonds and try to guess what is driving them. But increasingly you can skip this step and just ask prediction markets directly- the same markets that just had a very goodelection night. Kalshi now has markets on both who Trump will nominate to cabinet posts, as well as the fate of specific policies like ‘no tax on tips‘

I doubt anyone has been waiting for my take on the Trump and Harris economic plans to decide their vote. More than that, it is entirely reasonable to vote based on things other than their economic plans entirely- like foreign policy, character, or preservingdemocracy. But either Trump or Harris will soon be President, and thinking through their economic plans can help us understand how the next 4 years are likely to go.

The bad news is that both campaigns keep proposing terrible ideas. The good news is that, thanks to our system of checks and balances, most of them are unlikely to become policy. The other good news is that our economy can handle a bit of bad policy- as Adam Smith said, there’s a lot of ruin in a nation. After all, the last Trump admin and the Biden-Harris admin did all sorts of bad economic policies, but overall economic performance in both administrations was pretty good; to the extent it wasn’t (bad unemployment at the end of the Trump admin, bad inflation at the beginning of Biden-Harris), Covid was the main culprit.

Note that this post will just be my quick reactions; the Penn Wharton Budget Model has done a more in-depth analysis. They find that Harris’ plan is bad:

We estimate that the Harris Campaign tax and spending proposals would increase primary deficits by $1.2 trillion over the next 10 years on a conventional basis and by $2.0 trillion on a dynamic basis that includes a reduction in economic activity. Lower and middle-income households generally benefit from increased transfers and credits on a conventional basis, while higher-income households are worse off.

We estimate that the Trump Campaign tax and spending proposals would increase primary deficits by $5.8 trillion over the next 10 years on a conventional basis and by $4.1 trillion on a dynamic basis that includes economic feedback effects. Households across all income groups benefit on a conventional basis.

We are already running way too big a deficit; candidates should be competing to shrink it, not make it worse. This isn’t just me being a free-market economist; Keynes himself would be saying to run a surplus in good economic times so that you have room to run a deficit in the next recession.

Now for my lightning round of quick reactions:

No tax on tips: both campaigns are now proposing this; it is a silly idea, there is no reason to treat tips differently from other income. The good news is that this almost certainly won’t make it through Congress.

Taxes: Trump’s Tax Cuts and Jobs Act of 2017 is set to expire in 2025. He says he wants to renew it and add more tax cuts, though he will need a friendly Congress to do so. Harris wants to let most of it expire, but renew and expand the Child Tax Credit while raising taxes on the wealthy and corporations. There’s a good chance we end up with divided government, in which case probably only the most popular parts of TCJA (increased standard deduction and child tax credit) get renewed and no big new changes happen.

Price controls: both campaigns, especially Harris‘, have talked about fighting ‘price gouging’, leading economists to worry about the price controls (any intro micro class explains why these are a bad idea). My guess is that no real bill gets passed, President Harris gets the FTC to make a show of going after grocery stores but nothing major changes.

Tariffs: Harris would probably leave them where they are; Trump is promising to raise them 10-20% across the board and 60% on China. This would lead to higher prices for US consumers and invite retaliation from abroad; we saw the same things when Trump raised tarriffs in his first term, but he is promising bigger increases now. This is worrisome because the President has a lot of power to change tariffs unilaterally; it would take a bill getting through Congress to stop this, and I don’t see that happening.

Regulation / One in two out: The total amount of Federal regulation stayed fairly flat during the Trump administration thanks to his one in two out rule, while regulation increased during the Biden-Harris administration. I expect that a second Trump admin would behave like the first here, while a Harris admin would continue the Biden-Harris trend.

Antitrust: FTC and DOJ have been aggressive during the Biden-Harris administration, blocking reasonable mergers and losing a lot in court. But Trump’s VP candidate JD Vance thinks FTC Chair Lina Khan is “doing a pretty good job”, so we could see this poor policy continue either way. More generally, voters should consider what a Vance presidency would look like, because making him Vice President makes it much more likely (Trump is 78 and people keep trying to shoot him; plus VPs get elected President at high rates).

Immigration: Immigration rates have been high under the Biden-Harris admin, while Trump’s top two planks in his platform are “seal the border” and “carry out the largest deportation operation in American history”. Economically, this would lead to a reduction in both supply and demand in many sectors, with the relative balance (so whether prices go up or down) depending on the sector. The exclusion of Mexican farmworkers in the 1960’s led to a huge increase in mechanization, to the point that domestic farmworkers saw no increase in their wages; presumably this also limited the potential harm to the food supply.

Crypto: The Biden admin has been fairly negative on crypto; both Harris and Trump are making pro-crypto statements in their campaigns, particularly Trump.

Marijuana: The Biden admin is in the process of rescheduling marijuana to no longer be in the most restricted category of drugs. I think Trump would probably see the process through, while Harris definitely would.

Elon Musk / Civil Service: Elon Musk has thrown his support hard behind Trump, spending lots of money, tweeting continuously, and attending rallies. It’s hard to know how much of this is genuine support for a range of Trump’s policies, how much is to get the Federal government to stop suing his companies so much, and how much is to get himself a direct role in government. In any case, it is a safe bet that more Federal civil servants get fired in a Trump admin than in a Harris admin. What’s much harder to say is how many get fired, and what proportion of firings come from a genuine attempt to improve efficiency vs a purge of those Trump sees as disloyal. Personally I think government could stand to treat its employees a bit more like the private sector, making it easier to fire people for genuine poor performance (not political views), but also allowing for more flexibility on improved pay, benefits, and the ability to focus on achieving goals more than following the way things have always been done. But I doubt that’s on the table either way.

CFTC/ Prediction Markets: The Biden CFTC has tried to crack down on prediction markets, though they have mostly failed in the courts, and the growth of Kalshi and Polymarket mean that prediction markets are now bigger than ever. Most of the anti-prediction-market decisions have been 3-2 votes of the democrats vs the republicans, so a new republican appointee could lock in the legal gains prediction markets have made, though this is far from guaranteed (not all Rs support this).

Final Thoughts: So much of how things turn out will depend not just on who wins the Presidency, but on whether their party wins full control of Congress. Because the Democrats have a lot more Senate seats up for grabs this year, Harris is much more likely to be part of a divided government (especially once you consider the Supreme Court).

Because of this, and because of the ability of the President to raise tariffs unilaterally, I see Trump as the bigger risk when it comes to economic prosperity, as well as non-economic issues. Harris with a Republican Senate is the best chance of maintaining something like the status quo, whereas a Trump victory is likely to see bigger changes, many of them bad.

That said, predicting the future is hard, and this applies doubly to Presidential terms. I’m struck by how often in my lifetime the most important decisions a President had to make had nothing to do with what the campaign was fought over. Who knew in 1988 that the President’s biggest task would be managing the breakup of the Soviet Union? In 2000, that it would be responding to 9/11? Bush specifically tried to distinguish himself from Gore as being the candidate more against “nation-building”, then went on to try just that in Afghanistan and Iraq. In 2004, who knew that the biggest issue of the term would be not Social Security or foreign policy, but a domestic financial crisis and recession? In 2016, who knew that they were voting on the President that would respond to the Covid pandemic? In 2020, who knew that they were voting on who would respond to Russia’s invasion of Ukraine?

The most important issue for the next President could easily be how they address China or AI, because those are clearly huge deals. I won’t vote based on this, because I don’t know who has the better plan for them, because I have no idea what a good plan looks like. Or the most important issue could be something that comes completely out of left field, like Covid did. Not even the very wise can see all ends.

What I do know is that, while much of the Libertarian Party has recently gone from its usual “goofy-crazy” to “mean-crazy“, Chase Oliver is so far the only candidate pandering to me personally. But it’s not too late for other politicians at all levels to try the same.

See you all again next Thursday, by which time the election will, I hope, be over.

Kalshi just announced that they will begin paying interest on money that customers keep with them, including money bet on prediction market contracts (though attentive readers here knew was in the works). I think this is a big deal.

First, and most obviously, it makes prediction markets better for bettors. This was previously a big drawback:

The big problem with prediction markets as investments is that they are zero sum (or negative sum once fees are factored in). You can’t make money except by taking it from the person on the other side of the bet. This is different from stocks and bonds, where you can win just by buying and holding a diversified portfolio. Buy a bunch of random stocks, and on average you will earn about 7% per year. Buy into a bunch of random prediction markets, and on average you will earn 0% at best (less if there are fees or slippage).

This big problem just went away, at least for election markets (soon to be all markets) on Kalshi. But the biggest benefit could be how this improves the accuracy of certain markets. Before this, there was little incentive to improve accuracy in very long-run markets. Suppose you knew for sure that the market share of electric vehicles in 2030 would over 20%. It still wouldn’t make sense to bet in this market on that exact question. Each 89 cents you bet on “above 20%” turns into 1 dollar in 2030; but each 89 cents invested in 5-year US bonds (currently paying 4%) would turn into more than $1.08 by 2030, so betting on this market (especially if you bid up the odds to the 99-100% we are assuming is accurate) makes no financial sense. And that’s in the case where we assume you know the outcome for sure; throwing in real-world uncertainty, you would have to think a long-run market like this is extremely mis-priced before it made sense to bet.

But now if you can get the same 4% interest by making the bet, plus the chance to win the bet, contributing your knowledge by betting in this market suddenly makes sense.

This matters not just for long-run markets like the EV example. I think we’ll also see improved accuracy in long-shot odds on medium-run markets. I’ve often noticed early on in election markets, candidates with zero chance (like RFK Jr or Hillary Clinton in 2024) can be bid up to 4 or 5 cents because betting against them will at best pay 4-5% over a year, and you could make a similar payoff more safely with bonds or a high-yield savings account. Page and Clemen documented this bias more formally in a 2012 Economic Journal paper:

We show that the time dimension can play an important role in the calibration of the market price. When traders who have time discounting preferences receive no interest on the funds committed to a prediction-market contract, a cost is induced, with the result that traders with beliefs near the market price abstain from participation in the market. This abstention is more pronounced for the favourite because the higher price of a favourite contract requires a larger money commitment from the trader and hence a larger cost due to the trader’s preference for the present. Under general conditions on the distribution of beliefs on the market, this produces a bias of the price towards 50%, similar to the so-called favourite/longshot bias.

We confirm this prediction using a data set of actual prediction markets prices from 1,787 market representing a total of more than 500,000 transactions.

Hopefully the introduction of interest will correct this, other markets like PredictIt and Polymarket will feel competitive pressure to follow suit, and we’ll all have more accurate forecasts to consult.

The Fed has now almost landed the plane, bringing us down from 9% inflation during the Covid era to something approaching their 2% target today. But it is not yet clear how hard the landing will be. Back in March I thought recurrent inflation was still the big risk; now I see the risk of inflation and recession as balanced. This is because inflation risks are slightly down, while recession risk is up.

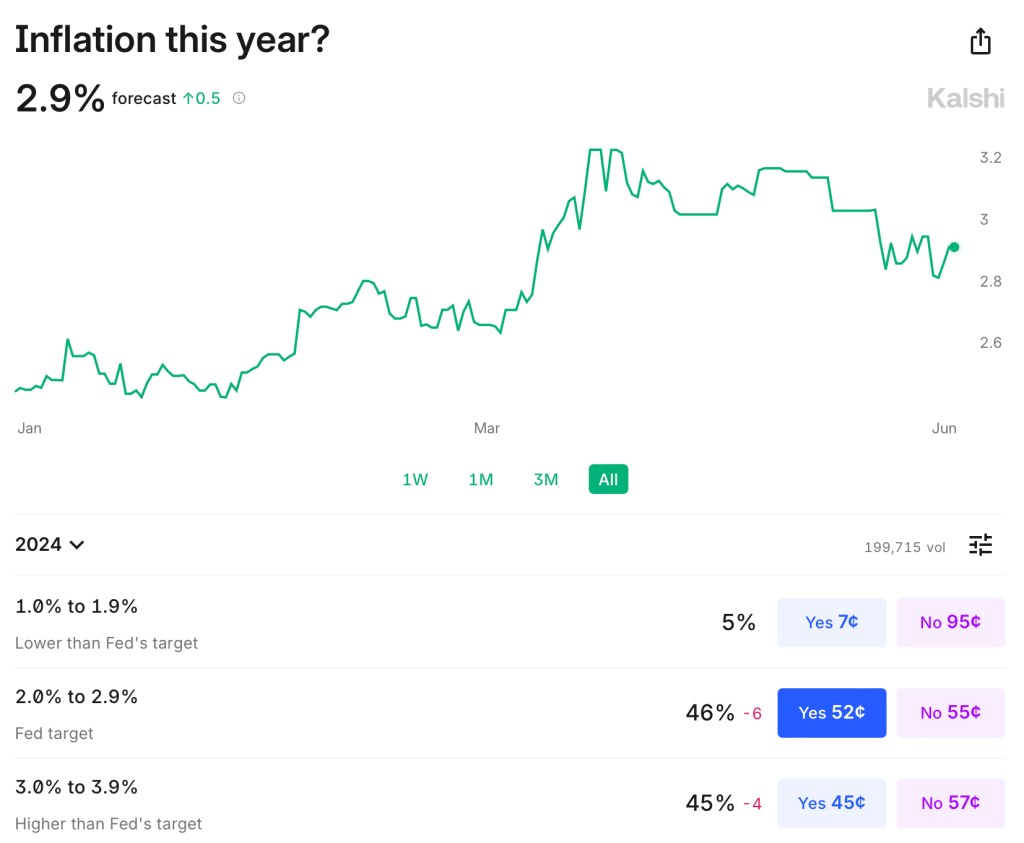

Inflation remains somewhat above target: over the last year it was 3.3% using CPI, 2.7% by PCE, and 2.8% by core PCE. It is predicted to stay slightly above target: Kalshi estimates CPI will finish the year up 2.9%; the TIPS spread implies 2.2% average inflation over the next 5 years; the Fed’s own projections say that PCE will finish the year up 2.6%, not falling to 2.0% until 2026. The labels on Kalshi imply that markets are starting to think the Fed’s real target isn’t 2.0%, but instead 2.0-2.9%:

The Fed’s own projections suggest this to be the somewhat the case- they plan to start cutting over a year before they expect inflation to hit 2.0%, though they still expect a long run rate of 2.0%. In short, I think there is a strong “risk” that inflation stays a bit elevated the next year or two, but the risk that it goes back over 4% is low and falling. M2 is basically flat over the last year, though still above the pre-Covid trend. PPI is also flat. The further we get from the big price hikes of ’21-’22 with no more signs of acceleration, the better.

But I would no longer say the labor market is “quite tight”. Payrolls remain strong but unemployment is up to 4.0%. This is still low in absolute terms, but it’s the highest since January 2022, and the increase is close to triggering the Sahm rule (which would predict a recession). Prime-age EPOP remains strong though. The yield curve remains inverted, which is supposed to predict recessions, but it has been inverted for so long now without one that the rule may no longer hold.

Looking through this data I think the Fed is close to on target, though if I had to pick I’d say the bigger risk is still that things are too hot/inflationary given the state of fiscal policy. But things are getting close enough to balanced that it will be easy for anyone to find data to argue for the side that they prefer based on their temperament or politics.

To me the big wild card is the stock market. The S&P500 is up 25% over the past year, driven by the AI boom, and to some extent it pulls the economy along with it. The Conference Board’s leading economic indicators are negative but improving overall this year; recently their financial indicators are flat while non-financial indicators are worsening.

Overall things remind me a lot of the late ’90s: the real economy running a bit hot with inflation around 3% and unemployment around 4%; the Fed Funds rate around 5%; and a booming stock market driven by new computing technologies. Naturally I wonder if things will end the same way: irrational exuberance in the stock market giving way to a tech-driven stock market crash, which in turn pushes the real economy into a mild recession.

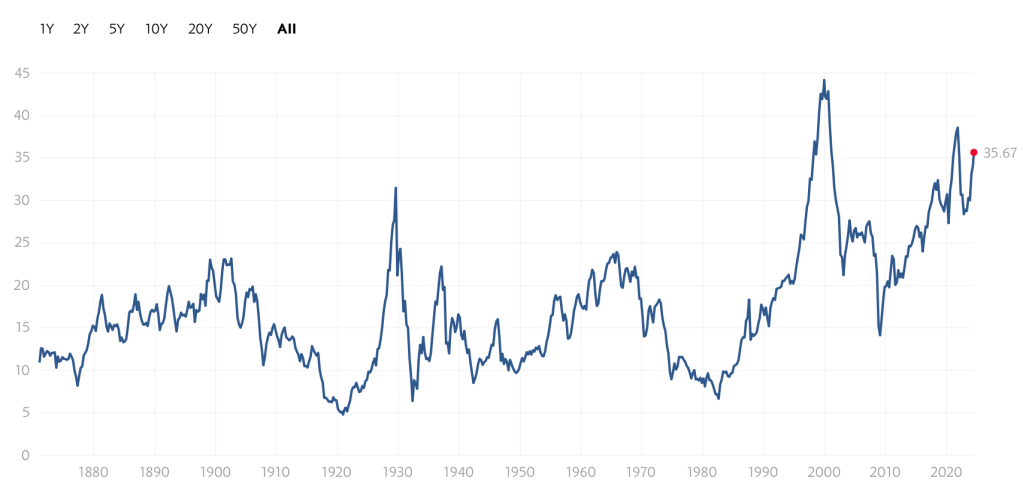

Of course there is no reason this AI boom has to end the same way as the late-90’s internet boom/bubble. There are certainly differences: the Federal government is running a big deficit instead of a surplus; there are barely a tenth as many companies doing IPOs; many unprofitable tech stocks already got shaken out in 2022, while the big AI stocks are soaring on real profits today, not just expectations. Still, to the extent that there are any rules in predicting stock crashes, the signs are worrying. Today’s Shiller CAPE is below only the internet and Covid meme-stock bubble peaks:

Again, this doesn’t mean that stocks have to crash, or especially that they have to do it soon; the CAPE reached current levels in early 1998, but then stocks kept booming for almost two years. I’m not short the market. But the macro risk it poses is real.

I’m back from Manifest, a conference on prediction markets, forecasting, and the future. It was an incredible chance to hear from many of my favorite writers on the internet, along with the CEOs of most major prediction markets; in Steve Hsu’s words, Woodstock for Nerds. Some highlights:

Robin Hanson took over my session on academic research on prediction markets (in a good way; once he was there everyone just wanted to ask him questions). He thinks the biggest current question for the field is to figure out why is the demand for prediction markets so low. What are the different types of demand, and which is most likely to scale? In a different talk, Robin says that we need to either turn the ship of world culture, or get off in lifeboats, before falling fertility in a global monoculture wrecks it.

Play-money prediction markets were surprisingly effective relative to real-money ones in the 2022 midterms. Stephen Grugett, co-founder of Manifold (the play-money prediction market that put on the conference), admitted that success in one election could simply be a coincidence. He himself was surprised by how well they did in the 2022 midterms, and said he lost a bunch of mana on bets assuming that Polymarket was more accurate.

Substack CEO Chris Best: No one wants to pay money for internet writing in the abstract, but everyone wants to pay their favorite writer. For me, that was Scott Alexander. We are trying to copy Twitter a bit. Wants to move into improving scientific publishing. I asked about the prospects of ending the feud with Elon; Best says Substack links aren’t treated much worse than any other links on X anymore.

Razib Khan explained the strings he had to pull for his son to be the first to get a whole genome sequence in utero back in 2014- ask the hospital to do a regular genetic test, ask them for the sample, get a journalist to tweet at them when they say no, get his PI’s lab to run the sample. He thinks crispr companies could be at the nadir of the hype cycle (good time to invest?).

Kalshi cofounder Luana Lopes Lara says they are considering paying interest on long term markets, and offering margin. There is enough money in it now that their top 10 or so traders are full time (earning enough that they don’t need a job). The CFTC has approved everything we send them except for once (elections). We don’t think their current rule banning contest markets will go through, but if it does we would have to take down Oscar and Grammy markets. When we get tired of the CFTC, we joke that we should self certify shallot futures markets (toeing the line of the forbidden onion futures). Planning to expand to Europe via brokerages. Added bounty program to find rules problems. Launching 30-50 markets per week now (seems like a good opportunity, these can’t all be efficient right?).

There was lots else of interest, but to keep things short I’ll just say it was way more fun and informative doing yet another academic conference, where I’ve hit diminishing returns. More highlights from Theo Jaffee here; I also loved economist Scott Sumner’s take on a similar conference at the same venue in Berkeley:

If you spend a fair bit of time surrounded by people in this sector, you begin to think that San Francisco is the only city that matters; everywhere else is just a backwater. There’s a sense that the world we live in today will soon come to an end, replaced by either a better world or human extinction. It’s the Bay Area’s world, we just live in it.