This week at my university the Economics Department Co-hosted an event titled “Interest Rates and Student Loans” with the Office of Financial Aid. I discussed interest rates for a broad audience of young adults. Below is my talk on interest rates.

When I first started reading of “Lender-on-Lender Violence” this year, images of bankers in three-piece suits brawling in the streets of Lower Manhattan came to mind. It turns out that this is a staid legal term for a practice which has been around for some time, but is becoming more common and consequential.

Consider a case where say three lenders (e.g. banks or more likely venture capital funds) have lent money to some startup or struggling company XYZ. Let’s call these lenders A, B, and C. Now XYZ needs even more funding, perhaps because they need to build another factory, or perhaps because things are not working out as they hoped and they cannot pay off the original loans and still stay in business.

Now Lenders A and B get together and cook up a scheme. They will lend some more money to company XYZ to largely replace the original loan, but they contrive to get legal terms for that new loan that give it a higher priority for payment than the original loan. This is called “up-tiering” the new loan. This has the effect of reducing the market value of the original loan.

Lender C is now hosed. It faces murky prospects for repayment on that original loan. Lenders A and B offer to buy them out of the original loan for 40 cents on the dollar. Lender C proceeds to sue Lenders A and B.

Will Lender C prevail? Probably not, if the course of recent cases is any guide. Unless there is very specific language in the legal “covenant” regarding the first loan forbidding this practice, it seems to be legal.

A similar maneuver would be for a new Lender D to offer a replacement loan to Company XYZ, with legal language giving it priority over the original loan. This is called “priming.”

Yet another tactic by the aggressive lenders includes working with Company XYZ to move its more valuable assets into a subsidiary or shell company, and to get the new loan to hold that as collateral. This again hoses the “victim” lenders, since again the assurance that they will be repaid has gone down.

My Personal Experience with Lender-on-Lender Violence

Some years ago, I bought the bonds of a company called SeaDrill. I bought the bonds instead of the common or preferred stock, for an additional margin of safety. Unlike the stock, the bonds must be repaid in full, right? Both the bonds and the preferreds were paying about 9%, back when general interest rates were much lower than that are now. So, I was a lender to the company.

Silly me. Times got tough in the oil patch, and the company would have had difficulty paying off its bonds AND paying its management their high salaries. So, they went for Chapter 11 bankruptcy. I had not realized the difference between Chapter 7 bankruptcy, where the company shuts down and liquidates and pays off its creditors in pecking order, and Chapter 11, which is largely a chance for the company to put the losses on its creditors and to keep on operating.

As with the example above, some big institution offered to refinance things with new secured bonds that had priority ahead of the old bonds (which I held). In the end I got about 44 cents on the dollar for my bonds. I was not happy about that, but I did make out better than the hapless preferred stockholders, who got just a tiny crumb to make them go away. It was a learning experience. I did feel, well, violated.

Implications for the Burgeoning Private Credit Market

I will be writing more on the booming “private credit” market. Many of the loans in this space are “covenant-lite.” Back before say 2008, a large fraction of loans to business were through banks, who would insist on strong legal protection for their money. But in recent years, private equity funds have competed for this lending, allowing the borrowers to borrow on terms that give much less protection to the lenders. Cov-lite is now the norm.

Traditionally, loans (as distinct from bonds) to businesses have enjoyed decent recoveries (e.g., around 70%) in case of defaults, thanks to strong collateral backing the loans. But if we face any sort of prolonged recession and elevated defaults, the recoveries on all these loans will be far less than in the past. These are uncharted waters.

As you drive through cities and many suburbs near cities, you see lot and lots and lots of office buildings. Employees by the tens of millions used to get dressed and fight their way through traffic to get to these building every weekday, park, and go up to their desks to do their white-collar jobs.

The demand for new office space seemed endless, and so developers borrowed money to build more office buildings, and firms like real estate investment trusts (REITs) also borrowed money to buy such buildings in order to rent them out.

Covid changed all that. Suddenly, in early/mid 2020, nearly all office buildings went dark, and people started working from home. With affordable computers and internet access, and with Zoom and other conferencing tools, it was found that workers could get their jobs done remotely. Even after vaccines rolled out in early/mid 2021, concerns over contagious Covid variants kept offices closed. 2022 was when things started opening up again big time, and by end 2022/early 2023 there were stories in the news about companies ordering employees back to their desks.

By January, 2023 Bloomberg could report “More than half of workers in major US cities went to the office last week, the first time that return-to-office rates crossed 50% of their pre-pandemic levels.” However, that movement seems to have stalled, and has even reversed in some cases, as workers have pushed back strongly against being forced back to the cubes. Notably, Elon Musk initially banned remote work at Twitter after taking it over in November, but after rethinking the costs of maintaining offices, has shut down Twitter’s offices in Seattle and Singapore, telling employees to work from home

Per the Morning Consult, “The pandemic lockdown triggered one of the swiftest, most significant behavior changes in human history. People’s habits changed overnight, and through the successive lockdowns, shutdowns and new standards, these new habits became ingrained. The experience triggered new, positive associations with working from home, working out with virtual trainers, cooking, gardening and more. A vast web of neural pathways formed to hold these new associations – and that web runs deep.”

And thus, many office buildings remain largely empty, which in turn is resulting in rising defaults on the loans for these buildings. A number of high profile corporate owners in recent months have deliberately (in their own pecuniary interest) defaulted on their loans, forfeited their equity interest in a building , and handed the keys back to the mortgage lenders, who are now stuck with big losses on their loans and with holding a building that nobody much wants.

There are many ramifications of these trends. The one I will focus on is how this extended underutilization of offices affects the parties that lent money to build or buy these buildings. In many cases, those lenders were smaller (regional) banks. They have much greater exposure to commercial real estate loans than the larger banks, which may cause serious problems in the coming months.

Eric Basmajian calls out some key differences between large and small banks in the U.S.:

At large US banks, loans make up 51% of total assets. Small banks have 65% loans as a percentage of total assets. So small banks have a lot of loans, and large banks have a lot of cash, Treasury bonds, and MBS.

…At small US banks, loans make up 65% of assets. Of that loan portfolio, real estate is 65%, meaning a lot of real estate exposure….Within that real estate loan portfolio, almost 70% was commercial real estate lending. So small banks have a high concentration of commercial real estate loans…. Within the commercial real estate category, the highest concentration is “non-residential property,” which can include office buildings, retail stores, and data centers.

….So small banks have a potentially large problem. Deposits are starting to leave after the SVB crisis in search of more safety, but also in search of higher yields on safe assets like Treasury bills. Deposit outflows will make it hard for small banks to grow lending and may cause a deleveraging. If deposit outflows are severe, deleveraging will cause banks to sell securities or loans.

Securities can be pledged at the Fed for a relatively high-interest rate. This keeps a bank solvent but at a material hit to earnings. The loan portfolio is a much bigger problem because the value of these potentially permanently impaired assets will be called into question.

Basmajian summarizes:

There are major differences between large and small US banks.

Large banks hold a lot of reserves, Treasuries, MBS, and residential real estate loans. The asset mix at large banks is very conservative.

Small banks have most of their assets in loans, with commercial real estate holding the highest weight. Small banks appear to have outsized exposure to highly impaired office buildings which could generate significant losses.

It will be critical to monitor lending standards and availability at small banks because, in the post-2008 cycle, small banks are the lifeblood of credit to the private economy.

Money can be simplistically defined as “A medium that can be exchanged for goods and services and is used as a measure of their values on the market, and/or a liquifiable asset which can readily be converted to the medium of exchange”. Earlier we described the amounts of various classes of “money” in the U.S. Here is a chart showing the amount of currency in circulation (coins and bills; lowest line on the chart) for 2005-2020, and also M1 (green), M2 (upper curve, purple) and “monetary base” (currency plus reserves at the Fed; red line).

To recap what M1 and M2 are:

M1: Physical currency circulating outside of the Fed and private banking system, plus the amount of demand deposits, travelers’ checks and other checkable deposits. This is highly “liquid” money, i.e. accepted and used for transactions in the private economy.

M2: M1 + most savings accounts, money market accounts, retail money market mutual funds, and small denomination time deposits (certificates of deposit of under $100,000).

The funds in these additional savings and money market accounts can in general be easily transferred to checkable accounts, and thus could go towards making purchases if desired.

Physical currency is made and put into circulation by the government or quasi-governmental agencies (the Treasury mints coins, and the Federal Reserve prints bills). But what about all the other money (M1, M2, etc.), which dwarfs the physical currency? How does it grow?

Without getting into all the weeds, it turns out that the major driver of money creation in modern economies is the process of bank loans. The vast majority of money in countries like the U.S. is not created directly by government or central bank operations, but is created in the private sector when commercial banks make loans. When individuals or companies decide to take out more loans (including loans for cars, houses, or business investment), the effective money supply in the nation increases. This is true for other modern economies. For instance, the Bank of England states:

There are three types of money in the UK economy:

3% Notes and coins

18% Reserves

79% Bank deposits

A typical scenario of how bank lending increases money might go something like this: Fred would like to add an enclosed back porch to his house, but doesn’t have the money in hand to pay a carpenter to build it for him. So the base case is no payment to the carpenter and no porch for Fred. However, Fred realizes he can go the bank and get a loan to pay for the porch. So he obtains a $20,000 loan from the bank, which first shows up as a $20,000 credit to Fred’s checking account. The bank credits Fred’s account, and in exchange obtains a contract from Fred promising that Fred will pay it back, with interest.

Fred writes a check for $20,000 to the carpenter, who in turn pays $10,000 to a lumberyard for materials and keeps the other $10,000 as his fee. The lumberyard is able to pay its workers for that day, and order replacement lumber from a mill. The workers spent their pay on various items. The carpenter puts $5000 of his $10,000 fee in a savings account, and pays the rest to a car dealer for a used car.

The initial loan to Fred set off a chain of spending and economic activity, which would not have otherwise occurred. Fred has his porch, the lumberyard workers continue to be employed and supporting their local merchants, the carpenter gets a second car, and this money keeps ricocheting around until it gets drained away into stagnant savings, or is used to pay down prior debt. Although they are not aware of it, part of the lumberyard workers’ pay for that day came out of the debt incurred by Fred.

The granting of that loan created $20,000 of spending capability, i.e. money. As far as the economy is concerned, that $20,000 did not exist as effective money prior to the loan. Thus, the money came into existence simultaneously with the debt associated with the loan. Fred received the capacity to spend $20,000 today, but in turn accepted the obligation to pay back this money, with interest. It is assumed that Fred had a stable income, such that he would in fact be able to pay back the loan in the future.

In general, increasing debt increases the money supply, and paying down debt extinguishes money. For simplicity, suppose Fred repays the $20,000 loan (with $2000 interest added) in one big lump, two years later. In that year, he will presumably spend into the economy something like $22,000 less than he would have otherwise. Thus, his paying down of his debt will act as a decrease in the circulating money.

In normal times, as one person is paying down his loan (and thereby shrinking the money supply), someone else is taking out a new and even larger loan, so total debt and the amount of money in circulation stays about the same, or grows somewhat. A feature of the 2008-2009 recession, however, was a big drop in consumer demand for credit; folks decided to pay down debts and not borrow so much money to buy stuff. The effect was a big drop in spending and thus in overall economic activity (GDP) and in employment.

Where was that $20,000 before Fred borrowed it? We might think that it was sitting unused in the bank vaults, just waiting to be borrowed. That turns out to be an incorrect picture of the lending process.

Bank loans differ in key ways from, say, an interpersonal loan. If I lend you money, I might draw down my checking deposit and give you a check which you would deposit in your bank account. No new money is created. You may hand me an I.O.U. slip stating when you will pay me back and with what interest, but that would still be just the same funds being traded back and forth between the two of us. I would have to have the money in my account to start with before I could loan it to you.

Bank lending is different. A bank can lend money and hence create a new deposit, which amounts to brand-new money, even if the bank does not have that money to start with. This is counterintuitive. In a later post we may flesh out this seemingly magical aspect of bank lending. See Overview of the U. S. Monetary System for a more complete discussion.

A week ago, we described commercial loans in general, and how they differ from bonds. Companies nearly always need money to make money, and thus have to borrow money in addition to selling stock shares. Companies that are new or smaller or doing poorly or have already borrowed a lot can still get loans, but these loans typically come with stringent conditions and require paying relatively high interest. These “leveraged loans” are the loan equivalent of “junk” bonds. When a bank lends money as a “Senior Secured Loan”, this entails agreements (“covenants”) which may specify that in event of default, this loan gets paid off ahead of any other creditor, and also that some specific asset held by the company, such as a building or an oil field, will be given over to the bank.

Financial institutions like insurance companies and pension funds are hungry for “investment grade” securities like bonds rated BBB or higher. Normally, these institutions would not consider buying into the senior loan marketplace, since these instruments are not considered investment grade.

Enter “Collateralized Loan Obligations” (CLOs). With a CLO, 200 or so loans which have been made by banks and then sold off into the market are bundled together, and then the cash flow from the interest paid on these loans plus the principal paid back is repackaged into slices or “tranches”. The highest level tranches get first dibs on being paid from the overall CLO cash flow, then the lower and lower tranches. The majority of bank loans today end up being packaged into CLOs. CLOs are an example of a lucrative operation known as “securitization”: “Securitization is the process of taking an illiquid asset or group of assets and, through financial engineering, transforming it (or them) into a security” (per Investopedia).

The rate of loan defaults in recent years has been only 3-4%, and on average the recovery on a given defaulted senior secured loan has been around 80%. So the actual losses (e.g. 4% x 20%, or 0.8% net) have been quite low. The highest annual default rate in recent memory was about 10%, in the Global Financial Crisis of 2008-2009.

The theory is that, although any particular loan has a nontrivial chance of defaulting, it is unthinkable that more than say 20% of all loans would default; and even if a full 20% of the loans did default, we would expect that the actual losses after liquidating the pledged collateral would be more like 4% of the entire loan portfolio (i.e. 20% defaults x 20% loss per default). This means that the top 95% or so of CLO cash flow should be considered very secure, and the top 60-70% are utterly secure.

Thus, the top 60-65% of the CLO cash flow is packaged as super secure, relatively low-yielding AAA rated debt, and as such is bought up by conservative financial institutions, including banks. This arrangement keeps those institutions happy, and also facilitates the making of loans to the needy companies who are taking out the underlying loans.

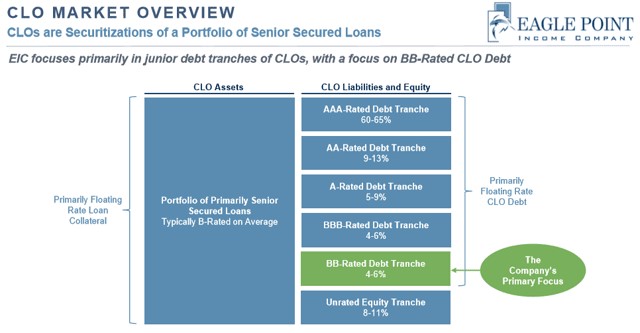

The figure below from an Eagle Point Investment Company presentation depicts typical CLO tranches:

The lower the position in the CLO cash flow “waterfall”, the higher the yield and the higher the risk of non-payment. The AA, A, and BBB debt tranches are all considered investment grade, though with higher risk and higher yields than the AAA tranche. The Eagle Point Investment Company happens to buy into the BB-rated debt tranche, which is just below investment grade. You, the public, can buy shares Eagle Point Investment (stock symbol EIC). These shares pay about 7% yield, after hefty management fees have been subtracted.

The equity tranche lies at the very bottom of the CLO heap. If there were, say, 20% loan defaults with only 50% recovery of the loans, the equity tranche might get completely wiped out. So these are more risky investments. As usual, there is high reward along with the risk. Oxford Lane Capital (OXLC) deals in CLO equity, and it will pay you about 15% per year, which is huge in today’s low-interest world. But….you need to be prepared to have the stock value cut in half every ten years or so, whenever there is a big hiccup in the financial world.

Anyone who was an economics-savvy adult during the GFC should be asking, “But, but, but…aren’t these CLOs essentially the same thing as the collateralized debt obligations (CDOs) that blew up the world in 2008?” The answer is partly yes, in that in both cases a bunch of loans get bundled together and then resliced into tranches. That said, we hope that the underlying loans in today’s CLOs are more robust than the massively shady home mortgage loans of 2003-2008 that fed into those CDOs. Back then, unscrupulous banks and mortgage companies handed out thousands of housing loans to ill-informed private individuals who did not remotely qualify for them, and then the banks dumped these loans out into the broader financial markets via CDOs. The bank loans behind today’s CLOs are more sober, serious, vetted affairs than those ridiculous subprime home mortgages.

This past summer, in the thick of the Covid shutdowns which have stressed small businesses, The Atlantic published a dire assessment of the potential for CLOs to sink the system, with the catchy title The Looming Banks Collapse . The article noted, fairly enough, that there has been a trend in the past few years to weaken the covenants on loans which would normally protect the lender against losses. Most loans these days are considered “covenant-lite”, compared to several years ago. There is genuine concern that the recovery on these loans might be more like 40-50%, instead of the historic 70-80%. On the other hand, the looser requirements on these loans may mean that fewer of them will technically violate these looser covenants and thus fewer companies will actually default. A recent survey estimates that the default rate in the $ 1.2 trillion dollar leveraged loan universe will peak at only 6.6% in 2021.

Also, today’s CLOs seem to be rated by the major ratings agencies more responsibly than the notoriously optimistic ratings given to CDO’s back in 2008. “CLOs are usually rated by two of the three major ratings agencies and impose a series of covenant tests on collateral managers, including minimum rating, industry diversification, and maximum default basket”, according to an article by S&P Global Market Intelligence. That article has a good description of CLOs, including a brief tutorial video on the nuts and bolts of how they work.

Corporations raise money in various ways to invest in their operation. A company may sell common stock to the public; the shareholders are not guaranteed any particular return on their investment, but if the company does well, the share price and the dividends paid by the stock can be expected to go up.

Preferred stock falls in between common stock and bonds. Investors mainly buy preferred stock for its dividends. Typically, the price of the preferred stock doesn’t go up like common stock can, but the company cannot pay any dividends on the common unless all of the promised dividends on the preferred are paid up.

CORPORATE BONDS: INVESTMENT GRADE AND JUNK

Companies can sell bonds to raise money. Bonds are somewhat standardized securities, which are marketed to the broad investing community. The company is legally bound to pay the interest, and eventually the principal, of a bond. Bonds are senior to stocks in case of extracting value from a company that has gone bankrupt. Some bonds are more senior than others, depending on the “covenants” in the fine print of the bond description (debenture). For smaller, less stable companies, the only way they may get someone to buy their bonds is to agree to certain conditions that make it more likely the bond will be repaid. For instance, the company selling the bond might be restricted from issuing more than a certain amount of total debt relative to its earnings, or from taking on additional debt which might be senior to its existing debt.

Bonds are rated by agencies such as Moody’s and Standard and Poor’s. Large, stable companies get high ratings (e.g. AA), and can pay lower interest. You, the public, can buy into investment grade bonds through funds such as iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD). This fund currently pays about 2.6%, but most of the returns in the past several years have been from an increase in the price of the fund shares. (For longer term bonds, the market price of a previously-issued bond increases as market interest falls, which it has in recent years).

The lowest investment grade is BBB. The bonds of shakier companies are rated at BB or lower, and have pay higher interest. This is called high yield debt or junk bonds. You can invest in junk bonds through funds such as JNK and HYG.

CORPORATE BANK LOANS

Companies also obtain loans from banks. Banks scrutinize the operations of the company to decide whether they want to risk their money in making a loan. Banks usually demand restrictions and guarantees to help ensure the loan will paid back. These restrictions are called covenants. Sometimes the payback of the loan is tied to a specified asset. For instance, if the income of a company falls below a certain level (which might imperil paying off the loan), the covenant may require the company to give ownership of some asset, like a building or a set of oil wells, to the bank, so the bank can sell it to pay back the loan immediately, before economic conditions worsen.

This graphic shows some of the conditions a company might have to sign to in order to get a loan from a bank:

Here is a summary of the differences between bonds and loans, courtesy of WallStreetMojo (slightly edited):

The main difference is that a bond is highly tradeable. If you purchase a bond, there is usually a market place where you can trade it. It means you can even sell the bond, rather than waiting for the end of the thirty years. In practice, people purchase bonds when they wish to increase their portfolio in that way. Loans tend to be the agreements between borrowers and the banks. Loans are generally non-tradeable, and the bank will be obliged to see out the entire term of the loan.

In the case of repayments, bonds tend to be only repaid in full at the maturity of the bond – e.g., 10, 20, or 30 years. With bank loans, both principal and interest are paid down during the repayment period at regular intervals (like a home mortgage).

Issuing bonds give the corporations significantly greater freedom to operate as they deem fit because it frees them from the restrictions that are often attached to the loans that are lent by the banks. Consider, for example, that lenders or the creditors often require corporates to agree to a variety of limitations, such as not to issue more debt or not to make corporate acquisitions until their loans are repaid entirely.

The rate of interest that the companies pay the bond investors is often less than the rate of interest that they would be required to pay to obtain the loan from the bank. Sometimes the interest on the loan is not a fixed percent, but “floats” with general short-term interest rates.

A bond that is traded in the market possesses a credit rating, which is issued by the credit rating agencies, which starts from investment grade to speculative grade, where investment-grade bonds are considered to be of low risk and usually have low yields. On the contrary, a loan don’t have any such concept; instead, the creditworthiness is checked by the creditor.

LEVERAGED LOANS

The rough equivalent of a junk bond in the world of corporate loans is called a “leveraged loan”. A leveraged loan is a type of loan that is extended to companies or individuals that already have considerable amounts of debt or poor credit history. Lenders consider leveraged loans to carry a higher risk of default, and so they demand higher interest on the loan. Leveraged loans and junk bonds play a key role in helping smaller or struggling companies achieve their financial goals. Leveraged loans are widely used to fund mergers and acquisitions.

Because the company itself is considered shaky, creditors typically require that the company offers some specific asset for collateral to “secure” the loan. Also, the loan is typically written to be “senior” to other debt, including bonds, in case of bankruptcy. Historically, the recovery rate for such senior secured loans has been about 80%, as compared to a recovery of about 40% for unsecured bonds, if the company goes bankrupt.

Typically, a bank would not want to take all the risk of such a loan upon itself. Therefore, for a leveraged loan, the bank arranges for a syndicate of multiple banks or other financial institutions to own pieces of the loan. You, too, can get a piece of this action by buying shares of the fund Invesco Senior Loan ETF (BKLN), which is currently yielding 3.2%.

S&P Global Market Intelligence offers a primer on leveraged loans, complete with tutorial videos. As shown below, the market for leveraged loans in the U.S. is now over $ 1 trillion: