Lately there has been lots of both good and bad news about the pandemic and its impact on the economy. But here’s once piece of good news you might have missed: the recession which began in February 2020 ended in April. And not April 2021… it ended in April 2020. At least, that’s according to the NBER Business Cycle Dating Committee, which made the announcement last week.

The 2020 recession of just 2 months is by far the shortest on record. NBER maintains a list of recessions with monthly dates going back to 1854 (there are annual business cycles dates before that, including important modern revisions of the original estimates, but the monthly series starts in 1854). In that timeframe, there have been 7 recessions in the 6-8 month range, but nothing this short. Still, it was mostly definitely a recession, as unemployment briefly spiked to levels not seen since the Great Depression. But only for 2 months. Keep in mind that the first part of the Great Depression last 43 months.

But how can this be? Is the recession really over? There are still about 6-7 million fewer people working than before the pandemic began. Lots of businesses are still hurting. The unemployment rate is still 2 full percentage points above pre-pandemic levels. How in the world can we say the recession ended 15 months ago?

To answer that question, it helps to know what NBER and most macroeconomists mean by a “recession” — essentially, it is used interchangeably with “contraction.” It means the economy, by a broad array of measures (NBER uses about 10 measures), is shrinking — or we might say, going in the wrong direction. The only other option, at least in the NBER chronology, is an expansion — when the economy is going in the right direction.

Does an economic expansion mean that everything is fine the economy?

No, of course it doesn’t. And no economist would pretend it means everything is fine. But it is useful to know the direction the economy is heading. It’s useful for public policy (although given the long lag in reporting, it’s not exactly super useful). It’s useful for the public to know. But probably most importantly, it’s useful for the historical record.

(You may be wondering why the NBER committee waiting so long to make the annoucement, even though it was pretty clear recovery started in April or May 2020 for quite some time. This is actually pretty normal. First, they want to make sure there isn’t a second contraction that’s really part of the same long contraction. Second, they want the best data to precisely date the month of the beginning of the expansion, and not have to revise it later on).

And in some sense, our current economic expansion is not that unusual. Look at the unemployment chart above. The shaded areas are the NBER recessions. Notice that the end of the recession is almost also right around the peak of unemployment. The end of a recession does not mean things are fine. It means things are getting better. But how long before the economy gets back to the pre-recession levels is an open question, and it can vary a lot.

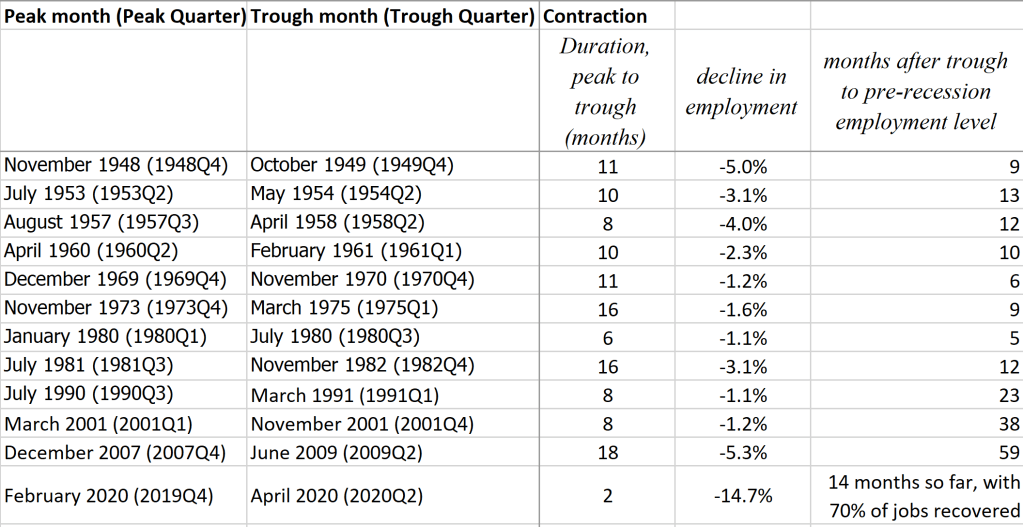

Or here’s another way to look at it, in the table below. Compared to most recessions in the post-WW2 period, 14 months would be a long time to wait to return to pre-recession employment levels. Usually after 12-13 months, the labor market is back to pre-recession levels or well above them. However, if we look at recent recessions, it typically takes much longer, even though most of the employment declines before 2020 were within normal historical ranges. Starting with the 1981 recession, each subsequent recovery took longer and longer to recover pre-recession employment levels: 1 year, 2 years, 3 years, 5 years!

And while the official employment data isn’t available until after the Great Depression, there are estimates which suggest it took about 7 years after the trough to achieve pre-recession employment levels (thanks in part to a subsequent recession in 1937-1938 before full recovery from the depths of the Depression). As before, comparisons to the Great Depression are mostly unwarranted, but it’s always a useful reminder of how bad things can really get in a perfect storm of a bad recession and poor public policy response.

OK, so if we’re now “going in the right direction” and have been so for 14-15 months, what comes next? When do we return to pre-recession employment levels? When do we return to a more “normal” economy and lifestyle? I am sorry dear reader, but I do not possess the answers to these questions. But we’ll continue to watch the data, be on the lookout for another secondary recessions that could occur, and just generally try to all muddle through our slow — but not really so slow given the particular details — economic expansion.