A blog post titled “The Death of Behavioral Economics” went viral this summer. The clickbait headline was widely shared. After Scott Alexander debunked it point-by-point on Astral Codex Ten, no one corrected their previous tweets. I recommend Scott’s blog for the technical stuff. For example, there is an important distinction between saying that loss aversion does not exist versus saying that its underlying cause is the Endowment Effect.

The author of the original death post, Hreha, is angry. Here’s how he describes his experience with behavioral economics.

I’ve run studies looking at its impact in the real world—especially in marketing campaigns.

If you read anything about this body of research, you’ll get the idea that losses are such powerful motivators that they’ll turn otherwise uninterested customers into enthusiastic purchasers.

The truth of the matter is that losses and benefits are equally effective in driving conversion. In fact, in many circumstances, losses are actually *worse* at driving results.

Why?

Because loss-focused messaging often comes across as gimmicky and spammy. It makes you, the advertiser, look desperate. It makes you seem untrustworthy, and trust is the foundation of sales, conversion, and retention.

He’s trying to sell things. I wade through ads every day and, to mix metaphors, beat them off like mosquitoes. Knowing how I feel about sales pitches, I don’t envy Hreha’s position.

I don’t know Hreha. From reading his blog post, I get the impression that he believes he was promised certain big returns by economists. He tried some interventions in a business setting and did not get his desired results or did not make as much money as he was expecting.

According to him, he seeks to turn people into “enthusiastic purchasers” by exploiting loss aversion. What would consumers be losing, if you are trying to sell them something new? I’m not in marketing research so I should probably just not try to comment on those specifics. Now, Hreha claims that all behavioral studies are misleading or useless.

The failure to replicate some results is a big deal, for economics and for psychology. I have seen changes within the experimental community and standards have gotten tougher as a result. If scientists knowingly lied about their results or exaggerated their effect sizes, then they have seriously hurt people like Hreha and me. I am angry at a particular pair of researchers who I will not name. I read their paper and designed an extension of it as a graduate student. I put months of my life into this project and risked a good amount of my meager research budget. It didn’t work for me. I thought I knew what was going to happen in the lab, but I was wrong. Those authors should have written a disclaimer into their paper, as follows:

Disclaimer: Remember, most things don’t work.

I didn’t conclude that all of behavioral research is misleading and that all future studies are pointless. I refined my design by getting rid of what those folks had used and eventually I did get a meaningful paper written and published. This process of iteration is a big part of the practice of science.

The fact that you can’t predict what will happen in a controlled setting seems like a bad reason to abandon behavioral economics. It all got started because theories were put to the test and they failed. We can’t just retreat and say that theories shouldn’t get tested anymore.

I remember meeting a professor at a conference who told me that he doesn’t believe in experimental economics. He had tried an experiment once and it hadn’t turned out the way he wanted. He tried once. His failure to predict what happened should have piqued his curiosity!

There is a difference between behavioral economics and experimental economics. I recommend Vernon Smith’s whole book on that topic, which I quoted from yesterday, for those interested.

The reason we run experiments is that you don’t know what will happen until you try. The good justification for shutting down behavioral studies is if we get so good at predicting what interventions will work that the new data ceases to be informative.

Or, what if you think nudges are not working because people are highly sensible and rational? That would also imply that we can predict what they are going to do, at least in simple situations. So, again, the fact that we are not good at predicting what people are going to do is not a reason to stop the studies.

I posted last week about how economists use the word “behavioral” in conversation. Yesterday, I shared a stinging critique of the behavioral scientist community written by the world’s leading experimental researcher long before the clickbait blog.

Today, I will share a behavioral economics success story. There are lots of papers I could point to. I’m going to use one of my own, so that readers could truly ask me anything it. My paper is called “My reference point, not yours”.

I started with a prediction based on previous behavioral literature. My design depended on the fact that in the first stage of the experiment, people would not maximize expected value. You never know until you run the experiment, but I was pretty confident that the behavioral economics literature was a reliable guide.

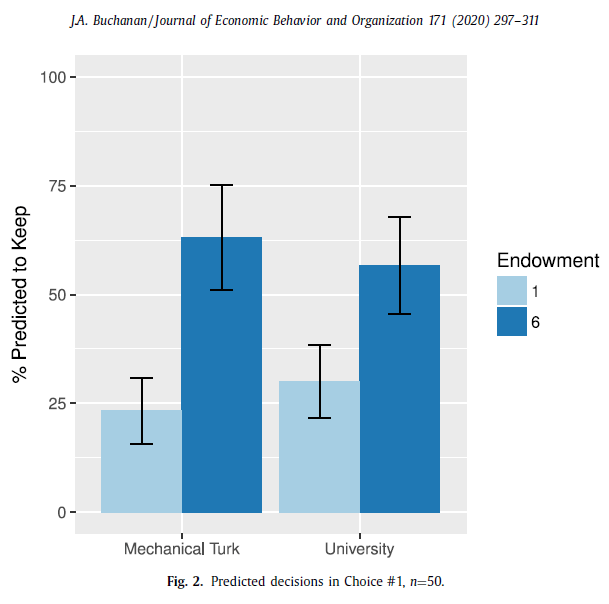

Some subjects started the experiment with an endowment of $6. Then they could invest to have an equal chance of either doubling their money (earn $12) or getting $1. To maximize expected value, they should take that gamble. Most people would rather hold on to their endowment of $6 than risk experiencing a loss. It’s just $5. Why should the prospect of losing $5 blind them to the expected value calculation? Because most humans exhibit loss aversion.

I was relying on this pattern of behavior in stage 1 of the experiment for the test to be possible in stage 2. The main topic of the paper is whether people can predict what others will do. High endowment people fail to invest in stage 1, so then they predict that most other participants failed to invest. The high endowment people failed to incorporate easily available information about the other participants, which is that starting endowments {1,2,3,4,5,6} were randomly assigned and uniformly distributed. The effect size was large, even when I added in a quiz to test their knowledge that starting endowments are uniformly distributed.

Here’s a chart of my main results.

Investing always maximizes expected value, for everyone. The $1 endowment people think that only a quarter of the other participants fail to invest. The $6 endowment people predict that more than half of other participants fail to invest.

Does this help Mr. Hreha get Americans to buy more stuff at Walmart, for whom he consults? I’m not sure. Sorry.

My results do not directly imply that we need more government interventions or nudge units. One could argue instead that what we need is market competition to help people navigate a complex world. The information contained in prices helps us figure out what strangers want, so we don’t have to try to predict their behavior at all.

Here’s the end of my Conclusion

One way to interpret the results of this experiment is that putting yourself in someone else’s shoes is costly. We often speak of it as a moral obligation, especially to consider the plight of those who are worse off than ourselves. Not only do people usually decline to do this for moral reasons, they fail to do it for money. Additionally, this experiment shows that, if people are prompted to think about a specific past experience that someone else had, then mutual understanding is easier to establish.

I’m attempting to establish general purpose laws of behavior. I’ll end with a quote from Scott Alexander’s reply post.

A thoughtful doctor who tailors treatment to a particular patient sounds better (and is better) than one who says “Depression? Take this one all-purpose depression treatment which is the first thing I saw when I typed ‘depression’ into UpToDate”. But you still need medical journals. Having some idea of general-purpose laws is what gives the people making creative solutions something to build upon.

Argh, there went an hour of my morning…that Scott Alexander article was so good I read it all, and even got sucked into reading links therein…

Anyway, he nailed it – – (properly done) studies clearly do show loss aversion. There is legitimate debate, however, on whether this behavior is due to a generic “loss aversion” human trait, or whether each specific observed instance of loss aversion can be more elegantly correlated with some other, more generalizable human trait(s).

I was impressed by his knowledge of the history of science, as shown by this apt analogy he used”

“loss aversion is real, but not fundamental, like centrifugal force in physics.”

LikeLiked by 1 person