People have expectations about the world. When those expectations are violated, they usually change their behavior in order to account for the new information (on the margin at least). Does unexpected inflation affect people’s behavior? Of course. William Phillips thought so (the famous version of the Phillips Curve assumes constant inflation expectations).

Macroeconomists often separate the world into reals and nominals. Sometimes we produce more and other times we produce less. Those are the reals. The prices that we pay and the money that we spend are the nominals. There is what’s sometimes called a ‘loose joint’ between reals and nominals. That is, they do not move in tandem, nor are they entirely independent. If the Fed suddenly slows the growth of the money supply, then economic activity growth might also slow – but not by the same amount. In the long run, reals and nominals are largely independent. Whether we have 2% vs 3% annual inflation over the course of some decade is probably not important for our real output at the end of that decade.

It Takes Two to Tango.

It is often said that the Fed can achieve any amount of total spending in the economy that it prefers. It can achieve any NGDP. But, the Fed doesn’t control NGDP as a matter of fiat. The Fed changes interest rates and the money supply in order to change the total spending in our economy. Importantly, the effect of Fed policy changes is contingent on how the public reacts. After all, the Fed can increase the money supply. But it is us who decides how much to spend.

MV=PY=NGDP

Economists call this rate of spending ‘velocity’. The public controls the V in MV=PY. The Fed controls the M. Together, we determine the total spending in the economy. Whereas principles of macroeconomics books like to keep separate the reals and the nominals, the fact that our behaviors affect both should give us pause. They are not entirely separate. They are a loose joint. But just as the Fed can adjust total spending contingent on how people behave, people adjust their behavior contingent on the policies of the Fed. Kydland and Prescott played this out using game theory to conclude that people will adjust their behavior by changing prices rather than changing output when there are changes in total spending.

Fool me once, Shame on you

If money isn’t a production input, then the extent by which inflation expectations are mistaken mimics the extent to which people will engage in economic miscalculation. If people expect the prices at which they purchase to be higher tomorrow, then they will increase the prices at which they sell today. If our expectations are wrong, then we misprice today and sell an amount that we would not have chosen had we known better.

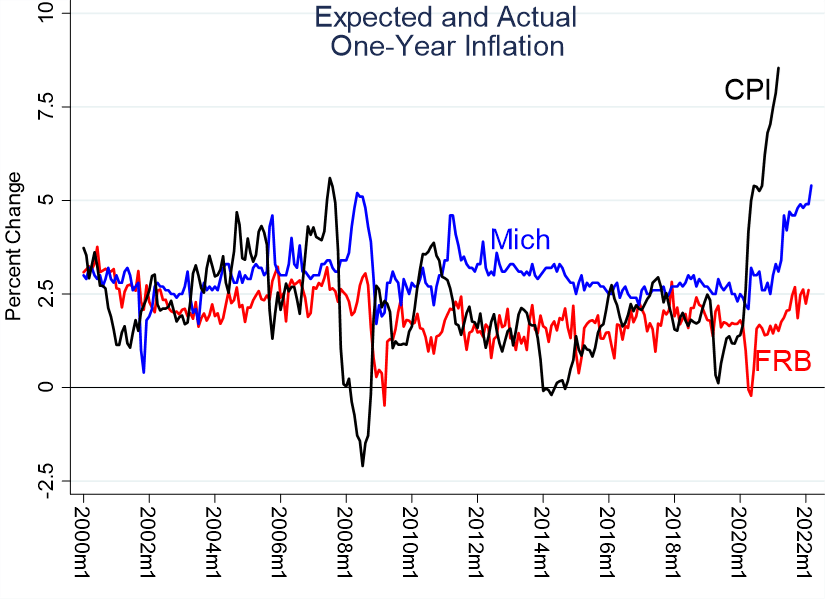

What does this look like in real life? The Federal Reserve Bank of Cleveland and University of Michigan both publish measures of expected inflation at the one-year horizon. The Fed’s estimate is calculated by experts. The University of Michigan uses a consumer survey. Looking at the graph below, it looks like consumers almost always say that they expect higher inflation than do the experts.

But, we are interested in the unexpected inflation, the gaps between the forecasts and the actual inflation. Below are how the FRB and the Michigan forecasts differ relative to the actual 1-year forward CPI change. Consumers forecasts are more erratic. Also, when consumers overestimate inflation, it’s by more than the FRB. When the FRB underestimates inflation, it’s by more than consumers.

Finally, we care about unexpected inflation because of its impact on economic miscoordination. When people over or underestimate inflation, it’s supposed to affect the real side of the economy. That’s why we care. Otherwise, we don’t much mind what consumer inflation expectations are. In terms of welfare, we care about real people and real behavior. Not about the stories that people weave for themselves in their head, which may or may not have bearing on reality. Do wrong inflation expectations matter? Below is the graph of unexpected inflation and the 12-month forward real consumption growth rate. What do you see?

Personally, I see not a whole lot. Like, maybe there’s something negative with a lag, but it’s hard to tell. Examining the coefficients from a simple VAR reveals the lagged correlations. You know what’s awkward? Real consumption growth isn’t predicted at all by unexpected inflation. You know what’s awkward still further? Unexpected inflation is predicted by real consumption growth. People don’t seem to have a very good idea of what inflation will be. They look around at current conditions, and then they take a stab at predicting future.

What are we to conclude? Do inflation expectations not matter at all? Unfortunately, this exercise illustrates the temptation of statistical hubris. It’s possible that inflation expectations don’t matter. It’s also possible that I’ve chosen a poor measure. Maybe, consumers are pretty good at inflation expectations, but not at the 1-year horizon. Maybe they’re good at predicting at the four-month horizon. Finally, maybe the Federal Reserve responds to inflation expectations and unexpected inflation. Maybe, the effect of unexpected inflation is being papered over by changes in the money supply and NGDP. That is the Fed’s job after all, to smooth over economic fluctuations.

Very interesting!

LikeLike