In the US wealth distribution, which group has seen the largest increase in wealth during the pandemic? A recent working paper by Blanchet, Saez, and Zucman attempts to answer that question with very up-to-date data, which they also regularly update at RealTimeInequality.org. As they say on TV, the answer may shock you: it’s the bottom 50%. At least if we are looking at the change in percentage terms, the bottom 50% are clearly the winners of the wealth race during the pandemic.

Average wealth of the bottom 50% increased by over 200 percent since January 2020, while for the entire distribution it was only 20 percent, with all the other groups somewhere between 15% and 20%. That result is jaw-dropping on its own. Of course, it needs some context.

Part of what’s going on here is that average wealth at the bottom was only about $4,000 pre-pandemic (inflation adjusted), while today it’s somewhere around $12,000. In percentage terms, that’s a huge increase. In dollar terms? Not so much. Contrast this with the Top 0.01%. In percentage terms, their growth was the lowest among these slices of the distribution: only 15.8%. But that amounts to an additional $64 million of wealth per adult in the Top 0.01%. Keeping percentage changes and level changes separate in your mind is always useful.

Still, I think it’s useful to drill down into the wealth gains of the bottom 50% to see where all this new wealth is coming from. In total, there was about $2 trillion of nominal wealth gains for the bottom 50% from the first quarter of 2020 to the first quarter of 2022. Where did it come from?

I’ll stick with nominal dollars throughout this analysis. While inflation-adjusted numbers are better for judging real gains in wealth, if we are interested in divvying up the increase, it doesn’t matter, since we’d be adjusting everything by the same inflation factors.

We can use the Fed’s Distributional Financial Accounts to get a sense of what is causing the $2 trillion increase in wealth. The most current data in that dataset is for the first quarter of 2022, but as the Blanchet, Saez, and Zucman real-time estimates suggest, there hasn’t been a huge change to wealth for the bottom 50% in the months since the first quarter ended. This is despite the downturn in the stock market in 2022 (you’ll see why in a moment).

Wealth is the difference between assets and liabilities. So it’s useful to look at these categories separately (though some items from each category clearly go together, such as the asset of real estate and the liability of mortgage debt).

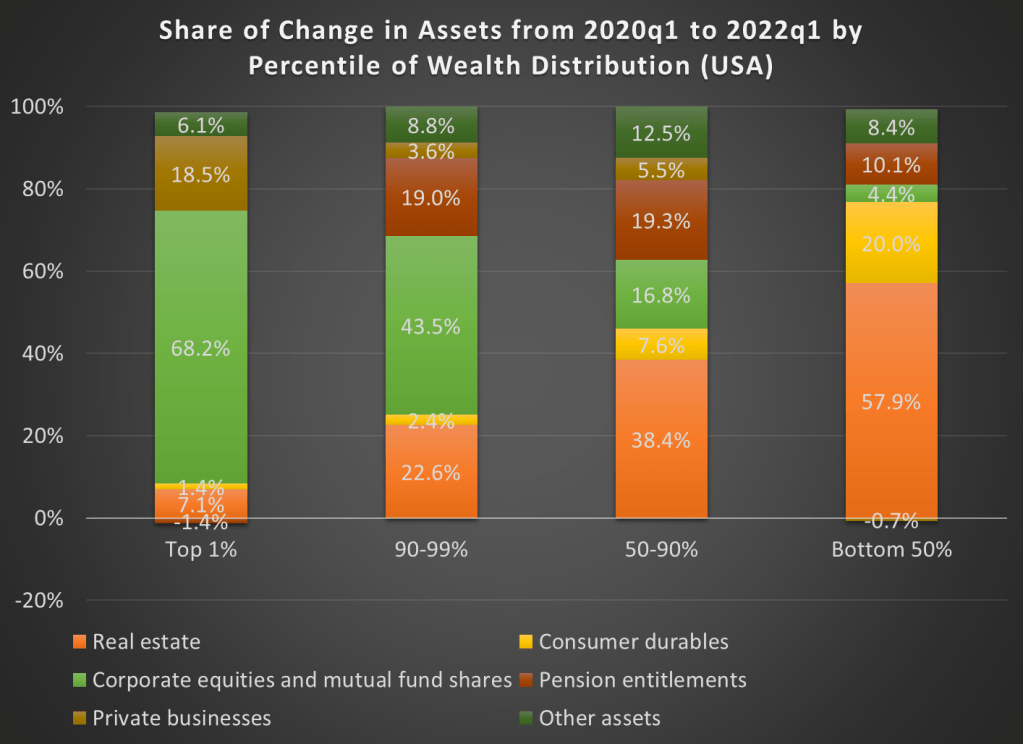

Total assets for the bottom 50% rose by about $2.8 trillion in the past 2 years. Of this increase, the bulk has been from Real Estate assets, which increased by $1.6 trillion, or about 58% of the total. Real estate constitutes just a bit over half of the total assets of the bottom 50%. Consumer durables (cars, appliances, furniture, etc.) also saw a big increase, comprising about 20% of the total increase in assets. Pension entitlements (which includes both DB and DC plans, but not Social Security and other government programs) also saw a decent increase, contributing 10% of the total increase in assets.

And… that’s about it for major categories of assets. Ownership of shares of stock and mutual funds (outside of pensions) saw a negligible increase of about 4 percent for the bottom 50%, but that’s for an important reason: the bottom 50% don’t own much in terms of stocks: it’s only about 3% of their total assets. Contrast this with the top 1%, who hold almost half of their total assets in the stock market.

On the liabilities side, there was an increase of $0.7 trillion for the bottom 50% (that’s how we get to a net increase in wealth of $2 trillion). The Fed DFA data only provides three categories of liabilities, and for the bottom 50% here’s how the increase in the past 2 years breaks down: 60% from mortgage debt, 25% from consumer credit, and 15% “other liabilities.” There is a further breakdown of the “other” category, but unfortunately we don’t get a breakdown for one category that has generated a lot of interest lately: student loan debt. It is lumped in with “consumer credit.”

(Note: we can get more information on student loans from the Fed’s Survey of Consumer Finance, the baseline for the DFA, but it is only available for 2019 right now. About 30% of those in the bottom 50% held student debt, with an average of debt level of $54,000 of the bottom 25% and $28,000 for the next 25%. Those averages are only among those that held student debt, and medians are quite a bit lower at $32,000 and $17,000.)

We can combine the asset and liability categories to some extent. For example, if we combine real estate and mortgage debt, we see that the net increase was about $1.7 trillion, meaning that net home values contributed 57% of the increase in overall net worth for the bottom 50%. In other words, using the “net home value” metric gives us a similar percent increase to just looking at the asset side of home values. It’s not just an increase in debt that fueled this increase in assets, but a real appreciation in home values.

Finally, what about the other parts of the income distribution above the 50th percentile? What asset classes contributed the most to their growth in wealth since the beginning of 2020? The chart below answers those questions.

As I explained above, stock market wealth was clearly the biggest component for the top 1%, and it also we for the remainder of the top 10%. For the 50-90% percentiles of wealth, the growth was from across all different asset classes. While real estate assets were the biggest contributor to their asset growth, the sum of stock market equity and pensions (which also includes stocks) was almost as large as the real estate growth.

One thing to keep in mind with real estate wealth: it’s clearly an important part of the overall wealth picture in the US, especially once you get past the top 1%. Of the total personal assets in the US, about 25% of it is in real estate. But for those that don’t currently own a home, the rise in real estate prices is not a boon to them. In fact, it’s a huge cost, as this both raises the cost of purchasing their first home, and the real estate appreciation is feeding into higher rent payments for non-homeowners. I don’t really know what to say about it past that, since the price of anything rising is both good (for the owners of the asset) and bad (for the potential buyers of the asset), but it’s an important factor to keep in mind when thinking about wealth in the US today.

Excellent analysis as always.

LikeLike

These are averages, so… for the bottom 50% who are homeowners, the increase of wealth from home ownership must be even greater, while their non-homeowning peers are even more cut off from the housing market. “Homeowner vs renter” may become as significant a political divide as “rich vs poor”.

LikeLike