Yesterday Federal Reserve researcher Nathan Blascak presented a paper at my Economics Seminar Series that was a surprise hit, with the audience staying over 40 minutes past the end to keep asking questions. So today I’ll share some highlights from the paper, “Decomposing Gender Differences in Bankcard Credit Limits”.

The challenge here is that its hard to get data that includes both gender and credit card limits (its illegal to use gender as a basis for allocating credit, so credit card companies don’t keep data on it, as they don’t want to be suspected of using it). The paper is original for managing to do so, by merging three different datasets. But even this merged data only lets them do this for a fairly specific subgroup- Americans who hold a mortgage solely in their name (not jointly with a spouse). Even this limited data, though, is quite illuminating.

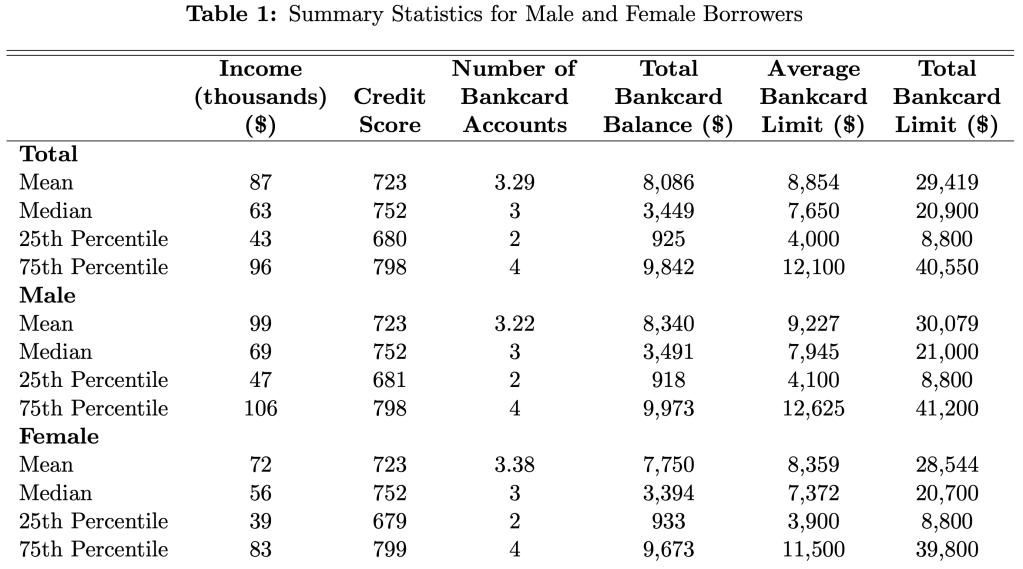

Their headline result is that men have 4.5% higher credit limits than women. Women actually have slightly more credit cards (3.38 vs 3.22), but have lower limits on each card; summing up their total credit limit across all cards yields an average of $28,544 for women vs $30,079 for men.

Two of the big factors that determine limits, and so could cause this difference, are credit scores and income. The table above shows that men and women have remarkably similar credit scores, while men have higher incomes. Still, when the paper tries to predict credit limits, controlling for credit scores, incomes, and other observables explains only about 13% of the gender gap.

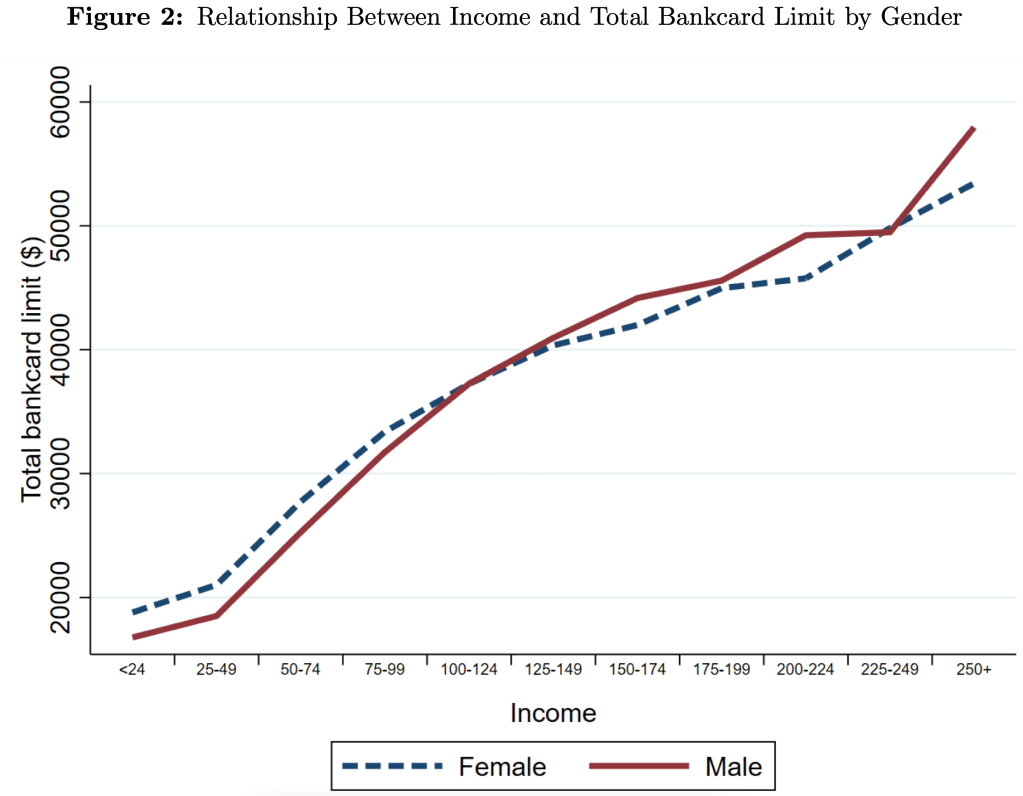

Men have 4.5% higher credit limits on average, but this difference varies a lot across the distribution. For credit scores, the gap is narrow in the middle but bigger at the extremes. For income, we see that men get higher limits at higher incomes, but women actually get higher limits at lower incomes- and not just “low incomes”, women do better all the way up to $100,000/yr:

The papers data covers 2006-2018, so they also show all sorts of interesting trends. The average number of credit cards held by men and women plunged after the 2008 recession and remains well below the peak. Total credit limits plunged too, though they were almost totally recovered by 2018.

There’s lots more in the paper, which is a great example of the value of descriptive work with new data. If anything I’d like to see the authors push even harder on the distribution angle. Its nice to see how limits vary across all incomes and credit scores, but why not show the full distribution of credit card limits by gender? My guess is that the 1st and 99th percentiles are very interesting places, because there’s all sorts of crazy behavior at the extremes. Finally, I wonder if higher limits are actually a good thing once you get beyond a relatively low amount- do you know of anyone who ever had a good reason to get their personal credit card balances over $20,000?

I would have thought that women would generally be thought of as lower risk than men. Also that So what’s the difference? Higher debt? More likely to be single earner? Risk aversity (less likely to apply for a higher credit balance)?

LikeLike