Much of what economics has to say about tariffs comes from microeconomic theory. But it’s mostly sectoral in nature. Trade theory has some insights. But the effects on the whole of an economy are either small, specific to undiversified economies, or make representative agent assumptions that avoid much detail. Given that the economics profession has repeatedly said that the Trump tariffs would contribute to inflation, it seems like we should look at the historical evidence.

Lay of the Land

Economists say things like ‘competition drives prices closer to marginal cost’. Whether the competitor lives abroad is irrelevant. More foreign competition means lower prices at home. But that’s a partial equilibrium story. It’s true for a particular type of good or sector. What happens to prices in the larger economy in seemingly unrelated industries? The vanilla thinking that it depends on various elasticities.

I think that the typical economist has a fuzzy idea that the general price level will be higher relative to personal incomes in some sort of real-wages and economic growth mental model. I don’t think that they’re wrong. But that model is a long-run model. As we’ve discovered, people want to know about inflation this month and this year, not the impact on real wages over a five-year period.

Part of the answer is technical. If domestic import prices go up, then we’ll sensibly see lower quantities purchased. The magnitude depends on the availability of substitutes. But what should happen to total import spending? Rarely do we talk about the expenditure elasticity of prices. Rarely do we get a simple ‘price shock’ in a subsector. It’s unclear that total spending on imports, such as on coffee, would rise or fall – not to mention the explicit tax increase. It’s possible that consumers spend more on imports due to higher prices, or less due to newly attractive substitutes. The reason that spending matters is that it drives prices in other parts of the economy.

For example, I argued previously that tariffs reduce dollars sent abroad (regardless of domestic consumer spending inclusive of tariffs) and that fewer dollars will return as asset purchases. I further argued that uncertainty makes our assets less attractive. That puts downward pressure on our asset prices. However, assets don’t show up in the CPI.

According to the above discussion, it’s unclear whether tariffs have a supply or demand impact on the economy. The microeconomics says that it’s a supply-side shock. But the domestic spending implications are a big question mark.

What is a Tariff Shock?

That’s the title of a recent working paper from the Federal Reserve Bank of San Francisco. It’s a fun paper and I won’t review the entirety. They start by summarizing historical documents and interpreting the motivation of tariffs going back to 1870. They argue that tariffs are generally not endogenous to good or bad moments in a business cycle and they’re usually perceived as permanent. The authors create an index to measure tariff rates.

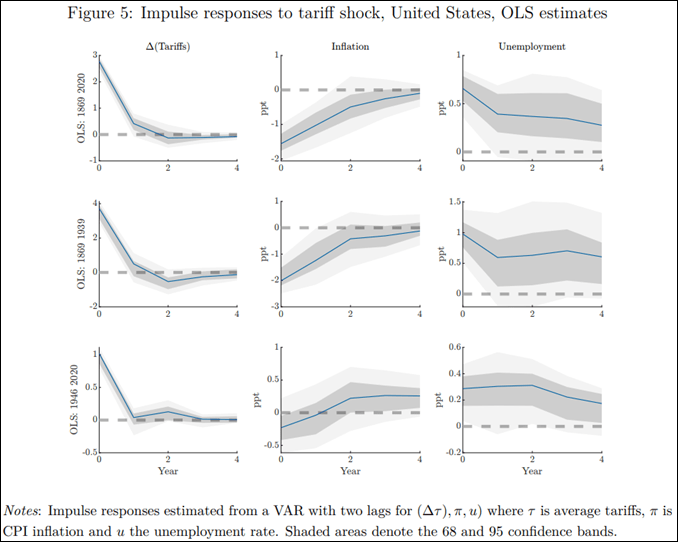

Here’s the fun part. They run an annual VAR of unemployment, inflation, and their measure of tariffs. Unemployment in negatively correlated with output and reflects the real side of the economy. Along with inflation, we have the axes of the Aggregate Supply & Aggregate Demand model. Tariffs provide the shock – but to supply or demand?. Below are the IRF results:

What does it mean?

A tariff shock is an unanticipated rise in tariffs. They measure the impact unexpected tariffs on inflation and unemployment over 3 periods: post WWII (bottom), pre WWII (middle), 1869-2020 (top). The results show that a surprise increase in tariffs result in an initially negative impact on inflation and a positive impact on unemployment. If tariffs had an immediately negative productivity impact, then we’d observe higher prices. Instead, the lower prices make tariffs look more like a negative aggregate demand shock. WHAT?!

How does that work?

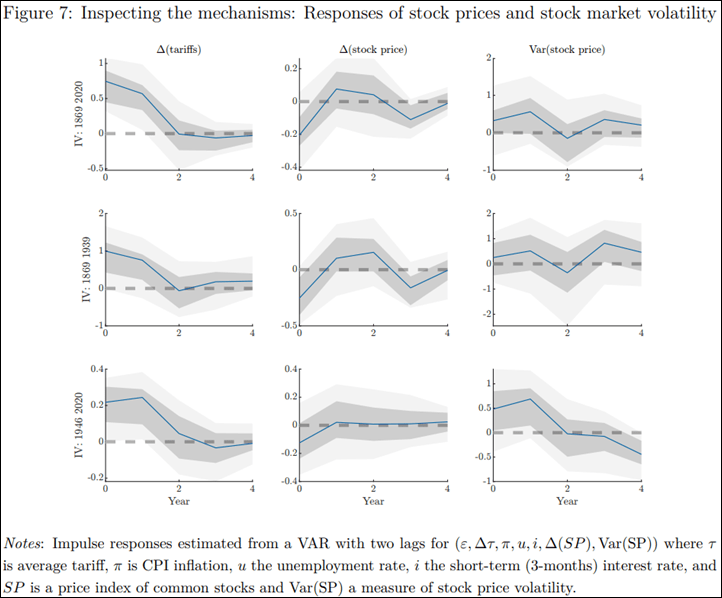

The authors speculate two mechanisms. First, greater domestic uncertainty can cause individuals to hold back on all spending until the world looks more stable and predictable. It’s as if major policy changes of any sort cause demand to fall until the relative price effects of the shock are better known. On the investor side, managers wait before making big project investments until they have a better idea of what the returns will be. A second mechanism is that uncertainty reduces the expected value of assets and consumers experience a negative wealth shock, reducing their willingness to consume in lieu of saving. The authors measure another VAR that includes tariffs, a stock index level, and stock index volatility. They find evidence for the wealth effect at all times and stronger evidence for the uncertainty effect in the modern era.

Like I said, the authors do more than I cover here. But I buy it. New tariffs disrupt trade and reduce certainty about future relative prices and harm economic coordination. People reduce their total spending and that has macroeconomic effects on prices and employment – even in the non-trade sectors of the economy. Just so we’re clear, tariff shocks aren’t benign to the domestic economy, even in non-tradable sectors. Hikes and cuts have real effects and should not be adjusted with levity.

Barnichon, Régis and Aayush Singh. 2025. “What Is a Tariff Shock? Insights from 150 years of Tariff Policy.” Federal Reserve Bank of San Francisco Working Paper 2025-26. https://doi.org/10.24148/wp2025-26

A small caveat: if your economy has a halfway competent central bank that targets inflation, than nothing, no shock no anything, will have any systematic, measurable impact on inflation. Especially if market participants anticipate the central bank’s actions.

Very similar to when you set your Aircon to 15C, the room will stat at 15C, even if you light a few candles: the aircon will just work a bit harder and your electricity bill will go up.

LikeLike

You’re absolutely right. However, the Fed does not have a single target. Even targeting prices or aggregate demand, they can’t control them perfectly from moment to moment. So brief shocks can occur hopefully not on the order of years (just like with your AC). Baker Bloom and Davis found that uncertainty shocks affect employment and output negatively, though I don’t recall them saying what happened to CPI that was during the great moderation and gfc when the fed said that it was inflation targeting.

LikeLike