Alex Tabarrok noted in Oil versus Ice Cream that he and Tyler, as textbook authors, “chose the oil market as our central example. Oil is always in the news…”

when a student sees that the price of crude has surged past $100 a barrel because Iran closed the Strait of Hormuz—choking off 20% of the world’s oil supply—they have the framework to understand what is happening. Supply shock, inelastic demand, expectations and speculation, the macroeconomic transmission to GDP—it’s all right there in the headlines.

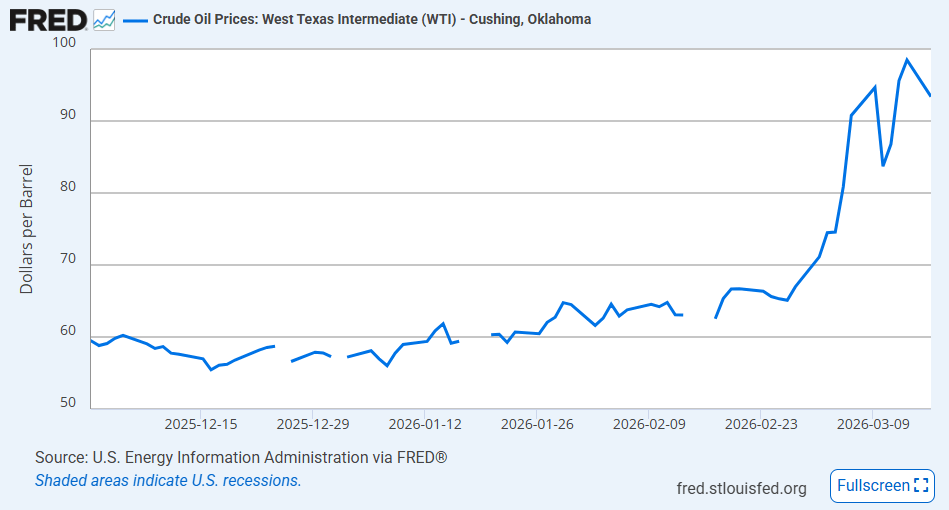

In a classroom, a good way to begin is to ask the students to tell you what they have noticed recently about oil or gas prices. Having the students obtain the oil price data themselves could be fun, if you are in an environment with screens/computers.

A data source for undergrads is the FRED chart for WTI crude oil prices. It is clean and easy to explain in class. An instructor with slides could pull this up in real time. https://fred.stlouisfed.org/series/DCOILWTICO

Ask students: “Is this price change primarily explained by

- Increase in demand

- Decrease in demand

- Increase in supply

- Decrease in supply

Correct answer: d. Decrease in supply

If you cover elasticity, this is especially helpful as an example. “Why would the price jump more when demand is inelastic?”

It’s not too late to work this into a lesson plan for the Spring 2026 semester, economic teachers. I might use it to illustrate supply shocks next week.

This event is a classic example of a negative supply shock: a disruption in the Strait of Hormuz would reduce the amount of oil reaching world markets, pushing energy prices sharply upward. Because oil is an important input for transportation, manufacturing, and heating, higher oil prices raise costs across much of the economy. Firms may cut production, households may spend more on gasoline and utilities and less on other goods, and overall economic activity can slow. That is why economists worry that large oil supply shocks can contribute to recessions. They do not just make one product more expensive; they can ripple outward, reducing real income, lowering consumer confidence, and weakening GDP growth while inflation rises.

Related posts. The whole crew showed up this month:

James from March 12: Is a US Oil Export Ban Coming?

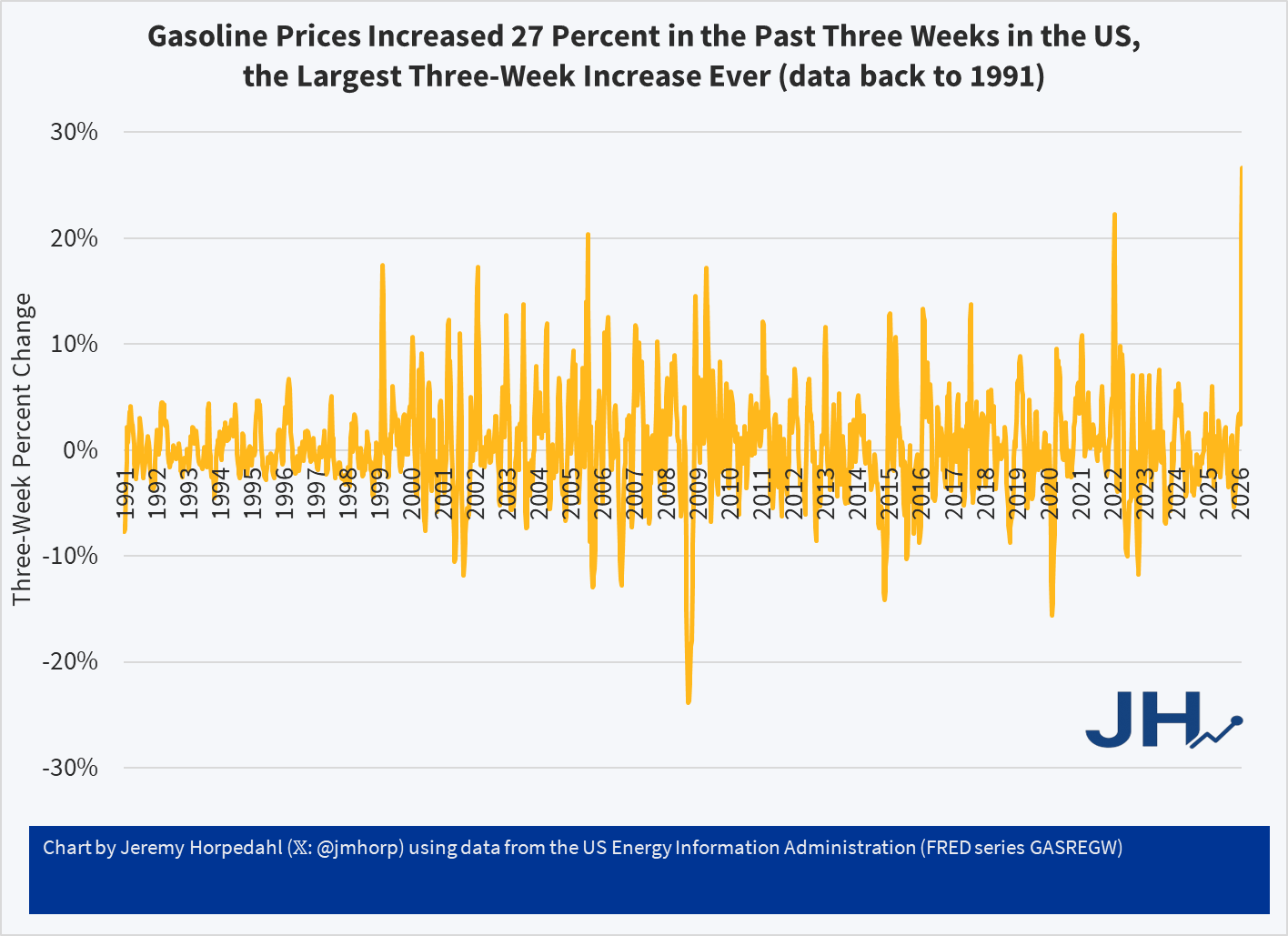

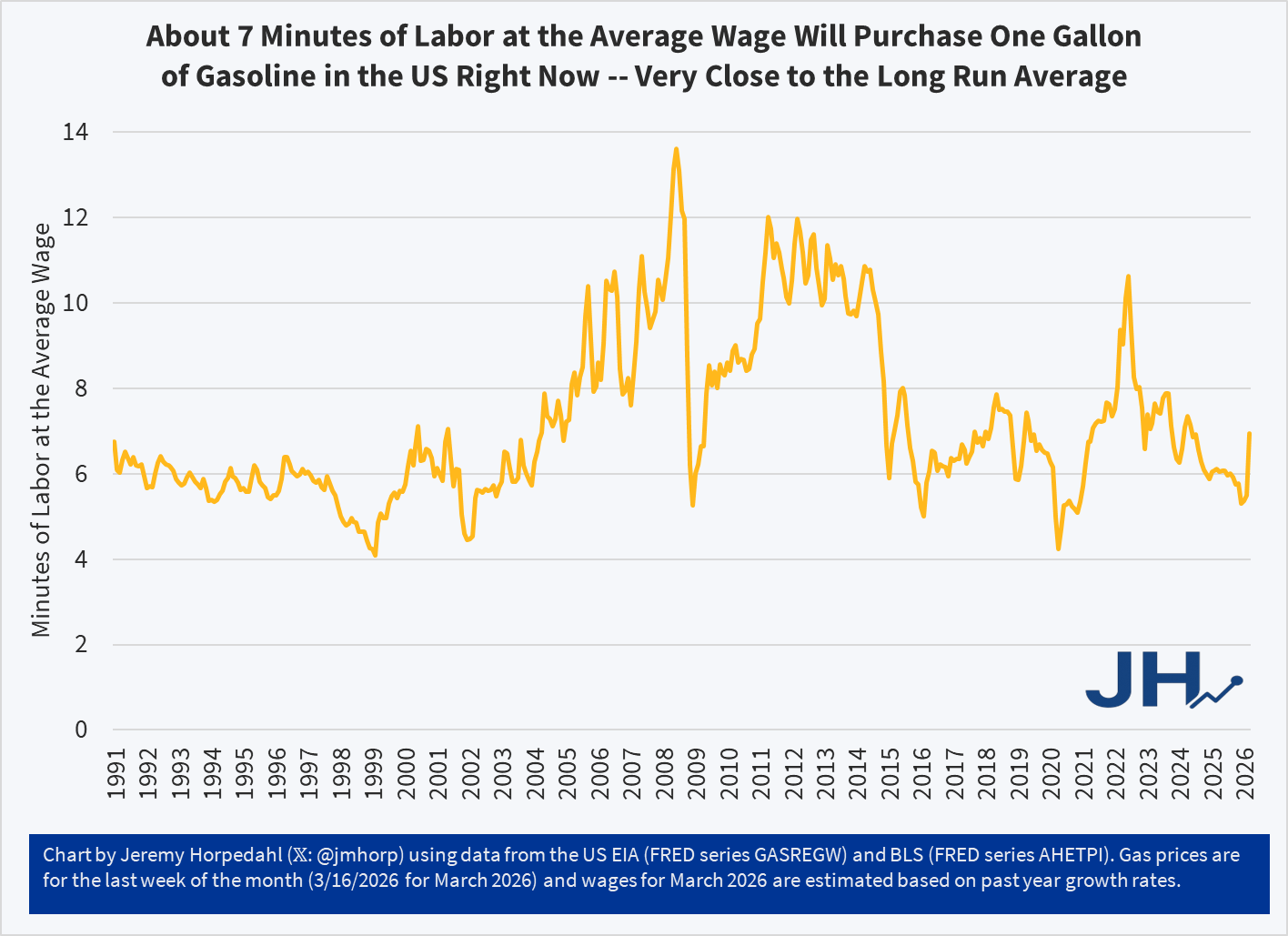

Jeremy from March 18: Gasoline Prices Have Increased at Record Rates, but Remain At About Average Levels of Affordability

Tyler from March 22: How much more will oil prices have to go up?

MattY from March 24: Why hasn’t oil gotten even more expensive?

Austin Vernon: https://www.austinvernon.site/blog/thestrait.html