Public choice economists emphasize the process by which we select political leaders. Electoral and voting rules influence the type of leaders we get. Institutional economists agree and go one step further. Who we choose matters less than the environment we place them in. Leaders, regardless of their personal qualities, respond to the incentives that surround them. The ultimate policies, therefore, largely conform to those incentives. From this perspective, it’s important to adopt institutional incentives for leaders to promote policies oriented toward economic growth and provide the option to flourish.

The same principle applies to the private economy. Productivity is crucial, and higher IQ often correlates with greater productivity. Yet, genetic endowment—including IQ—is beyond individual control. Many other determinants of productivity are not exogenous when we can affect policy. Let’s adopt policies that allow individuals with lower IQ to act productively as if they had higher IQ. Protecting the freedom to contract and private property rights creates conditions whereby even those at the lower end of the cognitive ability distribution can thrive. These principles expand their opportunities. Market signals give them valuable feedback on their activities and enable them to contribute to the economy.

I offer a cleaned version of the state-level NSDUH in Stata .dta and Excel .xlsx formats here.

The NSDUH is mostly quite good as government datasets go- they share individual-level data in many formats and with the option to get most years together in a single file. But due to privacy concerns, the individual-level data doesn’t tell you what state people live in, which means it can’t be used to study things like state policy. SAMHSA does offer a state-level version of their data, but it is messy and only available in SAS format. So I offer the 1999-2019 state-level NSDUH Small Area Estimation Dataset in Stata .dta and Excel .xlsx formats here.

If you have Stata I recommend using that version, since the variables are labelled, making it much easier to understand what they represent.

This is the latest addition to my data page, where you can find cleaned/improved versions of other government datasets.

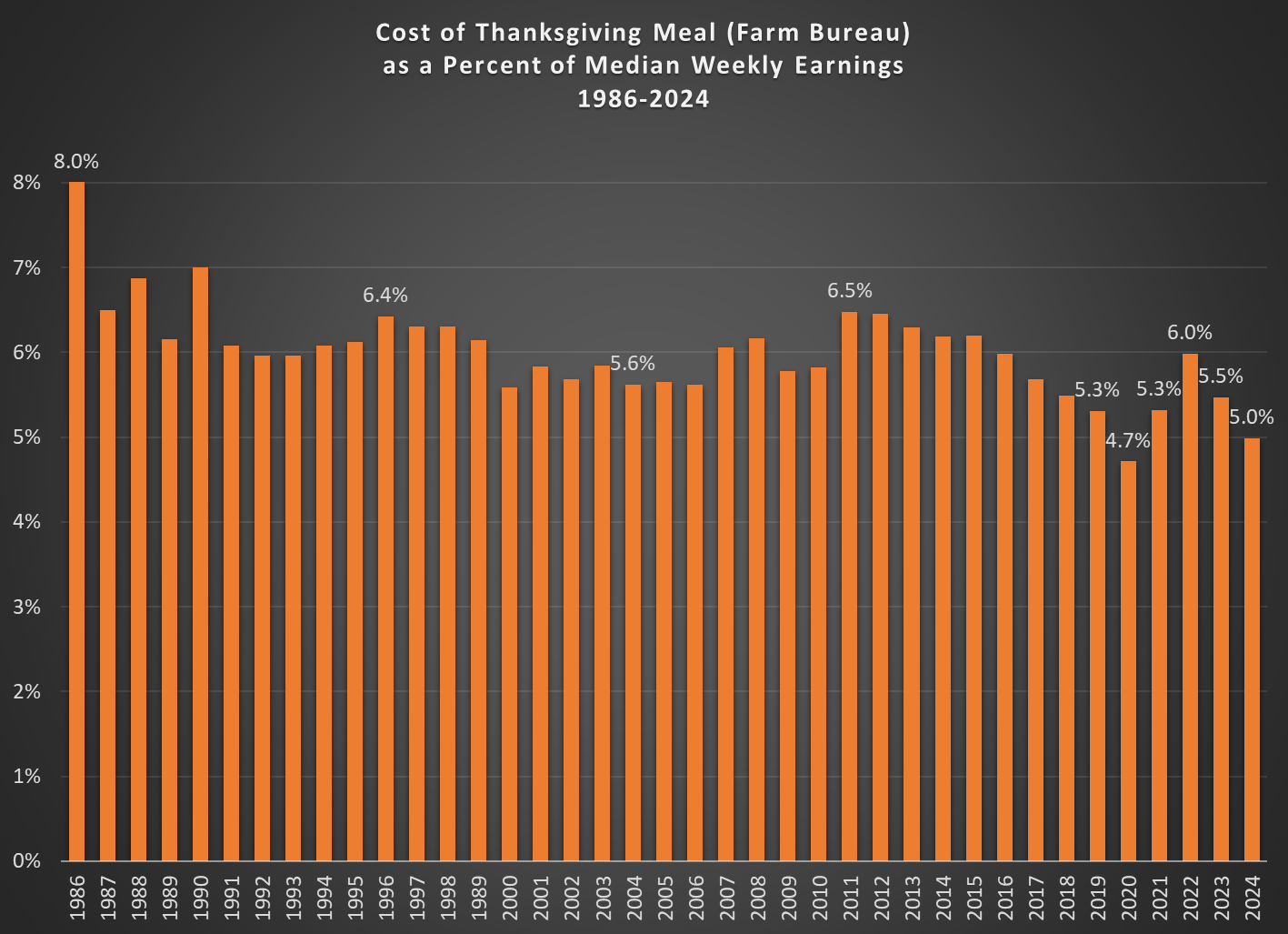

Farm Bureau has released their annual data on the cost of a Thanksgiving meal. The headline is that this meal has declined, in nominal terms, for 2 years in a row — back-to-back years of roughly a 5 percent decline. That’s good news for consumers. But they note it’s not all good news, because the meal is still 19 percent higher than 2019, “which highlights the impact inflation has had on food prices – and farmers’ costs – since the pandemic.”

However, the news is even better than they say. If we compare the price of this meal to median earnings, it is actually cheaper than it was in 2019. It’s now the second most affordable Thanksgiving on record, and the only lower year was 2020 — an anomalous year for many reasons (prices fell, due to decreased demand, while median wages were artificially lifted by lower-wage workers losing their jobs).

As a percent of median weekly earnings for full-time workers, the Farm Bureau Thanksgiving meal will cost just 5 percent of weekly earnings (note: I use 3rd quarter earnings for each year, since it is the latest available for 2024). In 2020 it was only 4.7 percent, but other than that 2024 is lower than all other years for which we have data, which goes back to the mid-1980s, when it took 6-8 percent of earnings to buy this meal.

Last year I also said that this meal was the second cheapest ever — if you ignore the weird years of the pandemic. But now if you ignore those years, it is the most affordable it has ever been.

That’s something to be thankful for next week, but also every time you go to the grocery store. Since October 2019, average wages have increased more than prices at the grocery store — not by much, but still better than you might suspect (and yes, I have checked my receipts). If we go back to the 1980s, wages beat inflation by a much larger margin.

It seems to be an accepted fact that there is a momentum effect with stock prices: a stock which has done well over the past 6-12 months is likely to continue to do better than average over the next six months or so. A number of funds (ETFs) have been devised which try to take advantage of this factor.

On the other hand, sometimes trends reverse, and stock that was hot twelve months ago has now run up in price, and may be due for a pause.

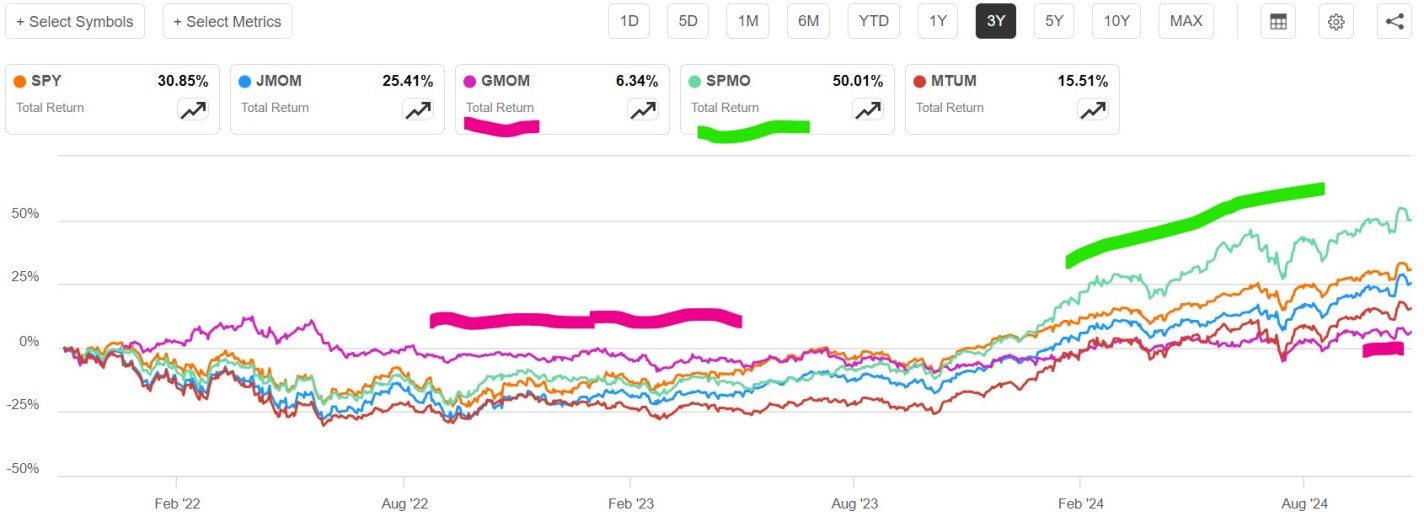

Here we will compare several momentum ETFs against the plain S&P 500 fund, SPY. In order to make it an apples-to-apples comparison, I am looking mainly at momentum funds that primarily draw from the S&P 500 large cap universe of stocks, excluding small-cap or tech only funds. [1] These large cap momentum funds are MTUM, JMOM, and SPMO. These funds all select stocks according to various rules. Besides trying to identify stocks with raw price momentum, these rules typically aim to minimize risk or volatility. I added one outlier, GMOM, that is very diversified. This fund does not hold individual stocks. Rather, it draws on some 50 different ETFs, including funds that focus on fixed income, commodities, or international or small cap as well as large cap US stocks, seeking to hold funds that show good relative momentum.

A plot of total returns over the past three years for these funds is shown below. It can be seen that plain SPY (orange line) beat all of the momentum funds except for SPMO (green line) in this timeframe. This is partly explained by the fact that SPY itself is a sort of momentum fund: the more a given stock’s price goes up, the bigger its representation in this capital-weighted fund. Also, over the past ten years or so, simply the biggest companies (the big tech quasi-monopolies like Google, Microsoft, etc.) have been generating more and more earnings, leaving the traditional auto and oil companies and banks, etc., in the dust.

By not focusing on U.S. large cap stocks, the diversified GMOM (marked with purple highlighter line) is less volatile. Its price did not drop nearly as much as the other funds in 2022, but it missed out on the great 2023-2024 stock run-up. SPMO (marked with green highlighter) really took off in that 2023-2024 big tech fiesta, by virtue of being concentrated in stocks like Nvidia, which went up roughly 10X in this timeframe. But this outperformance may be something of a one-off lucky strike. SPMO is still about the best of the momo funds, normally at least keeping up with SPY, but it does not consistently outperform it.

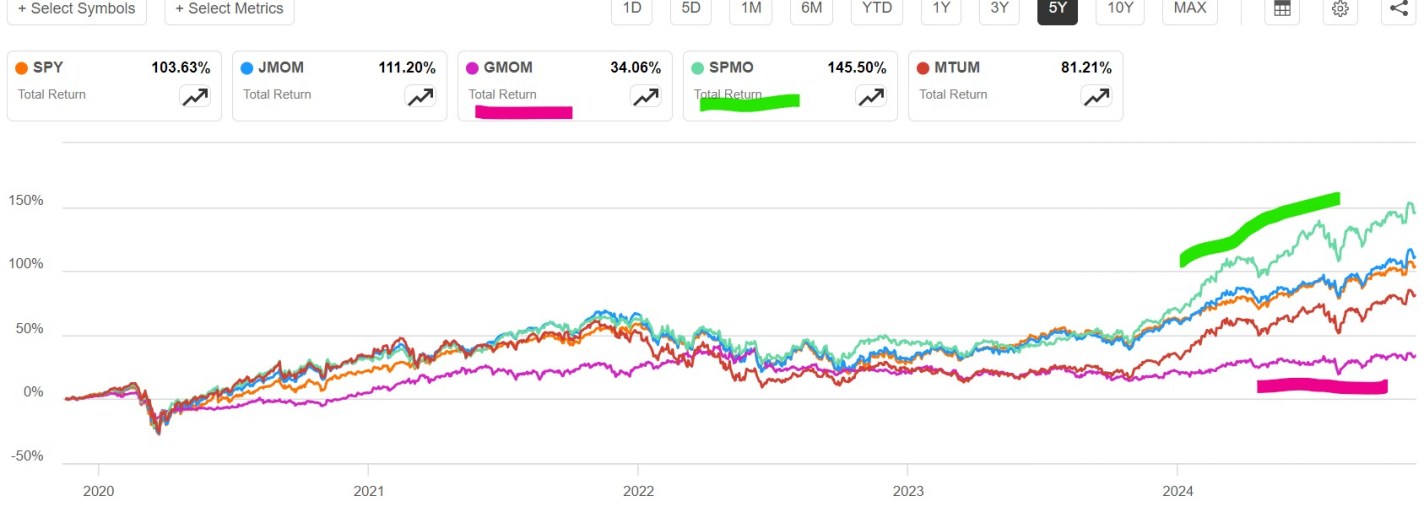

The five-year plot below illustrates similar trends, though it is a bit harder to read. Again, SPMO (green highlighter) largely keeps up with SPY, with a big outperformance spurt at the end. And GMOM is pretty flat; that really hurt it in the big 2020-2021 runup of big tech stocks. Over this five-year timeframe, JMOM kept up with SPY, and actually edged a bit ahead. MTUM, like most of the stock momo funds, actually ran ahead of SPY in the 2020-2021 runup, but fell somewhat more in 2022, and then got left in the dust in 2023. It is likely that it fell prey to trend reversal, which is a constant hazard for momentum funds. For most of 2022, the “best” stocks were dull value stocks, while tech stocks did terribly. Thus, a plain momentum algo fund would come into 2023 loaded with non-tech stocks. I suspect that is what happened to MTUM.

It happens that the SPMO algo has features that try to protect it from loading up on non-growth stocks during a bear market. So, it seems to be the best general momentum stock fund. It selects stocks which have shown positive momentum over the past twelve months, with the most recent month excluded (so as not to discriminate against a stock which had a temporary drop). Its chief vulnerability is that it only updates its holdings once every six months (mid-March and mid-September), so it is often acting on very old information. (Supposedly, it is better to update a momentum fund every three months).

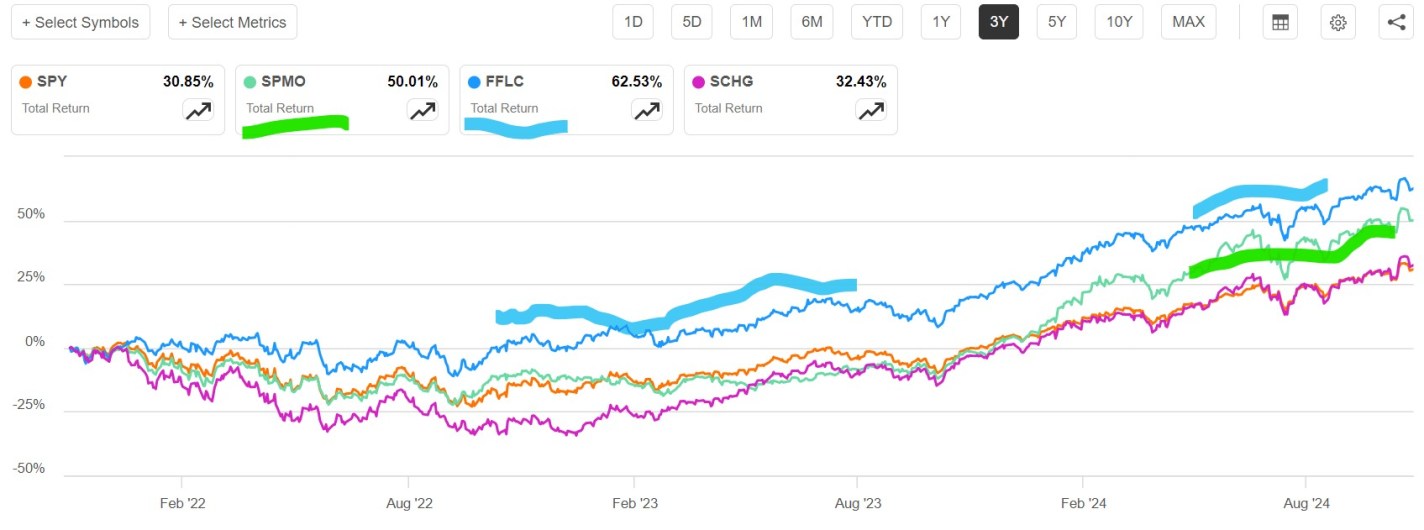

How does SPMO compare to a top actively-managed fund like FFLC or plain growth stock fund SCHG? The three-year plot below shows that FFLC (blue line, 63% total return) beat SPMO (green line, 50% return). Although SPMO had an impressive surge in the past year, FFLC just kept steadily outperforming SPY over the whole three-year period. This suggests that having good human judgement at the helm, able to adapt to differing market environments (2022 bear vs. 2023-2024 tech bull) can do better than a single, focused algorithm. I prefer a fund which keeps steadily outperforming “the market” (i.e., S&P 500) rather than one which only occasionally has moments of glory, so I hold more FFLC than SPMO.

In the plot above, the growth fund SCHG suffered more in 2022 when the tech high-flyers fell to earth, but made up for it in 2023-2024, to end up matching SPY over three years. On longer time-frames, SCHG handily beats SPY, as we noted in an earlier article on growth stocks.

[1] See this Insider Monkey article for a listing of ten best U.S. stock momentum funds. Some of these focus on small cap, mid cap, or technology stocks.

Can they all be true? No, but also yes. At least, that’s where my thinking is at the moment. What all of the preceding pieces seem to do is acknowledge the benefits and costs of remote work while also emphasizing any one particular cost or benefit that generates their preferred lede.

Remote workforces bring lower labor efficiency (e.g. more distractions, less monitoring, more shirking) and greater labor flexibility (e.g. larger labor pools to select from, faster labor turnover) to a firm or industry. It gives firms the ability to pay employees in something other than money, such as schedule flexibility and locational choice, capturing some of the rents from those compensating wage differentials for themselves in the form of lower labor costs. It also means firing and hiring people with greater efficiency and lower costs when each subsequent wave of technological obsolescence hits, more effectively curating your labor force to fit the newest technological opportunities and needs.

How this story plays out will be bespoke to every firm, industry, and sector, but one broad trend I’m looking for is how industries separate by technological turnover. Industries differentiate by the historical rate of technological upheaval. Construction is different today than it was 25 years ago, but that amount of change is almost trivial compared to the televison entertainment industry. I expect that firms industries that reward “nimbleness” in the adoption of and adaption to new technologies will embrace work from home in far greater numbers. This will, in turn, shrink the “periodicity” of industry business cycles. Industires with high remote work labor forces will both more quickly collapse to a dominant set of firms when excludable technology gives them and advantage. They will also, however, more quickly reinflate to a more competitive landscape from new firm entry enter as remote work allows rivals to rapidly update their labor force to match the newest technological landscape. I expect applied micro work on remote work preferences and theoretic work on the consequences of search costs for competition to find each other atop the empire state building and yield the kind of policy recommendations that would make Nora Ephron proud.

This is just one of many broad trends to look for as remote work evolves. The complexity of interacting forces makes forecasting both a fool’s errand and palm reading. All of the forecasts will be internally logical, collectively incompatible, partially correct, and completely wrong.

Just when you think there might be one arena of human life free of status competition, you will turn out to be wrong.

Consider the 4th graders who get to do “safety patrol” as volunteer work. This is a badge of honor and the kids like power. A casual observer might think that any kid who volunteers to do safety patrol would simply be having a great experience. Surely this is as simple as adding a unit of utility from consumption, in comparison to the times when the child is not allowed to do safety patrol.

But all is not well. Jackson Carter, says Rachel Pratt, has been hogging the prime safety patrol spot for weeks. He walks to school earlier than anyone and sits on the good spot, excluding the other 4th graders from having the chance to catch the highest volume of younger kids to boss around.

Rachel Pratt and several other girls are conspiring to, collectively, prevent Jackson from getting so disproportionately many days on the prime spot. They have agreed that if any one of them can beat him to the spot, they will share it with anyone except Jackson. The crew has also planned to loudly comment on the situation in earshot of the school principal in hopes that Jackson will have to share the spoils more evenly.

Remember that one time, back when we had a global pandemic, when interest rates fell really low and everyone was borrowing and refinancing? Good times. But they were also times of surging demand for durable goods, supply chain disruptions, and shortages. Specifically, the price of lumber surged by 54% between 2019 and 2022. There were stories of contractors who were unable to do their jobs at their typical prices. Some of them went without work. Others did much less work. Theft of precious lumber was in the news.

As we know, sudden price spikes often make the front pages and the social media rounds. But they peter out and the subsequent decline in prices hardly ever gets coverage in the same way. People used to talk about higher gasoline prices all the time, but never discussed with the same enthusiasm when prices fell. The same is true for lumber. We heard hysterical stories of record high prices, alleged shortages, and the sawmills that lacked adequate capacity to keep up with demand.

I thought this was going to be another election post, but it didn’t turn out that way.

My plan was to do another annual portfolio review, with a focus on changes I’ll make to my portfolio as a result of how the election impacts various market themes, and how my take on the election differs from the market’s take. But as I looked at my portfolio, what struck me wasn’t how the election changes things, but instead how severely my stock picks underperformed the incredible 26% return the S&P has posted so far this year.

My first couple years of stock picking tended to match the S&P, roughly what you’d expect if markets are efficient and I’m just throwing darts. But more recently so much of the overall return of the market has been driven by just 7 mega-cap stocks, the “Magnificent 7”, that if you don’t own them you are probably underperforming big time.

Of course buying a broad index, especially a market-cap-weighted one like the S&P, is a way to ensure you own at least a piece of the big winners, which is one reason economists usually recommend buying the broad index. And I did this with 80% of my portfolio, to match my 80% belief in the efficient markets hypothesis. But I’m now back up to 90% belief in efficient markets, at least for stocks.

This efficiency seems to change a lot over time. Probably fewer than 10% of US stocks have obvious mis-pricings right now; really none stand out as super mispriced to a casual observer like me. Instead, it seems like every 10 years or so a broad swathe of the market is driven crazy by a bubble or a crash, and you get lots of mispricing- like tech in 2000, forced/panic selling at the bottom in 2009, or meme stocks in 2021. The rest of the time, the stock market is quite efficient. So, in typical times, just be boring and buy and hold a broad index fund.

Of course, you might think that AI is a bubble now. I certainly don’t love the 68 P/E on NVIDIA, but this doesn’t strike me as a true bubble driven by irrational hope- peoples’ hopes have proven well justified so far, with AI performing miracles and the Mag 7 delivering huge profits. So like Scott, I’m finally giving up on being overweight value stocks. Perhaps our capitulation is the sign that growth’s decade-plus run is finally about to reverse; but if so, I’ll try not to regret it. After all, the S&P has plenty of value stocks too.

A new essay by J. Zachary Mazlish answers the title question in the affirmative: yes, inflation made the median voter poorer. The post is data-heavy, with lots of charts and different ways of slicing the data, which is great! But since I am called out by name (or rather, my evil twin, Jeremy Horpendahl), I want to respond specifically to the claim about my data, but also I’ll make a few broader points.

Regular readers will recognize the chart in that Tweet comes from an EWED post from April 2024. Mazlich says that my chart and others like it are “misleading for understanding the election because a) they compare wages now versus January 2020, rather than January 2021.”

Fair enough, but if you read my Tweet you will see that I am specifically responding to an NPR story which said, “if you look at the difference between what… groceries cost in 2019 and what it costs today, and what wages looked like in 2019 and today, the gap is really gigantic.” So, they are specifically using 2019 as a baseline in that story, and my chart specifically used that as the baseline too! That’s why I thought that chart was relevant.

It’s true, of course, that if you want to understand median voter sentiment about the Biden administration, you should probably start the data at the beginning of the Biden administration. But I was responding to the more general claim people make, that they are worse off than in 2019.

With that clarification out of the way, what does Mazlich’s broader post say?

Will Growth Stocks Continue to Trounce Value Stocks?

It’s no secret that growth stocks, mainly big tech companies like Apple and Microsoft, have massively out-performed so-called value stocks in the past fifteen years. Value stocks tend to have lower price/earnings and steady earnings and low price/earnings. They include sectors such as petroleum, utilities, traditional banks, and consumer products. These companies often pay substantial dividends from their cash flow.

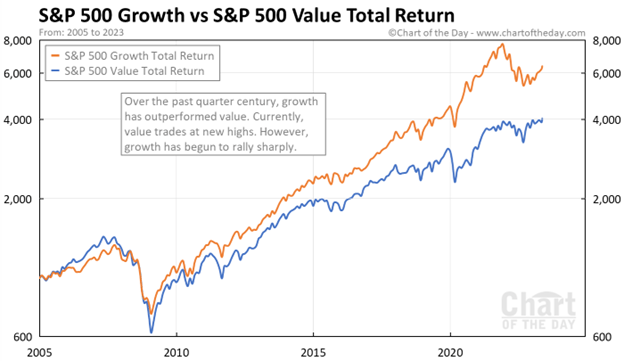

Here are some charts which make the point. This 2005-early 2023 chart shows value stocks (blue curve) having a small edge 2005-2008, then the growth stocks (orange curve) keep ripping higher and higher. Financial stocks, which mainly fall in the value category, were hit particularly hard in the 2008-2009 downturn.

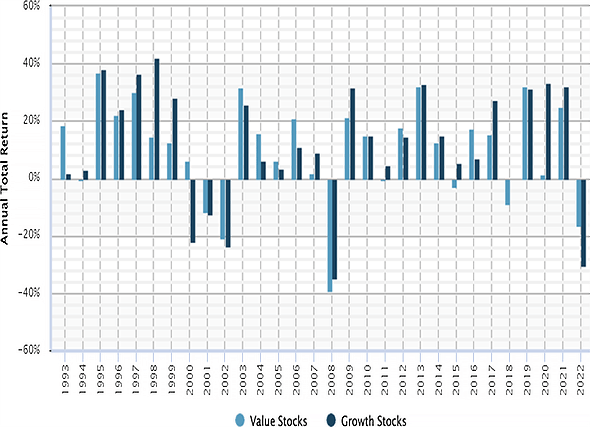

Here is a bar chart display of annual returns of value stocks (blue bars) and of growth stocks for the years 1993-2022. In 1997-1999 growth stocks outperformed. This was the great tech bubble – I remember it well, investors were shoveling money into any enterprise with a customer-facing website, whether or not there was any reasonable path to profitability. Reality caught up in 2000 (“What was I thinking??”), tech stock prices crashed and then tech was hated for a couple of years. But by 2009 or so, today’s big tech firms had emerged and established their quasi-monopolies, and started actually making money and even more money.

So, is the answer to just allocate all your equity portfolio to big tech and walk away? This is a question I have been asking myself. Even as growth stocks dominate year after year, there have continued to be voices warning that this is anomaly; historically, value stocks have performed better. So, with the sky-high valuations of today’s big tech, there is due to be a big mean reversion where the “Magnificent 7” get crushed, and Big Banks and Big Oil and Proctor & Gamble and even humble utilities finally get to shine.

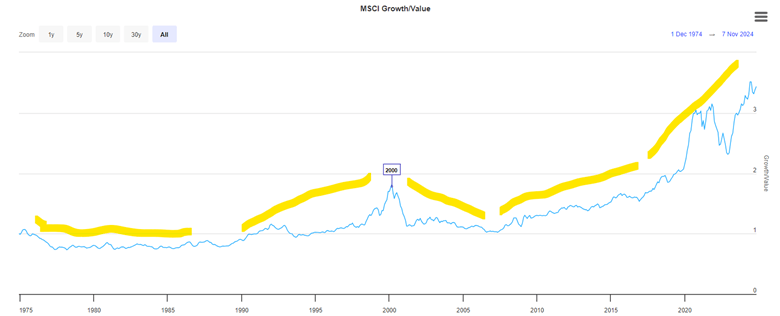

I don’t have a chart that goes that far back, but I have read that over the past 100 years, value has usually beat “growth”. Here is a hard-to-read plot of value vs growth for 1975-2024. I have added yellow highlighter lines to mark major trend periods. Growth underperformed 1975-1990, then growth picked up steam and culminated in the peak in the middle of the chart at 2000. Growth then underperformed 2000-2008, as noted earlier, as the excesses of the tech bubble were unwound, and people made paper fortunes in the real estate bubble of 2001-2007.

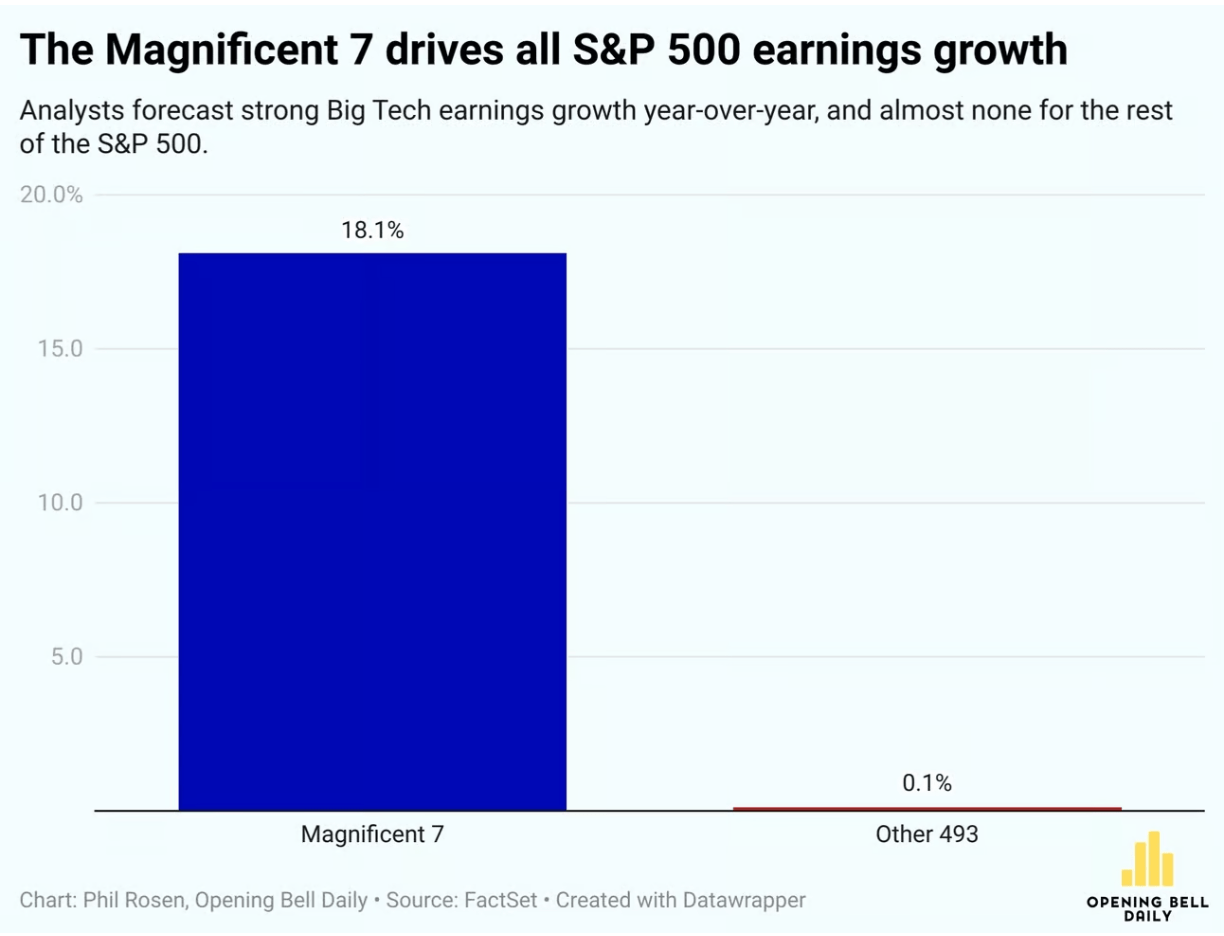

Growth has dominated since 2009, excerpt for 2022. That was the year the Fed raised interest rates, which tends to punish growth stocks. However, with their unstoppable increases in earnings (accounting for the vast majority of the earnings in the whole S&P 500), big tech has come roaring back. Yes, they sport high P/E ratios, but they have the earnings and the growth to largely justify their high valuations.

I have been influenced by the continual cautions about growth stocks becoming overvalued. Many an expert has advocated for value stocks. In June of this year, Bank of America head of US equity strategy Savita Subramanian told an audience at the Morningstar Investment Conference: “I have one message to you: Buy large-cap value.” So, for the past couple of years, I have gone relatively light on big tech and have over-allocated to “safer” investments like fixed income and value stocks. Silly me.

In the last few months, I finally decided to give up fighting the dominant trend, and so I put some funds into SCHG, which is specifically large cap growth, and in other growth-heavy funds. As you may imagine, these funds are loaded with Nvidia and Meta and other big tech. They have done very well since then.

How about going forward? Will the growth dominance continue, or will the dreaded mean reversion strike at last? At some point, I suspect that big tech earnings will slow down to where their high valuations can no longer be supported. But I don’t know when that will be, so I will just stay diversified.

Boilerplate disclaimer: Nothing here should be taken as advice to buy or sell any security.