The Affordable Care Act was supposed to make it easier for American workers to switch jobs by making it easier to get health insurance from sources other than their current employer. Mostly it didn’t work out that way. But a new paper finds that one piece of the ACA actually made people less likely to switch jobs.

The ACA Dependent Coverage Mandate required family health insurance plans to cover young adults though age 26, when prior to the 2010 passage of the ACA many had to leave the family plan at age 18 or 19. I thought these newly covered young adults would be more likely to switch jobs or start businesses, but there turned out to be absolutely no effect on job switching, and no overall increase in businesses (though it did seem to increase the number of disabled young adults starting businesses, and other parts of the ACA increased business formation among older adults).

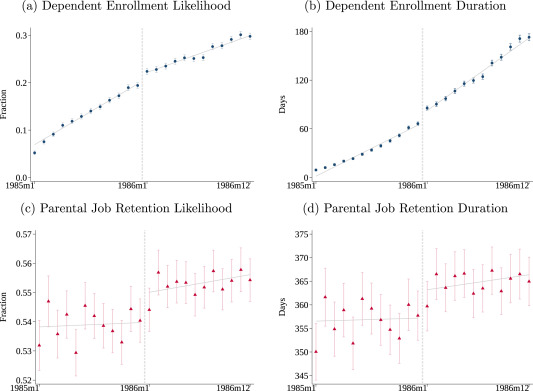

But while the Dependent Coverage mandate seems not to have reduced job lock for young adults, it increased job lock among their parents. That is the finding of a new paper in the Journal of Public Economics by Hannah Bae, Katherine Mackel, and Maggie Shi. Using a large dataset with exact months of age and coverage, MarketScan, allows them to estimate precise effects:

We find that dependents just to the right of the December 1985/January 1986 cutoff—those eligible for longer coverage—are more likely to enroll and remain covered for longer once the mandate is in effect. Dependent enrollment increases by 1.8 percentage points at the cutoff, an increase of 9.2 % over the enrollment rate for dependents born in December 1985. In addition, the enrollment duration increases by 9.7 days (14.6 %). Turning to their parents, we find that parental job retention likelihood increases by 1.0 percentage point (1.8 %) and job duration increases by 5.8 days (1.6 %) to the right of the cutoff. When scaled by the estimated share of dependents on end of year plans, our findings imply that 12 additional months of dependent coverage correspond to a 7.7 % increase in job retention likelihood and a 7.0 % increase in retention duration.

I believe in this parental job lock effect partly because of their data and econometric analysis, and partly through introspection. I plan to work for years after I have the money to retire myself in order to keep benefits for my kids, though personally I’m more interested in tuition remission than health insurance.

On top of working longer though, benefits like these enable employers to pay parents lower money wages. A 2022 Labour Economics paper from Seonghoon Kim and Kanghyock Koh found that the Dependent Coverage Mandate “reduced parents’ annual wages by about $2600 without significant reductions in the probability of employment and working hours.” But at least their kids are better off for it.