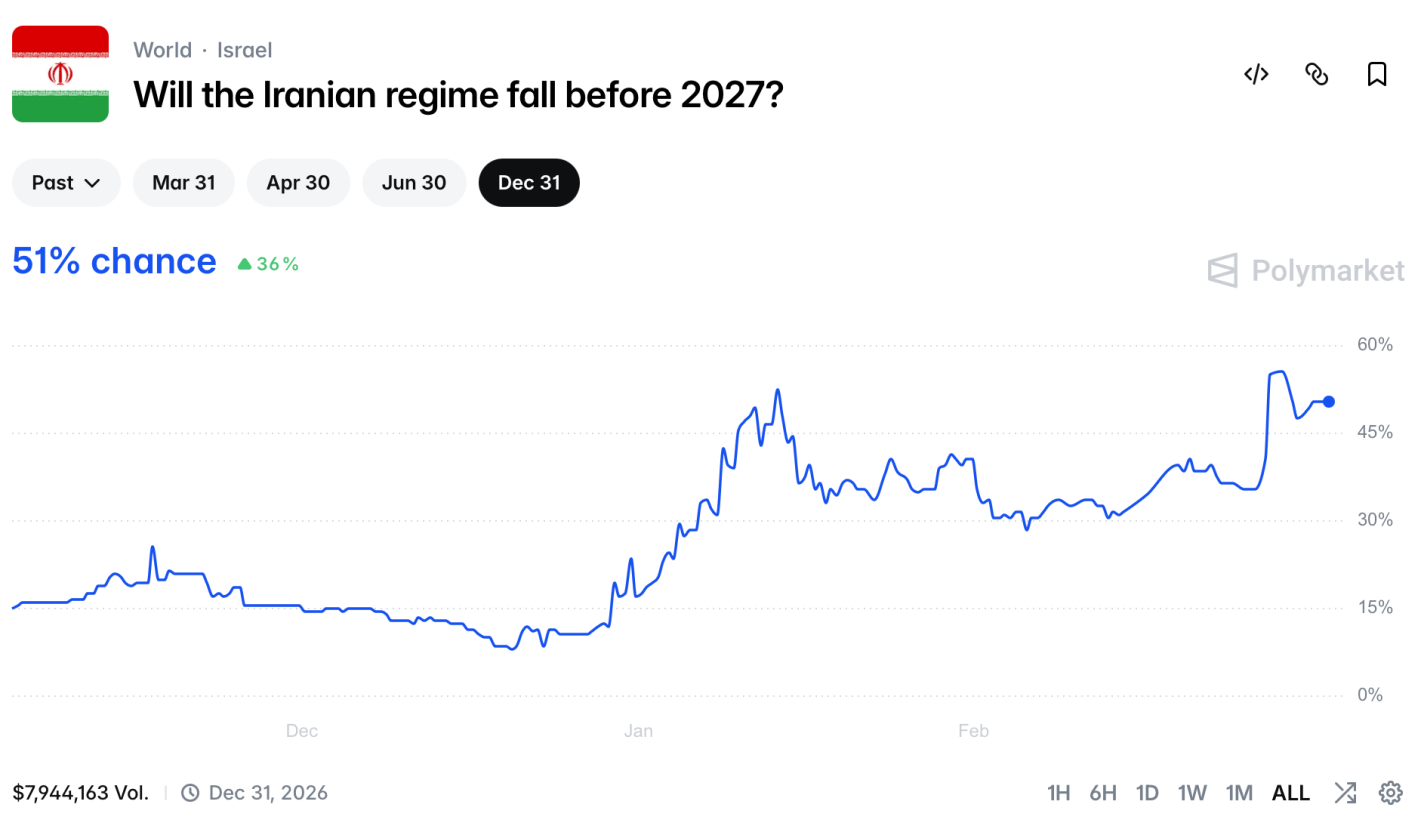

The Iran regime’s military strategy seems to be that by bombing the oil infrastructure of their neighbors and neutral shipping, US gasoline prices will go so high that Americans will demand an end to the war.

How many Americans would be willing to pay $6/gallon gas for months for a ~50% chance of toppling a regime that oppresses 90 million people and destabilizes its region on the other side of the world? Probably only a minority of voters, especially when the President didn’t make the case to the American people or Congress beforehand.

But the US produces more than enough oil for its own needs. Why does the Strait of Hormuz being closed mean higher gas prices here? Only because US oil companies can sell to global markets, and they won’t choose to sell a barrel of oil to a US refiner for $60 when they could sell it to a foreign refiner for $100. If the government took away the foreign option, US oil producers would sell to US refiners at prices consistent with pre-war sub-$3/gallon gasoline.

Naturally there would be costs to an export ban. US oil producers would miss out on windfall profits, while Russian producers would benefit. Foreign customers of US oil, many of them in allied countries, would be angered by the missed shipments and global oil prices would soar further.

But if the US administration wants to avoid a midterm wipeout driven by high gas prices, I see only 3 options:

- Get lucky and see the Iranian regime fall quickly

- Negotiate an end to the war quickly (which might itself be unpopular if they can’t get a good deal) or just declare victory and go home (but its not clear whether Iran would re-open the strait now just because the US stopped bombing)

- Restrict Exports

I say “restrict” not “ban” because I don’t think a complete export ban is necessary to stabilize US prices. You could instead do an export tax (high enough to stop many exports but low enough to allow the buyers with the highest values / fewest alternatives to stay in the market), or you could do a ban but allow a few export waivers for favored buyers or sellers (which seems like Trump’s style), or similarly a quota limiting exports to a certain number (say, limit each company’s monthly exports to 90% of their volume in the same month last year).

This has an obvious precedent: the Biden administration stopped issuing new permits to export liquified natural gas in 2024 to prevent prices spiking here during the Ukraine war (which led to even higher prices for our European allies). But a total ban on oil exports would be a much bigger deal.

Will the Trump administration actually try something like this? It will be an interesting test of US political economy to see what happens when the interests of the military-industrial complex conflict with the interests of oil producers.