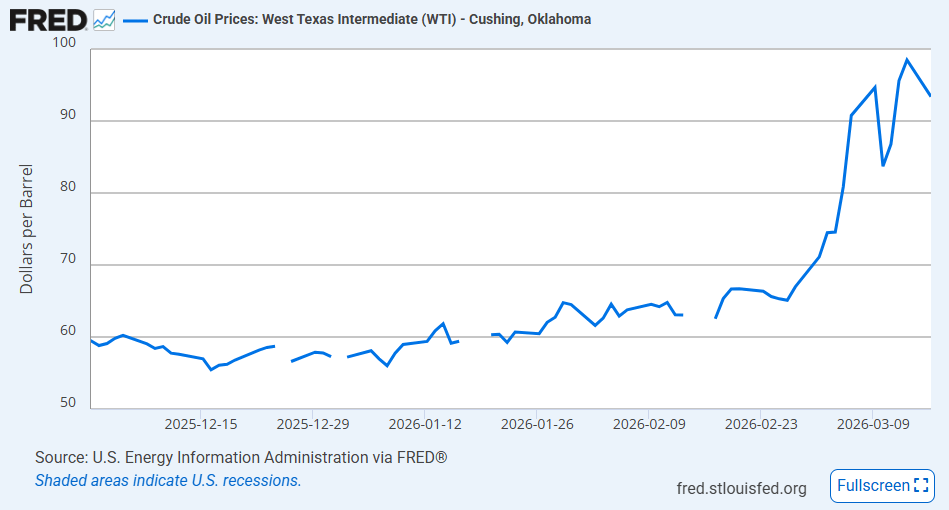

Alex Tabarrok noted in Oil versus Ice Cream that he and Tyler, as textbook authors, “chose the oil market as our central example. Oil is always in the news…”

when a student sees that the price of crude has surged past $100 a barrel because Iran closed the Strait of Hormuz—choking off 20% of the world’s oil supply—they have the framework to understand what is happening. Supply shock, inelastic demand, expectations and speculation, the macroeconomic transmission to GDP—it’s all right there in the headlines.

In a classroom, a good way to begin is to ask the students to tell you what they have noticed recently about oil or gas prices. Having the students obtain the oil price data themselves could be fun, if you are in an environment with screens/computers.

Ask students: “Is this price change primarily explained by

Increase in demand

Decrease in demand

Increase in supply

Decrease in supply

Correct answer: d. Decrease in supply

If you cover elasticity, this is especially helpful as an example. “Why would the price jump more when demand is inelastic?”

It’s not too late to work this into a lesson plan for the Spring 2026 semester, economic teachers. I might use it to illustrate supply shocks next week.

This event is a classic example of a negative supply shock: a disruption in the Strait of Hormuz would reduce the amount of oil reaching world markets, pushing energy prices sharply upward. Because oil is an important input for transportation, manufacturing, and heating, higher oil prices raise costs across much of the economy. Firms may cut production, households may spend more on gasoline and utilities and less on other goods, and overall economic activity can slow. That is why economists worry that large oil supply shocks can contribute to recessions. They do not just make one product more expensive; they can ripple outward, reducing real income, lowering consumer confidence, and weakening GDP growth while inflation rises.

Related posts. The whole crew showed up this month:

The Iran regime’s military strategy seems to be that by bombing the oil infrastructure of their neighbors and neutral shipping, US gasoline prices will go so high that Americans will demand an end to the war.

How many Americans would be willing to pay $6/gallon gas for months for a ~50% chance of toppling a regime that oppresses 90 million people and destabilizes its region on the other side of the world? Probably only a minority of voters, especially when the President didn’t make the case to the American people or Congress beforehand.

But the US produces more than enough oil for its own needs. Why does the Strait of Hormuz being closed mean higher gas prices here? Only because US oil companies can sell to global markets, and they won’t choose to sell a barrel of oil to a US refiner for $60 when they could sell it to a foreign refiner for $100. If the government took away the foreign option, US oil producers would sell to US refiners at prices consistent with pre-war sub-$3/gallon gasoline.

Naturally there would be costs to an export ban. US oil producers would miss out on windfall profits, while Russian producers would benefit. Foreign customers of US oil, many of them in allied countries, would be angered by the missed shipments and global oil prices would soar further.

But if the US administration wants to avoid a midterm wipeout driven by high gas prices, I see only 3 options:

Get lucky and see the Iranian regime fall quickly

Negotiate an end to the war quickly (which might itself be unpopular if they can’t get a good deal) or just declare victory and go home (but its not clear whether Iran would re-open the strait now just because the US stopped bombing)

Restrict Exports

I say “restrict” not “ban” because I don’t think a complete export ban is necessary to stabilize US prices. You could instead do an export tax (high enough to stop many exports but low enough to allow the buyers with the highest values / fewest alternatives to stay in the market), or you could do a ban but allow a few export waivers for favored buyers or sellers (which seems like Trump’s style), or similarly a quota limiting exports to a certain number (say, limit each company’s monthly exports to 90% of their volume in the same month last year).

This has an obvious precedent: the Biden administration stopped issuing new permits to export liquified natural gas in 2024 to prevent prices spiking here during the Ukraine war (which led to even higher prices for our European allies). But a total ban on oil exports would be a much bigger deal.

Will the Trump administration actually try something like this? It will be an interesting test of US political economy to see what happens when the interests of the military-industrial complex conflict with the interests of oil producers.

I make a hobby of reading, and sometimes acting on, investment advice, particularly regarding high-yielding securities (many of my holdings are now yielding over 10%/year). One of the best authors on the Seeking Alpha investing site writes under the name of Colorado Wealth Management. He mainly writes on REIT (real estate investment trust) stocks, but recently opined on the wisdom of raising interest rates to combat inflation regarding some of the major components of CPI.

His article, Why High Yields Will Be Popular Again, may be behind a paywall for some readers, so I will summarize some key points. He kind of sidesteps the influence of massive federal deficit spending that injected trillions and trillions of new dollars into the economy for COVID, which I think has been the major driver for this inflation; and the reignited deficit spending which is already on the books for November and likely even huger for December of this year. However, he does make some interesting (and new to me) points regarding food prices in particular.

He sees the price 2021-2022 price increases in some major food items as being driven by supply constraints, rather then by excessive demand. Specifically eggs, coffee, and vegetable oils have been hit by exogenous factors which have constrained supply; raising interest rates will not help here, and may even hurt if higher rates make it harder for farmers to recover and re-start high production. I’ll transition to his charts and mainly his excerpted words, in italics below:

Avian Flu, Culled Hens, and the Price of Eggs

The background here is that tens of millions of chickens, including egg-laying hens, have been deliberately killed (“culled”) this year in an attempt to slow the spread of avian flu. This, of course, cuts into the egg supply and raises egg prices. We went through a similar cycle in 2015 with avian flu, where culling led to a rise in egg prices, but then prices fell naturally as a new crop of chicks grew into egg-laying hens. Similarly, the current shortage in eggs should correct itself:

Raising interest rates has never produced additional eggs. Raising interest rates and driving a recession (with larger credit spreads) only makes it more difficult for farmers to get the funding necessary to replace tens of millions of hens that were culled to slow the spread of the avian flu….If interest rates don’t work, what will? The cure for high prices is high prices. We can see how it played out with the Avian flu in 2015:

Is Jerome Powell going to lay even one egg? Probably not.

Are farmers going to focus on turning their chicks into egg-laying hens? Absolutely.

Since eggs go into several other products, it drives inflation throughout the grocery store. Even if a product doesn’t use eggs, the drop in egg production means more people eating other foods.

Drought in Brazil and the Price of Coffee

Coffee prices have been rising rapidly. Well, domestic prices have been rising rapidly. Global prices actually declined since peaking in February 2022:

So, what drove the price up? Brazil normally produces over 35% of the world’s coffee and bad weather in Brazil (not to mention the pandemic impacts) drove dramatically lower production in 2021. As the shortfall in production became evident, global prices began rising rapidly. That’s why the global [wholesale] prices were ripping higher in 2021, not 2022. However, [retail] consumers are seeing most of the impact over the last several months.

War in Ukraine and the Price of Sunflower Oil

Margarine requires vegetable oil. Soybean, palm, sunflower, and canola oil are the key ingredients. What country produces the most sunflower oil? Ukraine. This is one of several inflationary impacts of the war. You can see the impact of reduced supply in the following chart:

Government Bungling in Indonesia and the Price of Palm Oil

What happened to palm oil? How could it soar so much and then fall so hard?

The first issue is that dramatic increases in the price of fertilizer made production more expensive. … That contributed to a reduction in supply. However, Indonesia is the world’s largest exporter of palm oil. Yet exports of palm levy were subject to a huge levy. That made exporting far more expensive. Despite the levy, it was still worth producing and exporting palm oil. Then the Indonesian government decided to simply ban exports over concern about higher domestic prices. Banning exports for a country that produces 59% of the world’s total palm oil exports had a predictable impact.

If you guessed that the supply of palm oil couldn’t be sold domestically, you’d be right. The ban was lifted. However, it was only after:

“High palm oil stocks have forced mills to limit purchases of palm fruits. Farmers have complained their unsold fruits have been left to rot. There were 7.23 million tonnes of crude palm oil in storage tanks at the end of May, data from the Indonesian Palm Oil Association (GAPKI) showed on Friday.“

With palm oil prices at all time-record highs, nearly triple the level from two years prior, the supply was left to rot. Each business tried to make the best decision they could, given the ban on exports. Rather than record profits for mills and record profits for farmers, the produce was wasted. That’s supply constraints for the global market, and it destroys the local economy.

Global prices are plunging now as mills seek to unload their storage. As bad as the higher prices were for the rest of the world, no one suffered worse than the farmers whose product became worthless as a result of government failure.

Contrary to today’s popular opinion, higher interest rates won’t do anything to improve production of vegetable oil.

I’ve always been confused by the US alliance with Saudi Arabia. Its a state with values abhorrent to many Americans, and it seems like we don’t get much practical value out of the alliance.

This essay on Saudi history, politics, and economics by Matt Lakeman makes the situation more comprehensible. I still don’t know that I want the alliance, but I can now see how so many US presidents have continued with it without necessarily being stupid, crazy, or corrupt. In short, they think that most of the realistic alternatives are worse. Some highlights:

Before starting this research, I had the same perception as Wood that the Saudi economy is essentially what he calls a “petrol-rentier state.” Basically, Saudi Arabia sits on top of a giant ocean of easily-accessed oil which they suck out of the ground and sell at enormous profit to prop up the rest of their extremely inefficient economy and buy the loyalty of their own people and foreign powers. Saudi Arabia is the wealthiest large state in the Middle East today by sheer virtue of geographic luck rather than any innovation or business acumen on the part of its people.

And after doing my research, all of the above is… basically true.

But all of that should also be true of Iran, Iraq, Venezuela, Libya, and a few other countries which are also situated on giant oceans of oil but are far poorer than Saudi Arabia.

Economically, Saudi Arabia deserves little credit for its success. Politically, Saudi Arabia deserves a tremendous amount of credit for enabling its economic success.

Dealing with the resource curse is always challenging, and foreign ownership is an additional challenge. How did they manage it?

the Sauds struck a clever balance between being too aggressive and too placating of the foreigners operating their oil wells. If the Saudi state had been aggressive and tried to nationalize its oil quickly, Saudi Arabia could have ended up becoming another Venezuela or Iran with lots of external political pressure from hostile Western countries and a low-efficiency oil industry. But if they had nationalized too late, they would have ended up like a lot of African nations who have all their natural wealth siphoned away by foreigners.

Instead, the Sauds executed a patient, and most importantly, amicable assertion of power over Aramco, which did not become fully owned by Saudis until 1974. At the very start of Aramco, the company was entirely owned and operated by Americans aside from menial labor. However, the Saudi government inserted a clause into their contract with the corporation requiring the American oil men to train Saudi citizens for management and engineering jobs. The Americans held up their end of the bargain, and over time, more and more Saudis took over management and technical positions.

In addition to carefully negotiating the balance of power with various foreigners, the Sauds have done so with the religious establishment:

Though the monarch has absolute power, his authority is at least in part derived from Saudi Arabia’s Islamic religious establishment. The ulema (a group of the highest-ranking clerics) is officially integrated into the government, and plays an important role in legal matters. However, the religious establishment has slowly been marginalized by the monarchy over the last few decades, and has possibly been subjugated entirely since the reform era began five years ago.

Winning freedom of action has been a long road with many setbacks:

[King] Abdulaziz constantly had to reassure enraged Wahhabi clerics that he wasn’t selling out the Arab homeland to treacherous infidels. IIRC, it was some time in the 1920s that Abdulaziz had to publicly smash a telegraph to prove to the clerics that he wasn’t bewitched by infidel technology.

In late 1979, 400-500 extremist Sunni Saudis seized the Grand Mosque in Mecca (the holiest Islamic site on earth) and demanded the overthrow of the Saud dynasty in favor of a theocratic state meant to await an imminent apocalypse. They held on for two weeks while managing to fight off waves of Saudi police and military squads. Eventually, three French commandos flew to Mecca, converted to Islam in a hotel room, and led a successful assault to retake the Mosque. Over 100 men died on each side, with hundreds more wounded.

The Grand Mosque seizure was the final wake-up call for the Saud dynasty. Something drastic had to be done or their regime would likely be ground down under mounting internal and external pressure…. King Khalid led a social/religious/political reactionary revolution within Saudi Arabia to align with the Sunni extremists. Up until about four years ago, Saudi society was still gender segregated and enforced a largely literalist interpretation of Sharia, hence the array of bizarre and antiquated laws – gender segregation in public, requiring women to cover their faces, outlawing of non-Muslim religious buildings (there are a few Shia mosques), restrictions on foreign media, etc. Saudi Arabia was always conservative, but most of these draconian laws were only put into place in the 1980s. The Saud dynasty purposefully induced a reactionary legal regime and pulled Saudi Arabia further away from liberalism.

The charitable take on making an already oppressive regime even more oppressive is that the Sauds were trying to bend Saudi Arabia to the extremists so the country would not break. And by all accounts, it worked; the conservative Wahhabi clerics backed by the Saud dynasty placated a sizeable portion of the Sunni extremists inside and outside of Saudi Arabia, and they became a pool of support against the Shia and Baathists. Saudi Arabia was certainly made a worse country for its citizens, but that was the price to pay for averting civil war.

More recently, Crown Prince Salman has consolidated power to the point where he can make modernizing reforms that Wahhabis might have opposed, like allowing women to drive, allowing non-Muslim foreigners to to get tourist visas, allowing music concerts, et c. Lakeman obviously likes these reforms, but at the same time worries that the concentrated power that so far Salman has largely used to enact positive reforms could be abused going forward, and on a larger scale than murdering the occasional dissident.

Wood argues that a worst case scenario parallel to MBS is Syrian Dictator Bashar al-Assad. Like MBS, there were high hopes that Assad would be a liberal reformer when he took over Syria. After all, Assad had been living and working in the UK as an ophthalmologist with no political aspirations, and was known to be a fan of Phil Collins. He was called to the throne after the unexpected death of his older brother, and so the West hoped that this nerdy British doctor would bring upper-middle class liberal values to Syria. Instead, Assad became one of the worst dictators of the modern Middle East, probably second only to Saddam Hussein.

I recommend reading the whole thing, here I’m quoting relatively small parts of an article full of interesting detail on the history, economics, and politics of Saudi Arabia. There’s also a section on visiting:

The silver lining to Saudi Arabia’s lack of tourism is that there aren’t many tourist restrictions. I went to two ancient settlements and I found no guards, no gates, no notices at all. I walked in, around, and on top of 2,000 year old houses, and I honestly have no idea if I was allowed to.

Although fracking technology has enabled renewed oil production in the U.S., the West remains heavily dependent on oil imports, especially from the Middle East. Even in the U.S., the current refining capacity is not well-matched to the type of light oil produced by fracking, so we still import oil (of types that our refineries can handle), although we also export fracked oil. Since oil remains the basis of so much economic activity, and since many oil exporting countries are unstable or even hostile to the U.S and our allies, the U.S. in 1975 established a large Strategic Petroleum Reserve (SPR) to store up crude oil. The storage is mainly in caverns in Texas and Louisiana, dissolved out of underground salt deposits. It was mainly filled in the Reagan/Bush administrations in the late 1970’s, and topped up under Bush II around 2003-2004.

The statutory purpose of this stockpile is to protect us and our allies against a “a significant reduction in supply which is of significant scope and duration,” per the Department of Energy. If such an event occurs, leading to high prices and associated economic impact, the President is authorized to release oil from the SPR. However,

In no case may the Reserve be drawn down…

(A) in excess of an aggregate of 30,000,000 barrels with respect to each such shortage;

(B) for more than 60 days with respect to each such shortage;

Somehow various administrations and also Congress have circumvented these restrictions on draining the SPR, and over the years have sold off bits and pieces to raise money for government spending. However, the current administration has decimated the SPR, selling off a third of it (some 200 million barrels), mostly in the past six months:

The administration projects this gusher to stop after November. Essentially all objective observers recognize this as primarily a political move, to reduce gasoline prices in order to curry favor with voters for the mid-term elections this November. It’s one thing to knock the price of gasoline down from $5.00/gallon back in the spring, when the world was panicked about Russia’s invasion of Ukraine, but to keep on selling into a moderated market is irresponsible. We haven’t had an actual shortfall in supply these past few months. Among other things, Russia keeps happily pumping and selling, out into the global grey market.

I won’t belabor the point here (stay tuned for more posts on this subject), but the world is structurally short of oil. With this administration having spent its first year demonizing oil and oil companies, the petroleum industry is understandably cautious about making expensive investments in future oil production. They know they will be stabbed in the back as soon as the current party in power no longer needs them.

By dumping this oil now, the administration is making the U.S. and the West more vulnerable later, if there is an actual global oil supply crisis (think: Iran vs. Saudi Arabia in the Persian Gulf…). Irritated by the lowish oil prices engendered by the SPR release, OPEC just announced production cuts which will drive prices right back up. They can cut production far longer than we can drain the SPR. If this all motivates further investment in low CO2 energy (including nuclear), that is perhaps a good thing. But between now, and attaining a carbon-free utopia in the future, we need to keep the crude flowing. Let us hope for the best here.

Ultimately, drawing down the SPR was a political decision. Think about it. An administration that has frequently emphasized the importance of reducing carbon emissions is trying to increase oil supplies to bring down rising oil prices — which will in turn help keep demand (and carbon emissions) high.

But even though the Biden Administration wants to address rising carbon emissions, high gasoline prices cause incumbents to lose elections. So, they try to tame gasoline prices even though it contradicts one of their key objectives of reducing carbon emissions.

The SPR has now been depleted since President Biden took office from 640 million barrels to 450 million barrels…

President Biden’s gamble to deplete the SPR in order to fight high oil prices may not hurt him at all. Of course, if for some reason we had a true supply emergency and found ourselves needing that oil, it would be looked upon as a terrible decision.

Shell Oil scientist M. King Hubbert made a remarkable prediction in 1956. He had analyzed the depletion patterns of various natural resources, and proposed that the production rates of a given resource from a given region would tend to follow a roughly bell-shaped curve. More specifically, he used what is now called the “Hubbert curve”, which is a probability density function of a logistic distribution curve. This curve is like a gaussian function (which is used to plot normal distributions), but is somewhat “wider”:

Hubbert used various reasonable assumptions (which we will not canvass here) in formulating this model curve. Notably, it predicts that the peak production rate will occur when the total resource from that region is 50% depleted, and that the fall in production on the back side of the curve will be as fast as the rise in production on the front (left) side of the curve.

In 1956, while U.S. oil production was still rising briskly, he fit his curve to the data to that point in time, and predicted that U.S. production would peak in 1970 and thereafter enter a rapid and permanent decline. His prediction was somewhat ridiculed at the time, but it proved to be uncannily accurate over the following 25 years; oil production peaked right when King said it would, and then declined per his curve until about 1990:

Lower 48 U.S. Oil Production: Actual (Green curve) vs. 1956 Hubbert Prediction (Red Curve). Blue Arrow marks deviation ~ 1990-2008, and green arrow marks acceleration of shale oil production. Source: Wikipedia, with arrows added.

I drew in a red arrow at 1956 to show when King made his prediction, and also a blue arrow showing a significant deviation that starting to show after about 1990. Once production had declined maybe halfway down from its peak, the production started to flatten out and decline much more slowly. More on this “fat tail” feature below.

Another feature I called attention to with a green arrow is the remarkable resurgence in production after 2008, which is mainly due to “fracking” of tight shale formation. That new-to-the-world technology has unlocked a new set of oil fields which had previously been inaccessible for production. This illustrated a well-recognized feature of Hubbert curves, which is that a given curve can (at best) apply only to a given region and for a “normal” pace of technological improvement. Fracking production should sit on its own up-and-then-down production curve.

The plot above is for lower 48 states only; a big find in Alaska gave a bump in production 1980-2000 (not shown here) which distorted the whole-U.S. production curve. That Alaska oil peaked by about 2000 and is now in its own terminal decline pattern.

The shape of production curve on the back (declining) side is of particular interest in trying to do economic modeling of future oil production. If the declines really follow a Hubbert curve, the prognosis is pretty scary – – oil production is slated to crash to practically nothing in the near future. However, it seems that in reality, after an initially rapid decline, production can often be sustained much longer than predicted by a simple symmetrical curve. We saw that pattern in the lower 48 curve above, starting around 1990, even before the fracking revolution. Below I show two other examples showing the same feature. The first example, from Hubbert’s original paper, is Ohio oil production 1885-1956:

I am not prepared to make quantitative generalizations, but there does seem to be a pattern of sustained production at reduced levels, following the initial rapid decline from the peak. Others also have noted that asymmetric curves may give better fits to real-world production. These “fat tails” on production from various oil-producing regions should help us keep our cars running longer than predicted by simple peak-oil models. How this pertains to future U.S. shale oil production, and to global oil production, are (since oil and gas are the main energy sources for the world economy) key questions, which we may address in future articles.

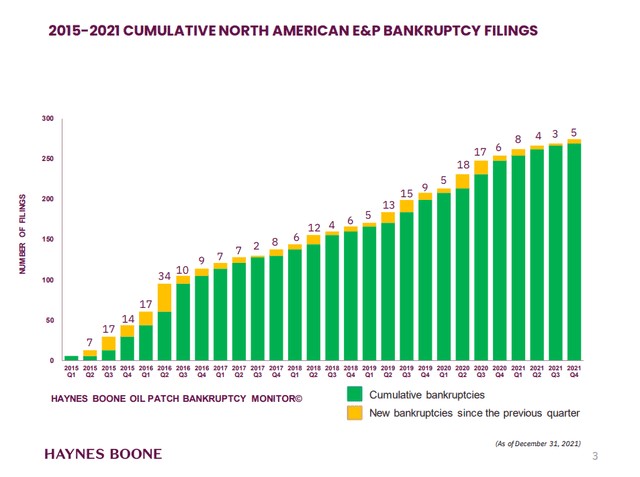

Oil production is a difficult, risky business even under favorable regulatory regimes. For instance, here is a chart of cumulative bankruptcy filings of exploration and production (E&P) companies for 2015-2021:

A few companies go bust every year, but there are some years like 2015-2016 and 2019-2020 when a lot of companies go bust. That happens when the oil industry collectively has overproduced and driven the price of oil below the effective cost of production. Even the mighty ExxonMobil ran deep in the red in 2020, losing an eye-watering 22.4 billion dollars. With all that in mind, shareholders since 2020 have been pressuring companies to show “financial discipline”, which means “drill less”.

Beyond these basic business realities, there is a whole new set of pressures to inhibit petroleum production. Environmental activists have pushed banks to withhold funding from petroleum companies, to strangle further oil production. It was big news in 2020 when activists, alarmed by ExxonMobil’s plans to actually (gasp) increase its oil production, successfully elected several alternative members to the board of directors with the specific goal of curtailing further drilling.

There have been attacks on the oil industry on the political front, as well. Joe Biden ran on a platform of banning drilling on public lands, and one item he checked off his to-do list on his first day in office was to issue an executive order killing a pipeline that would have facilitated imports of oil from the abundant reserves in Canada. One of his nominees for a top financial regulatory post remarked regarding oil producers that “we want them to go bankrupt if we want to tackle climate change”. All these are the sorts of things that make execs less willing to commit capital for expensive drilling programs that may take years to pay back. (The counter-claim by the administration that the U.S. oil industry is just sitting on thousands of unused oil leases is a red herring).

There is only a finite amount of oil in the ground, so it makes sense to move with all deliberate speed toward renewable and nuclear energy (which emits little or no CO2). However, our European friends who have installed lots of solar panels and windmills have discovered that the sun does not shine at night (!) and the wind does not always blow strongly (!!) , and so during their energy transition they need to maintain an adequate supply of fossil fuel power in order to keep the lights on. They elected to let their own oil and gas production dwindle, and rely instead on gas and oil purchased from Russia. We warned back in September that this European policy would give Russia leverage for harassing Ukraine, but apparently not enough EU leaders read this blog. Anyway, even back in the fall of 2021, Russia had restricted natural gas deliveries to Europe, causing sky-high prices there for gas and power.

The European experience ought to have been a cautionary tale for America, but political attacks on oil production continued in the halls of Congress itself. In an October 2021 hearing over climate change prevention, Carolyn Maloney (D-NY) and Ro Khanna (D-CA) insisted that Big Oil commit to reducing US oil and gas production by 3-4% annually (50-70% total by 2050). In a follow-up February 8, 2022 hearing, the two legislators again demanded concrete commitments from oil companies to reduce their domestic production (although, strangely, Mr. Khanna supported President Biden’s call for other regions, such as OPEC and Russia to increase production).

With oil drilling having been curtailed for the past several years (as desired by environmentalists), the world has now flopped from an oil surplus to an oil shortage, exacerbated by Russia’s invasion of Ukraine and subsequent sanctions. And of course world oil prices (which are not under the control of U.S. companies) have gone up in response. Oil companies are actually making money again instead of going bankrupt like two years ago

In 2021 Apple had a 26% net profit margin and an effective tax rate of only 13%, while the oil industry had an average profit margin of 8.9% and an effective tax rate of 26.9%. Yet Congress (mainly Democrats) “investigates” price gouging every time gas prices go up, without hauling in Tim Cook to grill him over the price of each new iPhone model. Repeated previous investigations have shown that domestic gasoline prices are mainly a function of world oil prices, which are not under the control of U.S. companies. Nevertheless, after berating oil execs for increasing oil production, here come the grandstanding Congressional attack dogs, holding a hearing last week titled (wait for it…) “Gouged at the Gas Station: Big Oil and America’s Pain at the Pump”.

The oil producers patiently explained that “We do not control the price of crude oil or natural gas, nor of refined products like gasoline and diesel fuel,” and “”It [the U.S. oil industry] is experiencing severe cost inflation, a labor shortage due to three downturns in 12 years, shortages of drilling rigs, frack fleets, frack sand, steel pipe, and other equipment and materials.” But it is not clear that anyone was listening to the facts.

Overall, I’ve been disappointed with the reporting on the US embargo against Russian oil. The AP reported that the US imports 8% of Russia’s crude oil exports. But then they and other outlets list a litany of other figures without any context for relative magnitudes. Let’s shine some more light on the crude oil data.*

First, the 8% figure is correct – or, at least it was correct as of December of 2021. The below figure charts the last 7 years of total Russian crude oil exports, US imports of Russian crude oil, and the proportion that US imports compose. That 8% figure is by no means representative of recent history. The average US proportion in 2015-2018 was 7.8%. But the US share as since risen in level and volatility. Since 2019, the US imports compose an average of 11.9% of all Russian crude oil exports.

As an exogenous shock, the import ban on Russian crude oil might have a substantial impact on Russian exports. However, many of the world’s oil importers were already refusing Russian crude. The US ban may not have a large independent effect on Russian sales and may be a case of congress endorsing a policy that’s already in place voluntarily.