In a previous post, I contrasted the income and property taxes, but I left out the other important tax: the retail sales tax. So let’s rectify that omission.

The retail sales tax is like the “Little Engine that Could,” delivering a steady stream of revenue to governments, while mostly staying out of the passionate debates surrounding the income and sales taxes. About 23% of state and local tax revenue comes from general sales taxes in the US, roughly equal to income taxes, and if you include selective sales taxes it’s slightly larger than the property tax share.

But there’s a problem with sales tax. The sales tax “base,” basically the extent of economic activity that the base covers, has been shrinking. A lot. As Jared Walczak has recently written, in just the past 20 years the “breadth” of the sales tax (how much of the potential base it covers) has fallen from about 50% to 30%.

As Walczak also notes, there are seven or so broadly agreed on principles of sales taxes, but I would say there are two primary ones (the first two on his list):

- An ideal sales tax is imposed on all final consumption, both goods and services.

- An ideal sales tax exempts all intermediate transactions (business inputs) to avoid tax pyramiding.

But US states violate these two principles in various ways, leading to (oddly enough) a tax base that is simultaneously too narrow and too wide. Why is this?

First, let’s look at few examples. The variation across states is especially notable. Massachusetts has the narrowest sales tax base, covering only about 22% of potential tax revenue (that’s using total personal income as the potential base, which is an upper bound). In other words, with a very broad base, the Massachusetts sales tax rate could be roughly one-fifth of its current level and generate the same amount of revenue. And since the deadweight loss increases roughly with the square of the tax rate, the deadweight loss from the sales tax in Massachusetts is twenty-five times higher than it could be with a broad bases and offsetting lower rate.

On the opposite end of the spectrum is Hawaii, where sales tax collections are 119% of the tax base. Huh? How can it be more than 119%? Simple: Hawaii violates principle #2 above, and taxes many intermediate business transactions (having a lot of tourism helps too). In fact, most states with a seemingly broad sales tax base partially achieving it by taxing many business inputs (the Dakotas and New Mexico fall into this group). The only state with a sales tax covering more than 50% of the potential base without resorting to taxing a lot of business inputs is Nevada (and separately they also have a gross receipts tax, one of the more inefficient taxes that seems kinda like a sales tax, but isn’t).

So what are the ways in which principle #1 is violated? States have large areas of consumption that are exempt from the sales tax, but I think they can be lumped into two areas:

- Broad categories of exemption, such as personal services, which often have never been included in the base

- Narrow goods that are exempted, such as groceries, which for most states were carved out by a specific piece of legislation

Both of these errors move a state from an ideal sales tax, but we should treat them differently. The exemption for personal services is long-standing; very few state ever broadly taxed services, and some states that tried, such as Florida in 1987, very quickly backtracked. Some states have slowly started to bring certain services into the sales tax base, but no state broadly taxes services.

Why not? Because taxing new things makes people mad. And not just anybody: specific people. Specific businesses. Industries which are already organized into lobbies. In a flip of the usual public choice mantra: concentrated costs, diffuse benefits. Moreover, there often are no benefits explicitly spelled out, such as lowering the overall rate. It’s often purely new tax revenue. Contrast this with New Zealand, who in 2010 increased their value-added tax in exchange for lowering their income tax.

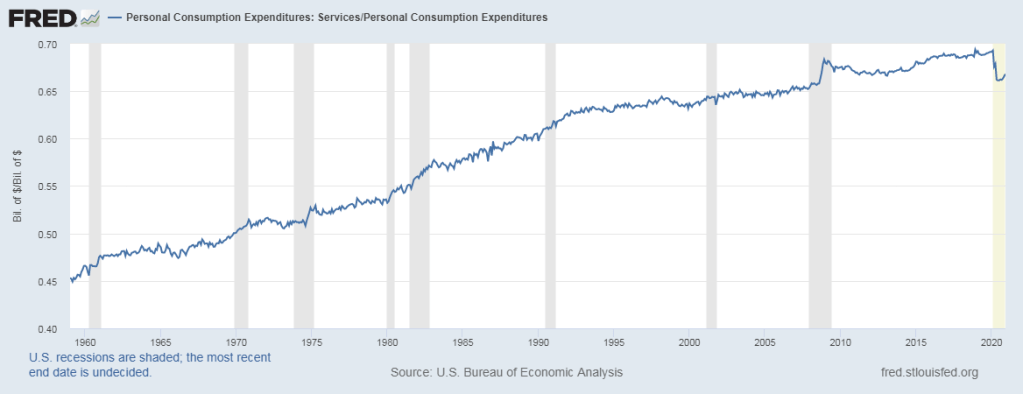

The problem with the exemption for services has been compounded over the years by the changing structure of the economy. Personal services were just 45% of personal consumption in 1959, but rose to 69% in 2020 (before the pandemic). This means that most states are excluding over 2/3 of their potential sales tax base!

Finally, let me briefly mention specific exemptions to the sales tax. The biggest example is groceries. Almost every state exempts groceries, taxes them at a lower rate, or provides a credit for the purchase of groceries: only South Dakota, Alabama, and Mississippi fully tax groceries with no offsetting credit. This seems like a good idea, since food is a necessity. It’s also very politically popular!

So what’s the problem? I have written about this issue before, so I won’t go into great detail here. But the short version is: this is a very costly way to achieve a certain goal, such as making food more affordable for poor citizens. But more importantly, I think it’s a bad idea because it chips away at the principle of a broad sales tax base. And it does so in a very big way: grocery purchases are over 20% of spending on goods.

Does the retail sales tax have a future? I think it does! States are always looking for more revenue. The recent experience of incorporating internet sales into the tax base is a good example. But these changes will always be politically unpopular unless they can be paired with some offsetting benefit for consumers, such as lowering other taxes or providing some clear new government service (rather than just incremental increases in spendong on existing government services).