You’ve probably seen the headlines. Corn prices are double what they were a year ago. Lumber prices are triple. You can find all kinds of other scary examples. Is runaway inflation just around the corner? Is it already here?

And yet, measures of prices that consumers pay are much more stable. The most widely tracked measure, the CPI-U, is up 4.2% over the past year. That’s through April — and keep in mind that it’s starting from a low base since March-May 2020 saw falling prices). The Personal Consumption Expenditures index, often preferred by economists, is up just 2.3% (though that’s only through March).

So what gives? Do these consumer measures understate inflation in some way? Or is the increase in commodity prices telling us that consumer prices will increase soon?

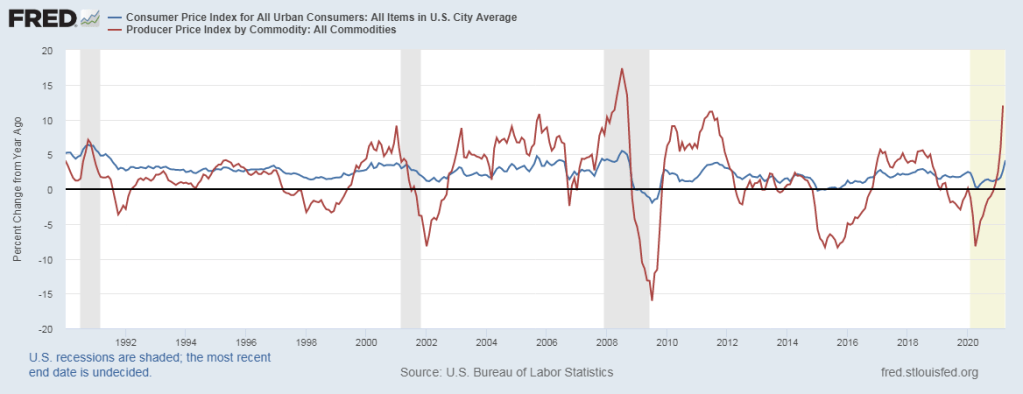

Let’s take that second question first. Do higher commodity prices necessarily lead to higher consumer prices? The answer is a clear no. First, we can see that in the data. The producer price index for all commodities (such as corn and lumber) is up 12% over the year (through March, with April data coming out tomorrow). That’s a big increase. But as the chart below suggests, that probably will not lead to 12% increases in consumer prices. It probably won’t even lead to a 5% increase in consumer prices.

Notice two things about this chart. First, commodity prices (the red line) are much more volatile than consumer prices, both on the upside and downside. Second, there really isn’t much of a lag, if any. The direction of change is similar in both indexes, almost to the month. When producer commodity prices go up, consumer prices also go up, that very same month, but not by the same amount. So all of that 12% increase in producer prices is probably already reflected in consumer prices.

Why might this be? Simple supply and demand analysis (hello Econ 101 critics!) can tell us why.

Recall that when any cost for the seller increases in a simple supply and demand model — whether that be the cost of labor, raw materials, or taxes — the market price of the good does indeed increase but not by the full increase in cost. Why? Most importantly, because demand curves slope downward. Businesses would love to pass all those costs along to consumers, but they find that as they increase prices consumers purchase less of the good. Also important: product markets are generally pretty competitive, so businesses must consider how much their competitors are increasing prices as well.

Putting these two together — downward-sloping demand curves and competitive product markets — we see that businesses are only partially able to pass along increased costs to consumers. How much depends — as usual! — on the relative elasticities. Businesses also don’t like changing their menu prices a lot, at least in the short term. The price of beef fluctuates a lot every month, but McDonald’s generally doesn’t change the price of hamburgers every month. Some of this is “menu costs,” but even with digital menus today they still like to keep prices pretty stable. Consumers probably like that consistency, and they’ll only increase the price of burgers when there is a clear secular increase in beef prices.

And probably even more important: the price of beef isn’t really the main cost of a burger for McDonald’s. Labor costs are much more important. Ditto for lumber: it’s not the main cost of building a home. The workers framing the house are a bigger cost than the wood itself.

Finally, let’s return to the earlier question I posed: do standard measures of consumer prices understate the true increase in consumer prices? You can find lots of people on the internet claiming this. You can probably find lots of people at the grocery store or local diner claiming this, if you ask them (you usually don’t have to ask people on the internet, they will just tell you).

But ask an economist, and they will tell you the opposite: measures like the CPI-U probably overstate inflation. The Boskin Commission said the overstatement was about 1.1%. That was from the mid-1990s, but most economists would tell you that it’s still about right.

The BLS does make some adjustments to the raw data, including some adjustments based on the assumption that consumers substitute between goods when prices change. But economists would argue that these adjustments make sense.

Some critics of the CPI simply don’t understand this substitution process and wrongly believe it’s a trick to understate inflation. For example, one popular criticism is that when the price of steak goes up, consumers switch to buying hamburger. Consumers probably do this! But the critics charge that you are worse off if you have to eat hamburger when you wanted steak. Shouldn’t the CPI account for consumers being worse off, if it is trying to measure changes in the cost of living?

This common criticism is incorrect: the CPI does not assume that consumers substitute hamburger for steak! It’s just a minunderstanding. Substitutions are made within categories of goods. For example, if the price of some kinds of ground beef in Chicago go up, but others don’t for ground beef in Chicago, the index assumes some substitution between different kinds of ground beef. But not substitution between hamburger and steak.

You can find “inflation” indexes online that claim consumer price inflation has been running at 10% for years. A quick perusal of these websites indicate that they don’t understand the CPI and construct indexes in weird ways that are even less reflective of what consumers actually pay.

For example, the Chapwood Index (website currently down) has a page criticizing the CPI, but clearly doesn’t understand it. For example, it claims the CPI excludes taxes (it doesn’t) as well as food and energy prices. The “core” CPI does exclude food and energy, but only because these are more volatile (in the long run, the average increase is very similar to the overall CPI). The regular CPI-U that you see reported every month includes food and energy. Really, it does!

How does the Chapwood Index attempt to correct for the apparent deficiencies of the CPI? By creating a much worse index. The CPI is based on the prices of tens of thousands of goods. Chapwood? Just 500 goods. And the list of goods is pretty weird. Three types of steak? Lots of items related to beds and sleeping. Lots of pasta too. I’m not saying the CPI couldn’t be improved, but these internet indexes are not improvements.

OK, but given all that I have said, couldn’t inflation still be on the horizon? Couldn’t price increases be just around the corner? Yes, they could! But we don’t know. And the fact that lumber prices tripled over the past year tells us next to nothing about what lumber prices will do over the next month or the next year. If you think you know, you can get very rich. But future price movements are determined by future conditions of supply and demand, not past increases in prices. If anything, the high price of lumber right now is encouraging some producers to find more sources of lumber, which could be an indicator that prices will fall over the next year.

But maybe not. Price movements are really hard to predict.

Finally, I haven’t said anything about monetary inflation, that is, the increase in the supply of money. Ultimately, this is one of the main causes of long-run price inflation. Haven’t we seen a big increase in the money supply in the past year? Indeed we have. M2, one measure of the money supply, is up over 20% in the past year. And for the money supply, there likely is a lag before consumer prices will rise.

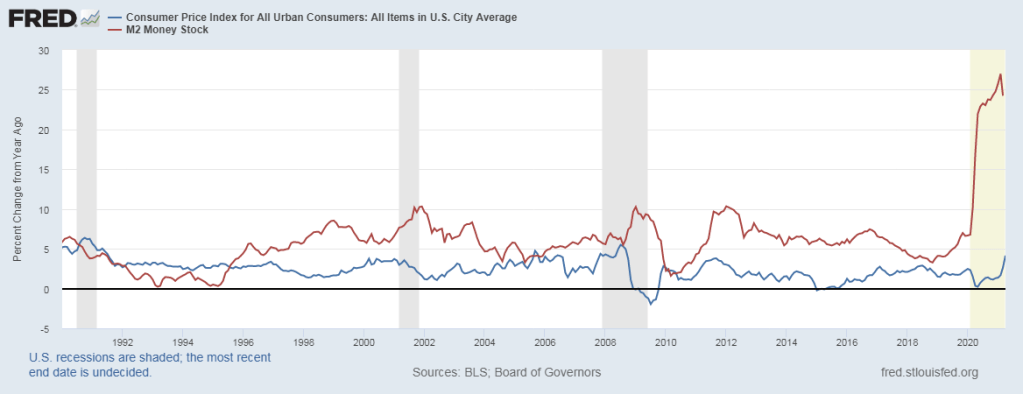

Consider the following chart

What we see here is that increases in M2 don’t necessarily lead to large increases in consumer prices. In recent years, we’ve seen increases in M2 of about 10% in 2001, 2009, and again in 2011-2012. But we never saw 10% consumer price inflation. Not even close. But what about a 20-25% increase in M2? Could that cause a lot more price inflation? It could. And that rate of money growth is even higher than we saw than in the high inflation 1970s and early 1980s.

I would just repeat that the future is unknown, especially with respect to price movements. We’ll keep watching these changes, but when watching them it is important to have a good understanding of what inflation is. And as always, if you think you know which direction prices will move in the future, you can get very rich!