As noted last week, I am happily receiving 9% interest in my new crypto account at BlockFi. How can they do that? The short answer is that BlockFi lends out my holdings to other parties, who pay somewhat more than 9% interest to BlockFi. This model is common to essentially all of the crypto brokers who pay out interest, but I will focus on BlockFi because (a) I have skin in the game there, and (b) they have been fairly transparent about their operations.

On the simplest level, this operates like a plain bank savings account does. A bank takes in funds from depositors, and (to oversimplify) lends those funds out to borrowers. The bank then pays to its depositors a portion of the interest it receives from its borrowers. Up until the last few years, this bank savings account model worked pretty well; a depositor might receive something like 2-3% interest on a savings account or certificate of deposit. More recently, short term rates have been near zero, so depositors get almost nothing in a bank savings account.

As noted earlier, BlockFi pays up to 4.5% interest on Bitcoin and 5% on Ethereum. These are leading, high volume coins that are widely used in decentralized finance (defi). Here is how BlockFi describes the parties to which it lends (mainly) Bitcoin:

Who Borrows Crypto?

BlockFi works with institutional counterparties for trading and lending cryptocurrency. These counterparties look to us to help them provide liquidity for their businesses. But who are some of these borrowers?

( 1 ) Traders and investment funds who see a fragmented marketplace and discover arbitrage trading opportunities. Arbitrageurs need to borrow crypto in order to close mispricing between exchanges or dispersed markets. Similarly, margin traders need to borrow in order to execute their trading strategies. This is a simple example, but it demonstrates how arbitrage and margin trading activities facilitate price discovery, which is an essential component of developed markets.

( 2 ) Over the counter (OTC) market makers make money by connecting buyers and sellers who do not want to transact over public exchanges. OTC desks need to keep inventory on-hand to meet their client demand. Owning crypto outright is capital intensive and comes with the attendant risks of price fluctuations. Instead, they may prefer to borrow inventory in order to facilitate transactions. Liquidity is another essential component to healthy markets.

( 3 ) Businesses that require an inventory of crypto to provide liquidity to clients. This bucket includes companies like crypto ATMs. These businesses also need to be able to support withdrawals while keeping the vast majority of their crypto assets in cold storage. The liquidity we provide them helps with these basic and important functions.

A key piece of this lending is to require that the counterparty post adequate collateral for the loans. This is somewhat similar to a bank lending you money to buy a house, with the house as collateral for your loan. If you lose your job and cannot pay back the loan, the bank has the right to sell your house to recovery its money. Similarly, BlockFi wants to ensure that if something goes sour with their loan of your Bitcoin, they can get their funds back and make your account whole. Obviously, BlockFi customers like me are relying on BlockFi to manage this properly and to minimize lending losses. BlockFi goes on to reassure us:

The BlockFi Team can draw on over 30 years of combined traditional finance and banking experience to create a robust on-boarding and credit risk underwriting process for institutional counterparties. The results of our underwriting help us assess our counterparty’s credit profile and enables us to make informed decisions on pricing, deal terms, and counterparty borrowing limits. BlockFi’s goal is to safeguard client funds by working with a diversified group of creditworthy counterparties. Every deal we make is monitored 24/7 by our automated risk management system, which has the ability to automatically issue margin calls to ensure the health of the trade.

Besides loaning to big institutional counterparties, BlockFi lets its users borrow dollars (or dollar-based stablecoins) using the users’ Bitcoin or Ethereum as collateral.

Alex Moskov at CoinCentral interviewed BlockFi, asking questions on the safety of these crypto loans:

We asked the BlockFi team some doomsday questions:

What happens if BlockFi gets hacked?: “Gemini is BlockFi’s primary custodian and BlockFi doesn’t hold private keys directly. Gemini keeps the vast majority of its assets in cold storage and is insured by Aon. Gemini is a licensed custodian and regulated by the NYDFS. They recently received SOC2 Type 1compliance audit from Deloitte for their custody solution. We encourage users to read more about Gemini’s security. “

What happens if a user account is compromised?: “Since inception, BlockFi has not lost any customer funds. In the event that a user’s account is compromised, which our security protocols have caught in the past, we freeze the individual’s account for one week. Then, we conduct a Videoconference with the affected individual to verify their identity. We can then change their email address and password, so they can regain control of their account.”

What happens if suddenly everyone defaults on their cryptocurrency loans?: “When we lend crypto assets to generate yield, we have an extremely thorough risk management and credit analysis process. We only primarily lend to large, well-capitalized, institutional borrowers, or to counter-parties willing to post collateral and provide the ability to margin call them on a 24/7 basis.”

“What that means is, if we are lending $1M worth of BTC to Firm XYZ, Firm XYZ collateralizes the loan (typically ~120%) by giving us ~$1.2M USD. If the loan were to then enter margin call and the borrower was unable to provide additional collateral (default), we would use their USD collateral to buy crypto.”

“We have actively lent since January of 2018, including throughout multiple periods of high volatility, without any losses across our entire lending portfolio. BlockFi is bound by NDA’s to discuss terms of specific borrowers/rates.”

Whew, I feel better now. But actually, I think that most of the above applies to loans of Bitcoin and Ethereum. Their dollar value can fluctuate widely. More details on this Bitcoin-based lending are here.

My specific interest, however, is in the stablecoins like Coinbase USDC and Gemini GUSD. Their value is pegged 1:1 to the U.S. dollar. As such, there is less demand to borrow these for fancy arbitrage plays.

Here is BlockFi’s reply to a query on the high interest rate (currently 9%) offered on USDC and GUSD:

“We are able to use stablecoin deposits to fund our consumer loans (average APR is ~10-13%) so we can afford to pay higher interest to GUSD / Stablecoin depositors.”

That got me a little concerned. Instead of lending my precious funds to “trusted institutional counterparties” like they do with Bitcoin, BlockFi is apparently lending my stablecoin (or the dollars it represents) to lowly personal consumers. And at what seem like pretty punishing rates (10-13%). I would never willingly borrow money at those rates. I’m not sure, but I get the impression that these loans are not collateralized. BlockFi did not disclose the actual channels by which it funds consumer loans. It’s possible that they partner with some established loan provider, and just provide funding for the consumer-facing partner.

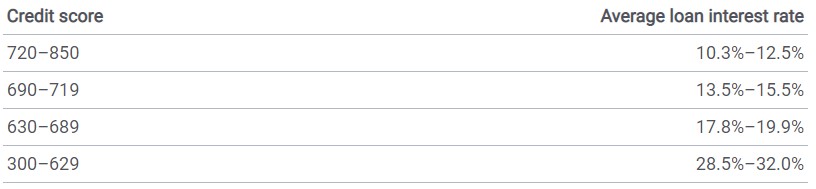

Are these high rates a red flag for lending to seedy, high-risk consumers? Well, not as much as I thought. It turns out the rates on generic, unsecured personal loans are just plain high. Here is a table from Holly Johnson at bankrate.com, showing typical loan rates for various credit scores:

The average credit card charges about 16% interest, so folks with good credit ratings are incentivized to seek alternative sources for personal loans, such as those provided from BlockFi. The rates charged by BlockFi on its consumer loans (10-13%) correspond to the higher tier of credit scores, so I guess my money is pretty safe being loaned out here.

UPDATE MAY, 2022 – – With the overall deep sag of crypto currencies, and the crash/burn of the Terra/Luna coins, and more intrusive government regulations, there may be less market activity with crypto lending. The interest rates I see for stablecoins like USDC have dropped from around 9% to around 6.5%. Plus, BlockFi got hounded by the feds to the point of paying a big fine and being prohibited from accepting more funds. The main interest-paying crypto player still standing that I am aware of is Gemini. Gemini is very conscientious about audits and has always tried to work closely with regulators. It is offering about 6.5% interest on stablecoins (which is still way better than money markets or CDs), and a measly 1-1.25% on Bitcoin and Ethereum.