Released this April, but I just heard about it today. Researchers did the painstaking work of going through all 50 states to determine which steps must be taken in each state before new regulations can take effect. For instance, it turns out half of states require economic analysis for new regulations, and half don’t. The paper is here: https://www.mercatus.org/publications/regulation/50-state-review-regulatory-procedures

Author: James Bailey

Two Types of News: Elections vs Crashes

Some events are like elections: it was obvious that some big political news would break on Election Day, we just had to wait to find out what exactly would happen. Others are like market crashes: you might know in principle they’re a thing that can happen, but you don’t really expect any particular day to be the day one happens, so they seem to come out of the blue. As it turns out, for one of the largest crypto exchanges the day of the crash also happened to be Election Day.

FTX.com is facing a bank run sparked by competitor Binance tanking the price of the token that backed some of their assets. Customers are having issues withdrawing their money, Binance has withdrawn its offer to bail out FTX by taking them over, and bankruptcy seems likely. Supposedly this doesn’t affect Americans using FTX US, but I’d be nervous about any funds I had there, or indeed with funds in any centralized crypto exchange or stablecoin (Tether and even USDC seem to be having issues holding their pegs). All this was especially shocking because many considered FTX founder Sam Bankman-Fried one of the most trustworthy people in the often sketchy world of crypto. He was always meeting with US regulators and lawmakers, and seems not to be motivated by greed; he had already begun to give away his fortune at scale.

After any surprising event like this, some people claim it was actually obvious and they saw it coming (despite usually never having said so beforehand), while others start looking back for warning signs they missed. The most interesting one is something that shocked me when I first heard it March, but I never considered the risk it implied for FTX until the crash:

Going forward, red flags to watch out for seem to be topping a list of youngest billionaires (as Elizabeth Holmes also did) and buying naming rights to a stadium.

In contrast to this crash, the election happened right when we all expected, and at least largely how I expected. Like markets, I underestimated Democrats a bit; polls overall were impressively accurate this year, though they of course missed on some particular races. Votes are still being counted, and as of now we don’t even know for sure which party will control Congress (PredictIt currently gives Democrats a 90% chance in the Senate and a 20% chance in the House). But here are some early attempts to assess forecast accuracy. As I said, some polls were quite good:

Some polls weren’t so good, which means its important to weight better pollsters more heavily when you aggregate them. Some attempts at that were also quite good:

Oddly, some no money (Metaculus) / play money (Manifold Markets) forecasting sites seem to have done better than the real-money prediction sites:

A Dragonfly’s View of Election Day 2022

This is my last post before the US midterm elections on Tuesday, so I’ll leave you with a prediction for what’s coming.

Who is the best predictor of elections? Nate Silver at FiveThirtyEight has had a pretty good run since 2008 using weighted polls. Ray Fair, an economics professor at Yale has a venerable and well-credentialed model based on fundamentals. I typically favor prediction markets, because they incorporate a wide range of views weighted by how willing people are to put their money where their mouth is, and traders are able to incorporate other sources of information (including predictors like FiveThirtyEight). But which prediction market should we trust? There are now many large prediction markets, and the odds often differ substantially between them.

When there are many reasonable ways of answering a question or looking at a problem, it can be hard to choose which is best. Often the best answer is not to choose- instead, take all the reasonable answers and average them. Dan Gardner and Philip Tetlock call this approach Dragonfly Eye forecasting, since dragonfly’s eyes see through many lenses. So what does the dragonfly see here?

Lets start with the US House, since everyone covers it.

- FiveThirtyEight’s latest forecast shows that Republicans have an 85% chance of taking the House; it shows a range of possible outcomes, but on average predicts that Republicans win the popular vote by 4.3% and take 231 House seats (substantially over the 218 needed for a majority)

- The Fair Model predicts that Democrats will win 46.6% of the two-party vote share (leaving Republicans with 53.4%). This has Republicans winning the popular vote by 6.8%, a moderately bigger margin than FiveThirtyEight. The reasoning is interesting; the economy is roughly neutral since “the negative inflation effect almost exactly offsets the positive output effect”, so this is mainly from the typical negative effect of having an incumbent party in the White House.

- Prediction markets: PredictIt currently gives Republicans a 90% chance to take the House. Polymarket gives them 87%. Insight Prediction also gives them 87%. Kalshi doesn’t have a standard market on this, but their contest (free to enter, 100k prize) predicts 232 Republican seats.

Its a bit tricky to average all these since they don’t all report on the same outcome in the same way. But the overall picture is clear: Republicans are likely to do well in the House, with an ~87% chance to win a majority, expected to win the popular vote by ~5.55% and take ~232 seats.

The Senate is closer to a coin flip and harder to evaluate.

- FiveThirtyEight gives Republicans a 53% chance to win a majority (51+ seats for them; Democrats effectively win if the Senate stays 50-50 since a Democratic Vice President breaks ties for at least 2 more years). The most likely seat counts are 50-50 or 51-49, but confidence intervals are pretty wide and 54-46 either direction isn’t ruled out.

- The Fair Model doesn’t make Senate predictions, only House and Presidential predictions.

- Prediction markets: PredictIt gives Republicans a 70% chance to win a Senate majority, probably with 52-54 seats. PolyMarket gives Republicans a 65% chance, as does Insight Prediction. Kalshi predicts 53 Republican seats.

Overall we see a much higher variance of predictions in the Senate; a 17pp gap between the highest (70%) and lowest (53%) estimates of Republican chances, vs just a 5pp gap for the House (90% to 85%). This shows up with the seat counts too; everyone agrees there’s a substantial chance Republicans lose the Senate, but if they do win, it will probably be by more than one seat. The average estimate is ~52 Republican seats. FiveThirtyEight and PredictIt agree that the closest Senate races will be Georgia, Pennsylvania, Arizona, Nevada, and New Hampshire (though they rank order them differently), so those are the races to watch.

Forecasts for governors aren’t as comprehensive, but FiveThirtyEight predicts we’ll get about 28 Republican (22 Democratic) governors, while PredictIt expects 31+ Republicans; I’ll split the difference at 30. Everyone agrees that Oregon is surprisingly competitive because of an independent drawing Democratic votes. The biggest difference I see is on New York, where PredictIt gives Republican challenger Lee Zeldin a real chance (26%) but FiveThirtyEight doesn’t (3%).

Overall forecast: moderate red wave, Republicans take the House and most governorships, probably the Senate too. But if they lose anything it is almost certainly the Senate.

These forecasts seem about right to me. Democrats are weighed down by an unpopular (-11) President and the highest inflation in 40 years. This would lead to a huge red wave, but Republicans have their own weaknesses; an unpopular former President lurking in the background, and the Supreme Court making a big unpopular change voters blame them for. This shrinks the red wave, but I don’t think its enough to eliminate it. The effect of Roe repeal is fading with time, and the unpopular Biden is more salient than the unpopular Trump; Biden is the one in office and is more prominent in media coverage. Facebook and recently-acquired Twitter may be doing Republicans a favor by keeping Trump banned through Election day. But if he drags Republicans down anywhere, it will be the Senate, where candidate quality (not just party affiliation) is crucial and his endorsements pushed some weak/weird/extreme candidates through primaries. We’ll also see this “extremist” Trump effect (abetted by cynical Democratic donations to extreme-right candidates) dragging down Republicans in some key governor’s races like Pennsylvania, where Democrats are now 90/10 favorites..

Bounce Houses are Surprisingly Cheap

Last year was the first time I saw a family that owned their own bounce house and just set it up in their living room. At the time I thought, what a lucky rich kid, that must cost at least a thousand dollars. But my wife looked into it and found out that bounce houses are surprisingly cheap these days. She got our kids this one last Christmas, its currently going for $234 on Amazon:

The kids love it and its still going strong ten months later, despite substantial use from kids and the presence of two sharp-clawed cats. It was certainly a bigger hit than the other major gift we tried last Christmas- telescopes are surprisingly hard to use.

Should Virologists Regulate Themselves?

Last Friday a group of researchers mostly from Boston University posted a paper which revealed they had created a new chimeric coronavirus and used it to infect mice.

We generated chimeric recombinant SARS-CoV-2 encoding the S gene of Omicron in the backbone of an ancestral SARS-CoV-2 isolate and compared this virus with the naturally circulating Omicron variant. The Omicron S-bearing virus robustly escapes vaccine-induced humoral immunity, mainly due to mutations in the receptor-binding motif (RBM), yet unlike naturally occurring Omicron, efficiently replicates in cell lines and primary-like distal lung cells. In K18-hACE2 mice, while Omicron causes mild, non-fatal infection, the Omicron S-carrying virus inflicts severe disease with a mortality rate of 80%.

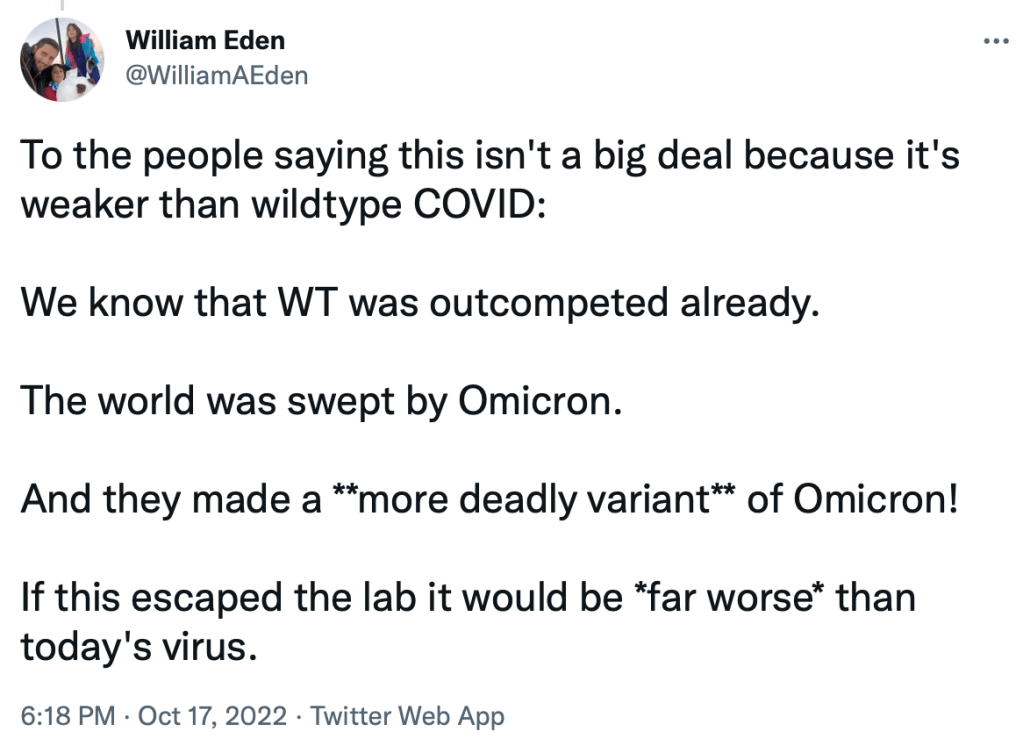

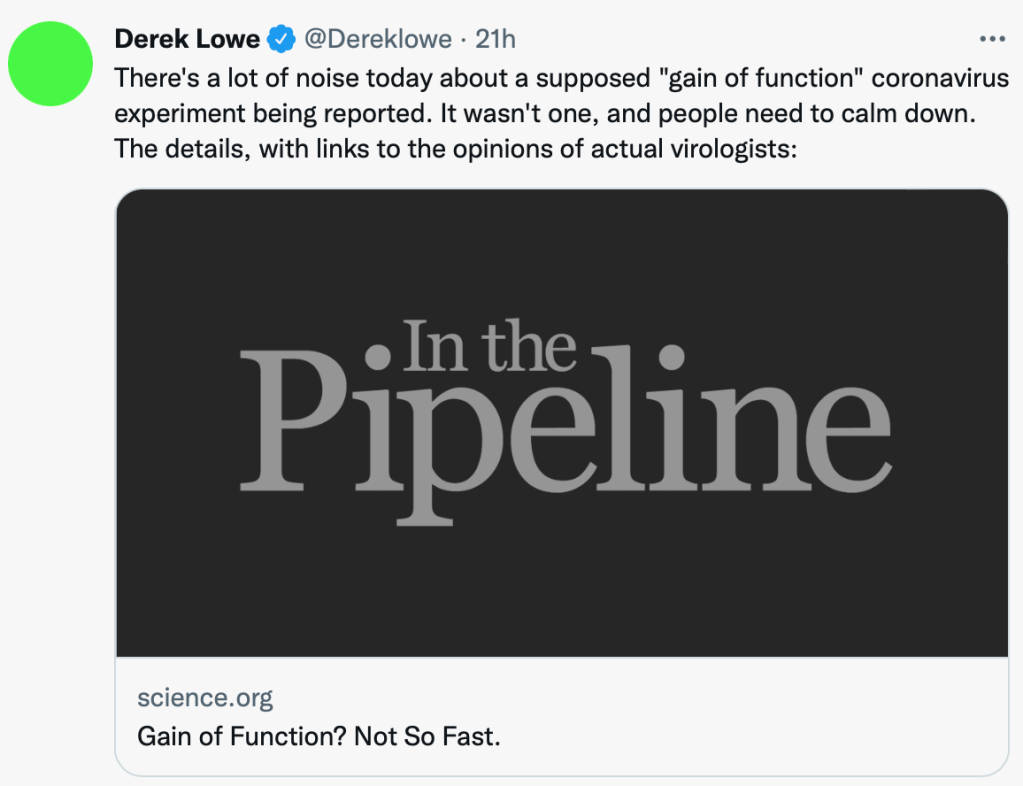

Many people who heard about this expressed concern that the risk of creating more contagious and/or deadly versions of Covid that could escape from a lab outweigh any potential benefits of what we could learn from this research.

Several researchers have responded to these concerns with variants of “trust virologists to weigh the risks here, they know more than you.”

Here’s the thing: the virologists do know the risks better than the public or potential regulators- but they also have different incentives. What I want to point out today is that virology isn’t special; this is true of just about every field. A nuclear engineer knows much more about what’s happening at their plant than voters do, or distant bureaucrats at the Nuclear Regulatory Commission. Should we leave it to the engineers on site to decide how much risk to take? Should federal regulators leave it to the financial experts at Bear Sterns and AIG to decide how much risk they can take?

To some extent I actually sympathize with these critiques; industry practitioners really do tend to have the best information, and voters often push regulatory agencies to be insanely risk-averse. With any profession this information problem is a reason to regulate less than you otherwise would, and/or pay to hire expert regulators.

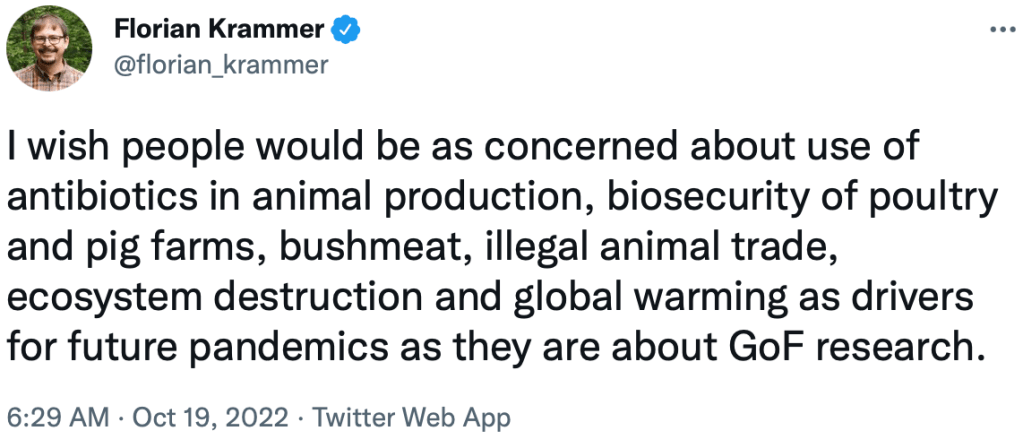

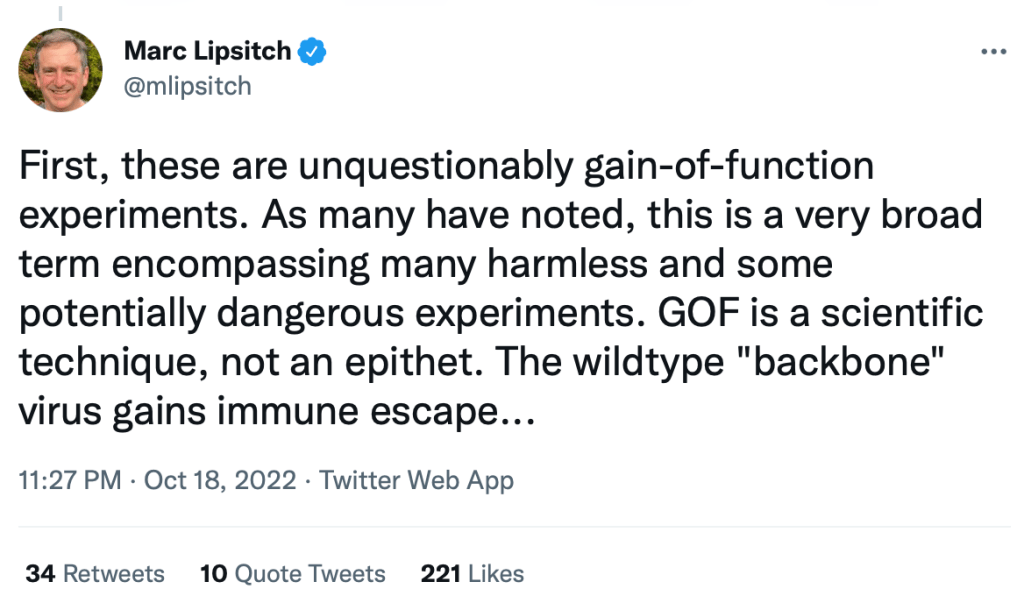

But externalities are real- the practitioners who have the best information use it to promote their own interests, which tend to differ from the interests of the public. In finance this means moral hazard at best and fraud at worst (who are you to say Bernie Madoff is a fraud? You know more about finance than him?). In medicine it means doctors who get paid more for doing more; they gave the guy who invented lobotomies a Nobel Prize in Medicine. In research that involves creating new viruses, researchers get the private benefits of prestige publications for themselves, but the increased pandemic risk is shared with the whole world. In this case its not just outsiders who are concerned, some subject-matter experts are too (and not just “usual suspects” Alina Chan and Richard Ebright; see also Marc Lipsitch).

The main current check on research like this is supposed to be Institutional Review Boards. The chimeric Covid paper notes “All procedures were performed in a biosafety level 3 (BSL3) facility at the National Emerging Infectious Diseases Laboratories of the Boston University using biosafety protocols approved by the institutional biosafety committee (IBC)”. But there are many problems with this approach. The IRB is run by employees of the same institution as the researcher, the institution that also claims a disproportionate share of the benefits of the research.

IRBs are also incredibly opaque. The paper claims it was approved by Boston University’s institutional biosafety committee, but these committees don’t maintain public lists of approved projects; I e-mailed them Sunday to ask if they actually approved this project and they have yet to respond. There is also no public list of the members of these committees, although in BU’s case you can get a good idea of who they are by reading the meeting minutes. This chimeric Covid proposal appears to have been reviewed as the second proposal of their January 2022 meeting, reviewed by Robert Davey and Shannon Benjamin and approved by a 16-0 vote of the committee. During the January meeting the committee approved all 6 projects they considered unanimously, after hearing 6 reports of lab workers at BU being exposed to lab pathogens in the previous month, e.g.:

MD/PhD student reported experiencing low grade temperatures and other symptoms after he accidentally injured his thumb percutaneously on 12-6-21 while cleaning forceps that he had used to remove infected lungs from mice injected with NL63 virus

IRBs are supposed to protect research subjects from harm, but in practice largely serve to protect their institutions from lawsuits and PR disasters (part of why they’re often too strict). The fact that this did get institutional approval provides one silver lining here; if this chimeric Covid ever did escape and cause an outbreak, those infected by it could potentially sue for damages not only the individual researchers, but Boston University and its $3.4 billion endowment. Being able to internalize externalities in this way is one of many good reasons to be testing those infected with Covid to see what variant they have.

I think we should at least consider stronger national regulations against research like this, rather than leaving each decision to local institutional review boards (ask any researcher how much they trust IRBs). At the very least we should stop subsidizing it; NIH claims they don’t fund “gain of function” research like this, but the researchers who made a new version of Covid conclude their paper:

This work was supported by Boston University startup funds (to MS and FD), National Institutes of Health, NIAID grants R01 AI159945 (to SB and MS) and R37 AI087846 (to MUG), NIH SIG grants S10- OD026983 and SS10-OD030269 (to NAC)

The Quotable Walter Russell Mead

I listen to a lot of podcasts, but many are forgettable, and even the good ones can be hard to share, since they get their point across slowly and gradually. But on the latest Conversations with Tyler, I found foreign policy thinker Walter Russell Mead to be eminently quotable. Some highlights:

On Germany:

Kennan’s goal for Germany was to have a united, neutral, disarmed Germany at the heart of Europe. In some ways, [laughs] Kennan’s goal looks, maybe, closer than ever.

China’s development plan, much more than its Taiwan policy or its human rights, is a gun pointed at the head of German business

On America:

Over the last 40 years, there’s been an enormous increase in the number of PhD grads engaged in the formation of American foreign policy. There’s also been an extraordinary decline in the effectiveness of American foreign policy. We really ought to take that to heart.

The American academy is actually a terrible place for coming to understand how world politics works.

One of the teachers at Groton used to take aside some of the boys — it was an all-boys school at the time — and explain to them how their family fortune was made. He might say, “Well, George, we’ve been reading a lot about war profiteers in World War I. You need to know that your grandfather . . .”

I think neoconservatism reflected a sense of people who’ve never been wrong and never been beaten, at least in their own minds

On the Middle East:

In the Arab world, the Middle East, Islamism, and jihad — just call it jihadi ideology more broadly — is seen to have failed. Like socialism, like Arab nationalism, it’s one more in a long list of failed ideological movements. Not that there still aren’t terrorists, or for that matter, Arab socialists, but it’s not the same.

Nobody really thought, in 2008, as George W. Bush left office, that you could possibly mess up the Middle East worse than the Bush administration. But President Obama proved that that was wrong and that you could actually take the Middle East at the end of 2008 and make it almost infinitely worse, both for American interests and for the safety and happiness of the people in the region

On Ukraine:

The message, actually the totality of the message that we sent to Putin [through the intelligence we released] is, “You are going to win if you do this”.

I read Mead’s book Special Providence in college and enjoyed it then, but have’t kept up with his work since. The book’s title comes from another great quote, this time attributed to Otto von Bismarck:

God has a special providence for fools, drunks and the United States of America.

Svante Pääbo: The Surprising Science behind Who We Are and How We Got Here

Its Nobel Prize season- the economics prize will be announced Monday, while most prizes are announced this week. My favorite so far is the Medicine prize being awarded to Svante Pääbo “for his discoveries concerning the genomes of extinct hominins and human evolution”. He figured out how to sequence DNA from Neanderthal remains despite the fact that they were 40,000 years old.

As recently as 2010 it was controversial to suggest that Neanderthals might have mixed with humans, until Pääbo’s DNA definitively settled the debate, showing that “Neanderthals and Homo sapiens interbred during their millennia of coexistence. In modern day humans with European or Asian descent, approximately 1-4% of the genome originates from the Neanderthals”

While the Neanderthal genome settled an existing controversy, Pääbo’s other big discovery came entirely unlooked for. The Nobel Foundation explains:

In 2008, a 40,000-year-old fragment from a finger bone was discovered in the Denisova cave in the southern part of Siberia. The bone contained exceptionally well-preserved DNA, which Pääbo’s team sequenced. The results caused a sensation: the DNA sequence was unique when compared to all known sequences from Neanderthals and present-day humans. Pääbo had discovered a previously unknown hominin, which was given the name Denisova. Comparisons with sequences from contemporary humans from different parts of the world showed that gene flow had also occurred between Denisova and Homo sapiens. This relationship was first seen in populations in Melanesia and other parts of South East Asia, where individuals carry up to 6% Denisova DNA.

Pääbo’s discoveries have generated new understanding of our evolutionary history. At the time when Homo sapiens migrated out of Africa, at least two extinct hominin populations inhabited Eurasia. Neanderthals lived in western Eurasia, whereas Denisovans populated the eastern parts of the continent. During the expansion of Homo sapiens outside Africa and their migration east, they not only encountered and interbred with Neanderthals, but also with Denisovans

The same techniques that enabled these discoveries have been applied much more widely throughout the field of Paleogenomics, which continues to rewrite what we thought we knew about history and pre-history. The field has been advancing so quickly over the last decade that its hard to keep up with it. I’ve found the best introduction to be David Reich’s Who We Are and How We Got Here, though again the field is moving so fast that a 2018 book is already a bit out of date. Razib Khan is always writing about the latest updates at Unsupervized Learning. If you haven’t kept up with this stuff since school, this post and diagram give a quick introduction to how much our understanding of human origins has recently changed:

Highlights from EA Global DC

I was in DC last weekend for the Effective Altruism Global conference. I met a lot of smart people who are going to have a huge impact on the world, and some who already are. I’ll share a few of my favorite highlights here, with the disclaimer that most quotes won’t be exact:

The mistake every do-gooder makes is coming to a country and thinking ‘I’m just here to help people, I’m not a political actor.’ Guess what? You are. What you do changes the balance of power, often toward the center

Chris Blattman

I’m funding the Yale spit test? The world doesn’t make sense [Yale, NIH, et c should be on it]… its like, if I won an academy award or NBA MVP, how screwed up would the world be?

Tyler Cowen, referring to Fast Grants

You should all be political independents, both parties are terrible. You should be voluntary social conservatives, behave like Mormons…. we need a marginal revolution toward the better parts of the Mormon / social conservative package

Tyler Cowen

Tyler later specified that the main things he meant by this were to marry young and not drink, though I don’t think he realized how common the latter already is:

As he often does, Tyler recommend that people travel more:

If I meet someone who’s been to 40 countries I tell them they should travel more, and to weirder places

Tyler Cowen

But when someone asked “How much travel is too much”, he came up with this limiting principle:

How much travel is too much travel? 10% after your significant other gets mad at you

Tyler Cowen

I asked Matt Yglesias how much of his policy influence comes just from writing things online, and how much from personal connections and being in DC. He said something like:

Personal connections matter a lot given how real people change their minds, but there’s also less of a dichotomy than you’d think. For instance, a WaPo column of mine was getting passed around the White House, but I wrote it because someone in the WH suggested the topic. Politicians often communicate with each other via the media, though I wish they wouldn’t. Just talk to each other, you work in the same building!

Matt Yglesias

His take on the changing media environment:

My tweets are more influential than my columns & substack, because they are read so much more & I’m followed by many journalists. Overall though now is a great time for specialists, obsessives and weirdos. Construction Physics is a great blog now but if he’d written it in 2003 people would just be like, WTF. On the other hand my [generalist] college blog did well in 2003 but if a college student wrote the same kind of things today people would say, who cares?

Matt Yglesias

Journalists are suspicious haters, that’s our function in society

Can’t remember if this was Matt Yglesias or Kelsey Piper

Tyler and Matt were both telling people that you can accomplish your goals more effectively by being more “normie” in some ways. This can be a bit of a sacrifice, but:

If you can give a kidney, you can learn to tie a tie, give a firm handshake, and look people in the eye

Matt Yglesias

I’m some combination of smart enough and arrogant enough that its normally rare for me to meet someone and think “oh, you’re smarter than I am”. But at EAG it was common; not just because of the ridiculous numbers of top-university degrees and real-world accomplishments, but the breadth and depth of the conversations, everything from mental math to number theory, AI to finance, to a surprisingly convincing pitch for the relevance of metaphysics for political theory.

It wasn’t a step up for everyone though; I talked to someone at a top hedge fund who said the people he worked with were “are the smartest, most dedicated people I’ve been around…. smarter than EAs, more able to execute than mathematicians at [top PhD program he was at]”. They work 12 hour days, actually working the whole time (no long lunch break, small talk with colleagues, reading social media on their computers)… but all in a ruthless, selfish, impressively successful quest to outsmart the market and make more money.

Overall it was a great time and helped me narrow down my plans for what to do with my time and brainpower post-tenure. If you’re interested there are more conferences ahead.

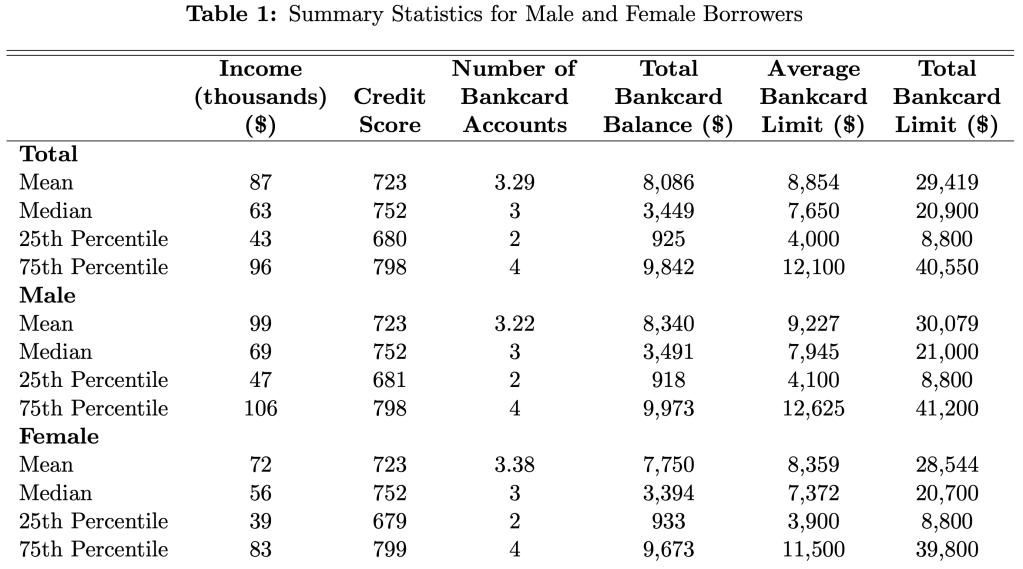

Credit Card Limits for Men and Women

Yesterday Federal Reserve researcher Nathan Blascak presented a paper at my Economics Seminar Series that was a surprise hit, with the audience staying over 40 minutes past the end to keep asking questions. So today I’ll share some highlights from the paper, “Decomposing Gender Differences in Bankcard Credit Limits”.

The challenge here is that its hard to get data that includes both gender and credit card limits (its illegal to use gender as a basis for allocating credit, so credit card companies don’t keep data on it, as they don’t want to be suspected of using it). The paper is original for managing to do so, by merging three different datasets. But even this merged data only lets them do this for a fairly specific subgroup- Americans who hold a mortgage solely in their name (not jointly with a spouse). Even this limited data, though, is quite illuminating.

Their headline result is that men have 4.5% higher credit limits than women. Women actually have slightly more credit cards (3.38 vs 3.22), but have lower limits on each card; summing up their total credit limit across all cards yields an average of $28,544 for women vs $30,079 for men.

Two of the big factors that determine limits, and so could cause this difference, are credit scores and income. The table above shows that men and women have remarkably similar credit scores, while men have higher incomes. Still, when the paper tries to predict credit limits, controlling for credit scores, incomes, and other observables explains only about 13% of the gender gap.

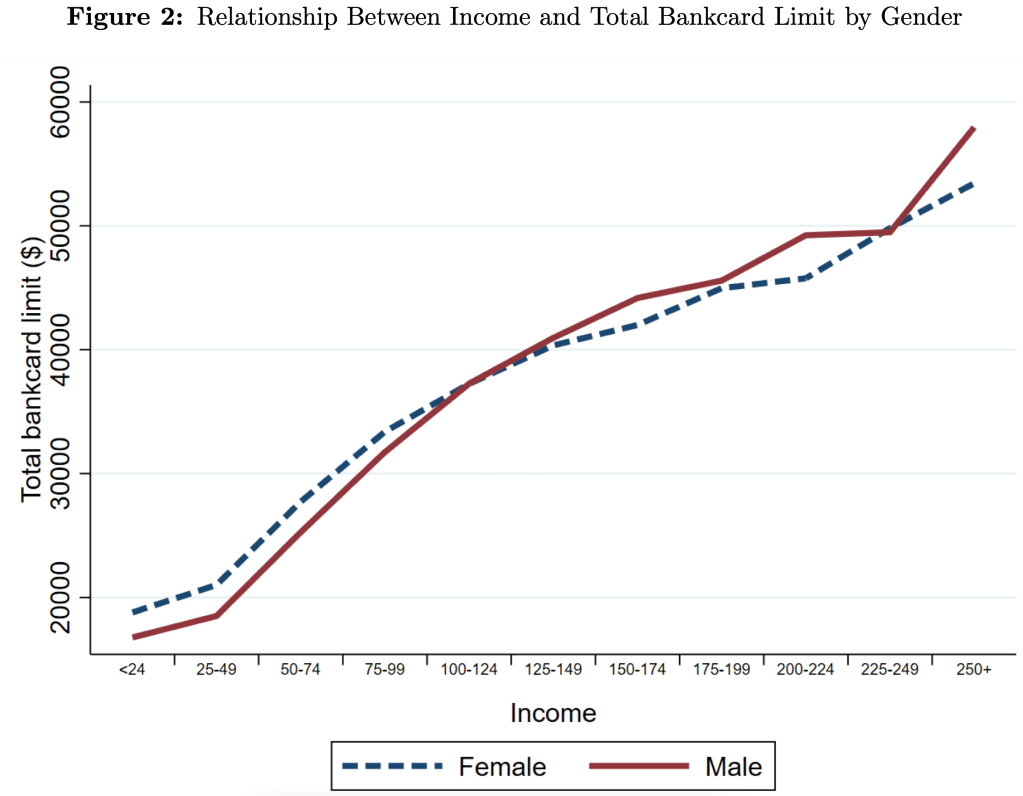

Men have 4.5% higher credit limits on average, but this difference varies a lot across the distribution. For credit scores, the gap is narrow in the middle but bigger at the extremes. For income, we see that men get higher limits at higher incomes, but women actually get higher limits at lower incomes- and not just “low incomes”, women do better all the way up to $100,000/yr:

The papers data covers 2006-2018, so they also show all sorts of interesting trends. The average number of credit cards held by men and women plunged after the 2008 recession and remains well below the peak. Total credit limits plunged too, though they were almost totally recovered by 2018.

There’s lots more in the paper, which is a great example of the value of descriptive work with new data. If anything I’d like to see the authors push even harder on the distribution angle. Its nice to see how limits vary across all incomes and credit scores, but why not show the full distribution of credit card limits by gender? My guess is that the 1st and 99th percentiles are very interesting places, because there’s all sorts of crazy behavior at the extremes. Finally, I wonder if higher limits are actually a good thing once you get beyond a relatively low amount- do you know of anyone who ever had a good reason to get their personal credit card balances over $20,000?

The Shrinking Allied Social Science Association

For many decades the Allied Social Science Association (ASSA) meetings, anchored by the American Economic Association, have been by far the world’s largest gathering of economists each year, typically attracting well over ten thousand. But the meetings went virtual-only for the past two years, and when they finally return in-person in 2023 they will likely be substantially diminished.

Some of this is due to potentially one-off factors; some people don’t want to travel to Louisiana because of its state laws, some still want to avoid large conferences because of Covid, others want to avoid the ASSA’s response to Covid:

All registrants will be required to be vaccinated against COVID-19 and to have received at least one booster to attend the meeting…. High-quality masks (i.e., KN-95 or better) will be required in all indoor conference spaces.

But the AEA made one big, apparently permanent change that means it could be a long time before we see a meeting as big as January 2020’s in San Diego- they gave up the job market. Prior to Covid the vast majority of first-round interviews to be a full-time US economics professor took place at ASSA. Naturally interviews moved online during Covid, but surprisingly the AEA has asked that they stay online, and in fact has specifically asked schools NOT to schedule interviews during ASSAs. This removes a huge source of demand for the meetings- the ~1200 new PhDs looking for their first jobs, the thousands of people there to recruit them (each hiring school typically sends 2-4 interviewers), and everyone trying to switch jobs. This was THE big thing that made AEAs special, that other conferences didn’t really have.

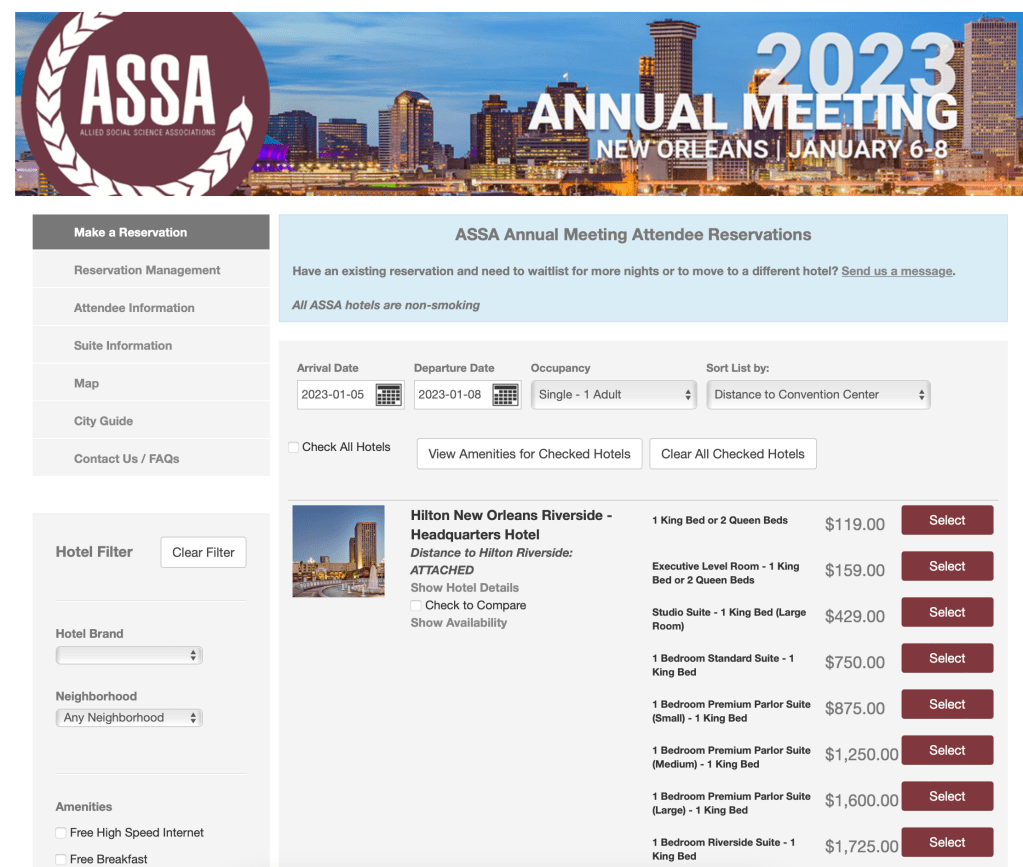

I’ll let everyone else debate whether this makes the job market better or worse; I’m agnostic there, but I’m sure it will shrink the conference. One silver lining to a smaller conference is that it is much easier to find a hotel room. Like usual I was waiting on the AEA website this Tuesday to book a hotel room on the first minute the AEA’s deeply discounted hotel blocks opened, because the good hotels tend to fill up near-instantly. But it appears this was unnecessary this year- two days later and even the headquarters hotel is still wide open:

I got the room I wanted at the Hotel Monteleone; I’ll be looking to grab a spot on the Carousel Bar, maybe see some of you there. I’ll present a poster at AEA, but mostly I’m just looking forward to spending real time in New Orleans for the first time since I moved away in 2017.

So I’m still looking forward even to a diminished AEA, but it does make me wonder- which other conferences will benefit most from AEA’s decline? I don’t know that anyone has put together the numbers for all the conferences enough to know what the 2nd-largest is, but my bet both for the 2nd-largest and most likely to benefit is the Southern Economic Association; I’ll be there too, in Ft. Lauderdale this November.